- Home

- »

- Electronic Devices

- »

-

Architectural Lighting Market Size & Share Report 2026-2033GVR Report cover

![Architectural Lighting Market (2026 - 2033)Report]()

Architectural Lighting Market (2026 - 2033)

Size, Share, & Trends Analysis Report By Component (Lamp Holders, Ballasts, Lamps, Trims), By Source (Incandescent Lights,Fluorescent Lights), By Application, By End Use, By Region, And Segment Forecasts

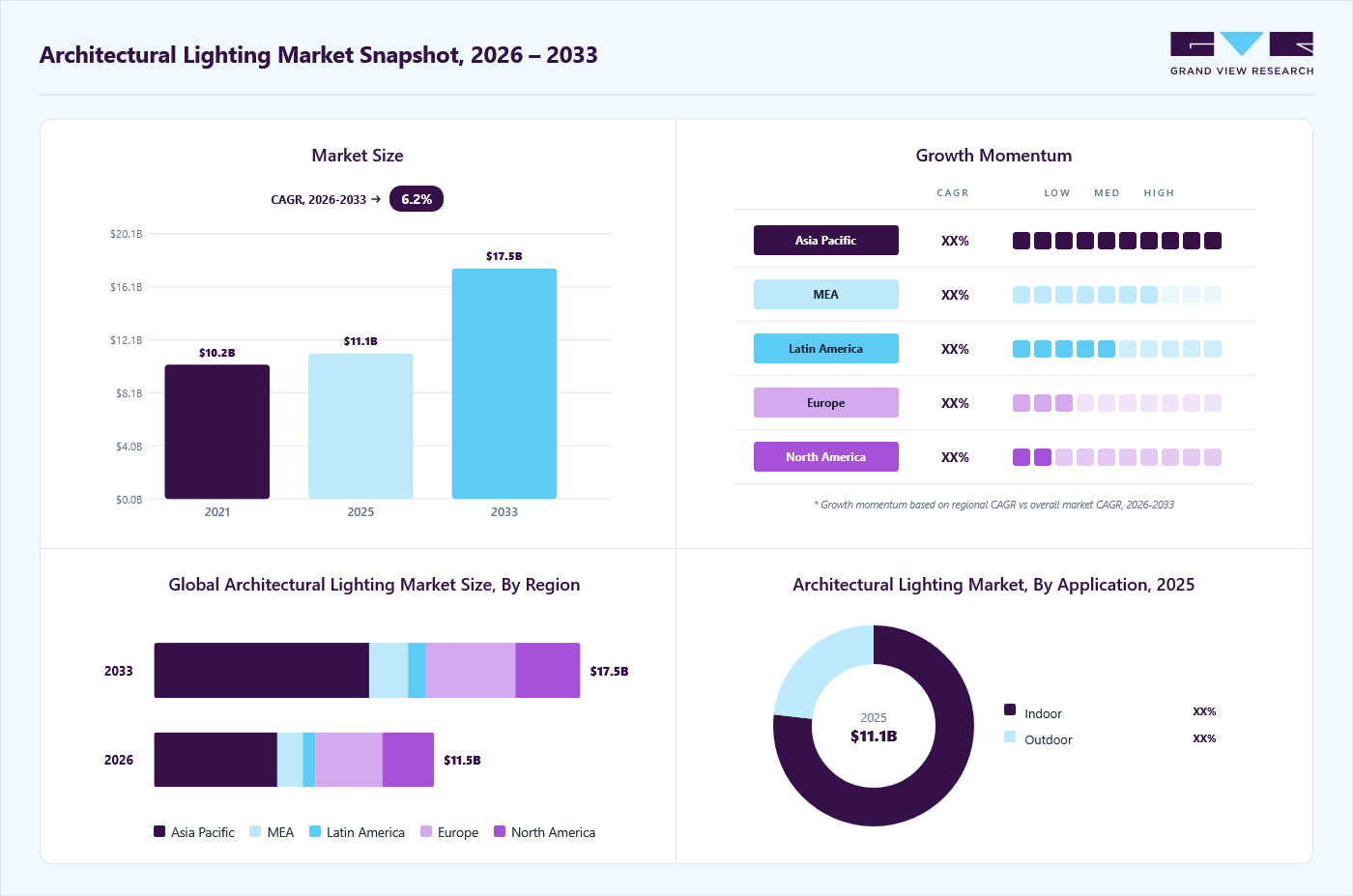

Market Size, 2025

$11.1BMarket Estimate, 2026

$11.5BMarket Forecast, 2033

$17.5BCAGR, 2026–2033

6.2%Architectural Lighting Market Summary

The global architectural lighting market size was valued at USD 11.1 billion in 2025 and is projected to grow from USD 11.5 billion in 2026 to USD 17.5 billion by 2033, at a CAGR of 6.2% from 2026 to 2033. Asia Pacific dominated with the largest revenue share of 43.2% in 2025, driven by the increasing legalization of cannabis for medical and recreational use. The adoption of LED technology has significantly driven growth in the architectural lighting industry due to its superior energy efficiency, longevity, and cost savings.

