- Home

- »

- Next Generation Technologies

- »

-

Autonomous Networks Market Size Report, 2026-2033GVR Report cover

![Autonomous Networks Market (2026 - 2033)Report]()

Autonomous Networks Market (2026 - 2033)

Size, Share & Trends Analysis Report By Component Type (Solution, Services), By Deployment Model Type (Cloud, On-premises), By Organization Size (SME, Large organization), By End User (Healthcare, BFSI), By Region, And Segment Forecasts

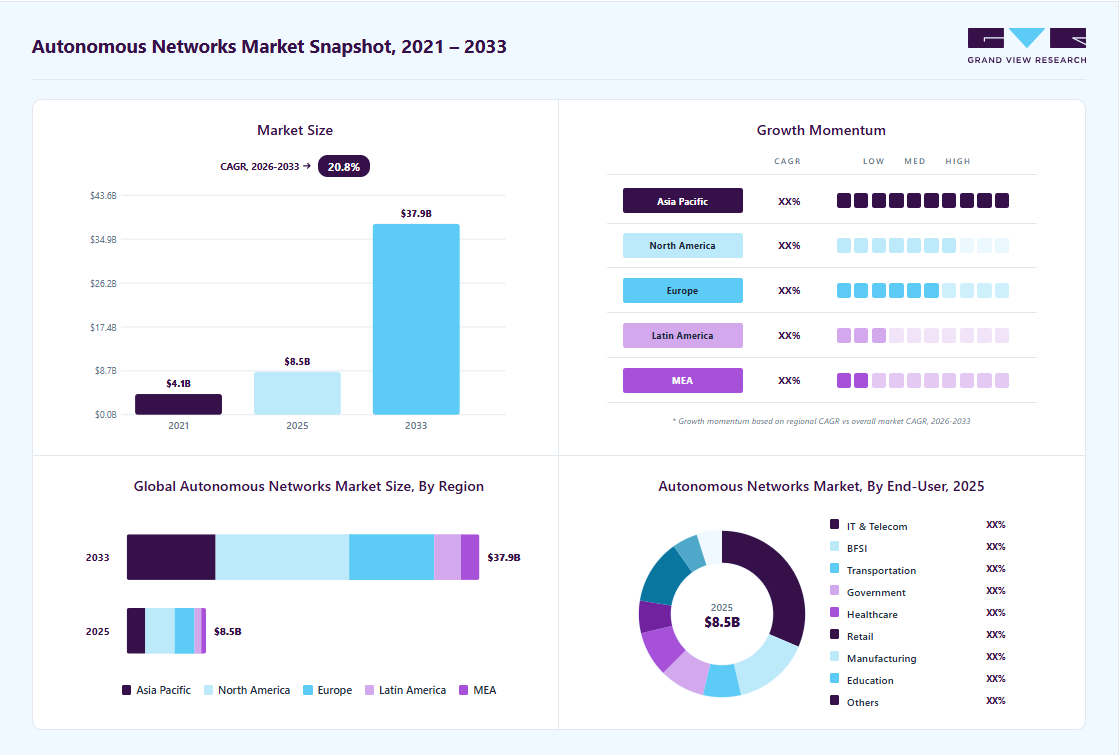

Market Size, 2025

$8.5BMarket Estimate, 2026

$10.1BMarket Forecast, 2033

$37.9BCAGR, 2026–2033

20.8%Autonomous Network Market Summary

The global autonomous networks market size was valued at USD 8.5 billion in 2025 and is projected to grow from USD 10.1 billion in 2026 to USD 37.9 billion by 2033, at a CAGR of 20.8% from 2026 to 2033. The market in North America dominated with a revenue share of 37.2% in 2025. Market growth is attributed to the rapid adoption of artificial intelligence and machine learning, which allows networks to be managed predictively and efficiently with minimal human intervention, thus improving efficiency and reducing operational costs.

Key Market Trends & Insights

- By component type: Solution segment held the largest market share of 57.9% in 2025.

- By deployment model type: On-premise segment held the largest market share in 2025.

- By organization size: Large organization segment held the largest market share in 2025.

