- Home

- »

- Healthcare IT

- »

-

Biosimulation Market Size, Share, Trends Report, 2026-2033GVR Report cover

![Biosimulation Market Size, Share & Trends Report]()

Biosimulation Market (2026 - 2033) Size, Share & Trends Analysis Report By Product (Software, Services), By Application (Drug Discovery & Development), By Therapeutic Area, By Delivery Model, By Pricing Model, By End-use, By Region, And Segment Forecasts

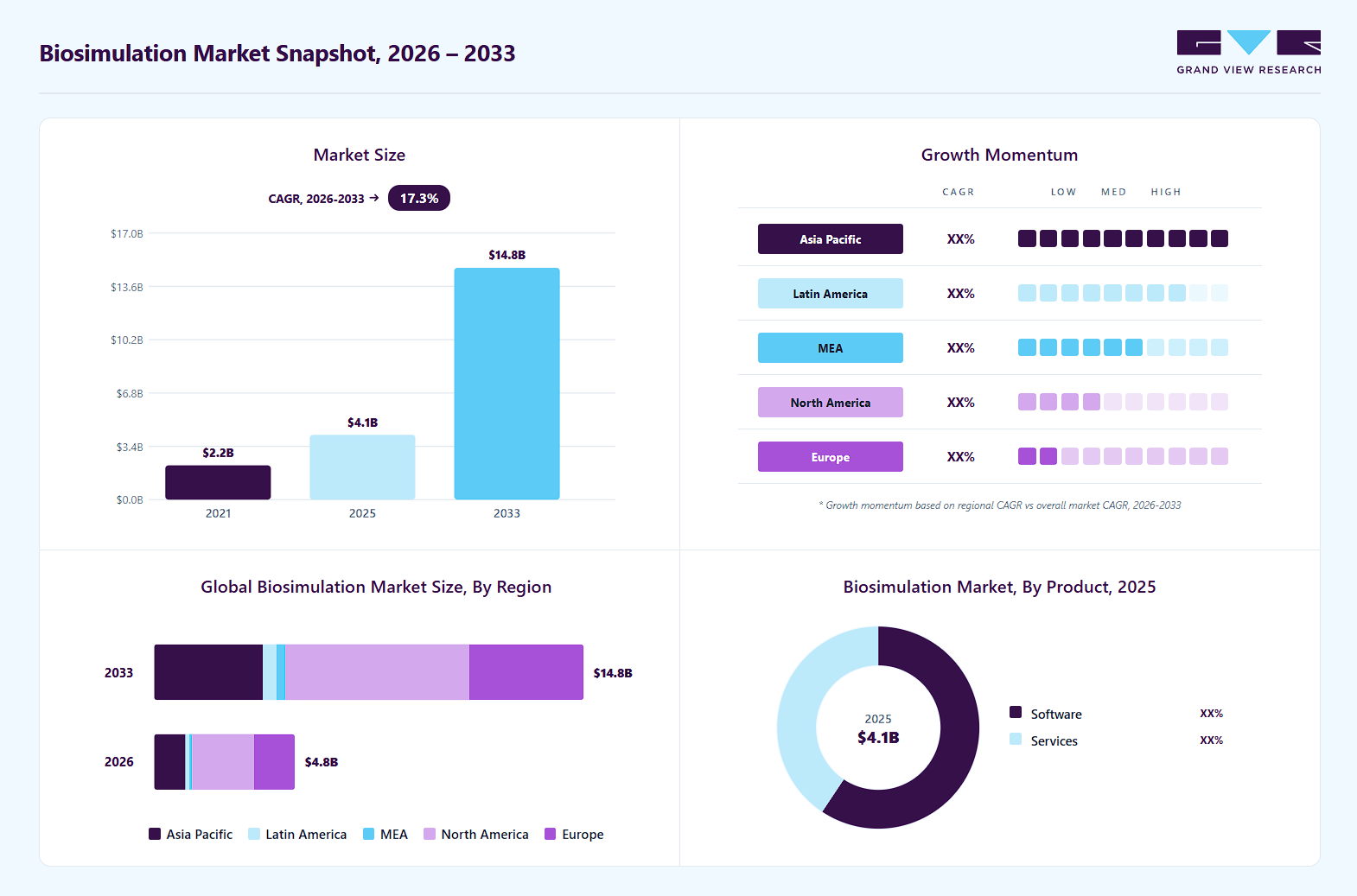

Market Size, 2025

$4.1BMarket Estimate, 2026

$4.8BMarket Forecast, 2033

$14.8BCAGR, 2026–2033

17.3%Biosimulation Market Summary

The global biosimulation market size was valued at USD 4.1 billion in 2025 and is projected to grow from USD 4.8 billion in 2026 to USD 14.8 billion by 2033, at a CAGR of 17.3% from 2026 to 2033. The market in North America dominated with a revenue share of 44.2% in 2025. This growth is driven by the increasing incidence of drug relapse cases due to drug resistance in diseases such as cancer, tuberculosis, and other bacterial infections.

Key Market Trends & Insights

- By product: Software segment dominated the market, with a revenue share of 59.4% in 2025.

- By application: Drug development segment held the largest market share of 55.4% in 2025.

- By pricing model: License-based model segment held the largest revenue share in 2025.

- By end use: Life science companies segment accounted for the largest revenue share in 2025.

Regional Highlights

- Largest regional market: North America (44.2% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 4.1 Billion

- Estimated market size in 2026: USD 4.8 Billion

- Projected market size by 2033: USD 14.8 Billion

- CAGR (2026-2033): 17.3%

")

These trends are key drivers of market growth, underscoring the critical need to integrate biosimulation into the early development of a new generation of drugs. In addition, the rising demand for biosimulation tools among researchers, fueled by technological advancements and software upgrades, is expected to further enhance market growth.Market Dynamics

The growing regulatory acceptance of biosimulation and model-informed approaches is accelerating the adoption of biosimulation platforms across the pharmaceutical industry. Regulatory agencies such as the U.S. Food and Drug Administration are increasingly promoting the use of pharmacokinetic/pharmacodynamic (PK/PD) modeling, physiologically based pharmacokinetic (PBPK) modeling, and clinical trial simulation to improve drug development efficiency and optimize dose selection. For instance, in January 2026, the FDA highlighted updates to its