- Home

- »

- Medical Devices

- »

-

Biocompatibility Testing Services Market Report, 2026-2033GVR Report cover

![Biocompatibility Testing Services Market (2026 - 2033)Report]()

Biocompatibility Testing Services Market (2026 - 2033)

Size, Share & Trends Analysis Report By Test Type, By Development Stage, By Industry Application, By End Use (Medical Device Manufacturers, CRO & CDMO), By Region, And Segment Forecasts

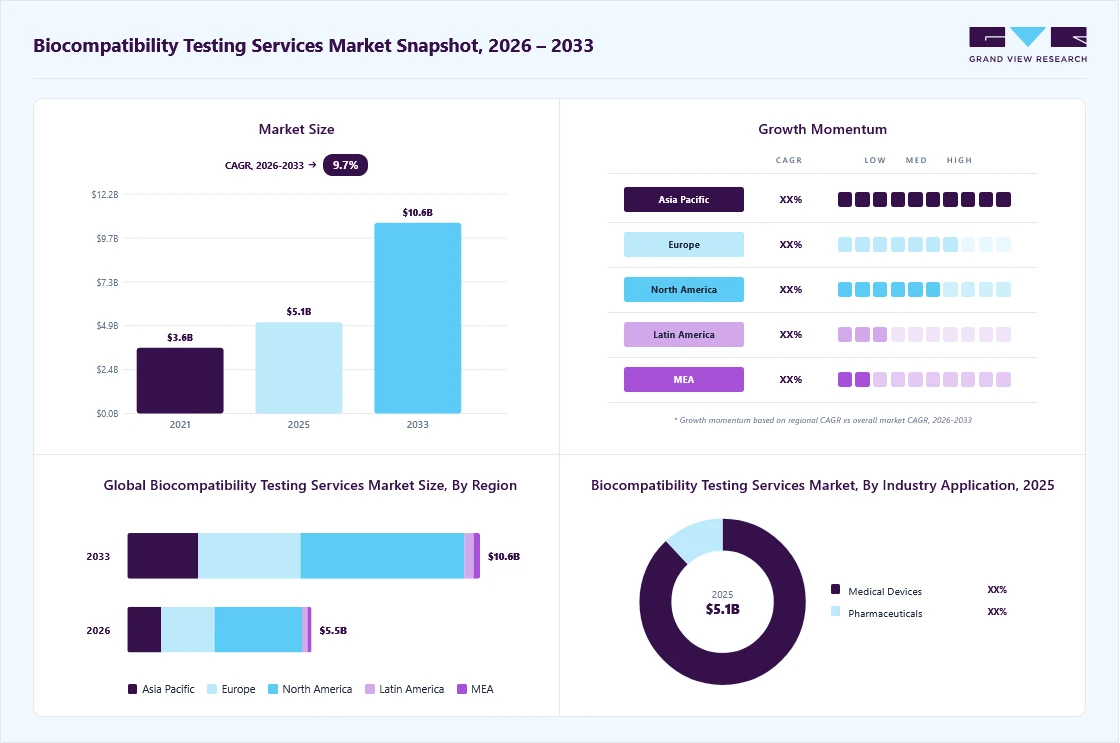

Market Size, 2025

$5.1BMarket Estimate, 2026

$5.5BMarket Forecast, 2033

$10.6BCAGR, 2026–2033

9.7%Biocompatibility Testing Services Market Summary

The global biocompatibility testing services market size was valued at USD 5.1 billion in 2025 and is projected to grow from USD 5.5 billion in 2026 to USD 10.6 billion by 2033, at a CAGR of 9.7% from 2026 to 2033. The North America held the largest share of 47.0% of the global market in 2025. The rising need for regulations and ISO 10993 compliance is driving demand for biocompatibility testing services, as companies must conduct biological assessments to obtain approval or make changes to their devices.

Key Market Trends & Insights

- By test type: Material & chemical characterization segment held the largest market share of 24.1% in 2025.

- By development stage: Clinical segment held the largest market share in 2025.

- By industry application: Medical devices segment held the largest market share in 2025.

