- Home

- »

- Food Safety & Processing

- »

-

Beverage Cans Market Size And Share Report, 2026-2033GVR Report cover

![Beverage Cans Market (2026 - 2033)Report]()

Beverage Cans Market (2026 - 2033)

Size, Share & Trends Analysis Report By Material (Aluminum, Steel), By Application (Carbonated Soft Drinks, Alcoholic Beverages, Fruits & Vegetable Juices), By Region (North America, Europe), And Segment Forecasts

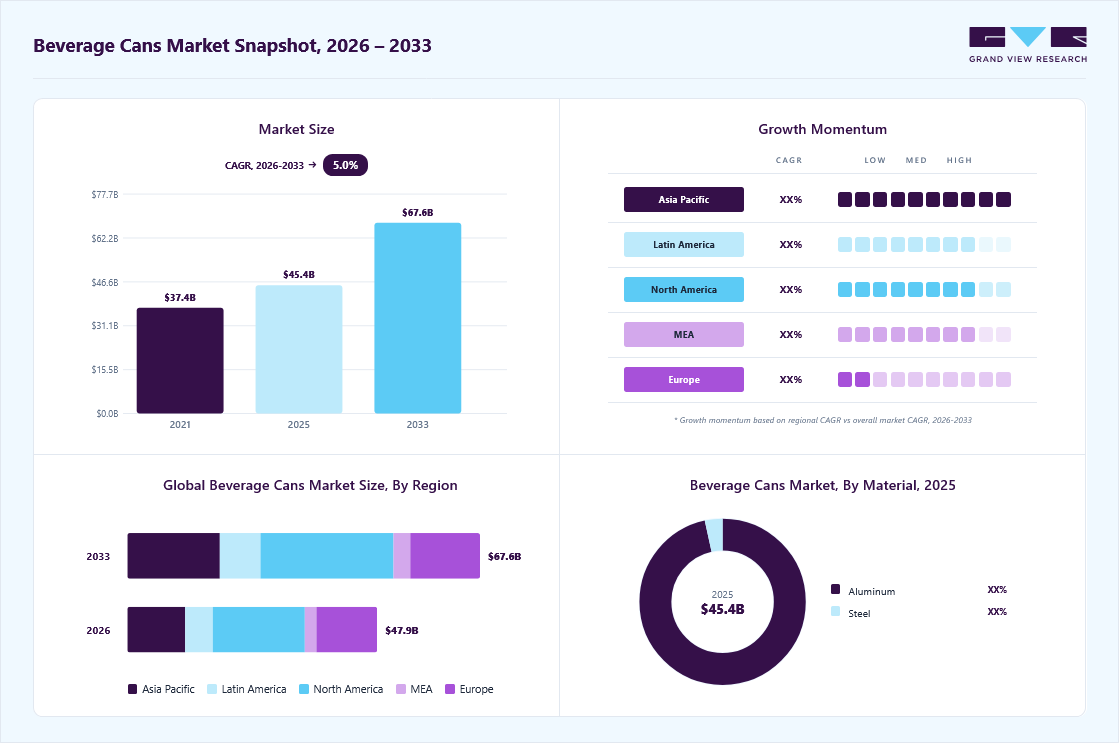

Market Size, 2025

$45.4BMarket Estimate, 2026

$47.9BMarket Forecast, 2033

$67.4BCAGR, 2026–2033

5.0%Beverage Cans Market Summary

The global beverage cans market size was valued at USD 45.4 billion in 2025 and is projected to grow from USD 47.9 billion in 2026 to USD 67.4 billion by 2033, at a CAGR of 5.0% from 2026 to 2033. The market in North America dominated with a revenue share of 36.0% in 2025. An increasing consumption of beverages such as carbonated soft drinks, beer, and cider on a global level is driving the demand for beverage cans.

Key Market Trends & Insights

- By material: Aluminum segment held the largest market share of 96.0% in 2025.

- By application: Alcoholic beverages segment held the largest market share of 38.0% in 2025.

Regional Highlights

- Largest regional market: North America (36.0% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 45.4 Billion

- Estimated market size in 2026: USD 47.9 Billion

- Projected market size by 2033: USD 67.4 Billion

- CAGR (2026-2033): 5.0%

Additionally, the high recycling rate of aluminum cans and the superior physical properties of metals over their alternatives are expected to drive the growth of the beverage can industry during the forecast period. Beverage cans offer exceptional convenience and portability, making them an attractive choice for on-the-go consumption. They are lightweight, easy to carry, and resealable, allowing consumers to enjoy their beverages at their convenience. This aspect is particularly appealing to urban populations with busy lifestyles and a preference for convenient packaging solutions. For instance, energy drink manufacturers have leveraged the portability of cans to cater to active consumers who demand readily available beverages during their workouts or outdoor activities.")