Key Market Trends & Insights

- By component: Ballasts held the largest revenue share of 18.2% in 2025.

- By source: LED held the largest market share of 29.4% in 2025.

- By application: Indoor held the largest market share of 76.8% in 2025.

- By end use: Commercial segment accounted for the largest market share of 50.9% in 2025

Regional Highlights

- Largest regional market: Asia Pacific (43.2% revenue share, 2025)

- By country: China held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 11.1 Billion

- Estimated market size in 2026: USD 11.5 Billion

- Projected market size by 2033: USD 17.5 Billion

- CAGR (2026-2033): 6.2%

LEDs consume less power, reducing energy costs and carbon footprints, aligning with global sustainability goals. Their longer lifespan minimizes maintenance costs, making them ideal for large-scale and long-term applications. Additionally, advancements in LED technology offer greater design flexibility, enabling creative lighting solutions for diverse architectural needs, from residential spaces to commercial and public infrastructure projects.The future of the architectural lighting market looks promising, driven by technological advancements and increasing demand for sustainable solutions. The integration of AI, IoT, and advanced control systems will lead to the proliferation of smart lighting in both residential and commercial spaces. Human-centric lighting will become a standard, promoting health and productivity in workplaces and homes. The expansion of smart cities and infrastructure projects globally will create substantial opportunities. Emerging markets in Asia, Africa, and Latin America will witness accelerated growth due to urbanization and increasing investments in infrastructure.

")

Smart and human-centric lighting solutions, while offering long-term energy and operational savings, require substantial upfront expenses for equipment, installation, and integration. These costs deter small-scale users and businesses with limited budgets. Additionally, retrofitting older structures with modern lighting systems is complex, often involving technical challenges like upgrading outdated wiring and infrastructure. Logistics, including compatibility with existing building designs and regulations, further complicate retrofitting. These factors collectively slow the penetration of advanced architectural lighting solutions, especially in regions lacking financial and technical resources.

Market Dynamics

The architectural lighting market is witnessing steady growth as urban development, commercial construction, and infrastructure modernization projects increasingly prioritize lighting as both a functional and aesthetic design element. Demand is rising for energy-efficient LED lighting systems, smart lighting controls, and human-centric lighting solutions that enhance visual comfort, productivity, and ambiance in residential, commercial, and public spaces. Government regulations promoting energy conservation and the gradual phase-out of conventional lighting technologies are further accelerating the shift toward advanced lighting systems. Additionally, the expansion of smart cities and sustainable building initiatives is encouraging the integration of connected lighting solutions that can be remotely controlled and optimized for energy efficiency.

The rapid expansion of commercial infrastructure, including retail centers, office spaces, hotels, and entertainment venues, also fuels market growth. These developments place a premium on lighting that enhances customer experience, strengthens brand identity, and creates inviting spaces. As construction activity continues in sectors tied to tourism, retail, and corporate growth, demand for customized architectural lighting solutions that balance efficiency with ambiance will continue to rise. For instance, in July 2025, the China Department of Transportation announced USD 488 million in funding under the Better Utilizing Investments to Leverage Development grant program, aimed at supporting 30 projects across the country. The investments are designed to strengthen key roadway, rail, maritime, and aviation infrastructure, with an emphasis on boosting safety, reducing congestion, and fostering economic growth.

The surge in infrastructure development and construction activities across both developed and emerging economies is driving market growth. As urbanization accelerates, cities are expanding with new residential complexes, commercial buildings, public infrastructure, and hospitality spaces, all of which demand advanced lighting solutions. Architectural lighting is increasingly being integrated into the design and planning stages of construction projects to enhance both functionality and aesthetics. Developers and architects are incorporating innovative lighting systems not only to provide illumination but also to create unique visual identities for structures, highlighting the importance of lighting as a key design element in modern infrastructure.

The adoption costs associated with architectural lighting typically include direct expenses and indirect expenses incurred throughout the complete life cycle of using an architectural lighting product, from procurement and installation to deployment. Architectural lighting also needs regular maintenance to keep it running, which adds to its operational costs. This can lead to relatively higher adoption costs and discourage the adoption of architectural lighting. Although the cost of ownership associated with LED lighting is comparatively lower than that of conventional architectural lighting, the average lifespan of LED lighting is much higher compared to that of CFLs, and the average electricity saved by LED lighting is 1.5 times higher compared to that saved by CFLs; consumers are hardly aware of all such benefits, such as energy efficiency, greater lifespan, and overall cost-effectiveness, associated with the adoption of LED lighting. This looming lack of awareness can potentially restrain the growth of the architectural lighting market. The lack of proper understanding and information about the capabilities of LED lighting and potential cost reductions can even lead to higher implementation costs. As a result, some consumers or organizations may not consider investing in LED lighting. A typical conventional consumer considers the product's pricing as crucial rather than focusing on the product’s long-term benefits, which means relatively higher adoption costs can particularly restrain the adoption of LED architectural lighting. Nevertheless, adequate consumer education and efforts to raise consumer awareness can help eliminate this barrier gradually.