- By end user: IT & telecom segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: North America (37.2% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 8.5 Billion

- Estimated market size in 2026: USD 10.1 Billion

- Projected market size by 2033: USD 37.9 Billion

- CAGR (2026-2033): 20.8%

The growing complexity of telecom and enterprise networks, fueled by cloud computing, 5G deployment, and increased data traffic, has also increased demand for automated network management solutions that provide real-time monitoring and fault resolution to maintain consistent performance and reliability. The growth of the autonomous network market is further driven by the rising demand for improved operational efficiency and cost optimization, where repetitive network management tasks have been increasingly automated to reduce dependency on manual intervention, thereby improving service reliability and minimizing downtime. Additionally, telecom operators and enterprises are increasingly adopting autonomous network solutions to significantly improve customer experience, enable faster, more accurate issue identification and resolution, support predictive maintenance, and ensure seamless, high-quality service delivery across highly dynamic, distributed network environments that require real-time responsiveness and adaptive intelligence.

Technological trends in the autonomous network market emphasize the increasing adoption of AI-native networking architectures. These systems embed intelligence directly into networks, enabling automated decision-making and self-configuration without human intervention. Telecom operators are deploying AI-enabled orchestration platforms that automatically adjust network resources during traffic surges. For instance, in November 2025, Deutsche Telekom AG launched the “RAN Guardian Agent,” an AI solution designed to improve mobile network performance by enabling faster analysis, automated troubleshooting, and enhanced resilience. The agent continuously monitored network behavior and initiated real-time corrective actions, advancing the development of autonomous and self-healing networks. Additionally, the growth of real-time closed-loop automation is supported by edge computing and advanced analytics. Networks now continuously monitor performance, analyze conditions, and execute corrective actions instantly.

")

Moreover, strategic collaborations in the autonomous network market are helping companies to accelerate innovation and deploy AI-driven network technologies more quickly across telecom infrastructure. By combining expertise in AI, cloud computing, and radio access technologies, these partnerships enable operators and vendors to develop automated and scalable network systems that meet 5G and 6G requirements. For instance, in March 2026, Nokia Corporation and Deutsche Telekom AG expanded their collaboration to advance AI-native and Open RAN innovation through joint development of Cloud RAN, open interfaces, and multivendor orchestration. They are developing AI-native RAN solutions, predictive optimization, and real-world validation of autonomous network capabilities, marking a significant step toward fully automated and self-optimizing mobile networks.

Regulatory standards play a critical role in the autonomous network market to ensure AI-driven systems operate securely, transparently, and in compliance. For instance, the European Union’s GDPR (General Data Protection Regulation) establishes strict rules for the collection, processing, and storage of user data in telecom networks. For autonomous networks, GDPR ensures that AI-based systems protect privacy, maintain data security, and uphold accountability, even when decisions are automated. Additionally, the Open RAN standards from the O-RAN Alliance define open, interoperable interfaces for radio access networks (RAN). These standards enable telecom operators and vendors to develop flexible, multivendor network architectures that support seamless integration of AI automation across technologies.

The autonomous network market faces certain restraints that may lower large-scale adoption. One of the major challenges is the high implementation costs and infrastructure complexity, which require significant investment in AI systems, cloud infrastructure, analytics platforms, and network modernization. Many telecom operators struggle to justify these upfront costs, which can delay deployment and limit adoption. Additionally, concerns about cybersecurity and system reliability persist, as reliance on AI-driven decision-making and real-time data processing increases the risk of cyberattacks or AI misconfigurations. These risks may disrupt critical communication services and make operators hesitant to fully automate without human oversight.

Market Dynamics

The growing adoption of AI-native, self-healing network architectures is driving the autonomous network market by enabling telecom operators and enterprises to automate network management, improve operational efficiency, and ensure real-time service optimization across increasingly complex digital ecosystems. As networks become more dynamic with the rapid expansion of 5G, cloud computing, IoT devices, and edge infrastructure, organizations are increasingly deploying AI-driven autonomous networking solutions to reduce manual intervention and improve network reliability.

