- Home

- »

- Plastics, Polymers & Resins

- »

-

Bottled Water Packaging Market Size Report, 2026-2033GVR Report cover

![Bottled Water Packaging Market (2026 - 2033)Report]()

Bottled Water Packaging Market (2026 - 2033)

Size, Share & Trends Analysis Report By Material (Plastic, Glass, Metal), By Distribution Channel (Retail Stores, Ecommerce, Supermarkets, Hypermarkets), By Application, By Region, And Segment Forecasts

Market Size, 2025

$117.7BMarket Estimate, 2026

$125.7BMarket Forecast, 2033

$204.3BCAGR, 2026–2033

7.2%Bottled Water Packaging Market Summary

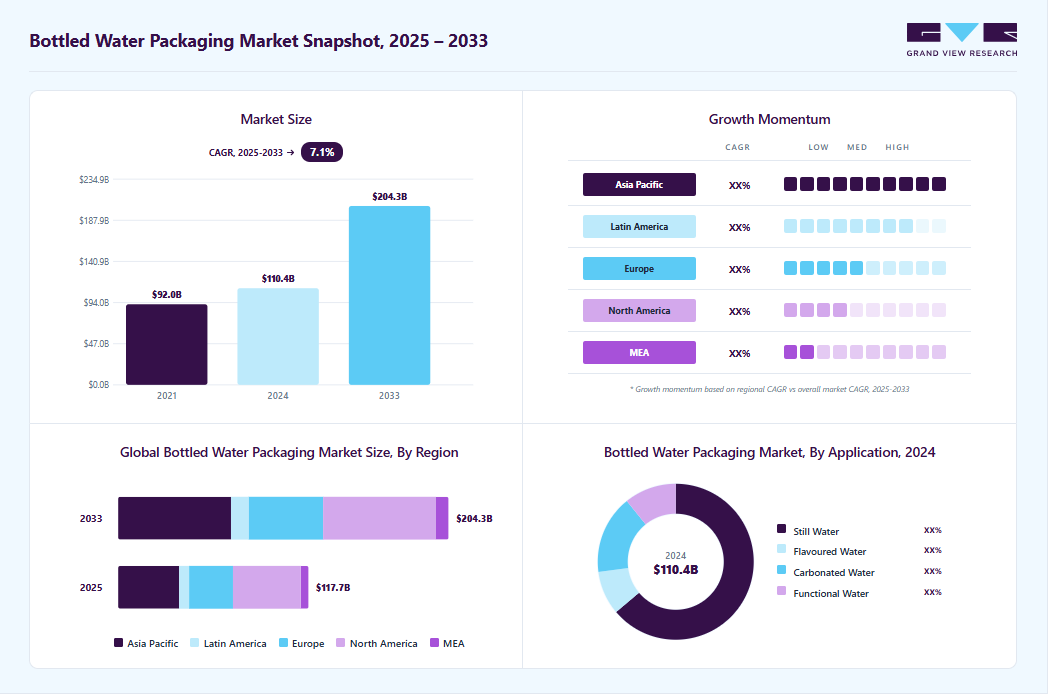

The global bottled water packaging market size was valued at USD 117.7 billion in 2025 and is projected to grow from USD 125.7 billion in 2026 to USD 204.3 billion by 2033, at a CAGR of 7.2% from 2026 to 2033. North America dominated the market, accounting for the largest revenue share of 35.5% in 2025. The global bottled water packaging industry's growth is driven by increasing health consciousness and rising demand for convenient, portable hydration solutions.

Key Market Trends & Insights

- By material: Plastic segment led the market with the largest revenue share of 77.5% in 2025.

- By distribution channel: Retail stores segment led the market with the largest revenue share of 37.6% in 2025.

- By application: Still water segment led the market with the largest revenue share of 63.5% in 2025.

Regional Highlights

- Largest regional market: North America (35.5% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest share of North America in 2025.