LED architectural lighting has become a widely adopted solution due to its advantages, including long operational life, lower energy consumption, and reduced maintenance needs. According to estimates from the China Energy Department, the widespread adoption of LED lighting is expected to save approximately 348 terawatt-hours of energy by 2027. Compared to traditional lighting technologies, LED systems consume significantly less electricity while delivering superior efficiency and durability. Unlike incandescent bulbs, which typically last about 1,000 hours, and fluorescent lamps, which have a lifespan of roughly 8,000-10,000 hours, LED lights can operate for approximately 30,000-50,000 hours, depending on product quality. While LEDs gradually lose brightness over time, they do not abruptly fail or burn out like conventional bulbs. This extended service life, combined with lower replacement frequency and reduced maintenance costs, makes LEDs a more economical choice. The relatively low cost of transitioning from conventional lighting systems to LED solutions further strengthens their market adoption. These combined benefits are creating strong growth opportunities for LED architectural lighting across residential, commercial, and infrastructure applications.

Analyst Perspective

The architectural lighting market is increasingly shaped by the convergence of design innovation, energy-efficiency mandates, and smart building technologies, rather than by lighting hardware alone. Competitive advantage is shifting toward providers that can combine aesthetic design capabilities with digital lighting controls, IoT connectivity, and adaptive lighting intelligence. As buildings become more connected and sustainability-focused, lighting systems are evolving into active components of building management systems rather than passive utilities. Companies that can align lighting solutions with occupant well-being, energy optimization, and architectural flexibility are expected to strengthen their positioning in both premium commercial projects and large-scale urban infrastructure developments.

Component Insights

The ballasts segment dominated the architectural lighting industry, accounting for a revenue share of 18.2% in 2025. The rising adoption of LED lighting has significantly increased the demand for LED-compatible ballasts, which enhance performance, reliability, and energy efficiency in lighting systems. These ballasts are crucial for optimizing the functionality of LEDs, ensuring consistent and efficient operation across various applications. Simultaneously, the growing retrofit market is a major growth driver for the ballasts segment. As older buildings replace traditional lighting systems with modern, energy-efficient alternatives, upgrading or installing new ballasts becomes essential to support advanced technologies like LEDs. This trend is particularly pronounced in urban areas and commercial spaces, where retrofitting projects aim to align with energy efficiency goals and regulatory compliance standards.

The lamps segment is anticipated to grow at a significant CAGR during the forecast period. The increasing adoption of LED lamps is driving the growth, as they offer superior energy efficiency, extended lifespan, and lower operational costs. Their versatility makes them suitable for applications ranging from decorative accent lighting to large-scale architectural projects. Additionally, heightened awareness of environmental sustainability and stricter energy efficiency regulations are boosting demand for eco-friendly lamp solutions. This trend is particularly prominent in developed markets, where sustainable lighting solutions align with global goals for energy conservation and reduced carbon footprints.

Source Insights

The light-emitting diode (LED) segment accounted for the largest market share of 29.4% in 2025. LEDs are gaining significant traction in the architectural lighting market due to their exceptional energy efficiency and cost-saving potential. By consuming much less energy than traditional lighting technologies like incandescent and fluorescent bulbs, LEDs help lower electricity bills, making them a sustainable and economical choice for both residential and commercial applications. Additionally, LEDs are integral to the rise of smart lighting systems, which offer advanced features such as IoT compatibility, remote control, and automation. These smart capabilities enable better energy management, customization, and integration into broader smart cities and building initiatives. As urbanization and the demand for energy-efficient, intelligent infrastructure grow, the adoption of LED-based smart lighting solutions becomes increasingly essential.

The high-intensity discharge (HID) segment is expected to grow at a considerable CAGR during the forecast period. High-intensity discharge (HID) lamps are valued for their high luminous output, making them ideal for large-scale applications like street lighting, stadiums, and industrial spaces, where bright, expansive illumination is essential. Their ability to efficiently light vast areas drives demand in these sectors. Additionally, modern HID technologies, such as metal halide and high-pressure sodium lamps, offer significant improvements in energy efficiency compared to older lighting technologies. This makes them an appealing option for energy-conscious users seeking cost-effective and powerful lighting solutions for both outdoor and industrial environments.

