- Home

- »

- Clinical Diagnostics

- »

-

Central Lab Market Size, Share & Trends Report, 2026-2033GVR Report cover

![Central Lab Market (2026 - 2033)Report]()

Central Lab Market (2026 - 2033)

Size, Share & Trends Analysis Report By Service (Genetic Services, Biomarker Services, Microbiology Services), By End-use (Pharmaceutical Companies, Biotechnology Companies), By Region, And Segment Forecasts

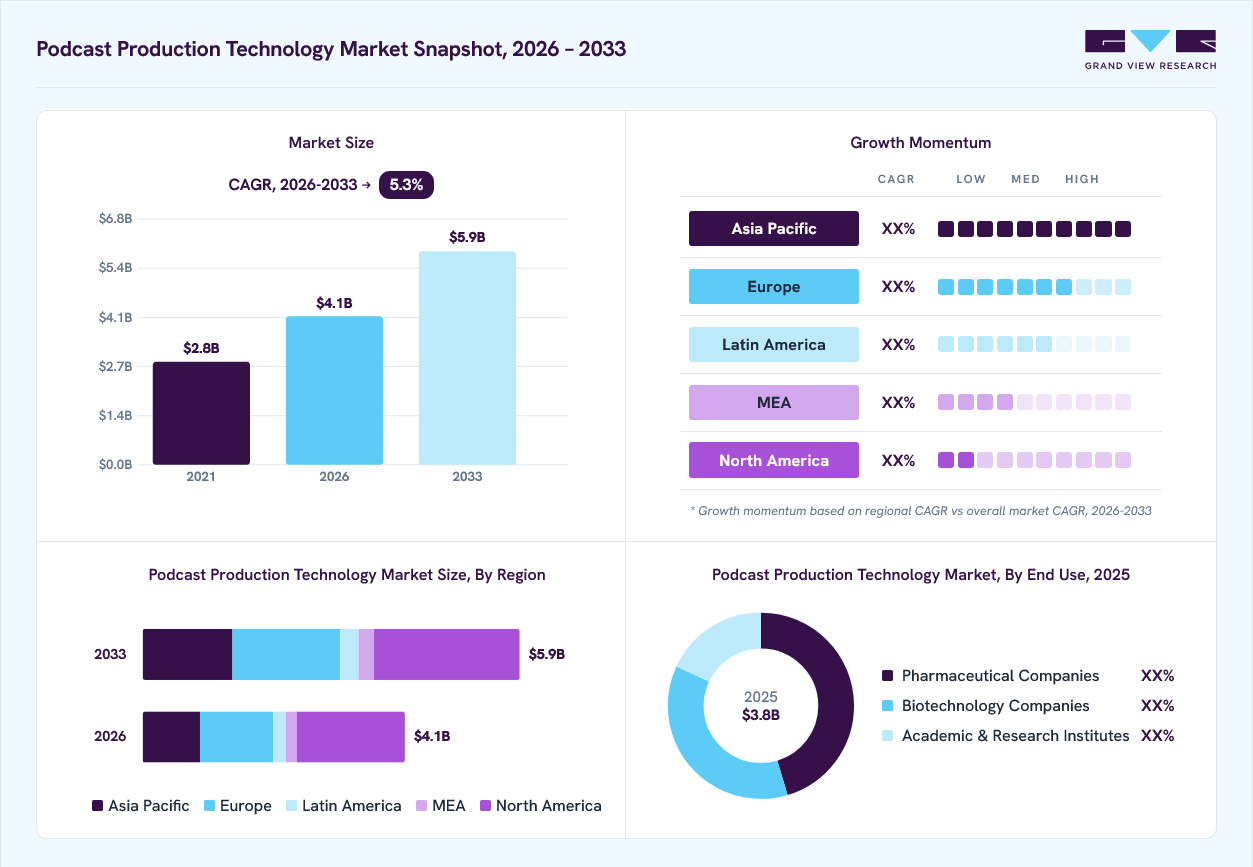

Market Size, 2025

$3.8BMarket Estimate, 2026

$4.1BMarket Forecast, 2033

$5.9BCAGR, 2026–2033

5.3%Central Lab Market Summary

The global central lab market size was valued at USD 3.8 billion in 2025 and is projected to grow from USD 4.1 billion in 2026 to USD 5.9 billion by 2033, at a CAGR of 5.3% from 2026 to 2033. North America dominated the market, accounting for a revenue share of 41.6% in 2025. The growth can be attributed to the increasing investment in R&D and the increased focus of sponsors & investigators on reducing research costs.

Key Market Trends & Insights

- By service: Biomarker services segment led the market with the largest revenue share of 38.3% in 2025.