Market Size & Forecast

- Market size in 2025: USD 117.7 Billion

- Estimated market size in 2026: USD 125.7 Billion

- Projected market size by 2033: USD 204.3 Billion

- CAGR (2026-2033): 7.2%

Additionally, growing urbanization and improved retail infrastructure are boosting bottled water consumption worldwide. The rising demand for convenience and on-the-go hydration is a major driver of the bottled water packaging industry. Urbanization, busy lifestyles, and increasing health consciousness have led consumers to prefer bottled water over sugary beverages. For example, in fast-growing economies such as India and China, the demand for packaged drinking water has surged due to rapid urbanization and the need for safe, portable drinking water. Additionally, the popularity of fitness trends has boosted sales of bottled water in ergonomic and resealable packaging, such as sports bottles from brands such as Gatorade and Smartwater.")

Growing concerns over water safety and contamination are also fueling market growth. In regions with unreliable tap water quality, such as parts of Africa, Latin America, and Southeast Asia, consumers rely on bottled water as a safer alternative. For instance, in Flint, Michigan (U.S.), the lead contamination crisis led to a spike in bottled water sales. Similarly, in countries such as Mexico, where tap water is often unsafe, companies such as Bonafont (a Danone brand) dominate the market with purified and mineral water offerings in durable PET bottles.

Innovations in sustainable packaging are reshaping the industry as environmental concerns push brands toward eco-friendly solutions. Many companies are shifting from single-use plastics to recycled PET (rPET), biodegradable materials, and even aluminum cans. For example, Evian has committed to using 100% recycled plastic by 2025, while startups such as Liquid Death use aluminum cans to appeal to eco-conscious consumers. Governments are also enforcing stricter regulations, such as the EU’s Single-Use Plastics Directive, pushing manufacturers to adopt greener alternatives.

Moreover, expansion in ecommerce and retail distribution is accelerating market growth. Online platforms such as Amazon and Alibaba have made bottled water more accessible, with subscription services ensuring regular deliveries. Supermarkets and convenience stores also play a key role, with private-label brands such as Costco’s Kirkland Signature gaining traction. The rise of functional waters (e.g., vitamin-infused, alkaline, or electrolyte-enhanced) further diversifies the market, with brands such as Essentia and Bai leveraging premium packaging to attract health-focused consumers. These trends, combined with rising disposable incomes in emerging markets, ensure sustained growth in the bottled water packaging industry.

Market Dynamics

The bottled water packaging market is witnessing steady growth, driven by increasing bottled water consumption, demand for convenient hydration solutions, and rising preference for sustainable packaging materials. Manufacturers are focusing on lightweight, recyclable, and eco-friendly packaging to meet evolving consumer expectations and regulatory requirements. Additionally, advancements in packaging technology, expanding retail distribution, and growing urbanization are supporting market expansion, while concerns over plastic waste continue to drive innovation in packaging materials and designs.

The increasing consumption of bottled water worldwide is a key driver of the bottled water packaging market. Growing health awareness, concerns regarding the quality of tap water in certain regions, and the rising preference for safe and convenient drinking water have significantly boosted bottled water sales. Rapid urbanization, busy lifestyles, and the expanding on-the-go beverage culture have further increased demand for packaged water products across residential, commercial, and travel-related applications, creating sustained demand for packaging solutions.

As bottled water manufacturers continue to expand their product portfolios and distribution networks, the need for efficient, durable, and cost-effective packaging is growing. Companies are investing in lightweight bottle designs, enhanced packaging formats, and improved labeling technologies to strengthen brand appeal and optimize logistics. The increasing availability of bottled water through supermarkets, convenience stores, vending machines, and e-commerce channels is further supporting the growth of the bottled water packaging market.

A significant restraint for the bottled water packaging market is the growing concern over plastic waste and the increasing implementation of stringent environmental regulations. Governments and regulatory bodies across various regions are introducing measures to reduce single-use plastics, encourage recycling, and promote sustainable packaging alternatives. These regulations, coupled with rising consumer awareness regarding environmental sustainability, are increasing compliance costs for manufacturers and creating pressure to invest in eco-friendly materials and packaging innovations, which can impact profit margins and slow market growth.