Application Insights

The indoor segment dominated the architectural lighting industry, accounting for the largest revenue share of 76.8% in 2025. Awareness of how lighting affects mood, productivity, and overall health is driving the demand for human-centric lighting solutions. These systems, which adjust color temperature and brightness to mimic natural daylight patterns, align with circadian rhythms, thereby benefiting indoor environments such as workplaces and healthcare facilities. Additionally, indoor lighting plays a vital role in enhancing both the aesthetics and functionality of spaces. As interior design trends evolve, there is a growing demand for customized decorative lighting solutions that complement modern architectural styles. This is especially evident in residential, commercial, and hospitality settings, where ambiance and lighting quality are integral to creating inviting and functional environments.

The outdoor segment is expected to register significant growth during the forecast period. Rapid urbanization and infrastructure development are significantly driving the demand for outdoor lighting solutions, as they enhance safety, visibility, and aesthetics in growing urban environments. The expansion of public spaces, streets, and highways requires efficient lighting systems to support these needs. Additionally, the rise of smart city initiatives is fueling the adoption of IoT-enabled outdoor lighting systems. These systems provide benefits such as automated control, energy management, and real-time monitoring, enhancing security, operational efficiency, and sustainability in urban settings.

End Use Insights

The commercial segment accounted for the largest market share of 50.9% in 2025. The demand for energy-efficient lighting solutions is driving growth in the commercial segment of the architectural lighting market. As commercial buildings such as offices, retail stores, and hotels prioritize sustainability, the adoption of energy-saving lighting technologies, such as LEDs, has surged. These solutions not only help reduce operating costs but also align with broader environmental goals by decreasing energy consumption. Additionally, businesses are increasingly focusing on sustainability to meet green building certification standards, such as LEED. As a result, eco-friendly, energy-efficient lighting solutions have become a core component of modern commercial building designs, enhancing operational efficiency and reducing a company’s environmental footprint. This trend is transforming the commercial lighting landscape.

The residential segment is anticipated to grow at the highest CAGR from 2026 to 2033. Homeowners are increasingly prioritizing aesthetics and interior design, leading to a growing demand for architectural lighting that complements and enhances the visual appeal of living spaces. Lighting is now seen as a critical element of interior design, used to highlight architectural features, create focal points, and set the mood within different rooms. From accent lighting that highlights art and furniture to ambient lighting that creates a warm, inviting atmosphere, the role of lighting in residential design has expanded significantly. This focus on home aesthetics drives the adoption of customizable and design-forward lighting solutions in the residential market.

Regional Insights

Asia Pacific dominated the architectural lighting market with a revenue share of 43.2% in 2025, due to rapid urbanization, as several cities undergo immense growth and expansion. Architectural lighting is essential for upgrading urban landscapes, improving cityscapes, and creating attractive environments. Many APAC countries are concerned with energy savings and environmental sustainability, increasing the adoption of energy-efficient and innovative lighting solutions. As urban areas continue to expand and evolve, the demand for advanced architectural lighting is expected to grow, driven by the need for modern, sustainable, and visually impactful lighting solutions.

The China architectural lighting market held a substantial revenue share in 2025. China’s push to develop smart cities is driving demand for integrated lighting systems that are compatible with IoT and building management systems (BMS). These systems offer energy management, automation, and enhanced functionality, supporting China’s ambitions to modernize urban infrastructure.

The architectural lighting market in Japan held a substantial revenue share in 2025. Japan is known for its focus on technological innovation, which is reflected in the market growth. The country is a leader in the development and adoption of advanced lighting technologies, such as OLEDs, LEDs, and smart lighting systems. These innovations offer energy efficiency, enhanced performance, and customization, driving market growth.

The India architectural lighting market is growing rapidly, driven by the booming hospitality and retail industries, which are fueling demand for innovative architectural lighting solutions. Lighting plays a crucial role in enhancing the ambiance and customer experience in hotels, restaurants, malls, and other commercial establishments.

North America Architectural Lighting Market Trends

North America held a significant share of the architectural lighting industry in 2025. The market growth can be attributed to vast developments in LED technology over the years, which have increased efficiency, extended lifespans, and lowered LED costs. As a result, LED lighting has become an increasingly popular option for new building and retrofit projects. North America's stringent energy-efficiency requirements and standards have driven the adoption of energy-efficient lighting systems across applications, including architectural lighting.

U.S. Architectural Lighting Market Trends

The U.S. architectural lighting industry is expected to grow significantly from 2026 to 2033. The expansion of commercial infrastructure, including retail spaces, office buildings, and hospitality sectors, is driving the demand for architectural lighting. Businesses are increasingly using lighting to enhance aesthetics, create ambiance, and improve energy efficiency, thus promoting market growth.

Europe Architectural Lighting Market Trends

The architectural lighting industry in Europe is expected to grow at a significant CAGR from 2026 to 2033. Europe's stringent regulatory framework, energy-efficiency policies, and standards significantly impact the region's architectural lighting sector. These laws require energy-efficient lighting technology and establish performance requirements for lighting systems. For instance, the EU Eco-Design Directive regulates energy efficiency requirements for lighting products, stimulating innovation and the utilization of efficient lighting solutions.