- By end use: Medical device manufacturers segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: North America (47.0% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest share in 2025

Market Size & Forecast

- Market size in 2025: USD 5.1 Billion

- Estimated market size in 2026: USD 5.5 Billion

- Projected market size by 2033: USD 10.6 Billion

- CAGR (2026-2033): 9.7%

In addition, the increase in demand for biologics and combination products is expected to drive extractable and leachable testing, especially in drug container-closure system applications, thereby boosting market growth.Increasing regulatory pressure, the growing complexity of medical devices, advancements in the use of biologics and combination products, and outsourcing services to CROs are among several key factors contributing to increased demand for ISO 10993-compliant biocompatibility testing, in turn driving the growth of the biocompatibility testing services market over the forecast period. Additionally, the product iteration and the development of materials used in medical devices further support the number of biological tests conducted on various devices.

")

In addition, the regulatory standards, such as those required by the U.S. FDA and the EMA, have mandated the complete safety analyses of medical devices used across several implants and delivery systems. The growing use of advanced materials in devices for heart disorders and orthopedics is driving greater emphasis on sensitization, irritation, and systemic toxicity testing. As a result, the demand for biological testing remains steady, irrespective of new devices being introduced or existing ones being improved.

Furthermore, due to the high complexity of medical devices and biomaterials, the testing process became multistage. This implies the need for cytotoxicity, genotoxicity, and implantation testing for each product at certain stages, thereby increasing testing efforts per product. Similarly, developments in polymer chemistry and implantable materials create greater unpredictability in biological reactions, making it necessary to repeat the cycle of testing after the first approval. Moreover, the emergence of combination products and drug delivery systems is increasing the demand for extractables and leachables testing, especially in drug container closures, where material interactions may pose serious risks. Additionally, the introduction of biologics and combination products requires new testing procedures, including assessing drug-device interactions from a chemical and toxicological perspective.

On the other hand, high prices of testing panels and lengthy study durations may pose obstacles for small manufacturers, and the inconsistencies in regulations worldwide are preventing the harmonization of global standards. However, the market is expected to continue growing steadily due to mandatory compliance requirements and the increased complexity of products.

Opportunity Analysis

The expanding adoption of innovative biomaterials, an increase in the development pipeline for combination products, higher demand for extractables & leachables analysis, and outsourcing of biocompatibility tests are anticipated to create significant growth opportunities for the biocompatibility testing services market. These prospects are supported by growing product complexity for cardiovascular, orthopedic, and implantable devices, which necessitate a thorough biological assessment. Besides, there is an increased demand for personalization in the field of medical devices & implants that require customized testing procedures. In addition, the rapidly evolving field of biologics and advanced drug delivery technologies has created opportunities in the pharmaceutical industry, especially in drug container closure systems.

The rising need for extractables and leachables studies offers substantial growth potential, as the demand for thorough chemical characterization from drug and combination product manufacturers is increasingly important in ensuring safety and stability throughout the life cycle. Also, the development of technologies in fields like mass spectrometry and chromatography has facilitated the discovery of compounds present in trace levels, making the testing services provided by the CROs significant. Additionally, the increasing use of in vitro methods of alternative testing has created opportunities for more efficient, cost-effective screening processes, especially during the early stages of development when in vivo testing is not possible. For instance, the increased application of organ-on-a-chip technology in preclinical testing has improved the prediction of biological responses without resorting to animal experiments.

Furthermore, the increased use of outsourcing, as small and medium-sized companies become more reliant on specialized testing providers for compliance and specialized technical knowledge, is likely to create new opportunities for market growth. Nevertheless, a shortage of skilled workers and the need for substantial investments in test equipment may limit the expansion rate, while changing regulatory requirements may complicate standardizing the services offered. Thus, the industry offers strong near-term growth potential driven by technological innovations, expanding regulations, and rising complexity in the biological evaluation process for healthcare products.

Impact of U.S. Tariffs on the Biocompatibility Testing Services Market

The effect of tariffs imposed by the U.S. on medical devices, polymers, and laboratory supplies has impacted the market through higher costs of inputs, altered supply chains, and localization of testing processes according to U.S. FDA regulations. Such practices have also affected manufacturers that use imported materials in their production, as the higher cost of purchasing these materials increases testing expenditures. The increase in the costs of specialty polymers and reagents used in material characterization and extractables analysis has raised total testing expenses, thereby boosting CRO service pricing.