Moreover, beverage cans offer a unique canvas for eye-catching designs and branding opportunities. Companies can leverage the 360-degree printable surface of cans to create visually appealing and distinctive packaging that stands out on retail shelves. This aspect is particularly important in the craft beer and flavored alcoholic beverage segments, where unique and creative can designs have become a key differentiator in the market.

Moreover, collaborations and agreements between raw material suppliers and beverage can manufacturers are expected to foster innovation and drive new product development in the beverage cans market. For instance, in January 2024, Novelis, a major sustainable aluminum solutions provider and the global player in aluminum rolling and recycling, entered into a new agreement with Ardagh Group S.A., a global supplier of sustainable aluminum beverage packaging solutions. Under the contract, Novelis will supply aluminum beverage packaging sheets to Ardagh's metal production facilities in North America.

In addition, the recyclability of beverage cans has emerged as a major growth driver, supported by rising environmental awareness among both consumers and brand owners. Aluminum cans exhibit strong circularity through can-to-can recycling, with 71% of cans globally recycled and 33% returned as new cans, significantly outperforming PET and glass. However, substantial untapped potential remains, as a large share of recycled aluminum is still down cycled into other products due to challenges such as contamination, scrap leakage, and alloy incompatibility. While markets such as the U.S. demonstrate very high closed-loop recycling efficiency and countries such as Thailand show strong can-to-can recovery rates, improving collection systems, recycling infrastructure, and alloy management remains critical to unlocking higher circularity worldwide.

Market Concentration & Characteristics

The beverage cans industry is characterized by high capital intensity, driven by the need for advanced high-speed manufacturing lines, precision forming equipment, and sophisticated quality control systems. Large-scale investments are required to achieve economies of scale, operational efficiency, and consistent product quality, creating significant entry barriers for new players. Continuous innovation in light weighting, coating technologies, and high-speed filling compatibility further increases the operational complexity. As a result, industry competitiveness is closely linked to production efficiency, asset utilization, and the ability to rapidly adapt to evolving beverage formulation and packaging requirements.

The industry is highly dependent on aluminum supply chains, making it sensitive to fluctuations in global aluminum prices, energy costs, and trade policies. Raw material typically accounts for a substantial portion of total production costs, exposing manufacturers to margin volatility. Long-term supply contracts, strategic sourcing, recycling integration, and backward linkages into aluminum rolling are widely adopted to mitigate cost risks. This structural dependence underscores the importance of procurement strategy, inventory management, and supplier partnerships as critical success factors in the beverage can market.

Material Insights

Aluminum led the beverage cans market, accounting for a revenue share of over 96.0% in 2025, and is expected to grow at the fastest CAGR of 5.1% over the forecast period. This dominance is due to its infinite recyclability, lightweight nature, superior barrier protection, and strong sustainability profile, which align with regulatory mandates and brand owner commitments to circular packaging. Additionally, cost efficiency at scale, high production speeds, and excellent printability for branding are accelerating its adoption across both alcoholic and non-alcoholic beverage segments, driving the fastest growth rate.

Steel serves as a niche material segment in the market, primarily used in selected carbonated soft drinks and food-beverage hybrid packaging due to its high strength, durability, and pressure resistance. However, its heavier weight, lower recycling economics, and higher logistics costs compared to aluminum limit large-scale adoption. As a result, steel maintains localized and application-specific demand, particularly in cost-sensitive and traditional markets.

Application Insights

Alcoholic beverages led the beverage cans industry, accounting for the largest revenue share of over 38.0% in 2025, driven by the rapid shift from glass bottles to cans in beer, hard seltzers, and ready-to-drink (RTD) cocktails due to superior portability, faster chilling, and enhanced product protection. Additionally, rising consumption of craft beer, premium alcoholic beverages, and outdoor and on-the-go drinking occasions, coupled with sustainability-driven packaging transitions, continues to strengthen demand for beverage cans in this segment.

The fruit & vegetable juices application segment is anticipated to grow at the fastest CAGR of 5.6% during the forecast period, driven by rising health consciousness, increasing demand for functional and natural beverages, and growing preference for preservative-free packaged juices. Additionally, advancements in can lining technologies, superior light and oxygen barrier protection, and expanding urban consumption of on-the-go nutrition products are accelerating the adoption of cans in this segment.