AI-native autonomous networks integrate artificial intelligence, machine learning, predictive analytics, and closed-loop automation directly into network infrastructure, enabling systems to continuously monitor performance, detect anomalies, predict failures, and automatically execute corrective actions without human involvement. These capabilities help operators reduce downtime, optimize bandwidth utilization, improve service quality, and significantly lower operational expenditure. In addition, self-healing networks improve customer experience by enabling faster fault resolution, intelligent traffic management, and proactive maintenance across highly distributed environments.

High infrastructure modernization costs and deployment complexity are restraining the growth of the autonomous network market by creating significant financial and operational challenges for telecom operators and enterprises. Implementing autonomous networks requires substantial investments in AI platforms, cloud-native architectures, advanced analytics systems, orchestration tools, and next-generation network infrastructure to support real-time automation and intelligent decision-making.

The expansion of Open RAN, edge computing, and 5G/6G ecosystems is creating significant growth opportunities for the autonomous network market by accelerating the need for intelligent, scalable, and highly automated network management solutions. Telecom operators and enterprises are increasingly deploying distributed network architectures to support ultra-low latency applications, massive IoT connectivity, industrial automation, smart cities, and immersive digital services.

The adoption of Open RAN architectures and multivendor network environments is increasing operational complexity, driving strong demand for autonomous orchestration platforms that enable seamless interoperability, intelligent resource allocation, and automated performance optimization. Autonomous network solutions powered by AI and machine learning help operators efficiently manage network slicing, dynamic traffic patterns, and real-time service delivery across highly decentralized infrastructures.

Market Concentration & Characteristics

The autonomous network market is moderately fragmented, with a strong, growing shift toward consolidation as demand rises for fully integrated, AI-driven network automation platforms. A mix of global telecom technology providers, cloud service providers, AI and analytics vendors, and specialized network automation startups characterizes the competitive landscape. While leading players hold significant influence in large-scale telecom deployments, a broad base of niche and mid-sized companies continues to operate across specific segments such as network analytics, orchestration, self-healing systems, and AI-based optimization tools.

Fragmentation is particularly evident across the solution landscape, where vendors are increasingly focusing on specialized capabilities rather than end-to-end autonomous networking platforms. Many players focus on discrete functional areas, such as real-time network monitoring, predictive analytics, automated configuration, and self-healing capabilities, enabling them to address specific operator pain points in complex telecom environments.

Component Type Insights

The solution segment accounted for the largest share of 57.96% in 2025. The growth of the segment is attributed to the increasing demand for integrated software platforms that enable end-to-end network automation and intelligence. This dominance is largely supported by the adoption of advanced capabilities such as network monitoring and analytics, network configuration and management, and network optimization and self-healing, which together form the core of autonomous network functionality. These advance capabilities help telecom operators and enterprises continuously track network performance, automatically configure and manage resources, optimize traffic flow, and resolve issues in real time without manual intervention, thereby improving operational efficiency and ensuring high network reliability and service quality.

The services segment is expected to grow at the fastest CAGR during the forecast period. The growth is driven by the increasing complexity of autonomous network deployment and the rising demand for expert support in integrating, managing, and optimizing AI-driven network solutions. As telecom operators and enterprises adopt more automated and intelligent networks, demand for consulting, implementation, integration, and managed services is rising to ensure smooth deployment and efficient performance. Ongoing requirements for network upgrades and technical support in AI-enabled and cloud-based infrastructures are further accelerating the expansion of the services segment, as organizations depend on service providers to maximize the value and efficiency of autonomous network solutions.

Deployment Model Type Insights

The on-premise segment dominated the market in 2025. The growth of the segment is attributed to organizations’ need for stronger data security, greater control over their network infrastructure, and lower latency for mission-critical applications. Telecom operators and large enterprises also prefer on-premise deployment to meet strict regulatory and data sovereignty requirements, particularly in industries such as BFSI, government, and healthcare. Additionally, the presence of significant legacy infrastructure and the need for seamless integration with existing in-house systems continue to support the adoption of on-premises solutions over cloud-based alternatives.