Model-Informed Drug Development (MIDD) Paired Meeting Program, which supports direct collaboration between sponsors and FDA experts for integrating simulation-based evidence into regulatory decision-making. This is encouraging pharmaceutical and biotechnology companies to invest in biosimulation software to reduce clinical trial burden, enhance predictive accuracy, and accelerate regulatory approvals.

The increasing focus on personalized medicine is driving demand for biosimulation tools capable of predicting patient-specific therapeutic responses. Biosimulation enables researchers to model variations in genetics, physiology, and disease progression to evaluate how different patient populations may respond to specific drugs or treatment regimens. This supports optimized dose selection, improved therapeutic efficacy, and reduced adverse drug reactions. Moreover, the growing adoption of pharmacogenomics and precision medicine approaches is further accelerating the need for advanced biosimulation platforms that can integrate genomic and clinical data into predictive drug development models.

Different biosimulation platforms often use different data formats, algorithms, and simulation methodologies, leading to inconsistent predictive outcomes and limited cross-platform interoperability. In addition, regulatory agencies across regions continue to have evolving, non-uniform guidelines for the acceptance of simulation-based evidence in drug development and approval processes. These factors increase validation requirements, prolong implementation timelines, and limit broader adoption of biosimulation technologies, particularly among small and mid-sized pharmaceutical companies.

The integration of artificial intelligence and machine learning technologies with biosimulation platforms is creating significant growth opportunities in the biosimulation market. AI-enabled biosimulation solutions enhance predictive accuracy, automate model generation, improve data interpretation, and accelerate drug development workflows, particularly for complex and precision therapies. These capabilities are helping pharmaceutical and biotechnology companies reduce computational burden, optimize dosing strategies, and improve decision-making across preclinical and clinical development stages. For instance, in October 2025, Certara launched Certara IQ, an AI-powered Quantitative Systems Pharmacology (QSP) platform designed to accelerate biosimulation-driven drug development by improving model reproducibility, optimizing dosing predictions, and supporting faster development of novel therapies.