A major opportunity for the bottled water packaging market lies in the increasing adoption of sustainable and recyclable packaging materials. Rising environmental awareness among consumers and the growing emphasis on circular economy initiatives are encouraging manufacturers to develop packaging solutions made from recycled PET (rPET), bio-based plastics, and other eco-friendly materials. As brands seek to strengthen their sustainability credentials and comply with evolving environmental regulations, demand for innovative, lightweight, and fully recyclable packaging is expected to create significant growth opportunities for packaging manufacturers across global markets.

Market Concentration & Characteristics

The bottled water packaging market is characterized by its high volume and low margin nature, driven by mass consumption and standardized production processes. The industry relies heavily on economies of scale, particularly in the production of PET bottles, caps, and labels. Manufacturers prioritize cost-efficiency, automation, and bulk procurement of raw materials such as plastic resins, labels, and closures. As bottled water is a fast-moving consumer good (FMCG), packaging design focuses on light-weighting, durability, and cost-effectiveness to maintain competitiveness. Leading players such as Amcor plc; Berry Global Inc.; ALPLA; and Silgan Plastics have optimized their operations around lean manufacturing and high-output technologies.

A defining feature of the industry is its dependence on plastic-based materials, especially polyethylene terephthalate (PET), due to its clarity, lightweight properties, and recyclability. However, environmental concerns and regulations are reshaping this characteristic, pushing the industry toward sustainable alternatives. Innovations in rPET, bio-based plastics, and even paper-based bottles are gaining traction, although adoption varies by region due to cost, infrastructure, and consumer awareness. Regulatory frameworks such as the EU's Single-Use Plastics Directive and the U.S. Plastics Pact are accelerating this shift, influencing product development and investment decisions.

Analyst Perspective

The bottled water packaging market is expected to experience steady growth, driven by increasing bottled water consumption, rising health awareness, and growing demand for convenient and safe hydration solutions. The market is also benefiting from the expansion of premium, flavored, carbonated, and functional water products, which require innovative packaging formats for product differentiation. Additionally, increasing emphasis on sustainability and recyclable materials is encouraging packaging manufacturers to develop eco-friendly solutions, creating new growth opportunities across global markets.

Material Insights

Based on material, the plastic segment led the market with the largest revenue share of 77.5% in 2025. Plastic is the most widely used material in bottled water packaging, with PET being the most common resin due to its lightweight, durability, and cost-effectiveness. Plastic bottles dominate the market, especially in single-use, small-sized formats for convenience and on-the-go consumption. The material offers excellent barrier properties against moisture and gases and is widely accepted in global recycling systems. The growth of plastic packaging is driven by its affordability, mass production scalability, and light shipping weight, which reduces transportation costs and carbon footprint.

The metal segment is expected to grow at the fastest CAGR of 7.5% during the forecast period. Aluminum and steel bottles are a niche but growing segment in bottled water packaging. They are valued for their durability, recyclability, and ability to protect the product from light and oxygen. Brands leveraging metal packaging often target sustainability-conscious consumers and active lifestyle markets. The growth of metal packaging is driven by increasing demand for sustainable and reusable options, especially in North America and Europe. Aluminum has one of the highest recycling rates among packaging materials, and its lightweight, shatterproof properties make it attractive for outdoor and travel uses.

Distribution Channel Insights

Based on distribution channel, the retail stores segment led the market with the largest revenue share of 37.6% in 2025. Retail stores remain a significant distribution channel for bottled water packaging, especially in urban and semi-urban areas. These outlets typically include small neighborhood shops, convenience stores, and independent grocers that stock bottled water from both global and local brands. They provide easy accessibility, allowing consumers to purchase bottled water in single units or small quantities as needed. Retail stores thrive on their proximity to consumers, impulse buying behavior, and the need for on-the-go hydration.

The ecommerce segment is expected to grow at the fastest CAGR of 7.7% during the forecast period. Ecommerce has emerged as a fast-growing distribution channel for bottled water, particularly in urbanized and digitally connected regions. Through online platforms such as Amazon, Walmart.com, BigBasket, and others, consumers can purchase a variety of bottled water products in bulk or as subscription services, with home delivery convenience. Ecommerce platforms also enable broader brand visibility and product assortment, including premium and functional water brands, which further drive bottled water packaging innovations such as tamper-evident seals and eco-friendly designs.