Regional Insights

The beverage cans market in North America held the largest revenue share of over 36.0% in 2025, driven by high per capita consumption of canned beverages, strong presence of major beverage brands, and rapid adoption of sustainable aluminum packaging. Additionally, robust recycling infrastructure, regulatory support for circular economy initiatives, and high penetration of RTD beverages, craft beer, and energy drinks continue to strengthen regional market leadership.

U.S. Beverage Cans Market Trends

The growth of the U.S. beverage cans industry is uniquely driven by aggressive sustainability commitments from major beverage brands, early adoption of high-recycled-content aluminum, and advanced closed-loop recycling ecosystems, which significantly accelerate aluminum can demand. Additionally, high penetration of craft breweries, rapid innovation in hard seltzers and RTD alcoholic beverages, and strong investments in high-speed can manufacturing capacity expansions distinctly position the U.S. as the strategic growth engine of the North American market.

Europe Beverage Cans Market Trends

Europe is the second-largest region in the beverage can industry, in terms of revenue. It accounted for a revenue share of over 24.0% in 2025. The region has experienced increased demand for the personalization of beverages and beverage cans. Besides, the significant presence of many of the prominent beverage manufacturing companies in the region is positively influencing the beverage packaging industry, including the beverage cans market across Europe. Some of the major beverage-producing companies operating in Europe are AB InBev, Diageo, Heineken N.V., Pernod Ricard, Carlsberg Breweries A/S, The Coca-Cola Company, PepsiCo, Red Bull, and Nestlé.

Asia Pacific Beverage Cans Market Trends

The Asia Pacific beverage cans industry is anticipated to grow at the fastest CAGR of 6.8% during the forecast period, driven by rapid urbanization, rising disposable incomes, and surging consumption of RTD beverages, energy drinks, and functional drinks across China, India, and Southeast Asia. Additionally, expanding middle-class populations, increasing investments in domestic can manufacturing capacity, and growing adoption of sustainable packaging solutions are accelerating market expansion across the region.

The China beverage cans market is expected to grow during the forecast period. The presence of major aluminum manufacturers, such as Aluminum Corporation of China Limited, Luneng Jinbei - Yuanping Alumina Refinery, Shandong Weiqiao Aluminum and Power Co., Ltd., and Shandong Xinfa Aluminium Group, in the country has led to an abundance in the supply of the metal, thus making it available at affordable prices for the manufacturers of beverage cans. The recycling rate of metal in the country is quite low compared to that in developed economies; however, it does not have a considerable effect on the beverage cans market, as the demand is met by the production of low-cost virgin aluminum produced in the country.

Key Beverage Cans Company Insights

The beverage cans market exhibits a highly consolidated and intensely competitive environment, dominated by a limited number of large multinational players with extensive global manufacturing footprints, long-term supply contracts with leading beverage brands, and strong technological capabilities. Competition is primarily driven by capacity expansion, cost leadership through scale economies, continuous lightweighting innovation, sustainability-led product development, and strategic geographic expansion, particularly in high-growth regions. High capital intensity, stringent quality standards, and the need for consistent high-volume supply create significant entry barriers, reinforcing the dominance of established players while encouraging mergers, acquisitions, and long-term strategic partnerships to enhance market positioning and operational resilience.

-

In May 2025, VulCan Packaging launched as North America's first commercial-scale manufacturer of aTULC (Aluminum Toyo Ultimate Can) aluminum beverage cans, introducing a revolutionary dry-forming process that eliminates bisphenol-based coatings and water usage for a cleaner, more sustainable product. This next-generation technology enhances shelf life, graphics quality, and recyclability, marking a shift in the U.S. can manufacturing industry.

-

In December 2024, Ball Corporation partnered with Dabur India Limited to launch Real Bites juice in fully recyclable aluminum cans, expanding the Real juice portfolio with a sustainable packaging solution in India. This eco-conscious move aligns with growing consumer demand for convenience and recyclability, as aluminum cans are among the most recycled beverage containers worldwide.

-

In January 2024, NOMOQ, a pioneer and leading provider of digitally printed cans in Europe, launched its Blank Cans Service for European drink brands. This new offering includes blank (undecorated) aluminum beverage cans, which expands NOMOQ's product range beyond its core business of digitally printed cans. This initiative is expected to provide greater flexibility and customization options for European drink brands, enabling them to create unique, personalized packaging solutions for their products.

Key Beverage Cans Companies:

The following key companies have been profiled for this study on the beverage cans market.

- Ball Corporation

- Ardagh Group S.A.

- Toyo Seikan Co., Ltd.

- CPMC Holdings Limited

- Orora Packaging Australia Pty. Ltd.

- CANPACK

- Crown Holdings, Inc.