The rise in raw materials prices has prompted manufacturers to change formulations or switch suppliers, requiring additional biocompatibility testing cycles that include cytotoxicity and sensitization tests to comply with ISO 10993 regulations. Besides, the fluctuations in the supply chain have made requalification tests more common, as even slight changes in material necessitate an extensive biological risk assessment before submission. For instance, the higher tariffs on medical components from China caused some U.S. medical device makers to use other Southeast Asian sources, leading to new rounds of testing.

Nonetheless, rising costs and lengthy validation processes might put pressure on small-scale manufacturers, while variations in tariff policies make long-term planning challenging for testing services providers.

Technological Advancements

The development in the fields of analytical chemistry, like LC-MS (Liquid Chromatography-Mass Spectrometry) and GC-MS (Gas Chromatography-Mass Spectrometry), has allowed the identification of trace levels of extractables in materials, helping improve toxicological risk assessment. The increased sensitivity in the process of detection is widening the range of characterization of chemicals, thus making the study of extractables and leachables important.

Furthermore, the use of 3D models and organs-on-chip technology helps simulate effects on humans at various biological endpoints, such as irritation and sensitization, thereby limiting the need for animal studies. Moreover, the use of these models has improved reliability in the prediction of outcomes and has decreased the time taken in the process of testing.

These have helped speed up safety tests and make effective regulatory submissions with evidence-based data. Additionally, innovations in high-throughput automated screening systems have improved laboratory efficiency by enabling simultaneous experiments across multiple screens. This has enabled CROs to scale their business processes and handle increased test volumes effectively. The formulation of specialized testing procedures for biomaterials is supporting the increasing use of resorbable polymers and nanomaterials in medical devices and drug delivery systems.

Pricing Model Analysis

Pricing models in the biocompatibility testing services industry have shifted from a transactional approach to a more integrated, value-driven model aligned with ISO 10993 standards, owing to the growing complexity of testing and the rising regulatory compliance demands that affect service valuation strategies. The fee-for-service model is still prevalent in routine tests like cytotoxicity and irritation, in which prices depend on the time required for each test, the level of preparation needed, and the level of detail in the reports, ultimately resulting in escalating costs as the number of tests increases. In addition, project-based pricing models are becoming more popular among manufacturers of high-risk medical devices and combination products, in which a bundle of fees covers multiple biological endpoints and toxicity studies.

Moreover, retainer-based pricing models have become prevalent among major pharmaceutical and medical device manufacturers, in which repetitive testing needs across the company’s pipelines are covered by negotiating favorable pricing terms and reserving capacity within laboratories. Such deals facilitate consistent turnaround times and minimize the variation in per-project costs, especially for clients with ongoing product development processes.

The high-level service areas, such as extractable/leachable and toxicological hazard analyses, are progressively charged based on complexity, analysis, and criticality, as these analyses involve specialized equipment and sophisticated interpretation. The costs are determined by parameters such as the number of compounds detected, the level of sensitivity, and the amount of data required to compile comprehensive reports. In addition, geographic diversity in service delivery and laboratory expertise is playing an important role in pricing variations, whereby developed countries charge more due to advanced facilities and compliance regulations.

Furthermore, the small-sized manufacturers and early-stage developers can face budget constraints due to the high initial costs for testing services, thus preventing them from adopting more complex testing panels. Thus, the pricing structures have been slowly moving towards an integrated model, which is based on the expertise of the test providers.

Market Concentration & Characteristics

The biocompatibility testing services market growth stage is medium, with the pace of growth accelerating. The market is characterized by the degree of innovation, level of M&A activities, regulatory impact, service expansion, and regional expansion.

The market is moving forward due to the use of automated laboratory processes, high-throughput screening, and sophisticated analysis technologies like LC MS and GC MS. Moreover, the inclusion of in vitro 3D tissue models and AI-based toxicological risk assessment techniques in safety evaluations is enhancing the prediction of biological responses and making the process more efficient. Additionally, continued investments in instruments, biomaterial testing methods, and advanced digital analytics are helping CROs deliver faster, more accurate test results.

Changes in regulations, such as the EU MDR and the U.S. FDA, are expanding the scope of services offered by biocompatibility testing service providers. In addition, regulatory compliance requires thorough biological evaluation plans and testing procedures, which, in turn, generate new opportunities. Thus, rising compliance costs are creating opportunities for CROs well-versed in regulations, making them key partners in product development.