Market Concentration & Characteristics

The biosimulation market experiences a high degree of innovation driven by technological advancements. Incorporating artificial intelligence (AI) and machine learning (ML) into biosimulation platforms allows for more sophisticated data analysis and pattern recognition. For instance, in October 2024, Simulations Plus and the University of Southern California secured an NIH grant to enhance AI-driven drug discovery. The funding is likely to support the development of innovative tools and methodologies, aiming to accelerate the drug discovery process and improve therapeutic outcomes through advanced artificial intelligence applications in pharmaceutical research.

The biosimulation industry is currently witnessing a significant increase in partnership and collaboration activities among several key players. This trend is driven by the desire to gain a competitive edge, enhance technological capabilities, and consolidate in a rapidly growing market. For instance, in August 2022, GNS—now rebranded as Aitia in 2023 partnered with LES LABORATOIRES SERVIER to enhance drug discovery and clinical development for Multiple Myeloma (MM) using AI and biosimulation. This collaboration aims to utilize GNS's Digital Twin technology to better understand disease progression and improve therapeutic strategies for MM patients.

"This collaboration furthers Servier's goal to accelerate its drug discovery and clinical development efforts through AI and biosimulation and other digital initiatives,"

-Claude Bertrand, EVP of Research and Development at Servier.

"We believe GNS' Digital Twin and unique causal AI models will help our research and early development group improve our understanding of MM disease biology and, ultimately, transform our drug discovery and clinical development process".

Health authorities such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) govern the regulatory landscape for the biosimulation industry. These organizations set stringent guidelines to ensure that biosimulation is safe and effective for patient use. These agencies have issued specific guidelines regarding the use of biosimulation in drug discovery and development. However, due to technological advancements, regulatory bodies are continuously updating their policies to incorporate new scientific knowledge and methodologies related to biosimulation.

The regional expansion of the biosimulation industry is notable, driven by increasing pharmaceutical R&D investments, rising adoption of model-informed drug development approaches, expansion of clinical trial activities, and growing regulatory acceptance of biosimulation tools across emerging healthcare markets.

Case Study: Enhancing Pharmacokinetics Workflows at Charles River (Laboratory)

Background: Charles River Laboratories, a global contract research organization, conducts pharmacokinetics (PK) analysis across multiple international sites to support preclinical drug development programs. The organization required a unified and scalable system to manage increasing data complexity and ensure consistency in PK analysis and reporting across its global operations.

Challenge: The existing PK workflow was highly fragmented, with multiple standalone systems and software versions used across seven global sites. This led to inconsistent data handling, limited interoperability, inefficient data retrieval, and increased time spent on compliance requirements such as 21 CFR Part 11 documentation. These inefficiencies slowed analysis timelines and reduced operational standardization.

Solution: Charles River implemented Certara’s integrated ecosystem comprising the Phoenix platform for standardized PK/PD analysis, Integral as a centralized data repository, and PKAssist to automate and streamline workflows. This unified environment enabled standardized global processes, improved data integrity, and seamless access to study information across teams.

Outcome: The integration resulted in a harmonized global PK workflow with improved efficiency, reduced manual effort, and enhanced regulatory compliance. It also enabled faster data access, better traceability, and established a scalable digital foundation for future enhancements, including advanced analytics and AI-enabled pharmacokinetic modeling.

Product Insights

The software segment dominated the biosimulation market with a revenue share of 59.4% in 2025, owing to the increasing availability of application-specific simulation platforms designed to meet targeted drug development and research requirements. Biosimulation software enables pharmaceutical and biotechnology companies to perform predictive modeling, dose optimization, toxicity assessment, and virtual clinical trial simulations, thereby reducing development timelines and improving decision-making efficiency. The growing adoption of AI-integrated simulation platforms is further strengthening segment growth by enhancing model reproducibility, computational efficiency, and predictive accuracy. For instance, in March 2026, SEQSTER launched 1-Click DataLake, a real-world data platform aimed at accelerating clinical trial design, recruitment, and evidence generation through advanced analytics and longitudinal patient data integration

Services segment is expected to experience the fastest compound annual growth rate (CAGR) during the forecast period. This growth can be attributed to the increasingly complex and multi-layered systems involved in drug development, where biosimulation services are likely to play a crucial role. This progress is anticipated to be driven by the development of new, more precise combination therapies.