The cloud segment is projected to grow at the fastest CAGR over the forecast period. Cloud deployment allows telecom operators and enterprises to quickly implement and manage technologies such as 5G, edge computing, and AI-driven autonomous networks. Various companies are launching cloud-integrated solutions and forming strategic partnerships to accelerate network transformation and improve service delivery capabilities. For instance, in February 2026, NEC Corporation launched an edge computing solution integrated with Amazon Web Services (AWS) Outposts, combining its User Plane Function (UPF) with cloud infrastructure to support efficient deployment of 5G services and low-latency applications. This demonstrates how cloud-enabled edge integration helps telecom operators modernize their networks and enable next-generation autonomous capabilities.

Organization Size Insights

The large organization segment dominated the market in 2025. The segment's growth is attributed to its strong financial resources and advanced IT infrastructure. These enterprises can invest in complex, high-cost autonomous networking solutions and generate significant data volumes, requiring scalable, secure, and efficient network management. Their operations across multiple locations further increase the need for real-time monitoring and intelligent network optimization. Moreover, large organizations quickly adopt technologies such as 5G, cloud computing, and edge computing, which increases demand for autonomous network solutions. Their emphasis on operational efficiency and reduced downtime also drives segment growth.

The SME segment is expected to grow at the fastest CAGR over the forecast period. Small and medium-sized enterprises are adopting cloud-based, AI-driven autonomous networking technologies to improve operational efficiency, minimize manual intervention, and improve network performance without requiring significant in-house IT resources. Additionally, the growing availability of subscription-based and managed service models is making advanced networking solutions more accessible to SMEs, enabling them to benefit from real-time monitoring, automated troubleshooting, and enhanced cybersecurity. Moreover, rapid digital transformation across industries, combined with the adoption of remote work and cloud applications, is further driving demand for autonomous network solutions among SMEs.

End User Insights

The IT & telecom segment held the largest market share in 2025. The segment is rapidly advancing in autonomous networking as AI, machine learning, and automation are increasingly integrated into network operations. These technologies make networks more self-managing and self-healing, reducing the need for manual intervention. Consequently, telecom operators can improve efficiency and manage growing data traffic more effectively across complex, distributed infrastructures. Moreover, the adoption of cloud-native architectures and software-defined networking (SDN) further strengthens this transition by providing the required flexibility, scalability, and programmability for modern network environments.

The healthcare segment is expected to grow at the fastest CAGR over the forecast period. The segment’s growth is driven by the increasing digitalization of healthcare services and the rising adoption of advanced technologies, including telemedicine, IoT-enabled medical devices, and AI-powered diagnostics. Healthcare organizations deploy autonomous network solutions to ensure secure and real-time data transmission, which is critical for patient monitoring and clinical decision-making. Moreover, the shift towards cloud-based healthcare infrastructure and connected medical ecosystems is further accelerating the demand for autonomous networks. These solutions help healthcare providers improve operational efficiency, reduce network downtime, and enhance data security and compliance.

Regional Insights

The North America autonomous network market held the largest market share of 37.25% in 2025. The region's growth is attributed to its advanced IT infrastructure and early adoption of 5G, edge computing, and cloud-native technologies. Regional operators are deploying autonomous networks to address the complexity of 5G environments, leveraging artificial intelligence, machine learning, and closed-loop automation to enable self-healing, self-configuring, and self-optimizing capabilities. This emphasis on automation aims to improve customer experience, boost operational efficiency, and simplify network management.

The region is also shifting toward intent-based networking, where networks automatically translate business objectives into optimized configurations. Moreover, North American operators are preparing for future 6G networks by integrating AI-driven predictive and adaptive capabilities. Companies such as Cisco Systems, Inc. are advancing this transformation with solutions that support automation, orchestration, and intelligent network operations, further reinforcing the region’s leadership in autonomous network adoption.

U.S. Autonomous Network Market Trends

The U.S. autonomous network market held a dominant position in 2025. The U.S. autonomous network market is shifting toward AI-driven, self-managing networks that can automatically configure, optimize, and fix issues with minimal human involvement. Telecom operators such as Verizon Communications Inc. are modernizing their 5G networks to support automation and self-healing functions. In the enterprise segment, technologies such as SD-WAN and intent-based networking enable organizations to set objectives such as low latency, enhanced security, and optimized application performance. The network then dynamically configures and adapts to meet these goals. The U.S. market continues to progress toward fully intelligent, autonomous networks that reduce manual intervention and improve speed, reliability, scalability, and efficiency.