The number of M&A activities in the biocompatibility testing services industry is on the rise due to the need to expand laboratory testing capacity, capabilities, and geographic reach. Furthermore, there is an increased effort to provide customers with integrated testing services, including analysis for chemical characterization, toxicology, and microbiology. Through the acquisition of niche and regional laboratories, service providers can improve their capabilities and competitive advantage.

Service expansion has become a popular growth strategy in the biocompatibility testing services industry, as service providers have gone beyond just providing stand-alone services to offering integrated services. Such services include biological evaluation plans, extractables and leachables testing, toxicology risk assessments, and regulatory affairs. Integrated service offerings make it easier for clients to collaborate with the service provider, thereby enabling a faster time-to-market.

Increased geographical coverage continues to be important as the laboratories are set up in regions that have a lot of demand for their services, like North America, Europe, and the Asia Pacific. Also, the emergence of developing economies brings cost benefits, along with increased production of medical devices, in countries like China and India. Regional expansion allows the firms to cater to their clients with local testing facilities.

Test Type Insights

In 2025, the material and chemical characterization segment held the largest revenue share of 24.14%. The segment growth is attributed to its essential role in assessing safety. It is always the initial step in the biological evaluation as per the ISO 10993 standards, allowing the identification of extractable/leachable substances from the material used in a medical device. It is a compulsory requirement for almost all medical devices, irrespective of their type. The growing complexity of polymers and combination products is further driving the need for such testing. Moreover, regulatory authorities have placed greater emphasis on risk-based assessment methods, making chemical characterization an essential tool prior to conducting in vivo tests. It also helps lower overall testing costs by eliminating redundant biological evaluations.

The hemocompatibility test segment is expected to grow significantly during the forecast period. The segment is driven by the rise in the use of cardiovascular and blood-related medical devices. Hemocompatibility tests assess the effects of biomaterials on blood components, including coagulation, hemolysis, and thrombogenesis. The rise in minimally invasive techniques and the adoption of implants has, in turn, increased the demand for such tests. Moreover, in vitro and ex vivo models are becoming increasingly advanced, improving efficiency and reducing reliance on animal testing. Furthermore, the growth in vascular devices, stents, and catheters has boosted adoption rates.

Development Stage Insights

The clinical segment accounted for the largest share of the biocompatibility testing services market in 2025. The issue of biocompatibility persists at the clinical level, especially for products used for extended periods or those considered very risky. The regulatory authorities insist on comprehensive clinical data for the approval and marketing of medical products. This can also be attributed to the rising complexity of conducting clinical trials and developing customized medical devices.

The preclinical segment is anticipated to grow significantly during the forecast period, attributed to the need to evaluate risks early in the developmental process. The preclinical biocompatibility testing is primarily conducted before clinical trials to assess potential hazards associated with products and to comply with regulatory requirements. With the growing use of risk-based assessment methodologies under ISO 10993, preclinical tests will become increasingly important. In addition, increased company spending on early testing will drive growth in the preclinical segment in the near future.

Industry Application Insights

The medical devices segment dominated the biocompatibility testing services industry, with the largest revenue share in 2025. The segment is driven bystrict safety guidelines applicable to all device classes. The compliance with regulatory guidelines requires a detailed biological assessment before product launch, especially under regulations such as those of the European Medicines Agency and ISO international standards. Furthermore, technological advancements in implantable and wearable devices are another contributing factor to the segment's growth. The growth in chronic disease prevalence will continue to encourage innovation in cardiovascular, orthopedic, and neurology devices. Biomaterials innovation requires regular assessment for efficacy, which is another factor promoting the growth of the medical devices sector.

The pharmaceuticals segment is expected to grow significantly during the forecast period. The growth is driven by increasing demand for the development of combination products and sophisticated drug delivery systems. There is also an increased need for biocompatibility testing of packaging materials, injection systems, and container closure systems. The increased regulatory demands, especially from agencies such as the U.S. FDA, for the extraction and leakage analysis of materials, are also anticipated to drive the segment’s growth.

End Use Insights

The medical device manufacturers segment dominated the market with the largest revenue share in 2025, attributed to their inherent obligation to ensure that all their products undergo rigorous testing to ensure safety and regulatory compliance. The growing number of innovations and investment in the development of new types of devices, such as implantable, wearable, or minimally invasive devices, has increased the volume of testing services. The testing requirements as per regulations from authorities such as the FDA and ISO 10993 across multiple endpoints are also anticipated to create demand for such services. The larger players in this industry use hybrid approaches, conducting basic testing in-house and outsourcing complex testing to specialized third-party organizations. At the same time, smaller firms depend entirely on such firms.