Application Insights

The drug development segment held the largest market share in 2025, driven by the increasing number of drug development processes. According to the Pharmaceutical Research and Manufacturers of America (PhRMA), more than 8,000 medicines are currently in the development pipeline. Biosimulation software is vital in drug development, as it allows researchers to create detailed models of biological systems. In addition, the growing adoption of biosimulation in fields such as pharmacogenomics and pharmacogenetics is driving the segment’s growth.

The disease modeling segment is anticipated to grow at the fastest CAGR during the forecast period. The increasing prevalence of infectious diseases globally necessitates robust modeling frameworks to predict outbreaks and assess their potential impacts on healthcare systems. Moreover, integrating big data analytics and artificial intelligence into disease modeling has further accelerated its growth, enabling more accurate predictions and real-time analysis.

Therapeutic Area Insights

The oncology segment held the largest revenue share in 2025. In oncology, biosimulation is crucial for understanding tumor dynamics, treatment responses, and patient-specific factors that influence cancer outcomes. By combining data from multiple sources, such as genomic information, clinical trials, and pharmacokinetics, researchers can develop advanced models that predict how tumors will respond to various therapies. For instance, in September 2024, Cellworks Group, Inc. announced advancements in its biosimulation technology that enhance predictions of immunotherapy responses in non-small cell lung cancer (NSCLC) patients. Integrating genomic and transcriptomic data with personalized tumor microenvironment modeling significantly improves treatment outcome predictions beyond traditional biomarkers like PD-L1 and TMB.

The infectious diseases segment is anticipated to grow at the fastest CAGR during the forecast period. Biosimulation models can integrate biological data, including pathogen behavior, host responses, and treatment effects, allowing researchers and clinicians to predict how infectious diseases progress and respond to different therapeutic interventions. Moreover, biosimulation can help assess the impact of drug resistance on treatment efficacy by modeling different cases where pathogens evolve resistance mechanisms.

Deployment Model Insights

Cloud-based deployment model dominated the market and held the largest revenue share of over 43.0% in 2025 and is expected to grow at the fastest CAGR during the forecast period. This growth can be attributed to the multiple advantages offered by the cloud-based deployment models. Traditional on-premises systems often require significant investments in hardware and software, which can limit the ability to expand computational resources as needed. Conversely, cloud platforms offer biosimulation companies the flexibility to adapt their resources up or down as required, facilitating a more responsive approach to their operational requirements.

In addition, the hybrid model segment held a significant share of the biosimulation market. This growth is attributed to its ability to combine mechanistic modeling with data-driven approaches, enabling higher predictive accuracy and improved flexibility across diverse drug development applications. The integration of both physics-based and statistical modeling techniques also enhances scalability, supports complex biological system simulations, and improves decision-making in clinical and preclinical research workflows.

Pricing Model Insights

The license-based model held the largest revenue share in 2025. The advantage of this model is that it provides users with access to sophisticated tools without the need for substantial investments in infrastructure or development. Moreover, as these models offer flexibility and scalability, companies can choose from various licensing options, including single-user licenses, multi-user licenses, or enterprise-wide agreements, depending on their specific needs and budget constraints. Such factors are expected to drive the segment growth over the forecast period.

The subscription-based pricing model is anticipated to grow at the fastest CAGR over the forecast period. By adopting a subscription model, organizations can manage their budgets and allocate resources more effectively. Moreover, the subscription model encourages collaboration among researchers and institutions by lowering barriers to access to sophisticated biosimulation tools.

End Use Insights

The life science companies segment accounted for the largest revenue share in 2025. These companies are increasingly adopting biosimulation software as a critical tool in drug development and research. This software enables companies to create detailed models of biological systems that simulate the effects of drugs on various physiological processes. Moreover, biosimulation software plays a crucial role in regulatory submissions and compliance for pharmaceutical companies. Tools such as PK-Sim and MoBi provide robust frameworks for modeling complex biological interactions essential for understanding how drugs behave in the body.