- By end use: Pharmaceutical companies segment led the market with the largest revenue share of 45.3% in 2025.

Regional Highlights

- Largest regional market: North America (41.6% revenue share, 2025)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 3.8 Billion

- Estimated market size in 2026: USD 4.1 Billion

- Projected market size by 2033: USD 5.9 Billion

- CAGR (2026-2033): 5.3%

Moreover, the increasing adoption of outsourcing laboratory services by pharmaceutical & biotechnology companies and other end users to reduce the overall cost of research activities further supports the market growth over the forecast period. Increased focus on diagnostics owing to COVID-19 led to a rise in funding for novel diagnostics with the potential to improve diagnosis scenarios. For instance, in April 2023, according to LabCentral 2022 Impact Report, companies raised USD 6.05 billion in funding, including 21% of all early-stage funding globally, dosed 4,504 participants in 37 clinical trials, and granted 56 patents. Such strategies are likely to improve the demand for central laboratory services for clinical studies in the country. Furthermore, in March 2021, Bio-Techne Corporation opened a new immunoassay-focused R&D and manufacturing facility in Minneapolis, U.S. This facility is engaged in the production of ELLA immunoassay cartridges for rapid detection of biomarkers for the diagnosis of diseases. Thus, the opening of such manufacturing facilities in countries strengthens the production of immunoassay test kits for the diagnosis of infectious respiratory diseases during the forecast period.")

The preference of consumers toward small- and medium-scale enterprises is rising, owing to the presence of depth & breadth of specialty lab solutions. For instance, in February 2023, Cerba Research signed a Memorandum of Understanding (MoU) with Teddy Clinical Research Laboratory to enter into a joint venture with an aim to combine Teddy's well-established reputation in mainland China, known for providing high-quality central lab solutions backed by more than 12 years of clinical trial experience, with Cerba Research's technical capabilities and scientific expertise. Cerba Research excels in areas such as vaccines, immuno-oncology, cell & gene therapy, and infectious disease research and drug development.

The presence of up-to-date and novel instruments in the new laboratory is expected to enhance automation and provide more efficient results with high-quality data. In May 2023, the China Association of Clinical Laboratory Practice Expo stood as the premier exhibition for IVD within China. Drawing a gathering of more than 30,000 experts, including entrepreneurs, scholars, users, and thought leaders in the clinical laboratory sector from across the world, CACLP fosters the exchange of advancements in the industry. It serves as a platform for enhancing partnerships and collectively shaping the future of the IVD industry. However, changes in government regulations can adversely affect the central lab market growth.

Central laboratories play a critical role in the clinical research ecosystem by providing standardized testing, data consistency, and logistical support that are essential for the success of global clinical trials. Labcorp, a leading central lab provider, exemplifies this through a well-structured set of four core services designed to ensure precision and reliability across every phase of sample management.

Central laboratories are pivotal in expediting the drug development process by implementing innovative strategies that address traditional challenges of time and cost. According to a November 2024 article by REPROCELL, three key approaches-automation, outsourcing, and artificial intelligence (AI) are instrumental in accelerating clinical trials and bringing new treatments to market more efficiently.

Market Dynamics

The central lab market is driven by increasing clinical trial activities, rising demand for biomarker testing, growing prevalence of chronic diseases, and advancements in molecular diagnostics. Demand for standardized, high-throughput testing and regulatory compliance supports growth, while high operational costs and logistical complexities remain key market challenges.

The growing volume of clinical trials and increasing adoption of biomarker-driven drug development are among the strongest drivers of the central lab market. Pharmaceutical and biotechnology companies are increasingly outsourcing laboratory testing to central laboratories to ensure standardized sample processing, data consistency, regulatory compliance, and multicenter trial coordination. Central laboratories play a critical role in managing biospecimens, genomic testing, biomarker validation, pharmacokinetic analysis, and companion diagnostics across geographically dispersed trial sites. The growing emphasis on precision medicine, oncology therapeutics, and targeted biologics has substantially increased demand for sophisticated central lab capabilities.

According to the U.S. FDA’s September 2024 guidance on decentralized clinical trials, clinical studies are increasingly incorporating remote and hybrid models, which require centralized laboratory infrastructure for consistent diagnostic testing and data harmonization across study locations. For instance, companies such as Labcorp Drug Development and IQVIA are expanding biomarker and genomic laboratory capabilities to support oncology and rare disease trials. Additionally, global drug development spending continues to increase, reinforcing demand for central laboratory services in Phase I-IV studies.