- Mahmood Saeed Can and End Industry Company Limited (MSCANCO)

- Kian Joo Can Factory Berhad

- SWAN Industries (Thailand) Company Limited

- GZI Industries Limited

- Olayan Group

- Bangkok Can Manufacturing

- Nampak Ltd.

- Envases Group

Beverage Cans Market Report Scope

Report Attribute

Details

Market size in 2025

USD 45.4 billion

Estimated market size in 2026

USD 47.9 billion

Projected market size by 2033

USD 67.4 billion

Growth rate

CAGR of 5.0% from 2026 to 2033

Historical data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, volume in million units, and CAGR from 2026 to 2033

Report coverage

Volume forecast, revenue forecast, competitive landscape, growth factors, and trends

Segments covered

Material, application, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country Scope

U.S.; Canada; Mexico; UK; Germany; France; Italy; Spain; Russia, Belarus; Bulgaria; Czech Republic; Poland; Hungary; China; Japan; India; Australia; South Korea; Kazakhstan; Uzbekistan; Tajikistan; Brazil; Argentina; Peru; Chile; Colombia; South Africa; Ghana; Nigeria; Kenya; Mauritius; Egypt; Iran; Kuwait; Israel; Saudi Arabia; UAE

Key companies profiled

Ball Corporation; Ardagh Group S.A.; Toyo Seikan Co., Ltd.; CPMC Holdings Limited; Orora Packaging Australia Pty. Ltd.; CANPACK; Crown Holdings, Inc.; Mahmood Saeed Can and End Industry Company Limited (MSCANCO); Kian Joo Can Factory Berhad; SWAN Industries (Thailand) Company Limited; GZI Industries Limited; Olayan Group; Bangkok Can Manufacturing; Nampak Ltd.; Envases Group

Customization scope

Free report customization (equivalent up to 8 analyst’s working days) with purchase. Addition or alteration to country, regional & segment scope

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Beverage Cans Market Report Segmentation

This report forecasts revenue & volume growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global beverage cans market report based on material, application, and region:

-

Material Outlook (Volume, Million Units; Revenue, USD Million, 2021 - 2033)

-

Aluminum

-

Steel

-

-

Application Outlook (Volume, Million Units; Revenue, USD Million, 2021 - 2033)

-

Carbonated Soft Drinks

-

Alcoholic Beverages

-

Fruits & Vegetable Juices

-

Other Applications

-

-

Regional Outlook (Volume, Million Units; Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

Russia

-

Belarus

-

Bulgaria

-

Czech Republic

-

Poland

-

Hungary

-

-

Asia Pacific

-

China

-

Japan

-

India

-

Australia

-

South Korea

-

Kazakhstan

-

Uzbekistan

-

Tajikistan

-

-

Latin America

-

Brazil

-

Argentina

-

Peru

-

Chile

-

Colombia

-

-

Middle East & Africa

-

South Africa

-

Ghana

-

Nigeria

-

Kenya

-

Mauritius

-

Egypt

-

Iran

-

Kuwait

-

Israel

-

Saudi Arabia

-

UAE

-

-

Frequently Asked Questions About This Report

Key players include Ball Corporation; Ardagh Group S.A.; Toyo Seikan Co., Ltd.; CPMC Holdings Limited; Orora Packaging Australia Pty. Ltd.; CANPACK; Crown Holdings, Inc.; Mahmood Saeed Can and End Industry Company Limited (MSCANCO); Kian Joo Can Factory Berhad; SWAN Industries (Thailand) Company Limited; GZI Industries Limited; Olayan Group; Bangkok Can Manufacturing; Nampak Ltd.; Envases Group.

Increasing consumption of alcoholic beverages, increasing ban on plastic packaging, and increasing government initiatives for recycling of aluminum material is expected to drive the beverage can market growth.

The global beverage cans market size was valued at USD 45.4 billion in 2025 and is estimated at USD 47.9 billion for 2026.

The global beverage cans market is expected to grow at a CAGR of 5.0% from 2026 to 2033, reaching USD 67.4 billion by 2033.

North America dominated with a 36.0% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

The alcoholic beverages segment led with a 38.0% revenue share in 2025, while fruit & vegetable juices is the fastest-growing application.

Aluminum dominated the beverage cans market with a 96.0% revenue share in 2025 due to its lightweight nature, superior barrier protection, and infinite recyclability, which align strongly with sustainability regulations and brand commitments.

About the Author(s)

Food Safety & Processing Research Team

Consumer Goods · Food Safety & ProcessingThis report was authored by the food safety & processing research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the food safety & processing segment of the consumer goods industry. All findings are based on proprietary consumer goods databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.