The UK architectural lighting market is expected to grow rapidly in the coming years. As the UK focuses on reducing its carbon footprint and meeting environmental targets, energy-efficient lighting systems are integral to achieving green building certifications like BREEAM and LEED. These certifications are driving demand for advanced, eco-friendly lighting solutions in commercial buildings, public infrastructure, and residential projects.

The architectural lighting market in Germany held a substantial revenue share in 2025. Germany emphasizes sustainable urban planning and architectural lighting as fundamental to developing environmentally friendly urban spaces. The country aims to incorporate energy-efficient street lighting, pedestrian-friendly lighting designs, and green infrastructure. Such initiatives drive the growth of the market.

Key Architectural Lighting Company Insights

Some of the key companies operating in the market include Acuity Brands, Inc. and Signify Holding.

-

Acuity Brands, Inc. is a provider of building and lighting technology solutions and services. Its product portfolio includes lighting controls, lighting components, prismatic skylights, power supplies, fluorescent luminaires, LED lighting products, architectural lighting, high-intensity discharge luminaires, and embedded and standalone light control solutions. The company offers solutions for residential, industrial, commercial, infrastructure, life-safety, and lighting-control applications. Its LED lighting products are available under the brands Lithonia Lighting, Luminaire LED, Aculux, Eureka, and Mark Architectural Lighting.

-

Signify Holding is a provider of lighting solutions. The company’s product portfolio includes IoT-based lighting products for residential and commercial customers. The company sells its products under the brands Philips, Interact, Modular, and Luceplan. The company also offers services such as lighting audits, maintenance, remote support, and lighting plans.

Cree Lighting and Delta Light Group are some of the emerging participants in the agricultural lighting market.

-

The company’s Cree Lighting business segment designs and manufactures LED lighting products, architectural lighting, and outdoor and indoor lighting fixtures for connected smart homes, residential lighting, and intelligent solutions. The products manufactured by the company are used for various applications, such as inverters, lighting solutions, video displays, and transportation. The company’s LED Products segment offers LED components and chips used in video screens, specialty lighting, and automotive lighting.

-

Delta Light Group manufactures architectural lighting fixtures, including downlights, spotlights, wall lights, linear lighting, pendant lights, and outdoor lighting. The company uses cutting-edge LED technology, optics, and materials to develop energy-efficient lighting solutions with eye-catching designs. Delta Light Group offers customization options, enabling customers to tailor lighting solutions to specific project requirements. This includes selecting finishes, colors, and configurations that are consistent with the design concept of the project. Delta Light Group also offers smart lighting solutions featuring remote control, automation, and dynamic lighting effects.

Key Architectural Lighting Companies

The following key companies have been profiled for this study on the architectural lighting market.

-

Acuity Brands, Inc.

-

Cree Lighting

-

Delta Light

-

Current Lighting

-

GVA Lighting, Inc.

-

Hubbell

-

OSRAM SYLVANIA Inc.

-

Panasonic Corporation

-

Signify Holding

-

Siteco GmbH

-

Technical Consumer Products, Inc.

-

Zumtobel Group AG

-

Feilo Sylvania

-

Seoul Semiconductor Co., Ltd.

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weakness

Established Players: (Signify; Osram; Zumtobel Group; Acuity Brands; Hubbell Incorporated)

- Mature players in the architectural lighting market focus on design-centric and energy-efficient lighting solutions for buildings and urban infrastructure. They integrate LED technology with smart lighting controls and IoT-based systems. Their strategy emphasizes customized lighting for commercial buildings, public spaces, and smart cities. They also expand through partnerships with architects, contractors, and infrastructure developers.

- Mature players benefit from strong global distribution and established relationships with construction ecosystems. Their products combine aesthetics with high energy efficiency and durability. Advanced R&D supports innovation in human-centric lighting and smart controls. Strong brand reputation helps secure large-scale architectural projects.

- These companies face high competition in commoditized LED segments. Project-based demand can create revenue fluctuations. Custom lighting design increases engineering and production complexity. Rapid technological changes in smart lighting require continuous investment.

Emerging Players: (Lutron Electronics; Casambi; Helvar; Opple Lighting; Flos)

- Emerging players focus on smart, connected, and design-led lighting systems for modern architecture. They emphasize wireless controls, app-based lighting management, and modular LED solutions. Their strategy targets premium residential spaces, boutique commercial projects, and smart interior design applications. Many also focus on human-centric lighting that adjusts to occupancy and natural light conditions.

- Emerging players offer highly flexible and design-oriented lighting solutions. Their systems are easier to integrate into smart building environments. Strong focus on user experience improves adoption in modern architectural projects. They also innovate quickly in lighting control and personalization technologies.

- Emerging players have limited participation in large-scale infrastructure projects. Their manufacturing capacity is smaller than that of global lighting giants. Brand recognition in industrial and municipal projects is relatively weak. Dependence on niche design markets can restrict revenue stability.