The contract research organizations (CROs) and contract development and manufacturing organizations (CDMOs) segment is expected to grow significantly during the forecast period. The segment growth is driven by increasing outsourcing in the medical device and pharmaceutical sectors. The increasing outsourcing activities are aimed at cutting down costs, speeding up operations, and enabling access to advanced testing procedures. Moreover, many smaller and medium-sized companies lack the essential in-house expertise; therefore, outsourcing biocompatibility studies is necessary. Furthermore, the clinical pipelines, along with combination products, are also driving increased outsourcing activities. Thus, due to these factors, the CRO and CDMO segment is registering the highest growth in end-use.

Regional Insights

North America dominated the global biocompatibility testing services market in 2025, accounting for a revenue share of 47.0%. The market growth is driven by strict regulatory compliance, a high level of medical device innovation, increasing use of biologics, and growing outsourcing practices. There are precise requirements imposed on medical devices by the FDA and ISO 10993 in North America, which positively impact the growth of the market during the forecast period. Also, the high number of Class II & Class III devices requiring approval drives increased demand for cytotoxicity, sensitization, and systemic toxicity testing at all stages of development. Moreover, the use of combination products and complex drug delivery systems is growing rapidly, resulting in increased extractables & leachables testing requirements, especially in the pharmaceutical industry.

Furthermore, the growth in biologics and cell-based therapy is also fueling the need for material safety evaluations, particularly in drug packaging systems, where interaction concerns persist. In addition, the presence of several well-established CROs along with the sophisticated lab facilities is helping in reducing turnaround times and achieving maximum efficiency in operations, which is also driving the market growth. In addition, the increased focus by regulatory agencies on developing detailed biological assessment programs is promoting outsourcing services, which is leading to greater use of toxicology risk assessment services.

U.S. Biocompatibility Testing Services Market Trends

The strengthening of regulatory control, a significant number of medical device applications, an increasing trend towards biologics, and the use of CROs are major factors propelling the market growth, along with strong mandates from the U.S. FDA. Due to the large number of Class II and Class III devices, there is increased demand for cytotoxicity, sensitization, and systemic toxicity testing across different stages of development, resulting in increased testing per individual product. In addition, the growing trend of combination drugs, in addition to sophisticated drug delivery methods, will lead to the increased need for extractable and leachable studies, especially for the drug container/closure system.

With an increase in development in the areas of biologics and cell-based therapies, there is an emerging requirement for conducting material compatibility tests, particularly in the case of product-contact surfaces that could get contaminated easily. Further, there is a strong availability of prominent CROs with well-developed testing facilities, thereby ensuring faster testing cycles. However, the high costs involved with testing compliance, along with strict regulatory norms, might prove to be barriers for small-scale manufacturers.

The Canada Biocompatibility Testing Services market is expected to grow at a significant CAGR during the forecast period. The continuous alignment of regulatory guidelines with Health Canada is ensuring steady demand for biocompatibility testing services in Canada, where approvals for medical devices necessitate biological evaluation. In addition, the market is being driven by increased use of implantable medical devices and combination products, thereby leading to demand for cytotoxicity testing, sensitization testing, and extraction & leaching studies. In addition, expansion in the fields of biologics and drug delivery technology is driving the need for material compatibility testing within the pharmaceutical industry.

Europe Biocompatibility Testing Services Market Trends

The growth of the Europe biocompatibility testing services industry is driven by increasing regulatory stringency under the EU MDR and adherence to ISO 10993 standards. Besides, the rising need to conduct biological evaluations for newly manufactured medical devices and those already in use. As a result of the shift towards the new EU MDR, the re-certification process has increased, leading to more testing for cytotoxicity, sensitization, and systemic toxicity. In addition, the growing adoption of combination products and drug-delivery devices will drive demand for studies on extractables & leachables, especially in the pharmaceutical segment.

There have been growing complexities in implantable and high-risk devices within the cardiovascular and orthopedic sectors, increasing the scope of testing and validation. Additionally, the presence of dedicated CROs and notified bodies in the European region will enable more robust analytics and regulatory services. Nonetheless, there may be limitations regarding testing and approval under the EU MDR, posing challenges for manufacturers due to high compliance costs.