One of the major restraints affecting the central lab market is the high operational cost associated with global sample logistics, storage, regulatory compliance, and sophisticated testing infrastructure. Central laboratories require significant investment in cold-chain transportation, biospecimen preservation, automated analyzers, laboratory information management systems (LIMS), and highly trained personnel to maintain data integrity and testing accuracy. Multinational clinical trials further increase complexity due to varying regional regulations for sample movement, customs approvals, and patient data privacy. For example, biomarker-based oncology trials frequently require ultra-low temperature storage and rapid transport of blood or tissue samples across continents, significantly increasing operating expenses. In 2024, several diagnostic companies reported continued pressure from cautious biotechnology spending and higher operating costs. Bio-Rad Laboratories highlighted weak demand from biotech customers and a slower recovery environment in 2024, reflecting financial constraints across the broader clinical research ecosystem that can indirectly limit outsourcing to central laboratories.

The expansion of decentralized clinical trials (DCTs) presents a major growth opportunity for the central lab market. Increasing use of telemedicine, remote patient monitoring, wearable devices, and home-based participation models is transforming clinical trial operations, creating demand for centralized diagnostic coordination and remote sample management. In September 2024, the FDA issued final guidance supporting decentralized clinical trials, emphasizing the use of local healthcare providers and remote laboratory testing to improve patient recruitment, retention, and diversity in trials. This transition significantly increases the need for central laboratories capable of coordinating standardized testing from dispersed collection sites while maintaining regulatory-grade quality control. For example, hybrid clinical trials in oncology and neurology increasingly depend on centralized biomarker analysis despite geographically distributed participants. According to recent academic evidence published in October 2024, decentralized clinical trials are expanding rapidly because they improve patient accessibility and real-world data collection, creating long-term opportunities for technologically advanced central laboratory service providers.

Market Concentration & Characteristics

The industry demonstrates a high degree of innovation, driven by the integration of advanced technologies like artificial intelligence (AI), automation, and next-generation sequencing (NGS). These advancements have enhanced the precision and efficiency of laboratory services. For instance, AI-driven systems are now capable of orchestrating complex laboratory workflows, leading to more streamlined operations and accelerated drug discovery processes. Additionally, the adoption of self-driving labs, which utilize AI for real-time coordination of instruments and personnel, is transforming traditional laboratory settings into more dynamic and responsive environments.

The industry experiences a high level of mergers and acquisitions (M&A), as major players seek to broaden their technological capabilities, enhance their product portfolios, and enter new regional markets. Several market players are acquiring smaller players to strengthen their market position. For example, Eurofins Scientific has been actively acquiring companies to bolster its capabilities, including the acquisition of Orchid Cellmark in the UK and Infinity Laboratories in the US. Similarly, SYNLAB Group has continued its expansion through strategic acquisitions, enhancing its diagnostic services across Europe. In India, Metropolis Healthcare has acquired Agra-based Scientific Pathology and Delhi NCR-based Core Diagnostics to strengthen its presence in North India. These M&A activities are reshaping the competitive landscape, allowing central labs to offer more comprehensive and integrated services.

Regulatory frameworks play a pivotal role in shaping the industry. In the US, the Food and Drug Administration (FDA) has implemented new rules requiring laboratory-developed tests (LDTs) to undergo FDA authorization, aiming to ensure the accuracy and reliability of these tests. This move is expected to enhance patient safety but may also increase the operational burden on laboratories. Globally, central labs are adapting to stricter data privacy regulations, such as the General Data Protection Regulation (GDPR) in Europe, necessitating robust data management and security protocols. Compliance with these regulations is essential for maintaining trust and ensuring the integrity of laboratory services.

Service expansion in the central labs industry is at a high level, with companies diversifying their portfolios to address a broader range of diseases. There is a growing emphasis on specialized testing services, including oncology, neurology, and infectious diseases. Advancements in diagnostics, such as liquid biopsy and NGS, are enabling more precise and early detection of diseases, thereby increasing the demand for specialized lab services. Furthermore, the integration of point-of-care testing (POCT) technologies is allowing for rapid testing at the patient’s location, enhancing the accessibility and convenience of laboratory services. These expansions are positioning central labs as critical players in modern healthcare delivery.

The industry is witnessing a medium to high level of regional expansion as companies aim to tap into growth opportunities in emerging markets while solidifying their presence in established regions. Asia-Pacific, Latin America, and the Middle East are becoming key targets. In June 2024, Labcorp introduced Labcorp Global Trial Connect, a suite of central laboratory solutions designed to expedite clinical trials by streamlining workflows and reducing data delays. Asia-Pacific is emerging as the fastest-growing region in the central labs market, propelled by a surge in clinical trials and investments in healthcare infrastructure. In June 2024, Pharmaceutical Product Development (PPD) launched central laboratory services in China, recognizing the country's burgeoning clinical research landscape. Similarly, in February 2023, Cerba Research signed a Memorandum of Understanding with Teddy Clinical Research Laboratory to establish a joint venture, combining Teddy's established presence in China with Cerba's technical expertise.