Application Insights

Based on application, the still water segment led the market with the largest revenue share of 63.5% in 2025. Still water, also known as non-carbonated water, is the most consumed form of bottled water globally. It includes spring water, purified water, and mineral water, and is typically sold in plastic (PET), glass, or carton-based packaging. This segment holds the largest market share due to its wide consumer base and low price point. The growth of still water packaging is primarily driven by increasing health consciousness among consumers who are shifting away from sugary and carbonated beverages. Urbanization, tourism, and the availability of small and large-size packaging options further boost its demand.

The functional water segment is projected to grow at the fastest CAGR of 9.5% during the forecast period. Functional water includes water that has been enhanced with ingredients such as vitamins, minerals, electrolytes, amino acids, or antioxidants. It is marketed for its health benefits and performance-enhancing properties, making it popular among athletes and fitness-conscious individuals. Rising awareness around fitness, immunity, and holistic wellness has led to increasing consumption of functional water. The packaging market benefits from this trend as brands innovate with clear labeling, sustainable bottles, and convenient formats. Growth in the sports and wellness sectors, coupled with endorsements from health influencers, further drives demand.

Regional Insights

North America dominated the bottled water packaging market with the largest revenue share of 35.5% in 2025. This positive outlook is due to health-conscious consumers shifting away from sugary drinks. The U.S. is the largest market, with premium and functional waters (alkaline, electrolyte-enhanced) gaining popularity. Brands such as Dasani (Coca-Cola), Aquafina (PepsiCo), and Essentia have strong market penetration, while startups such as Liquid Death target younger demographics with edgy marketing. The convenience culture in the U.S. also fuels demand for single-serve bottles, especially in vending machines and gas stations.

The Canada bottled water packaging market follows a similar trend, with a growing preference for natural spring and mineral water. Environmental concerns, however, are reshaping industry, with companies such as Nestlé Waters facing a backlash over groundwater extraction. In response, major brands are investing in rPET (recycled plastic) bottles and water refill stations. The rise of home and office water delivery services, such as Poland Spring and Arrowhead, also contributes to steady demand for bottled water packaging.

Europe Bottled Water Packaging Market Trends

Europe’s bottled water packaging industry’s growth is driven by strict regulations on tap water quality and a strong culture of mineral water consumption, particularly in Western Europe. Countries such as France, Italy, and Germany have long-standing traditions of drinking mineral water, with brands such as Evian, San Pellegrino, and Gerolsteiner being household names. The demand for premium sparkling water is particularly high in Europe, often associated with dining and luxury. Eastern Europe is also growing, with countries such as Poland and Hungary seeing increased bottled water sales due to improving economic conditions.

Sustainability is a major trend in Europe, with the EU pushing for higher recycling rates and reduced plastic waste. Many brands now use glass bottles or fully recyclable PET, and some, such as Denmark’s Aqua d’Or, focus on carbon-neutral production. The convenience of lightweight, resealable bottles remains popular, but there is also a shift toward bulk purchases (6-packs, 12-packs) in supermarkets. Additionally, flavored and functional waters are gaining traction, appealing to health-focused consumers seeking alternatives to soda.

Asia Pacific Bottled Water Packaging Market Trends

The Asia Pacific bottled water packaging industry is expected to grow at the fastest CAGR of 8.0% over the forecast period. This positive outlook is due to rapid urbanization, increasing health awareness, and limited access to clean tap water in many areas. Countries such as India and Indonesia have seen explosive growth in bottled water consumption due to rising disposable incomes and concerns over waterborne diseases. Additionally, the region’s hot climate and large population further boost demand. For example, India’s bottled water market is projected to grow at a CAGR of over 7%, driven by brands such as Bisleri and Kinley. Meanwhile, China dominates production, being the world’s largest bottled water consumer, with companies such as Nongfu Spring and Wahaha leading the market.