The Germany biocompatibility testing services market is expected to grow during the forecast period. Strict compliance norms in line with EU MDR are expected to drive the market growth as the manufacturing companies conduct elaborate biological testing of the newly developed products, as well as older devices. Also, the presence of several advanced medical device manufacturers in the cardiovascular and orthopedic segments will increase the intensity of biocompatibility testing for complex implantable devices.

The increasing use of combination products and drug delivery systems will boost the number of extractables & leachables testing studies, especially in pharmaceutical applications with a rigorous regulatory framework. In addition, the growing trend towards innovation in the biomaterial segment is expected to drive demand for testing bioresorbable and polymer-based devices. However, a lack of adequate testing capacity and strict compliance standards under the EU MDR can lead to delays, as well as the high costs of testing operations.

The biocompatibility testing services market in the UK is expected to grow during the forecast period. Aligning regulations with the Medicines and Healthcare products Regulatory Agency (MHRA) is contributing to the market dynamics for biocompatibility testing services in the UK. There will be an increase in the number of biocompatibility tests, such as cytotoxicity, sensitization, and systemic toxicity tests, due to the rise in medical device approvals and revisions amid changes in the post Brexit scenario. The increase in combination products and drug delivery systems will result in high demand for extractables and leachables testing services, especially in pharmaceutical products. The prevalence of biologics and cell-based therapies is growing in the UK, driving high demand for material compatibility and endotoxin testing of drug containers. Additionally, the availability of CROs and academic research institutes in the region will foster innovation in testing techniques and technologies. On the other hand, the emergence of personalized implants and devices will drive manufacturers to conduct more sophisticated and repetitive tests. However, divergent regulations and complex compliance requirements may hinder market growth and lengthen approval timelines.

Asia Pacific Biocompatibility Testing Services Market Trends

Asia Pacific is expected to grow at the fastest CAGR over the forecast period. The factors that have been contributing to the market growth include an increase in the manufacture of medical devices, the conduct of clinical trials, the usage of biologics, and the outsourcing of tests to regional CROs. Countries such as China, India, and Japan are experiencing high growth rates, and there is a growing need for biocompatibility testing for cytotoxicity, sensitization, and systemic toxicity, driven by increased local and foreign production and the export of medical devices.

The region offers cost benefits alongside increased laboratory capacity, leading global companies to outsource their testing processes to local organizations. Additionally, technological advancements within the cardiovascular and orthopedic sectors are making it more complicated to test implantable devices, increasing the frequency of retesting. On the other hand, government efforts to enhance regulatory policies have improved quality and fostered confidence in testing capabilities. Nevertheless, discrepancies in regulatory guidelines among different nations and a lack of advanced testing laboratories in specific regions might lead to inconsistencies in the provision of services.

The China biocompatibility testing services market is projected to grow during the forecast period. The rapid scale-up of local medical device manufacturing, regulated by the National Medical Products Administration (NMPA), is creating increased demand for locally conducted biocompatibility tests, enabling exports of such products. Furthermore, increased regulatory scrutiny by the NMPA will positively impact the China biocompatibility testing service market, driven by the growth of manufacturing and the export of medical equipment within the country. The growing trend towards manufacturing high-risk and implantable devices will drive the demand for tests such as cytotoxicity, sensitization, and systemic toxicity, among others, during various stages of development. Also, the development of combination products and biologics is increasing, thereby boosting the need for extractables and leachables testing services in the pharmaceutical industry.

The biocompatibility testing services market in Japan is driven by strict government regulations by the Pharmaceuticals and Medical Devices Agency (PMDA), along with conformity to ISO 10993 standards, as the companies are increasingly focused on biological assessment. The presence of a large number of precision medical device makers in the field of cardiovascular, orthopedic, dental, neurological, ophthalmic, and general surgical medical devices is anticipated to increase the demand for cytotoxicity, sensitization, and implantation tests. In addition, the increased use of combination products and drug-delivery systems will lead to greater testing.

The India biocompatibility testing services market is expected to grow during the forecast period. The emerging trend of increased regulatory compliance from the Central Drugs Standard Control Organization (CDSCO) is driving the market growth as a result of the growing indigenous manufacture of medical devices due to the initiative of import substitution. An increase in the manufacture of implantable and high-risk devices is driving greater demand for analyses of cytotoxicity, sensitization, and systemic toxicity. The increasing use of combination products and the expansion of the pharmaceutical industry are driving higher demand for extractable and leachables analysis of drug containers. The Indian industry benefits from cost efficiencies along with the emergence of CROs, which has led to the outsourcing trend among foreign and indigenous companies.