Analyst Perspective

The central lab market is expected to witness sustained growth over the coming years, primarily driven by the increasing complexity of clinical trials, rising outsourcing trends among pharmaceutical and biotechnology companies, and growing demand for biomarker-driven precision medicine. As clinical studies become more globalized and decentralized, sponsors increasingly rely on central laboratories to ensure standardized testing, regulatory compliance, and data consistency across multiple study sites. The growing adoption of genomic testing, companion diagnostics, and advanced biomarker analysis is further strengthening the market outlook.

Analysts observe that oncology, rare diseases, immunology, and cell & gene therapy pipelines are significantly expanding the need for specialized laboratory testing services. Additionally, the shift toward decentralized and hybrid clinical trials is creating new growth opportunities for central labs capable of integrating remote sample collection, digital pathology, and advanced data analytics. However, operational complexities, sample logistics, regulatory challenges, and pricing pressures may continue to affect profitability. Despite these challenges, continuous technological advancements, automation, and increasing clinical R&D expenditure are expected to position the central lab market for long-term expansion globally.

Services Insights

Based on service, the biomarker services segment led the market with the largest revenue share of 38.3% in 2025. Biomarkers represent a promising option for clinical development programs to ascertain new pathways for diagnostics and discern disease mechanisms for the development of better therapeutics. Biomarker studies provide early detection of life-threatening diseases, evaluation of the risk of side effects associated with investigation therapies, and disease progression in patients during clinical trials. Moreover, it helps in understanding a patient’s success prospects for the respective therapy, which creates opportunities for introducing personalized & precision medicines. Hence, the research related to biomarkers is one of the lucrative services offered by central laboratories, and multiple biomarkers are being used in clinical trials.

Emerging trends include advancements in omics technologies, personalized medicine, liquid biopsies for cancer detection, and the integration of artificial intelligence (AI) and machine learning in biomarker discovery and analysis. These innovations are enhancing the efficiency and accuracy of biomarker identification, enabling the development of more effective personalized medicine approaches. In August 2024, Illumina received FDA approval for its TruSight Oncology (TSO) Comprehensive test, which analyzes over 500 genes in solid tumors. This advancement improves the detection of immuno-oncology biomarkers and actionable mutations, aiding in targeted therapy selection and clinical trial eligibility.

The genetic services segment is anticipated to grow at the fastest rate over the forecast period with a CAGR of 7.79%. The growth is driven by the increasing significance of genetic analysis in clinical studies.Understanding the underlying genetic factors can aid in the development of targeted therapies for a variety of diseases, such as cancer and inheritable diseases. Furthermore, genetic differences in pathways for drug metabolism may alter a patient’s response to treatment. Hence, genetic services can add value to trial analysis and help guide treatment options.In addition, growing adoption of next-generation sequencing and growth of molecular testing options, driven by advancements in PCR technologies, are anticipated to boost the market growth for genetic services. In January 2024, Genomic Health launched a new portfolio of personalized genomic testing services to advance patient outcomes in cancer diagnostics. Additionally, in February 2024, Illumina introduced its new next-generation sequencing platform, the NextSeq 1000, aiming for greater throughput and cost-effectiveness in genomic research.

End-use Insights

Based on end use, the pharmaceutical companies segment led the market with the largest revenue share of 45.3% in 2025. The pharmaceutical industry develops, manufactures, and transports pharmaceuticals or prescription products to be used as medications to be provided to patients in order to heal, vaccinate, or relieve symptoms. Pharma companies may sell generic and branded drugs as well as medical equipment. Pharmaceutical companies rely on central laboratory service providers to evaluate the efficacy of new drug products. For the evaluation of investigational drugs, the service providers offer tests such as biochemistry, hematology, histopathology, immunology, endocrinology, microbiology, real-time PCR, and clinical pathology.Furthermore, market players are partnering with pharmaceutical companies to strengthen their service offerings and expand their geographic footprint. For instance, in April 2023, Sygnature Discovery collaborated with Daewoong Pharmaceutical to boost its global innovations in drug development.