The Academic and research institutes segment is expected to grow at the fastest CAGR during the forecast period. Biosimulation models facilitate modeling of biological systems to predict their behavior under various conditions. This software enables researchers to create virtual representations of complex biological processes, including drug interactions, metabolic pathways, and cellular responses.

Regional Insights

The North America biosimulation industry accounted for the largest revenue share of 44.2% in 2025. This growth can be attributed to the presence of key players, growing investment in drug discovery and development, and the rising prevalence of chronic diseases. Moreover, adopting in-silico models while enforcing regulatory policies to ensure high patient safety and treatment standards further contributes to regional market growth.

U.S. Biosimulation Market Trends

The biosimulation industry in the U.S. held the largest revenue share in 2025 due to the early adoption of model-informed drug development (MIDD) approaches and strong regulatory support from the U.S. Food and Drug Administration for physiologically based pharmacokinetic (PBPK) and quantitative systems pharmacology (QSP) modeling in drug evaluation. The market is further driven by high utilization of biosimulation in oncology, rare disease, and biologics development, increasing integration of AI-enabled simulation platforms, and strategic collaborations between pharmaceutical companies and biosimulation software providers to reduce clinical trial failures and accelerate regulatory submissions.

Europe Biosimulation Market Trends

The biosimulation industry in Europe is growing on the back of the strong presence of pharmaceutical companies and biotechnology research centers, coupled with the increasing R&D investments. Moreover, technological advancements, such as drug development, further expedite market growth. In addition, events such as the European Drug Discovery Innovation & Outsourcing Programme serve as a platform for knowledge exchange between companies and professionals engaged in drug discovery and development.

The UK biosimulation industry is expected to grow over the forecast period. This growth can be attributed to the robust R&D infrastructure and strong presence of pharmaceutical companies, CROs & CDMOs. Pharmaceutical companies are engaged in partnerships and collaborations with biosimulation software providers to enhance their drug development process. For instance, in March 2024, Exploristics collaborated with Exonate to utilize Exploristics’ KerusCloud platform for Exonate’s Phase IIb study for diabetic eye disease.

“We are delighted to have had the opportunity to work with Exonate to harness KerusCloud’s powerful and realistic simulations to ensure that the company’s clinical trial was primed for success. Exonate recognised the need to implement a data-driven approach to optimise efficiency and minimise the risks of their proof-of-concept studies by using rational design to manage key uncertainties and challenges. We look forward to a continuation of the relationship as Exonate progresses to Phase IIb clinical trials in 2024.”

-CEO, Exploristics

The biosimulation industry in Germany held the largest market share in 2025 in the European market. This growth can be attributed to the presence of key market players, increasing healthcare spending, and strong R&D infrastructure. In addition, increasing investments in drug discovery and development, along with a growing focus on personalized medicine, are other factors propelling market growth.

Asia Pacific Biosimulation Market Trends

The biosimulation industry in the Asia Pacific is anticipated to grow at the fastest CAGR from 2026 to 2033, driven by rapid technological advancements, expanding pharmaceutical and biopharmaceutical manufacturing capabilities, and the increasing presence of CROs and CDMOs across countries such as China, Japan, South Korea, and India. Rising investments in biotechnology research, precision medicine, and model-informed drug development (MIDD) are further supporting regional market growth. In addition, increasing industry collaborations, scientific conferences, and regulatory engagement initiatives are accelerating awareness and adoption of biosimulation technologies in the region. For instance, in September 2024, Certara expanded its Certainty client event with one-day conferences across China, South Korea, and Japan, bringing together drug development and regulatory science leaders to discuss biosimulation, PBPK modeling, QSP, and AI-enabled drug development approaches

The Japan biosimulation industry held a notable revenue share in the Asia Pacific region in 2025, driven by advanced pharmaceutical research infrastructure, increasing adoption of model-informed drug development, and strong regulatory support for simulation-based drug evaluation approaches. The presence of technologically advanced pharmaceutical companies and strategic collaborations between regulatory agencies and biosimulation providers are further supporting market growth in the country.