Latin America Biocompatibility Testing Services Market Trends

Growing regulatory policies, increased imports of medical devices, increased pharmaceutical production in the region, and increased outsourcing of testing to regional CROs are among the factors fueling the market growth. Countries like Brazil and Mexico are seeing increased demand for cytotoxicity, sensitization, and systemic toxicity testing services due to increasingly stringent regulations for the approval of these devices.

The stringent timeframes for registering medical devices with Agência Nacional de Vigilância Sanitária (ANVISA) and the stricter auditing by Comisión Federal para la Protección contra Riesgos Sanitarios (COFEPRIS) are prompting repeat biocompatibility tests on imported Class II and Class III devices, especially regarding material equivalency and label changes in accordance with ISO 10993 standards. The increased use of locally manufactured polymers and packaging materials in pharmaceutical manufacturing centers in Brazil is driving demand for extractables and leachables analyses, as supply chains have changed, necessitating revalidation of material safety. The lack of advanced laboratories in the region is driving cross-border shipments of samples to U.S.-based contract research organizations, delaying the process and increasing reliance on external testing resources.

The biocompatibility testing services market in Brazil is impacted by factors such as improvements in regulatory supervision and compliance with ISO 10993 standards, driving the demand for biocompatibility testing services since approval of medical devices involves performing a complete biological assessment. The growing need for biocompatibility testing of implantable devices and high-risk devices is likely to fuel market growth. The presence of regional contract research organizations (CROs) will contribute to this growth, but may be limited by technological imports and regulatory issues.

Middle East and Africa Biocompatibility Testing Services Market Trends

The MEA biocompatibility testing services industry’s growth is driven by factors such as changing regulations, rising investments in the healthcare industry, increased imports of medical equipment, and rising pharmaceutical production. Countries like Saudi Arabia, the UAE, and South Africa are experiencing increased demand for cytotoxicity, sensitization, and systemic toxicity testing for approval of the devices used.

A highly dependent region on medical device imports is creating a greater need for product certification through tests in the region before launching in the market. In addition, increased spending on healthcare facilities and the gradual expansion of CRO services are making testing more accessible. Furthermore, government policies towards the localization of drug production will add to the demand for materials safety testing. However, limitations such as a lack of advanced facilities and inconsistent enforcement of regulations might affect service quality and the time required.

The biocompatibility testing services market in South Africa is expected to grow at a significant CAGR during the forecast period, attributed to the strengthening of the regulatory control provided by the South African Health Products Regulatory Authority (SAHPRA), contributing to the development of the market in South Africa. The growing number of imported medical devices and the slow increase in the production of medical devices in the country are promoting the demand for biocompatibility testing services. Moreover, the growing uptake of combination products is boosting the demand for extractables and leachables testing.

The UAE biocompatibility testing services market is anticipated to grow during the forecast period. The increasing regulatory control of the Ministry of Health and Prevention is defining the UAE market for biocompatibility testing services, since imported medical devices necessitate extensive biological assessment before entering the market. The growing utilization of sophisticated medical devices is generating high demand for biocompatibility testing, including cytotoxicity, sensitization, and systemic toxicity, among others. Moreover, the rising number of combination products, along with the expansion of the pharmaceutical manufacturing industry, is increasing the need for biocompatibility testing.

Key Biocompatibility Testing Services Company Insights

The key market players are adopting strategic initiatives such as service launches, mergers & acquisitions, partnerships & agreements, and expansions to gain a competitive edge in the market. For instance, in January 2026, NAMSA acquired select assets of Labcorp’s early development medical device testing business, expanding its capabilities and giving it an edge in biocompatibility, microbiology, and preclinical testing services.

Key Biocompatibility Testing Services Companies:

The following key companies have been profiled for this study on the biocompatibility testing services market.

- NAMSA

- Eurofins Scientific SE

- SGS SA

- Intertek Group

- Charles River

- Nelson Laboratories, LLC

- Pacific BioLabs

- Labcorp (Toxikon Corporation)

- Medistri SA

- Wickham Laboratories

- Pace Analytical Services

Recent Developments

-

In November 2025, Eurofins Medical Device Services made a strategic acquisition of ac.biomed to bolster its capabilities in the area of medical device testing and biological evaluation testing services.