The biotechnology companies segment is anticipated to grow at the fastest rate over the forecast period.The increase in activities for the development of biological therapies is expected to drive the market in the coming years. By 2025, the U.S. FDA will approve 10 to 20 cell & gene therapy products per year.The market for cell and gene therapy-related services, which includes contract development & manufacturing, analytical testing, and regulatory consulting, has also been growing rapidly in response to the demand for these therapies. Moreover, Pace Analytical expanded its capabilities to support gene therapy projects by investing in analytical equipment, including capillary electrophoresis, Ultrapressure Liquid Chromatography (UPLC), large-molecule time-of-flight mass spectroscopy, and microplate readers.

Regional Insights

North America dominated the central lab market with the largest revenue share of 41.6% in 2025. The market is collectively driven by the increasing adoption of molecular testing due to its high accuracy, sensitivity, and specificity. The high prevalence of infections such as Sexually Transmitted Infections (STIs) & tuberculosis in the region is also anticipated to propel the demand for clinical research pertaining to the development of diagnostic devices and therapeutics. For instance, according to the CDC, in March 2022, in the U.S., over 20 million new cases of STIs are expected to occur annually, leading to approximately USD 10-USD 17 billion in costs per year, and the prevalence is expected to grow further. Moreover, key players are constantly focusing on expanding their presence in the field of clinical development. For instance, in July 2022, Labcorp announced the development of its spin-off company focusing on clinical development to enhance CRO capabilities. These factors are anticipated to positively impact the market growth in the region.

U.S. Central Lab Market Trends

The central lab market in the U.S. held the largest share in the North America region in 2025. The central lab market in the U.S. is advancing steadily, supported by a robust biopharmaceutical pipeline and increasing demand for specialized testing in clinical trials. The expansion of precision medicine and personalized therapies is driving sponsors to rely more heavily on centralized lab testing for consistency and data integrity. Recent developments include strategic collaborations between central labs and clinical research organizations (CROs) to streamline study timelines and enhance sample logistics. The U.S. also benefits from a well-established logistics infrastructure and digital health adoption, which allow central labs to efficiently manage large volumes of specimens. Key players are investing in automation and AI-based data analytics to boost throughput and quality control. Additionally, the rising number of decentralized and hybrid clinical trials is prompting U.S. central labs to integrate remote data collection technologies. These trends present opportunities for innovation in sample tracking systems and partnerships to support global studies led from the U.S.

Europe Central Lab Market Trends

The central lab market in Europe is experiencing steady growth, largely driven by the region’s role as a hub for multi-country clinical trials and complex biologic studies. The harmonization of regulatory requirements under the EU Clinical Trial Regulation (CTR) has simplified cross-border trial operations, benefiting central lab services. Recent developments include the integration of digital pathology and cloud-based lab data platforms that enhance cross-site collaboration. Additionally, there is a rising interest in biomarker-driven studies, which require advanced central lab capabilities such as genomic and proteomic analyses. Central labs in Europe are expanding their geographic presence to align with sponsors seeking pan-European coverage.

The UK central lab market is undergoing dynamic transformation, supported by strong clinical research infrastructure and government initiatives post-Brexit to maintain leadership in life sciences. The UK’s Medicines and Healthcare products Regulatory Agency (MHRA) has introduced streamlined processes for trial approvals, attracting international sponsors. Central labs are responding by expanding service offerings such as advanced biomarker analysis, companion diagnostics, and digital histology. Recent partnerships between academic institutions and private labs have also bolstered capacity and innovation. The increasing demand for centralized testing in oncology and rare disease trials is prompting investment in high-throughput instrumentation and AI-powered image analysis. Furthermore, with the UK prioritizing genomics and precision medicine, central labs are integrating next-generation sequencing (NGS) workflows.

The central lab market in Germany is growing steadily, propelled by the country’s reputation for high-quality clinical research and regulatory excellence. German central labs are key partners in large-scale trials conducted across the EU and are investing in automation to manage increasing test volumes. A major driver is the demand for standardized and validated laboratory results, particularly in immunology and oncology studies. Recent developments include the incorporation of electronic data capture (EDC) and integrated laboratory information management systems (LIMS) to streamline sample tracking and reporting. Collaborations with CROs and pharmaceutical firms have increased, with a focus on delivering real-time data and remote access to lab results. The government’s support for digital health and biopharma innovation is encouraging further investment in centralized lab infrastructure.

Asia Pacific Central Lab Market Trends

The central lab market in Asia Pacific is expected to witness the fastest CAGR of 7.82% over the forecast period due to the increasing adoption of central lab services in the region. The region comprises over one-third of the global population. China and India are considered prospective business hubs for clinical testing & service providers. Furthermore, with urbanization, an increase in disposable income, awareness about the prevention of severe diseases, and education, the market is expected to grow in this region. Asia Pacific markets, such as Australia, China, Korea already have healthcare reimbursement systems, which provide coverage for diagnostic tests. In addition, Positive developments like government healthcare benefits raised public knowledge, and a willingness to pay for top-notch medical care are also anticipated to fuel market expansion.