Another key factor is the expansion of modern retail channels and ecommerce, making bottled water more accessible. In Southeast Asia, tourism also plays a role, with countries such as Thailand and Vietnam seeing high demand from both locals and travelers. The preference for small, portable PET bottles (500ml-1L) is particularly strong, catering to on-the-go consumption. However, environmental concerns over plastic waste are pushing some markets, such as Japan and South Korea, toward sustainable packaging innovations, such as recycled PET and biodegradable bottles.

Key Bottled Water Packaging Company Insights

The competitive environment of the bottled water packaging market is characterized by intense rivalry among global packaging giants, regional converters, and specialized material suppliers. Key players such as Amcor plc, Berry Global Inc., ALPLA, and Silgan Plastics dominate through innovations in lightweight PET bottles, eco-friendly closures, and sustainable labeling. The market is driven by high demand for environmentally responsible packaging, pushing firms to invest in recyclable materials, bio-based plastics, and refillable bottle technologies. Barriers to entry remain moderate due to the need for advanced manufacturing capabilities and compliance with stringent food safety regulations. Meanwhile, private-label bottled water brands and increasing consumer awareness are putting pressure on packaging players to offer cost-effective yet sustainable solutions, intensifying competition further.

-

In August 2024, ALPLA, a global company in plastic packaging, launched a new line of PET bottles that boast a premium, glass-like appearance, targeting the beverage sector with a sustainable and visually appealing alternative to traditional glass. These innovative bottles, already introduced for mineral water brands in Poland, are designed to closely mimic the look and feel of glass while offering significant advantages such as being lightweight, shatterproof, and fully recyclable.

-

In August 2024, Berry Global Inc. partnered with Norwegian brand Aquafigure to launch a new line of reusable 330ml water bottles designed to encourage water consumption among young people through customizable, interchangeable 3D artwork cards. Made from BPA-free Tritan, a recyclable and food-approved copolyester. Production is handled at Berry’s facilities in the Netherlands and England, with a focus on ensuring a secure yet child-friendly seal. The partnership aims to deliver a “bottle for life” solution, advancing both sustainability and consumer engagement as Aquafigure expands into new markets.

Key Bottled Water Packaging Companies:

The following key companies have been profiled for this study on the bottled water packaging market.

-

Amcor plc

-

Ball Corporation

-

Sidel

-

Owens-Illinois (O-I)

-

Ardagh Group

-

Berry Global Inc.

-

ALPLA

-

Silgan Plastics

-

Ajanta Bottle

-

PGP Glass

-

JSK Plastic Industries

-

SIGG

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (Amcor plc, Ball Corporation, Sidel, Owens-Illinois (O-I), Ardagh Group, Berry Global Inc., ALPLA, and Silgan Plastics)

- Focus on global manufacturing networks, strategic acquisitions, and long-term supply agreements with major bottled water brands.

- Invest heavily in sustainable packaging solutions, recycled materials, lightweight bottle designs, and advanced automation technologies.

- Benefit from strong brand reputation, extensive geographic presence, and diversified packaging portfolios.

- Possess significant R&D capabilities and economies of scale, enabling cost-efficient production and continuous innovation.

- Large organizational structures can result in slower decision-making and reduced operational flexibility.

- High capital investment requirements and regulatory compliance costs can impact profitability and responsiveness to niche market trends.

Emerging Players (Ajanta Bottle, PGP Glass, JSK Plastic Industries, and SIGG)

- Emphasize regional market expansion and customized packaging solutions tailored to customer requirements.

- Focus on flexible manufacturing operations and targeted investments in high-growth bottled water packaging segments.

- Offer greater agility and faster response times to changing customer preferences and market demands.

- Maintain strong relationships with regional customers through specialized products and personalized service.

- Limited financial resources and production capacities restrict large-scale expansion and technology investments.

- Smaller distribution networks and lower brand visibility make it challenging to compete with established global packaging leaders.

