- Home

- »

- Next Generation Technologies

- »

-

Cloud Integration Software Market Size Report, 2026-2033GVR Report cover

![Cloud Integration Software Market (2026 - 2033)Report]()

Cloud Integration Software Market (2026 - 2033)

Size, Share & Trends Analysis Report By Type (IaaS, SaaS, PaaS), By Enterprise Size, By End-use (IT & Telecom, BFSI, Healthcare, Retail & E-commerce, Manufacturing), By Region, And Segment Forecasts

Market Size, 2025

$7.1BMarket Estimate, 2026

$8.0BMarket Forecast, 2033

$20.5BCAGR, 2026–2033

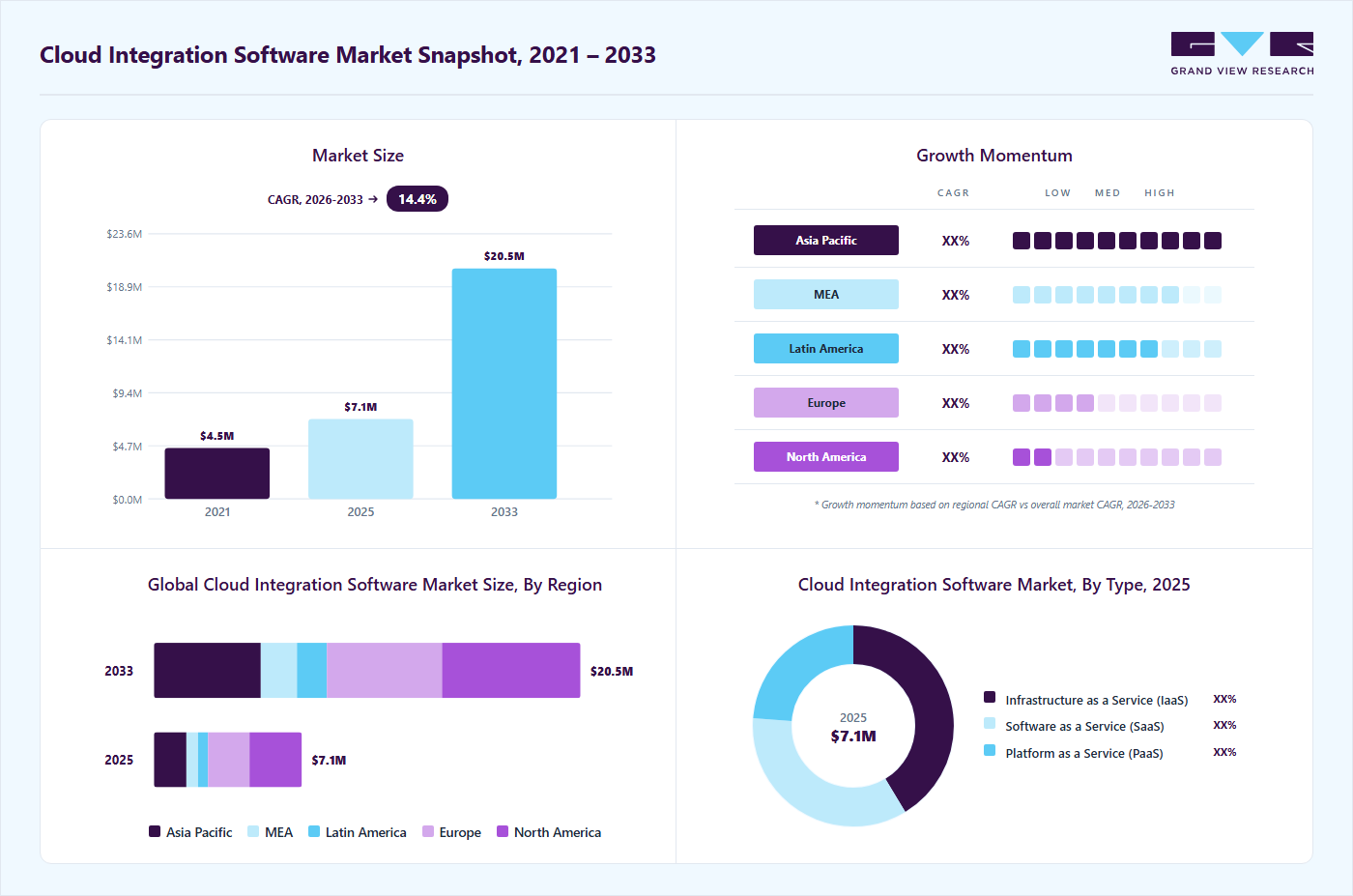

14.4%Cloud Integration Software Market Summary

The global cloud integration software market size was valued at USD 7.1 billion in 2025 and is projected to grow from USD 8.0 billion in 2026 to USD 20.5 billion by 2033, at a CAGR of 14.4% from 2026 to 2033. The market in North America dominated with a revenue share of 35.4% in 2025. Due to the increasing adoption of cloud computing across various industries, driving the growth of the market. As businesses transition to the cloud, they often encounter a complex landscape of disparate applications, databases, and systems that need to share data.

Key Market Trends & Insights

- By type: The Infrastructure as a Service (IaaS) segment accounted for the largest revenue share of 41.3% in 2025.

- By enterprise size: The large enterprises segment accounted for the largest share in 2025.

- By end-use: The IT & telecom segment accounted for the largest market share in 2025.

Regional Highlights

- Largest regional market: North America (35.4% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 7.1 Billion

- Estimated market size in 2026: USD 8.0 Billion

- Projected market size by 2033: USD 20.5 Billion

- CAGR (2026-2033): 14.4%

Cloud integration software enables seamless data transfer and helps businesses integrate on-premises and cloud-based applications, fostering a cohesive IT environment. These solutions enable seamless integration of applications, data, and processes across cloud and on-premise systems, supporting real-time data exchange and unified operations. The market is expected to expand at a strong double-digit growth rate, driven by the rising complexity of enterprise IT ecosystems and the growing use