China central lab market is experiencing strong momentum, driven by a surge in domestic clinical trials and increased participation in global studies. The government’s continued push for pharmaceutical innovation and fast-track regulatory pathways has significantly expanded the clinical research landscape. Central labs in China are scaling operations to meet demand for specialized testing, particularly in oncology and cell and gene therapies. Recent developments include the adoption of AI for histopathological image analysis and cloud-based data management systems that support multicenter trials. Leading labs are also forming strategic alliances with international CROs to provide end-to-end lab services for global sponsors. Opportunities are emerging in supporting multi-regional clinical trials (MRCTs) as China becomes a key destination for patient recruitment. Moreover, as clinical trials decentralize, Chinese central labs are investing in logistics and cold chain management to ensure timely and secure sample transportation, a critical factor in maintaining data reliability and regulatory compliance.

The central labs market in Japan is advancing steadily, bolstered by a strong demand for standardized testing in global and domestic clinical trials. The country’s demographic trend of an aging population has increased research in chronic diseases and oncology, creating consistent demand for central lab services. Regulatory reforms by Japan’s Pharmaceuticals and Medical Devices Agency (PMDA) to expedite clinical trial approvals have further stimulated lab testing volumes. Recent developments include the integration of AI-driven diagnostic tools in central labs to enhance data precision and efficiency.

Latin America Central Lab Market Trends

The central lab market in Latin America is gaining traction due to rising clinical trial activity in countries like Mexico, Argentina, and Colombia. Sponsors are increasingly turning to Latin America for its cost-effective trial operations and genetically diverse populations. This has spurred demand for central lab services that ensure uniform testing standards across distributed trial sites. Recent trends include the expansion of regional central labs and the introduction of multilingual laboratory information systems to handle cross-border studies. Moreover, growing investment from global CROs and pharma companies has led to infrastructure development in urban centers. Opportunities are particularly promising in trials for infectious diseases and chronic conditions such as diabetes, where centralized testing helps maintain data integrity.

Brazil central labs market is expanding rapidly, supported by a robust healthcare system and government backing for pharmaceutical R&D. The country is a key player in Latin America’s clinical trials landscape, and central labs are crucial for managing the logistics of multi-site trials. A major driver is Brazil’s regulatory improvements, including faster approvals for clinical studies under ANVISA. Recent investments in laboratory automation, digital pathology, and cloud-based data systems have enhanced the capabilities of leading central labs. The growing trend of decentralized clinical trials has spurred interest in mobile phlebotomy and remote specimen tracking, offering new growth opportunities. Brazil’s strategic role in South American trials makes it a vital node in the global central lab network.

Middle East & Africa Central Lab Market Trends

The central lab market in the Middle East and Africa (MEA) is on a growth path, supported by expanding clinical research in countries like the UAE, South Africa, and Egypt. As pharmaceutical companies explore untapped markets, the need for reliable centralized testing has grown. In the Gulf region, particularly the UAE and Qatar, investments in clinical trial infrastructure have led to the development of new central lab facilities with international accreditations. Recent developments include partnerships between local labs and global CROs to build integrated testing networks that align with ICH-GCP standards. In Africa, donor-funded health programs are driving trials for infectious diseases, creating consistent demand for centralized testing.

Saudi Arabia central lab market is growing steadily, aligned with the country’s Vision 2030 plan to expand healthcare and become a regional hub for clinical research. Government initiatives to attract multinational pharmaceutical trials are boosting demand for advanced central laboratory services. The Saudi Food and Drug Authority (SFDA) has streamlined clinical trial processes, making the country more attractive for global sponsors. Recently, central labs have adopted automated testing platforms and electronic data capture tools to enhance efficiency and regulatory compliance. Collaborations with universities and research hospitals have increased, enabling central labs to offer a wider range of molecular and genomic testing services.

Key Central Lab Companies Insights

Key players operating in the central lab market are undertaking various initiatives to strengthen their presence and increase the reach of their products and services. Strategies such as expansion activities and partnerships are key in propelling the market growth.

Key Central Lab Companies

The following key companies have been profiled for this study on the central lab market.

-

ACM Global Laboratories

-

Labconnect

-

Cerba Research

-

Eurofins Scientific

-

Medicover Integrated Clinical Services (MICS) (Synevo Central Labs

-

Versiti (Cenetron)

-

A.P. Møller Holding A/S (Unilabs)

-

Ampersand Capital Partners (Pacific Biomarkers)

-

Lambda Therapeutics Research Ltd

-

Cirion Biopharma Research Inc.