Recent Developments

-

In May 2025, Zumtobel Group AG launched the second generation of its continuous-row lighting system, combining advanced functionality, refined design, and ultra-efficient installation. With the launch of TECTON II, the company sets a new benchmark in lighting technology. In collaboration with the engineering firm Pininfarina, Zumtobel has enhanced its universal trunking system with innovative features in technology, design, and sustainability. The system includes quick-to-install track and batten components, all manufactured at the company’s facility in Dornbirn, Austria.

-

In March 2025, GVA Lighting partnered with Specification Lighting Sales, LLC as its representative for New York City and Northern New Jersey. This collaboration marks an important milestone in GVA Lighting’s expansion into one of the world’s most prominent architectural lighting design markets. By joining forces with the highly respected team at SLS, GVA will benefit from strong connections within influential design and distribution networks.

-

In December 2024, Zumtobel Group AG announced the acquisition of UK-based LED lighting company, AC/DC. This strategic move enhances Zumtobel's position in the architectural lighting market by expanding its portfolio with advanced LED lighting solutions. AC/DC specializes in high-quality, energy-efficient LED products, which aligns with Zumtobel’s focus on sustainable and innovative lighting technologies. The acquisition aims to leverage AC/DC's expertise to offer more diverse and energy-efficient lighting options to meet the growing demand in both residential and commercial sectors.

-

In February 2024, Panasonic expanded its lighting business by inaugurating a new facility in Daman, India. This strategic move aims to strengthen its presence in the lighting market by focusing on energy-efficient solutions. The facility will enhance Panasonic's manufacturing capacity, enabling the company to meet the growing demand for innovative and sustainable lighting products. The expansion aligns with the company's commitment to environmental sustainability and serves as a step forward in advancing its lighting technologies in the Indian market.

Architectural Lighting Market Report Scope

Report Attribute

Details

Market size in 2025

USD 11.1 billion

Estimated market size in 2026

USD 11.5 billion

Projected market size by 2033

USD 17.5 billion

Growth rate

CAGR of 6.2% from 2026 to 2033

Actual data

2021 - 2024

Base Year

2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Component, source, application, end use, and region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; KSA; South Africa

Key companies profiled

Acuity Brands, Inc.; Cree Lighting; Delta Light; Current Lighting; GVA Lighting, Inc.; Hubbell; OSRAM SYLVANIA Inc.; Panasonic Corporation; Signify Holding; Siteco GmbH; Technical Consumer Products, Inc.; Zumtobel Group AG; Feilo Sylvania Seoul Semiconductor Co., Ltd.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Architectural Lighting Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the architectural lighting market report based on component, source, application, end use, and region:

-

Component Outlook (Revenue, USD Million/Billion, 2021 - 2033)

-

Lamp Holders

-

Ballasts

-

Lamps

-

Lenses/Shades

-

Trims

-

Wiring

-

Reflectors

-

Others

-

-

Source Outlook (Revenue, USD Million/Billion, 2021 - 2033)

-

Incandescent Lights

-

Fluorescent Lights

-

Light-Emitting Diode (LED)

-

High-Intensity Discharge (HID)

-

Others

-

-

Application Outlook (Revenue, USD Million/Billion, 2021 - 2033)

-

Indoor

-

Outdoor

-

-

End Use Outlook (Revenue, USD Million/Billion, 2021 - 2033)

-

Commercial

-

Residential

-

Industrial

-

Others

-

-

Regional Outlook (Revenue, USD Million/Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

KSA

-

South Africa

-

-

Research Methodology

Segment Definition

Segment - Component

Revenue capture definition

Lamp Holders

The lamp holders segment refers to the category of components designed to securely hold, connect, and power various types of light sources within architectural lighting systems. Lamp holders serve as the essential interface between the electrical supply and the lighting fixture, ensuring proper positioning, stability, and electrical contact for lamps such as LEDs, fluorescent tubes, halogen bulbs, and other specialized light sources used in architectural applications.

Ballasts

The ballasts segment refers to the category of electrical devices that regulate the current supplied to lighting sources such as fluorescent lamps, high-intensity discharge lamps, and other gas-discharge lighting systems commonly used in architectural applications. Ballasts are essential for providing the appropriate voltage to initiate the lamp’s operation and for controlling the flow of electrical current to ensure stable and efficient performance throughout its use.

Lamps

The lamps segment refers to the core category of light-emitting sources that provide illumination for architectural spaces and structures. This segment includes a wide range of lighting technologies such as incandescent, fluorescent, halogen, high-intensity discharge, and increasingly LED lamps, each serving different functional and aesthetic purposes in architectural applications. Lamps act as the primary medium through which lighting designs are realized, shaping both the visual environment and the user experience by influencing brightness, color quality, energy efficiency, and overall ambiance.