The biosimulation industry in China is growing due to the increasing integration of AI-driven drug discovery, precision medicine, and computational modeling. The market has further gained ground with the use of in-silico methods and predictive analytics in biologics and cell & gene therapy development. This convergence is enhancing R&D efficiency and enabling better preclinical and clinical decision-making, expanding the application scope of biosimulation platforms in complex therapeutic areas. For instance, in February 2025, China Medical University Hospital announced advancements in AI-driven drug discovery and allogeneic CAR-T therapy, highlighting AI-powered drug discovery platforms, precision medicine technologies, and a novel CAR-T therapy showing over 90% tumor reduction in preclinical studies, along with ongoing FDA-reviewed clinical programs.

Latin America Biosimulation Market Trends

The biosimulation industry in Latin America is anticipated to grow at a significant CAGR over the forecast period, driven by the increasing adoption of digital technologies in healthcare and biotechnology, along with rising awareness of AI-enabled drug development solutions. Expanding pharmaceutical R&D activities, coupled with gradual increases in government and private sector investments in healthcare innovation, are further supporting market growth across the region.

Middle East & Africa Biosimulation Market Trends

The biosimulation industry in the Middle East and Africa is witnessing rising healthcare expenditures, increasing focus on drug development initiatives, and supportive government policies. The region is also witnessing the gradual adoption of advanced computational tools and AI-enabled healthcare technologies, which are strengthening pharmaceutical and biotechnology research capabilities and supporting improved R&D efficiency.

Key Biosimulation Company Insights

Key players operating in the biosimulation market are undertaking various initiatives to strengthen their market presence and increase the reach of their products and services. Strategies such as expansion activities and partnerships play a key role in propelling market growth.

Key Biosimulation Companies

The following key companies have been profiled for this study on the biosimulation market:

-

Certara, USA.

-

Dassault Systèmes

-

Advanced Chemistry Development, Inc. (now a part of Revvity )

-

Simulations Plus

-

Schrodinger, Inc.

-

Chemical Computing Group ULC

-

Physiomics Plc

-

Rosa & Co. LLC

-

BioSimulation Consulting Inc.

-

Genedata AG

-

Instem Group of Companies

-

PPD, Inc. (Acquired by Thermo Fisher Scientific)

-

Yokogawa Insilico Biotechnology GmbH

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

- Mature Players: Certara

- Focus on developing unified, end-to-end platforms that integrate PBPK, QSP, PK/PD modeling, and clinical trial simulation capabilities, enabling seamless drug development workflows and strengthening long-term client dependency across pharmaceutical R&D stages.

- Strong regulatory acceptance and long-standing partnerships with global pharmaceutical companies ensure high switching costs and sustained market leadership among mature biosimulation players.

- High platform complexity and cost of deployment limit adoption among small and mid-sized biotech companies, while long implementation cycles and rigid legacy systems reduce flexibility in rapidly evolving AI-driven drug development workflows.

Emerging Players: Simulations Plus - Focus on niche specialization in specific modeling domains such as QSP or mechanistic modeling, cloud-based delivery models, and collaborations with academia and biotech firms to build credibility and expand use cases.

- Agility and innovation allow rapid adoption of new technologies, faster product updates, and responsiveness to evolving clinical trial needs.

- Limited global reach and market presence compared with mature players, restricting scale and enterprise adoption.

Recent Developments

-

In November 2025, Revvity announced a definitive agreement to acquire ACD/Labs to strengthen its Signals software platform by integrating advanced analytical chemistry, molecular design, and AI-driven predictive capabilities.

“By integrating ACD/Labs’ technologies into the Revvity Signals platform, we’re giving our customers across pharmaceuticals and material sciences a truly unified SaaS environment—one that connects molecular design, analytical science, and manufacturing quality control within a single, end-to-end solution. This acquisition adds meaningful value to our portfolio and reinforces the importance of analytical sciences as a driver of innovation across disciplines.”

- Kevin Willoe, president of Revvity Signals Software. “

-

In October 2024, Certara acquired ChemAxon, a leading provider of cheminformatics software. This acquisition helped Certara enhance its drug discovery and development capabilities by integrating ChemAxon's advanced molecular modeling and data analysis tools.