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Well-Established Players (Labcorp Drug Development, IQVIA Laboratories, ICON plc, Eurofins Scientific, Medpace)

- Established players focus on expanding global laboratory networks, strengthening biomarker and genomic testing capabilities, investing in automation, regulatory compliance, acquisitions, and strategic partnerships with pharmaceutical and biotechnology companies to support large-scale multicenter clinical trials.

- Established players benefit from strong brand recognition, extensive geographic presence, broad service portfolios, advanced laboratory infrastructure, deep regulatory expertise, and long-standing relationships with pharmaceutical sponsors, enabling high reliability and operational scalability.

- Mature companies often face high operational and infrastructure costs, slower adaptation to emerging technologies, dependence on large clinical trial contracts, and complexities associated with managing global logistics and regulatory requirements.

Emerging Players (Frontage Laboratories, Precision for Medicine, Cerba Research, Nexelis, BioAgilytix)

- Emerging companies focus on specialized biomarker testing, precision medicine capabilities, niche therapeutic expertise, decentralized clinical trial support, flexible pricing models, and strategic collaborations to strengthen market positioning and expand service offerings.

- Emerging players gain a competitive advantage through technological agility, faster adoption of advanced genomic and biomarker testing, personalized customer support, specialized therapeutic expertise, and flexible service models tailored to smaller biotech firms.

- Emerging companies may face challenges including limited financial resources, lower brand visibility, narrower geographic coverage, regulatory limitations, and difficulties competing with large central laboratories for multinational pharmaceutical contracts.

Recent Developments

-

In June 2024, Labcorp introduced Labcorp Global Trial Connect, a suite of central laboratory solutions designed to expedite clinical trials by streamlining workflows and reducing data delays.

-

In July 2023, Versiti announced the acquisition of Quantigen, an Indiana-based company, to expand its clinical trial and service offerings.

-

In May 2023, LabConnect entered into strategic alliance with Labor Dr. Wisplinghoff to provide tailormade and high-quality central lab services in Europe.

Central Lab Market Report Scope

Report Attribute

Details

Market size in 2025

USD 3.8 billion

Estimated market size in 2026

USD 4.1 billion

Projected market size by 2033

USD 5.9 billion

Growth rate

CAGR of 5.3% from 2026 to 2033

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Service, End Use, Regional

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; Norway; Denmark; Sweden; China; Japan; India; South Korea; Australia; Thailand; Brazil; Argentina; Saudi Arabia; South Africa; UAE; Kuwait

Key companies profiled

ACM Global Laboratories; Labconnect; Cerba Research; Eurofins Scientific; Medicover Integrated Clinical Services (MICS) (Synevo Central Labs; Versiti (Cenetron); A.P. Møller Holding A/S (Unilabs); Ampersand Capital Partners (Pacific Biomarkers); Lambda Therapeutics Research Ltd; Cirion Biopharma Research Inc.

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Central Lab Market Report Segmentation

This report forecasts revenue growth and provides an analysis of the latest trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global central lab market report on the basis of services, end-use, and regions:

-

Services Outlook (Revenue, USD Million, 2021 - 2033)

-

Genetic Services

-

Biomarker Services

-

Microbiology Services

-

Anatomic Pathology/ Histology

-

Specimen Management & Storage

-

Special Chemistry Services

-

Others

-

-

End-use Outlook (Revenue, USD Million, 2021 - 2033)

-

Pharmaceutical companies

-

Biotechnology Companies

-

Academic and Research Institutes

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

Japan

-

China

-

India

-

Australia

-

South Korea

-

Thailand

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East and Africa (MEA)

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Research Methodology

The central lab market figures in this report are based on a proven research process that combines executive interviews with secondary research from proprietary databases, company filings, and recognized regulatory and institutional sources. Market size is built through value-chain sizing - reconciling supply-side and demand-side estimates - and triangulated with bottom-up and top-down approaches. Every estimate passes multiple levels of expert validation before publication, with each central lab segment quantified using the revenue-capture definitions in the table belowc

Segment Definition

Segment - Service

Revenue capture definition

Genetic Services

Revenue is generated through genomic sequencing, prenatal screening, hereditary disease testing, pharmacogenomics, and molecular analysis supporting precision medicine and clinical trials.

Biomarker Services

Revenue comes from biomarker discovery, validation, companion diagnostics, protein analysis, and disease monitoring services supporting oncology, immunology, and drug development.