of Software-as-a-Service (SaaS) applications that require efficient connectivity and orchestration.A key factor driving demand is the need for operational efficiency and faster decision-making through integrated data flows. Enterprises are investing in integration platforms to reduce data silos, improve workflow automation, and enable advanced analytics. The emergence of low-code and no-code integration tools, along with API management and event-driven architectures, is further accelerating adoption across industries such as BFSI, retail, and manufacturing. In addition, small and medium enterprises are adopting cloud integration solutions due to their scalability and reduced deployment complexity.

")

In addition, leading technology providers are forming strategic partnerships to enhance integration capabilities and expand cloud ecosystems. Such collaborations are focused on combining cloud infrastructure with AI-driven tools to deliver more seamless and intelligent integration solutions. For instance, in April 2024, Cloud Software Group and Microsoft Corporation announced an eight-year partnership to expand cloud and AI integration, strengthening Citrix solutions with Microsoft Corporation Azure. The collaboration enhances digital workspace offerings, accelerates cloud adoption, and integrates generative AI tools like GitHub Copilot to improve productivity. This partnership will drive innovation and increase the adoption of cloud integration software across enterprises.

Market Dynamics

The cloud integration software market is being strongly driven by the growing need for real-time data connectivity, faster analytics, and cost-efficient management of complex hybrid and multi-cloud environments. As enterprises increasingly rely on distributed data systems, they require integration platforms that unify data from multiple sources, support seamless interoperability across on-premises and cloud systems, and enable faster decision-making. In addition, the rising adoption of AI and advanced analytics is pushing organizations to modernize their data infrastructure, creating demand for scalable integration solutions that can process large volumes of data at high speed and with high reliability while optimizing operational costs.