Lenses/Shades

The lenses/shades segment refers to the components used to shape, direct, diffuse, or soften the light emitted from lamps and fixtures, enhancing both functional performance and aesthetic appeal. Lenses are typically designed to control the beam angle, focus, and distribution of light, allowing precise illumination for architectural features or specific areas within a space. Shades, on the other hand, primarily serve to diffuse or soften light output while also contributing to the decorative aspect of the fixture, aligning with the overall design theme of interiors or exteriors.

Trims

The trims segment refers to the visible components of recessed lighting fixtures that frame and shape the final appearance and distribution of light. Trims are designed to provide both functional and aesthetic value, as they influence how light is cast within a space while also blending with or accentuating the architectural style of the environment.

Wiring

The wiring segment refers to the electrical infrastructure that connects lighting fixtures, controls, and power sources, enabling the safe and efficient operation of lighting systems. Wiring serves as the backbone of architectural lighting installations, ensuring the reliable power supply to lamps, ballasts, drivers, and other components while supporting advanced features such as dimming, automation, and smart lighting integration.

Reflectors

The reflectors segment refers to the components within lighting fixtures that are designed to redirect and optimize the distribution of light emitted from a lamp or light source. Reflectors are typically engineered with specific shapes, materials, and finishes to control the direction, intensity, and spread of light, allowing designers to achieve precise illumination effects that enhance both functionality and aesthetics in architectural spaces.

Others

The others include brackets, poles, and controls.

Segment - Source

Revenue capture definition

Incandescent Lights

The incandescent lights segment refers to the category of lighting solutions that utilize a filament-based technology to produce illumination. These lights generate light when an electric current passes through a tungsten filament, heating it to a high temperature until it glows.

Fluorescent Lights

The fluorescent lights segment refers to the category of lighting solutions that operate using a gas-discharge process. An electric current excites mercury vapor, producing ultraviolet radiation, which is then converted to visible light by a phosphor coating inside the tube. Fluorescent lights are widely recognized for their energy efficiency, longer lifespan, and ability to deliver consistent illumination compared to traditional incandescent lamps.

Light-Emitting Diode (LED)

The light-emitting diode (LED) segment refers to the category of lighting solutions that use semiconductor technology to produce illumination when an electric current passes through a diode. LEDs are characterized by their exceptional energy efficiency, long operational life, compact size, and design versatility. This segment has become integral to both interior and exterior lighting, offering flexibility in creating dynamic effects, precise beam control, and a wide spectrum of color options to enhance architectural aesthetics.

High-Intensity Discharge (HID)

The high-intensity discharge (HID) segment refers to the category of lighting technologies that generate illumination by creating an electric arc between tungsten electrodes housed inside a transparent or translucent arc tube filled with gas and metal salts. They offer advantages such as strong illumination, long-range visibility, and durability, though they typically consume more energy and require longer warm-up times compared to newer technologies like LEDs.

Others

The others include incident lights and linear fluorescent lights (LFLs).

Segment - Application

Revenue capture definition

Indoor

The indoor segment refers to the category of lighting solutions specifically designed for use within enclosed spaces such as residential buildings, offices, retail stores, hotels, museums, healthcare facilities, and other interior environments. This segment focuses on enhancing both functionality and aesthetics by providing illumination that supports tasks, improves comfort, and elevates the overall design appeal of indoor spaces.

Outdoor

The outdoor segment refers to the category of lighting solutions designed for use in exterior spaces such as building façades, landscapes, pathways, bridges, monuments, parks, and public infrastructure. This segment emphasizes both functional and aesthetic purposes, providing illumination that enhances safety, security, and visibility while also highlighting architectural features and creating visually appealing environments.

Segment - End Use

Revenue capture definition

Commercial

The commercial segment refers to the category of lighting solutions developed for use in business-oriented environments such as offices, retail stores, shopping malls, hotels, restaurants, educational institutions, and healthcare facilities. This segment is centered on providing illumination that not only ensures functionality and efficiency but also enhances the overall aesthetic and experiential value of commercial spaces.

Residential

The residential segment refers to the category of lighting solutions specifically designed for use in homes, apartments, and other living spaces. This segment emphasizes creating comfortable, functional, and visually appealing environments through lighting that supports everyday activities while enhancing the aesthetic character of interiors and exteriors. Residential architectural lighting includes a wide range of applications such as ambient lighting for overall illumination, task lighting for specific activities, and accent lighting to highlight design features or décor elements.

Industrial

The industrial segment refers to the category of lighting solutions designed for use in manufacturing plants, warehouses, processing facilities, logistics centers, and other industrial environments. This segment focuses on delivering high-performance illumination that enhances visibility, safety, and productivity in spaces where operations are often large-scale, continuous, and demanding. Industrial architectural lighting typically includes fixtures such as high-bay and low-bay lights, floodlights, and task-specific luminaires, many of which are engineered to withstand harsh conditions like dust, moisture, vibrations, and temperature extremes.