“Combining Chemaxon’s expertise with Certara’s biosimulation capabilities provides life sciences companies with unique solutions to enhance productivity and increase their scientific innovation success rates,”

-William Feehery, Certara’s CEO.

“Together, we offer scientists more precise insights throughout drug discovery and development.”

-

In September 2024, Certara partnered with Ichnos Glenmark Innovation (IGI) to optimize the dosing strategy for a potential first-in-class cancer drug. This collaboration leverages Certara's modeling and simulation expertise to enhance the drug's development process, aiming to improve patient outcomes and streamline clinical trials.

“We were honored to work with IGI to develop a comprehensive biosimulation approach that allowed the team to successfully test ISB 2001 in virtual trials,”

- Senior Vice President and Head of Applied Biosimulation, Certara.

“Our unique expertise and experience using virtual patients plus mechanistic modeling solutions allowed us to accelerate the speed at which ISB 2001 gets to patients. Virtual patient technology is the future of optimizing dosing for human patients.”

-

In June 2024, Simulations Plus acquired Pro-ficiency. By this acquisition, Simulation Plus is likely to integrate Pro-ficiency's innovative software solutions with its existing capabilities, creating a novel platform designed to streamline and optimize the drug development process.

Biosimulation Market Report Scope

Report Attribute

Details

Market size in 2025

USD 4.1 billion

Estimated Market size in 2026

USD 4.8 billion

Projected Market size by 2033

USD 14.8 billion

Growth rate

CAGR of 17.3% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product, application, therapeutic area, deployment model, pricing model, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; Denmark; Sweden; Norway; China; Japan; India; South Korea; Australia; Thailand; Brazil; Argentina; South Africa; Saudi Arabia; UAE; Kuwait

Key companies profiled

Certara; Dassault Systèmes; Advanced Chemistry Development, Inc. (now a part of Revvity); Simulations Plus; Schrödinger; Chemical Computing Group; Physiomics Plc; Rosa & Co. LLC; BioSimulation Consulting Inc.; Genedata AG; Instem; Thermo Fisher Scientific (PPD acquired); Yokogawa Electric Corporation

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Biosimulation Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global biosimulation market report based on product, application, therapeutic area, deployment model, pricing model, end use, and region.

-

Product Outlook (Revenue, USD Million, 2021 - 2033)

-

Software

-

Molecular Modeling & Simulation Software

-

Docking, molecular dynamics, QSAR

-

Small Molecules

-

Biologics

-

-

In-silico ADME (ChemAxon-type tools)

-

Large Pharma (Top ~30)

-

Mid Pharma (~30–300)

-

Emerging / Long-tail Pharma & Biotech

-

-

Physicochemical property prediction (logP, pKa, solubility, permeability)

-

-

Clinical Trial Design Software

-

Clinical trial simulation

-

Adaptive design

-

Virtual patients

-

Dose optimization

-

MIDD-linked applications

-

-

PK/PD Modeling and Simulation Software

-

Software

-

Compartmental modeling

-

Population PK/PD (Pop PK/PD)

-

Non-compartmental analysis (NCA)

-

Dose-response, bioequivalence

-

-

Customer

-

Large Pharma (Top ~30)

-

Mid Pharma (~30–300)

-

Emerging / Long-tail Pharma & Biotech

-

-

-

Pbpk Modeling and Simulation Software

-

ADME (mechanistic)

-

DDI modeling

-

FIH dose prediction

-

Special populations

-

-

Toxicity Prediction Software

-

Hepatotoxicity, cardiotoxicity, genotoxicity

-

QSAR, mechanistic, AI/ML models

-

ADME-linked toxicity

-

-

QSP / Systems Biology Software

-

Software

-

Mechanistic disease modeling

-

Multi-scale simulation

-

Integration with PBPK

-

-

Customer

-

Large Pharma (Top ~30)

-

Mid Pharma (~30–300)

-

Emerging / Long-tail Pharma & Biotech

-

-

-

Other Software

-

AI-driven platforms

-

RWD-integrated tools

-

-

-

Services

-

Contract Services

-

Services

-

PK/PD services

-

Pop PK/PD

-

NCA

-

Compartmental

-

-

-

PBPK services

-

ADME

-

DDI

-

Special populations

-

-

Customer

-

Large Pharma (Top ~30)