For instance, in May 2025, Qlik launched Open Lakehouse within its Qlik Talend Cloud, built on Apache Iceberg. This solution strengthens cloud integration capabilities by enabling real-time data ingestion, delivering up to 5 times faster query performance, and reducing infrastructure costs by up to 50%. It also supports cross-engine interoperability and native deployment on Amazon Web Services, making it highly suitable for AI-driven analytics use cases. Overall, this development highlights how innovation in data lakehouse architectures and real-time integration is accelerating the growth of the cloud integration software market.

One key restraint in the cloud integration software market is vendor lock-in and limited interoperability across different cloud platforms. Many organizations use multiple cloud providers such as AWS, Microsoft Azure, and Google Cloud, but integration between them is often not seamless. This creates dependency on a single vendor ecosystem and reduces flexibility in switching or expanding services. As a result, enterprises face higher long-term costs and operational constraints. This challenge slows down the adoption of multi-cloud strategies. It also limits businesses' ability to fully optimize their cloud environments.

Another important restraint is performance and governance challenges in complex IT environments. Many enterprises operate hybrid systems that combine on-premise infrastructure with cloud applications, which often leads to latency and data synchronization issues. In addition, the rapid growth of APIs across applications creates API sprawl, making it difficult to manage versions, security, and usage effectively. This increases integration complexity and operational risks for large organizations. Businesses often struggle to maintain consistent performance across integrated systems. These issues reduce confidence in large-scale cloud integration deployments.

Market Concentration & Characteristics

The cloud integration software market is moderately concentrated. A few global technology leaders hold strong enterprise share, but many specialized and regional providers continue to compete by offering niche integration capabilities. Overall market growth is strong, supported by rapid cloud adoption, hybrid IT expansion, and increasing demand for real-time data connectivity across applications. The pace of market growth is also accelerating as organizations modernize legacy systems and shift toward multi-cloud environments. This ongoing transformation is pushing enterprises to adopt more advanced integration platforms faster than in previous years. As a result, the market is expanding quickly while gradually consolidating among leading players.

From a structural perspective, the market is shaped by high innovation, active consolidation, and strong enterprise-driven demand. Innovation remains a key driver as vendors continuously enhance API management, automation, and AI-enabled integration capabilities to improve efficiency and reduce complexity. Mergers and acquisitions are also significant, as larger technology firms acquire smaller integration specialists to strengthen their cloud and data ecosystems. Regulatory requirements for data privacy and governance further influence market behavior, underscoring the need for secure, compliant integration solutions. At the same time, moderate substitution from in-house tools and native cloud services create competitive pressure. End-user concentration is relatively high, with large enterprises across banking, telecom, and retail accounting for a major share of demand.

Type Insights

The Infrastructure as a Service (IaaS) segment accounted for the largest revenue share of 41.3% in 2025, by providing scalable compute infrastructure, storage, and networking resources that enable seamless integration across hybrid and multi-cloud environments. It supports key functions such as data integration, API management, workload automation, and real-time analytics, allowing enterprises to unify distributed systems and reduce infrastructure complexity. Organizations increasingly adopt IaaS due to its cost efficiency, pay-as-you-go pricing, and rapid scalability, which align with the growing demand for flexible digital transformation strategies and multi-cloud deployments. Furthermore, IaaS enhances cloud-native integration, microservices architecture, and event-driven workflows, making it essential for modern enterprise IT ecosystems.

The Platform as a Service (PaaS) segment is anticipated to grow at the fastest CAGR from 2026 to 2033, driven by a scalable application development environment, pre-built integration capabilities, and managed infrastructure that reduce operational complexity. It enables organizations to build, deploy, and integrate applications without managing underlying hardware, thereby accelerating digital transformation, API integration, and workflow automation. PaaS platforms are increasingly integrated with Integration Platform as a Service (iPaaS) solution, allowing seamless connectivity across cloud and on-premise systems, supporting use cases such as data synchronization, process orchestration, and real-time analytics. The rise of low-code/no-code development, microservices architecture, and containerization further strengthens the adoption of PaaS in integration-centric environments.