Microbiology Services

Revenue is derived from pathogen detection, antimicrobial resistance testing, infectious disease diagnostics, culture testing, and molecular microbiology services for trials.

Anatomic Pathology/Histology

Revenue is generated through tissue examination, histopathology, biopsy analysis, slide preparation, staining, and cancer diagnostic support for clinical research.

Specimen Management & Storage

Revenue arises from biospecimen collection, processing, tracking, biobanking, cold-chain logistics, storage, and long-term preservation supporting multicenter clinical studies.

Special Chemistry Services

Revenue is generated through endocrine testing, toxicology, immunochemistry, metabolic analysis, therapeutic drug monitoring, and specialized biochemical laboratory assessments.

Others

Revenue includes data management, clinical trial support, regulatory testing, cytogenetics, hematology, safety monitoring, and customized laboratory outsourcing solutions.

Segment - End Use

Revenue capture definition

Pharmaceutical Companies

Revenue is generated through central laboratory services supporting drug discovery, clinical trials, biomarker testing, safety assessments, and regulatory submissions.

Biotechnology Companies

Revenue comes from specialized testing, genomic analysis, biomarker validation, and laboratory support for biologics, precision therapies, and early-stage research.

Academic & Research Institutes

Revenue is derived from laboratory testing, translational research support, specimen analysis, grant-funded studies, and collaborative scientific investigation programs.

Estimation Model

The estimation model for the central lab market is developed using a combination of top-down and bottom-up approaches to ensure accurate market sizing and forecasting. The analysis begins with identifying the overall clinical trial and laboratory services market, followed by segmentation based on service type, end use, therapeutic area, and region. Revenue generated by major central laboratory service providers-including clinical trial support, biomarker testing, genetic services, microbiology, pathology, and specimen management-is assessed through annual reports, financial filings, and company disclosures.

A bottom-up methodology is applied by evaluating revenues of key market participants and aggregating segment-level performance across pharmaceutical companies, biotechnology firms, and research institutions. Simultaneously, a top-down approach validates findings using clinical trial volume, R&D expenditure, outsourcing trends, and healthcare investments. Market forecasts are further refined through analysis of macroeconomic indicators, regulatory developments, adoption of decentralized clinical trials, and expert interviews to ensure reliable projections and data triangulation.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Central Lab Market Competitive Landscape & Service Assessment

Assessed the global central lab market across genetic services, biomarker testing, microbiology, pathology/histology, specimen management, and special chemistry services. Evaluated key companies, service portfolios, therapeutic expertise, and laboratory automation capabilities.

Helped identify market growth opportunities, benchmark competitors, evaluate outsourcing trends, and assess service differentiation across clinical trial support segments.

Central Lab Clinical Trial Outsourcing & Technology Evaluation

Analyzed central laboratory outsourcing trends across pharmaceutical, biotechnology, and research organizations. Assessed adoption of biomarker testing, genomic analysis, decentralized trial support, digital pathology, and laboratory informatics platforms.

Supported strategic decision-making by identifying technology adoption patterns, improving vendor selection, and evaluating operational efficiencies in multicenter clinical trials.

Central Lab Regional Expansion & Service Benchmarking

Evaluated regional central lab capabilities, regulatory compliance requirements, logistics infrastructure, specimen management systems, and testing capacities across North America, Europe, Asia-Pacific, and emerging markets.

Enabled assessment of regional expansion opportunities, optimization of laboratory partnerships, regulatory preparedness, and competitive positioning for global clinical research operations.

Frequently Asked Questions About This Report

Based on service, the biomarker services segment led the market with the largest revenue share of 38.3% in 2025.

Key players operating in the central lab market are ACM Global Laboratories, LabConnect, Cerba Research, Eurofins Scientific, Medicover Integrated Clinical Services, Versiti, A.P. Møller Holding A/S, Ampersand Capital Partners, Lambda Therapeutics Research Ltd, and Cirion Biopharma Research Inc.

Key factors that are driving the central lab market growth include increasing investment in R&D and increased focus of sponsors & investigators on reducing research costs. The outsourcing of central lab work is further driving the market growth.

The global central lab market size was valued at USD 3.8 billion in 2025 and is projected to reach USD 4.1 billion in 2026.

The global central lab market is expected to grow at a compound annual growth rate of 5.3% from 2026 to 2033 to reach USD 5.9 billion in 2033.

Based on end use, the pharmaceutical companies segment led the market with the largest revenue share of 45.3% in 2025.

About the Author(s)

Clinical Diagnostics Research Team

Healthcare · Clinical DiagnosticsThis report was authored by the clinical diagnostics research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the clinical diagnostics segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.