-

Mid Pharma (~30–300)

-

Emerging / Long-tail Pharma & Biotech

-

-

-

Consulting

-

Large Pharma (Top ~30)

-

Mid Pharma (~30–300)

-

Emerging / Long-tail Pharma & Biotech

-

-

Implementation, Training & Support

-

Service

-

Deployment

-

Integration

-

Training

-

-

Customer

-

Large Pharma (Top ~30)

-

Mid Pharma (~30–300)

-

Emerging / Long-tail Pharma & Biotech

-

-

-

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Drug Discovery & Development

-

Disease Modeling

-

Other (Precision Medicine, Toxicology, etc., etc.)

-

-

Therapeutic Area Outlook (Revenue, USD Million, 2021 - 2033)

-

Oncology

-

Cardiovascular Disease

-

Infectious Disease

-

Neurological Disorders

-

Others

-

-

Deployment Model Outlook (Revenue, USD Million, 2021 - 2033)

-

Cloud-based

-

On-premise

-

Hybrid Model

-

-

Pricing Model Outlook (Revenue, USD Million, 2021 - 2033)

-

License-based Model

-

Subscription-based Model

-

Service-based Model

-

Pay Per Use Model

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Life Sciences Companies

-

Pharmaceutical Companies

-

Biopharma Companies

-

Medical Device Companies

-

CROs/CDMOs

-

-

Academic Research Institutions

-

Others (Regulatory Authorities, etc.)

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

Thailand

-

-

Latin America

-

Brazil

-

Argentina

-

-

MEA

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Platform & Vendor Evaluation

Comparative assessment of biosimulation platforms based on capabilities (PBPK, QSP, PK/PD, trial simulation), regulatory acceptance, integration capability, and usability within pharma R&D workflows.

Help buyers shortlist vendors and select platforms aligned with their therapeutic focus and regulatory needs.

Market Share Analysis

Developed a region-wise market share distribution of top 10 biosimulation players across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa based on revenue presence, installed customer base, regulatory engagement, and partnership intensity. Included comparative regional dominance mapping for each key player.

Enables clear visibility of where each leading vendor is strongest geographically, supporting competitive benchmarking, regional expansion strategy, and identification of under-penetrated markets for growth opportunities.

Case Study Analysis

Developed structured case studies showcasing real-world application of biosimulation in drug development, including use in dose optimization, clinical trial simulation, regulatory submissions, and translational modeling. Each case highlights the problem statement, the solution approach using biosimulation tools, the implementation workflow, and measurable outcomes such as reduced trial timelines, improved success rates, and cost savings.

Provides evidence-based validation of biosimulation impact, strengthens value proposition for vendors, supports sales enablement, and helps end-users understand practical benefits and ROI of adoption.

Frequently Asked Questions About This Report

The global biosimulation market size was valued at USD 4.1 billion in 2025 and is estimated at USD 4.8 billion for 2026.

The global biosimulation market is expected to grow at a CAGR of 17.3% from 2026 to 2033, reaching USD 14.8 billion.

Key factors include growing regulatory support for model-informed drug development (MIDD), AI/ML integration in computational modeling, rising R&D costs, and increasing demand for personalized medicine.

North America dominated with a 44.2% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

The software segment led with a 59.4% revenue share in 2025, while services is the fastest-growing segment.

Oncology held the largest revenue share in 2025, while infectious diseases is the fastest-growing area.

Cloud-based deployment held the largest share (over 43.0%) in 2025 and is the fastest-growing model.

Key players include Certara, Dassault Systèmes, Simulations Plus, Schrödinger, Chemical Computing Group, Physiomics Plc, Rosa & Co. LLC, BioSimulation Consulting Inc., Genedata AG, Instem, Thermo Fisher Scientific, Advanced Chemistry Development (part of Revvity), and Yokogawa.

About the Author(s)

Healthcare IT Research Team

Healthcare · Healthcare ITThis report was authored by the healthcare it research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the healthcare it segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.