Bottled Water Packaging Market Report Scope

Report Attribute

Details

Market size in 2025

USD 117.7 billion

Estimated Market size in 2026

USD 125.7 billion

Projected Market size by 2033

USD 204.3 billion

Growth rate

CAGR of 7.2% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Material, distribution channel, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; China; Japan; India; South Korea; Australia; Brazil; Argentina; Saudi Arabia; South Africa; UAE

Key companies profiled

Amcor plc; Ball Corporation; Sidel; Owens-Illinois (O-I); Ardagh Group; Berry Global Inc.; ALPLA; Silgan Plastics; Ajanta Bottle; PGP Glass; JSK Plastic Industries; SIGG

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Bottled Water Packaging Market Report Segmentation

This report forecasts revenue growth at a global level and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global bottled water packaging market report based on material, distribution channel, application, and region:

-

Material Outlook (Revenue, USD Million 2021 - 2033)

-

Plastic

-

Glass

-

Metal

-

Others

-

-

Distribution Channel Outlook (Revenue, USD Million 2021 - 2033)

-

Retail Stores

-

Ecommerce

-

Supermarkets

-

Hypermarkets

-

-

Application Outlook (Revenue, USD Million 2021 - 2033)

-

Still Water

-

Flavored Water

-

Carbonated Water

-

Functional Water

-

-

Regional Outlook (Revenue, USD Million 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

France

-

UK

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

Australia

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

South Africa

-

Saudi Arabia

-

UAE

-

-

Research Methodology

The bottled water packaging market figures in this report are based on a proven research process that combines executive interviews with secondary research from proprietary databases, company filings, and recognized regulatory and institutional sources. Market size is built through value-chain sizing - reconciling supply-side and demand-side estimates - and triangulated with bottom-up and top-down approaches. Every estimate passes multiple levels of expert validation before publication, with each bottled water packaging segment quantified using the revenue-capture definitions in the table below.

Segment Definition

Segment - Material

Revenue capture definition

Plastic

Revenue generated from the sale of plastic-based bottled water packaging, including PET, HDPE, and other polymer materials used for manufacturing bottles, caps, and closures. This segment includes packaging solutions for still, flavored, carbonated, and functional water applications due to their lightweight, durability, and cost-effectiveness.

Glass

Revenue generated from the sale of glass bottled water packaging designed to provide premium product presentation, chemical inertness, and recyclability. This segment includes glass bottles used for premium still water, sparkling water, flavored water, and specialty bottled water products.

Metal

Revenue generated from the sale of metal-based bottled water packaging, including aluminum bottles and cans that offer durability, extended recyclability, and reduced environmental impact. This segment includes packaging solutions used across premium, carbonated, flavored, and functional water categories.

Other Materials

Revenue generated from the sale of bottled water packaging manufactured from alternative materials such as paper-based composites, biodegradable plastics, bio-based polymers, and other sustainable packaging materials. This segment includes innovative packaging solutions developed to address environmental concerns and regulatory requirements.

Segment - Distribution Channel

Revenue capture definition

Retail Stores

Revenue generated from the sale of bottled water packaging supplied through convenience stores, specialty stores, and independent retail outlets. This segment includes packaging formats designed to support individual consumer purchases and localized distribution networks.

E-commerce

Revenue generated from the sale of bottled water packaging used for products distributed through online platforms and direct-to-consumer channels. This segment includes packaging solutions optimized for transportation, product protection, and efficient home delivery.

Supermarkets

Revenue generated from the sale of bottled water packaging supplied to supermarket chains that offer a broad range of bottled water products. This segment includes packaging formats designed for high-volume sales, shelf visibility, and consumer convenience.

Hypermarkets

Revenue generated from the sale of bottled water packaging supplied to large-format retail outlets and hypermarkets. This segment includes bulk packaging, multipacks, and high-capacity bottle formats designed to support large-scale consumer purchases and promotional sales.

Segment - Application

Revenue capture definition

Still Water

Revenue generated from the sale of packaging solutions used for non-carbonated bottled water products. This segment includes bottles, closures, and labels designed to maintain product quality, safety, and shelf appeal across various consumption occasions.

Flavoured Water

Revenue generated from the sale of packaging solutions used for bottled water infused with flavors, natural extracts, or sweeteners. This segment includes packaging designed to preserve product freshness, flavor integrity, and brand differentiation.

Carbonated Water

Revenue generated from the sale of packaging solutions used for sparkling and carbonated water products. This segment includes bottles and closures engineered to withstand internal pressure and maintain carbonation throughout the product lifecycle.