Asia Pacific Autonomous Network Industry Trends

The Asia Pacific autonomous network market is expected to grow at a fastest CAGR of 22.1% over the forecast period. The region’s growth is driven by 5G standalone deployments and increased adoption of Agentic AI technologies. Local operators are moving from Level 2 to Level 4 network autonomy, prioritizing AI-driven predictive maintenance, closed-loop automation, and intent-based networking to reduce operational costs. For instance, in September 2025, China Mobile announced that it had achieved Level 4 autonomous network capability within its network operations center by deploying intelligent agents to manage and optimize network operations. This milestone demonstrated how AI-driven automation can significantly improve operational efficiency by enabling autonomous fault detection, resolution, and service management with minimal human intervention. Moreover, the integration of Generative AI with traditional AI is enabling cognitive networks that predict failures and automate complex, multi-domain tasks, especially for 5G enterprise services.

The China autonomous network industry is expected to grow rapidly in the coming years. The country is rapidly moving toward autonomous telecom operations by using intelligent systems to manage and optimize network performance more efficiently. The telecom sector supports national initiatives such as smart cities, industrial digitalization, and IoT expansion, which require reliable, scalable network infrastructure. Moreover, telecom operators are also integrating AI with cloud and edge computing to enable real-time decision-making and improve service quality for consumers and enterprises.

The Japan autonomous network market is being supported by the country’s focus on miniaturized electronics and advanced IoT components, enabling highly dense and efficient connectivity. The strong presence of robotics, semiconductors, and smart manufacturing industries further increases demand for low-latency, highly stable networks. Additionally, AI and cloud-based orchestration tools are being integrated to improve network resilience and support next-generation applications in smart manufacturing and connected infrastructure.

Europe Autonomous Network Market Trends

The Europe autonomous network market was identified as a lucrative region in 2025. Autonomous networks in Europe are advancing steadily as they aim to achieve higher levels of autonomy to improve efficiency, self-healing, and service reliability. For instance, in February 2026, Telefónica, a multinational telecommunications company, accelerated its transformation to autonomous networks through its Autonomous Network Journey (ANJ) program, reaching 12 Level 4 use cases. This progress has been achieved through coordinated efforts across Spain, Brazil, and Germany, reflecting strong multi-market collaboration. The development positions Telefónica on a clear roadmap to reach Level 3.75 by 2028 and full Level 4 autonomy by 2030, highlighting Europe’s gradual but structured approach toward fully autonomous network operations. While many European operators remain at intermediate maturity levels due to legacy infrastructure challenges, they are increasingly adopting AI-driven, cloud-native solutions to enable greater automation and network optimization. The region’s growth is further driven by the need to reduce operational costs, manage the rising complexity of 5G networks, and prepare for future 6G networks.

The UK autonomous network market is expected to grow rapidly in the coming years. The country's local telecom operators are prioritizing AI-driven network automation to improve reliability, strengthen cybersecurity, and meet the rising demand for high-speed data in both urban and rural areas. Furthermore, the rollout of 5G and the acceleration of enterprise digital transformation are driving the adoption of intelligent network management systems. The UK is also advancing innovation in edge computing and smart connectivity, enabling more responsive network performance across sectors such as finance, healthcare, transportation, and others

The Germany autonomous network market is expanding, supported by the country’s strong industrial base and focus on Industry 4.0 transformation. Demand for highly reliable networks is increasing due to the widespread adoption of industrial automation and connected manufacturing systems. Moreover, the country’s emphasis on precision engineering and digital industrial ecosystems is driving the integration of autonomous networking solutions that ensure consistent performance and real-time connectivity across complex production environments.

Key Autonomous Networks Company Insights

Some of the key companies in the autonomous network market include Cisco Systems, Inc., Huawei Technologies Co., Ltd., Nokia Corporation, and others. Organizations are focusing on increasing the customer base to gain a competitive edge in the industry. Therefore, key players are taking several strategic initiatives, such as mergers and acquisitions, and partnerships with other major companies.