Others

The others include pathways, architectural buildings, sports complexes, and tunnels.

Estimation Model

Layer Name

Key Question

Description

Spatial Experience Layer

Where does architectural lighting create impact?

Identify built environments where lighting directly shapes spatial perception and user experience, such as commercial buildings, hospitality spaces, cultural institutions, retail environments, public infrastructure, and premium residential projects. This layer focuses on how lighting enhances architectural form, material texture, wayfinding, ambiance, and brand identity within designed spaces, rather than simply providing illumination.

Design Intent & Aesthetic Layer

What drives lighting design decisions?

Evaluate how architects, lighting designers, and interior planners define visual hierarchy, mood, contrast, and storytelling through light. Decisions are influenced by architectural style, cultural context, sustainability goals, human-centric lighting principles, and compliance with design standards. Increasing use of dynamic lighting scenes, tunable white systems, and façade illumination strategies reflects the shift toward experiential and adaptive design.

Technology & Control Integration Layer

Who enables smart and adaptive lighting environments?

Analyze the role of LED manufacturers, smart lighting control system providers, IoT platforms, and building automation systems that enable programmable and responsive lighting environments. Technologies such as Human-Centric Lighting, wireless control protocols, sensor-based dimming, and AI-driven lighting automation support energy efficiency and real-time adaptability in architectural applications.

Value Realization Layer

How is economic and experiential value generated?

Assess value creation through energy savings, reduced operational costs, increased property attractiveness, and enhanced tenant or visitor experience. Revenue streams include lighting fixture sales, design and consultancy services, installation contracts, smart control system subscriptions, and long-term maintenance agreements. Premium architectural lighting projects also generate indirect value by increasing real estate valuation, strengthening brand perception, and improving occupant satisfaction and productivity.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Architectural Aesthetic Lighting Design & Urban Ambience Trends

Conducted a focused analysis of architectural lighting applications across commercial buildings, hospitality spaces, cultural landmarks, retail environments, and public infrastructure, emphasizing design-driven illumination, façade lighting, and ambience creation.

Helps stakeholders identify design-led lighting opportunities, evaluate urban beautification trends, and assess commercialization potential in premium architectural lighting solutions.

Smart Lighting, Energy Efficiency & Building Automation Integration Trends

Evaluated adoption trends for IoT-enabled lighting systems, daylight harvesting solutions, motion-sensor lighting, tunable white lighting, and integration with building management systems (BMS) for energy optimization and automation.

Provides insights into energy-efficiency mandates, smart building transformation, and commercially attractive intelligent lighting solutions that support sustainability goals.

Experience-Driven Spaces & Human-Centric Lighting Opportunity Assessment

Assessed demand for human-centric lighting systems supporting wellness, productivity, and emotional experience in workplaces, healthcare facilities, retail environments, and hospitality spaces, along with challenges related to installation complexity, ROI justification, and design customization.

Supports investment and expansion strategies by identifying high-value experiential lighting segments, evaluating technology readiness, and strengthening long-term opportunities in adaptive and intelligent lighting ecosystems.

Frequently Asked Questions About This Report

The growth of the architectural lighting market can be attributed to rapid urbanization and the expansion of infrastructure development. Architectural lighting is becoming increasingly important in various settings, including independent bungalows, condominiums, community houses, skyscrapers, residential buildings, shopping malls, office spaces, hotels, public offices, and industrial lofts, among others.

The global architectural lighting market size was estimated at USD 11.1 billion in 2025 and is expected to reach USD 11.5 billion in 2026.

Some key players operating in the architectural lighting market include Acuity Brands, Inc., Cree Lighting, Delta Light, Current Lighting, GVA Lighting, Inc., Hubbell, OSRAM SYLVANIA Inc., Panasonic Corporation, Signify Holding, Siteco GmbH, Technical Consumer Products, Inc., Zumtobel Group AG, Feilo Sylvania, Seoul Semiconductor Co., Ltd.

The light-emitting diode (LED) segment led with a 29.4% revenue share in 2025 and it is also the fastest-growing segment.

The indoor segment held the largest share (over 76%) in 2025, while outdoor segment is the fastest-growing segment.

Asia Pacific dominated with 43.2% revenue share in 2025.

Commercial segment held the largest revenue share in 2025, while residential segment is the fastest-growing market.

The global architectural lighting market is expected to grow at a compound annual growth rate of 6.2% from 2026 to 2033 to reach USD 17.5 billion by 2033.

The ballasts segment led with a 18.2% revenue share in 2025, while lamps segment is the fastest-growing segment.

About the Author(s)

Electronic Devices Research Team

Semiconductors & Electronics · Electronic DevicesThis report was authored by the electronic devices research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the electronic devices segment of the semiconductors & electronics industry. All findings are based on proprietary semiconductors & electronics databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.