Functional Water

Revenue generated from the sale of packaging solutions used for bottled water enriched with vitamins, minerals, electrolytes, and other functional ingredients. This segment includes packaging formats designed to protect product stability, support branding, and meet consumer demand for health-focused beverages.

Estimation Model

Layer Name

Key Question

Description

Bottled Water Consumption Base Layer

What forms the demand base?

Identify global bottled water consumption volumes across key categories including still water, flavored water, carbonated water, and functional water. Assess consumption patterns across residential, commercial, hospitality, institutional, and on-the-go applications. This layer establishes the total addressable demand for bottled water packaging solutions.

Packaging Material Penetration Layer

Which packaging materials are utilized?

Estimate the proportion of bottled water packaged in plastic, glass, metal, and other materials across regions and application segments. Assess material adoption trends based on cost, sustainability requirements, recyclability, product positioning, and regulatory considerations.

Distribution Channel Intensity Layer

Through which channels is packaged water sold?

Analyze bottled water sales volumes across retail stores, e-commerce platforms, supermarkets, and hypermarkets. Evaluate channel-wise packaging demand based on consumer purchasing behavior, product formats, shelf requirements, transportation needs, and inventory turnover rates.

Revenue Layer

How is market revenue generated?

Market revenue is quantified through the sale of bottles, caps, closures, labels, and secondary packaging used for bottled water products. Revenue is generated from packaging demand across still, flavored, carbonated, and functional water segments, supported by new product launches, premium packaging innovations, sustainability initiatives, and replacement demand from beverage manufacturers worldwide.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Regional Segmentation Analysis

Detailed assessment of the bottled water packaging market across North America, Europe, Asia Pacific, Central & South America, and Middle East & Africa, covering regional demand patterns, packaging material preferences, sustainability regulations, consumption trends, and growth outlook by application and distribution channel.

Enables identification of high-growth regions, regional demand variations, and strategic expansion opportunities across key markets.

Cross-Segmentation Analysis

Comprehensive analysis of market opportunities across combinations of Material (Plastic, Glass, Metal, Other Materials), Distribution Channel (Retail Stores, Ecommerce, Supermarkets, Hypermarkets), Application (Still Water, Flavoured Water, Carbonated Water, Functional Water), and regional markets.

Helps identify the most lucrative segment combinations, demand pockets, and customer preferences to support targeted business strategies.

Competitive Benchmarking

Comparative benchmarking of leading bottled water packaging companies based on product portfolio alignment across materials, innovation capabilities, sustainability initiatives, manufacturing capacity, regional presence, distribution channel, and strategic developments.

Provides insights into competitor positioning, market share opportunities, and differentiation strategies within key segments.

Frequently Asked Questions About This Report

The plastic segment led the bottled water packaging market with a 77.5% revenue share in 2025.

The retail stores segment led the bottled water packaging market with a 37.6% revenue share in 2025.

The still water segment led the bottled water packaging market with a 63.5% revenue share in 2025.

Key factors driving the bottled water packaging market include rising bottled water consumption, growing health awareness, increasing demand for convenient hydration, expanding retail and e-commerce channels, and the adoption of sustainable and recyclable packaging solutions.

Key players in the bottled water packaging market include Amcor plc, Ball Corporation, Sidel, Owens-Illinois (O-I), Ardagh Group, Berry Global Inc., ALPLA, Silgan Plastics, Ajanta Bottle, PGP Glass, JSK Plastic Industries, and SIGG.

The global bottled water packaging market size was valued at USD 117.7 billion in 2025 and is estimated at USD 125.7 billion for 2026.

The global bottled water packaging market is expected to grow at a CAGR of 7.2% from 2026 to 2033, reaching USD 204.3 billion by 2033.

North America dominated the bottled water packaging market with a 35.5% revenue share in 2025.

Asia Pacific is the fastest-growing region in the bottled water packaging market with a CAGR of 8.0% over the forecast period.

About the Author(s)

Plastics, Polymers & Resins Research Team

Bulk Chemicals · Plastics, Polymers & ResinsThis report was authored by the plastics, polymers & resins research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the plastics, polymers & resins segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.