-

Cisco Systems, Inc. develops networking hardware, software, and related services. In the autonomous networks market, Cisco offers solutions that use automation, analytics, and artificial intelligence to improve network operations. Its technologies include intent-based networking, cloud-managed infrastructure, and security-integrated platforms that reduce manual configuration and improve efficiency. Enterprises and service providers use these solutions to manage complex networks across data centers, campuses, and cloud systems. The company also invests in research and acquisitions to strengthen its capabilities in network automation and intelligent system management.

-

Huawei Technologies Co., Ltd. provides information and communications technology solutions. In autonomous networks, the company develops frameworks and tools that integrate artificial intelligence, big data, and automation for telecom network management. Its Autonomous Driving Network (ADN) approach enables different levels of automation in network planning, deployment, maintenance, and optimization. Telecom operators use Huawei’s solutions to improve network efficiency and reduce operational complexity. The company also develops 5G infrastructure and cloud-based systems, supporting the shift to software-driven and automated global communication networks.

Key Autonomous Networks Companies:

The following key companies have been profiled for this study on the autonomous networks market.

- Cisco Systems, Inc.

- Huawei Technologies Co., Ltd.

- Nokia Corporation

- Telefonaktiebolaget LM Ericsson

- Hewlett Packard Enterprise

- NEC Corporation

- Ciena Corporation

- Arista Networks, Inc.

- Extreme Networks, Inc.

- Juniper Networks, Inc.

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: Cisco Systems, Inc.; Huawei Technologies Co., Ltd.; Nokia Corporation; Telefonaktiebolaget LM Ericsson; Hewlett Packard Enterprise;

- Mature players focus on delivering end-to-end autonomous networking ecosystems integrating AI-driven network automation, intent-based networking, and closed-loop orchestration across telecom and enterprise infrastructures.

- They emphasize development of AI-native network management platforms, 5G/6G-ready architectures, Open RAN integration, and cloud-native orchestration capabilities to support large-scale network transformation programs.

- Strong global presence with deep relationships across telecom operators, enterprises, and cloud ecosystems.

- Advanced R&D capabilities enabling leadership in AI-driven network automation, SDN/NFV, and self-healing network technologies.

- High solution complexity and integration challenges across multivendor environments.

- Significant capital requirements and long deployment cycles may slow adoption in cost-sensitive markets.

Emerging Players: Arista Networks, Inc.; Extreme Networks, Inc.; Juniper Networks, Inc.

- Emerging and challenger players focus on specialized autonomous networking capabilities such as AI-driven network assurance, cloud-managed networking, intent-based networking, and high-performance data center automation.

- Strategies emphasize modular, software-defined, and cloud-native solutions that can be rapidly deployed within enterprise and hyperscale environments.

- Strong innovation in cloud-native networking, data center automation, and AI-based network optimization.

- Agile product development cycles enabling faster feature rollout compared to traditional telecom vendors.

- Limited end-to-end autonomous network portfolios compared to large telecom infrastructure providers.

- Weaker penetration in large-scale telecom operator and government-led network transformation projects.

Recent Developments

-

In March 2026, Telefonaktiebolaget LM Ericsson & Nokia Corporation announced a landmark collaboration to advance intelligent automation across purpose-built, cloud RAN, and Open RAN networks. As part of the agreement, Ericsson became a member of Nokia’s SMO Marketplace, enabling CSPs and partners to develop and deploy automation applications. Simultaneously, Nokia joined the Ericsson rApp Ecosystem, which included CSPs, vendors, and developers. The platform supported network management and automation across open, multivendor, and multi-technology environments.

-

In February 2025, Hewlett Packard Enterprise (HPE) announced major innovations in its HPE Juniper Networking portfolio to advance the AI-native Mist platform for autonomous network operations. The update introduced agentic AI-powered troubleshooting, improved visibility, and new AIOps features for data centers. These capabilities strengthened GreenLake Intelligence, enabling proactive optimization, real-time problem-solving, and improved network efficiency.