-

In January 2025, NAMSA acquired the U.S.-based operations of WuXi AppTec that tested medical devices to develop a broader range of laboratory testing services, especially for biocompatibility and preclinical studies in North America.

Biocompatibility Testing Services Market Report Scope

Report Attribute

Details

Market size in 2025

USD 5.1 billion

Estimated market size in 2026

USD 5.5 billion

Projected market size by 2033

USD 10.6 billion

Growth rate

CAGR of 9.7% from 2026 to 2033

Actual data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Test type, development stage, industry application, end use, and region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; Italy; Spain; Denmark; Sweden; Norway; Japan; China; India; Thailand; South Korea; Australia; Brazil; Argentina; South Africa; Saudi Arabia; UAE; Kuwait; Oman; Qatar

Key companies profiled

NAMSA; Eurofins Scientific SE; SGS SA; Intertek Group; Charles River; Nelson Laboratories, LLC; Pacific BioLabs; Labcorp (Toxikon Corporation); Medistri SA; Wickham Laboratories; Pace Analytical Services

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Biocompatibility Testing Services Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global biocompatibility testing services market based on test type, development stage, industry application, end use, and region:

-

Test Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Material / Chemical Characterization

-

Cytotoxicity Testing

-

Sensitization Testing

-

Irritation & Reactivity Testing

-

Systemic Toxicity Testing

-

Hemocompatibility Testing

-

Implantation Testing

-

Pyrogenicity Testing

-

Others

-

-

Development Stage Outlook (Revenue, USD Million, 2021 - 2033)

-

Preclinical

-

Clinical

-

-

Industry Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Medical Devices

-

Cardiovascular Devices

-

Orthopedic Devices

-

Dental Devices

-

Neurological Devices

-

Ophthalmic Devices

-

General Surgical Devices

-

Aesthetic & Cosmetic Devices

-

Others

-

-

Pharmaceuticals

-

Drug-Container Closure Systems

-

Drug Delivery Systems

-

Combination Products

-

Others

-

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Medical Device Manufacturers

-

Pharmaceutical & Biopharmaceutical Companies

-

CRO & CDMO

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

Japan

-

China

-

India

-

Australia

-

Thailand

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

South Africa

-

UAE

-

Saudi Arabia

-

Kuwait

-

Qatar

-

Oman

-

-

Frequently Asked Questions About This Report

The material and chemical characterization segment led with a 24.1% revenue share in 2025, while the hemocompatibility test segment is expected to grow significantly.

The clinical segment held the largest revenue share in 2025, while the preclinical segment is is anticipated to grow significantly.

The medical devices segment held the largest revenue share in 2025, while the pharmaceuticals segment is expected to grow significantly.

Medical device manufacturers segment held the largest share in 2025, while the contract research organizations (CROs) and contract development and manufacturing organizations (CDMOs) segment is is expected to grow significantly during the forecast period.

The global biocompatibility testing services market size was estimated at USD 5.1 billion in 2025 and is expected to reach USD 5.5 billion in 2026.

The global biocompatibility testing services market is expected to grow at a compound annual growth rate of 9.7% from 2026 to 2033 to reach USD 10.6 billion by 2033.

Some key players operating in the biocompatibility testing services market include NAMSA, Eurofins Scientific SE, SGS SA, Intertek Group, Charles River Laboratories, Nelson Laboratories, LLC, Pacific BioLabs, Labcorp (Toxikon Corporation), Medistri SA, Wickham Laboratories, and Pace Analytical Services, among others.

Key factors that are driving the biocompatibility testing services market growth include the rising need for regulations and ISO 10993 compliance, an increase in demand for biologics and combination products, which is expected to drive extractable and leachable testing, especially in drug container-closure system applications, further contributing to market growth.

North America dominated the biocompatibility testing services market with a share of 47.0% in 2025. The market growth is driven by strict regulatory compliance, a high level of medical device innovation, increasing use of biologics, and growing outsourcing practices. Besides, growing requirements imposed on medical devices by the FDA and ISO 10993 in North America are further contributing to the market growth.

About the Author(s)

Medical Devices Research Team

Healthcare · Medical DevicesThis report was authored by the medical devices research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the medical devices segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.