Autonomous Network Market Report Scope

Report Attribute

Details

Market size in 2025

USD 8.5 billion

Estimated market size in 2026

USD 10.1 billion

Projected market size by 2033

USD 37.9 billion

Growth rate

CAGR of 20.8% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Component type, deployment model type, organization size, end user, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; Japan; India; South Korea; Australia; Brazil; KSA; UAE; South Africa

Key companies profiled

Cisco Systems, Inc.; Huawei Technologies Co., Ltd.; Nokia Corporation; Telefonaktiebolaget LM Ericsson; Hewlett Packard Enterprise; NEC Corporation; Ciena Corporation; Arista Networks, Inc.; Extreme Networks, Inc.; Juniper Networks, Inc.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Autonomous Networks Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global autonomous network market report based on component type, deployment model type, organization size, end user, and region.

-

Component Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Solution

-

Network monitoring and analytics

-

Network configuration and management

-

Network optimization and self-healing

-

-

Services

-

Professional

-

Managed

-

-

-

Deployment Model Type Outlook (Revenue, USD Million, 2021 - 2033)

-

On-premises

-

Cloud

-

-

Organization Size Outlook (Revenue, USD Million, 2021 - 2033)

-

Large organization

-

SME

-

-

End User Outlook (Revenue, USD Million, 2021 - 2033)

-

IT & Telecom

-

BFSI

-

Transportation

-

Government

-

Healthcare

-

Retail

-

Manufacturing

-

Education

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East and Africa (MEA)

-

KSA

-

UAE

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Autonomous Networks Market Opportunity Assessment

Country/region-wise autonomous network market sizing and growth forecasts across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Assessment of regulatory frameworks impacting autonomous networks (data privacy laws, AI governance policies, telecom automation standards.

Identified region-specific growth opportunities in high-adoption telecom automation and AI-native network markets.

Supported telecom operators and enterprise network modernization strategies.

Autonomous Network Technology & Deployment Behavior Study

Analysis of telecom operators and enterprise adoption patterns for autonomous networking solutions across industries and network architectures.

Evaluation of deployment preferences, including on-premises, cloud, and hybrid autonomous network models.

Improved segmentation of autonomous network demand by deployment model and enterprise size.

Supported product positioning for AI-native, cloud-based, and hybrid autonomous network solutions.

Competitive Benchmarking and Strategic Positioning in the Autonomous Networks Market

Benchmarking of key players across AI/ML capabilities, network orchestration platforms, self-healing technologies, and intent-based networking solutions.

Comparative assessment of partnerships with telecom operators, hyperscale cloud providers, and ecosystem integration in Open RAN and edge environments.

Identified competitive white spaces in end-to-end autonomous network platforms and real-time closed-loop automation.

Supported strategic positioning, partnership development, and ecosystem expansion with telecom operators and cloud providers.

Frequently Asked Questions About This Report

North America dominated with a 37.2% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

The on-premise segment held the largest revenue share in 2025, while the cloud segment is the fastest-growing.

The large organization segment held the largest revenue share in 2025, while the SME segment is the fastest-growing.

The global autonomous networks market size was estimated at USD 8.5 billion in 2025 and is expected to reach USD 10.1 billion in 2026.

The global autonomous networks market is expected to grow at a compound annual growth rate of 20.8% from 2026 to 2033 to reach USD 37.9 billion by 2033.

The solution segment accounted for the largest share of 57.9% in 2025. The growth of the segment is attributed to the increasing demand for integrated software platforms that enable end-to-end network automation and intelligence

Some key players operating in the autonomous networks market include Cisco Systems, Inc., Huawei Technologies Co., Ltd., Nokia Corporation, Telefonaktiebolaget LM Ericsson, Hewlett Packard Enterprise, NEC Corporation, Ciena Corporation, Arista Networks, Inc., Extreme Networks, Inc., Juniper Networks, Inc.

Market growth is attributed to the rapid adoption of artificial intelligence and machine learning, which allows networks to be managed predictively and efficiently with minimal human intervention, thus improves efficiency and reduces operational costs.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.