Enterprise Size Insights

The large enterprise segment accounted for the largest revenue share in 2025. Cloud integration software is crucial in large enterprises by facilitating the seamless connection of various applications and data. Moreover, it enables organizations to efficiently manage the data between hybrid environments, where some applications and data are on-premises and others are in the cloud. It ensures smooth interaction between on-premises applications and cloud-based resources, enhancing operational efficiency and data accessibility.

The SMEs segment is anticipated to grow at a significant CAGR during the forecast period, as small and medium enterprises adopt cloud-based integration, iPaaS solutions, and low-code platforms to streamline operations and reduce IT complexity. Limited budgets and resource constraints are driving SMEs toward cost-efficient, scalable, and easy-to-deploy integration tools that connect SaaS applications, APIs, and legacy systems into a unified ecosystem. The rising use of multiple cloud applications has created a need for real-time data integration, workflow automation, and centralized data management, enabling SMEs to improve decision-making and operational efficiency.

End-use Insights

The IT & telecom segment accounted for the largest market share in 2025, driven by the need to manage complex, distributed networks and enable real-time data integration, API-led connectivity, and cloud-native architectures. Telecom operators are increasingly leveraging integrated platforms to unify OSS/BSS systems, support 5G deployments, and enhance network automation and customer experience management. The growing volume of data from connected devices and digital services is further accelerating demand for AI-enabled integration, multi-cloud orchestration, and event-driven architectures across telecom ecosystems. In addition, companies are shifting toward API-based integration frameworks to reduce legacy system dependencies and improve scalability and agility in service delivery. For instance, in April 2025, Deutsche Telekom expanded its partnership with Google Cloud through 2030 to advance cloud integration, data platforms, and AI adoption. The collaboration includes SAP migration, development of a unified data ecosystem, and use of Vertex AI to enhance analytics and operational efficiency. This partnership will accelerate demand for cloud integration software by promoting scalable, AI-driven data integration across telecom and enterprise environments.

The manufacturing segment is anticipated to grow at the highest CAGR from 2026 to 2033, driven by the need for real-time data integration, operational efficiency, and scalable production systems. Manufacturers increasingly use cloud platforms to connect shop-floor systems, IoT devices, and enterprise applications, enabling end-to-end visibility across production, supply chain, and inventory management. Cloud integration supports predictive maintenance, digital twins, and AI-driven analytics, helping reduce downtime and improve product quality. It also enhances interoperability between legacy systems and modern applications, which is critical in complex industrial environments.

Regional Insights

North America cloud integration software market held the major share of the global market in 2025. The presence of developed cloud infrastructure in the region creates opportunities for seamless deployment and operation of cloud integration solutions. Many companies are launching solutions to cater to the increasing demand for cloud-integrated solutions. In addition, strategic collaborations among major technology providers are further enhancing integration capabilities and supporting the growth of multicloud environments in the region. For instance, in June 2024, Oracle and Google Cloud announced a multicloud partnership enabling integration of Oracle Cloud Infrastructure with Google Cloud services. The collaboration supports seamless data connectivity, application migration, and unified management, enhancing flexibility for enterprises across North America adopting hybrid and multicloud strategies. This partnership will strengthen the North America cloud integration software market by accelerating multicloud adoption and improving interoperability across enterprise platforms.

U.S. Cloud Integration Software Market Trends

The cloud integration software market in the U.S. is expected to grow significantly from 2026 to 2033. The increasing use of API-led integration and real-time data orchestration is enabling organizations to connect SaaS, legacy, and cloud-native applications efficiently. In addition, rising investments in digital transformation and iPaaS platforms are supporting workflow automation and enhanced data visibility across enterprises. Strict regulatory compliance requirements such as HIPAA and CCPA are further accelerating adoption of secure and auditable integration solutions.

Asia Pacific Cloud Integration Software Market Trends

The cloud integration software market in the Asia Pacific is growing significantly from 2026 to 2033, driven by rapid cloud adoption among SMEs, increasing digital transformation initiatives, and the expansion of multi-cloud and hybrid IT environments across enterprises. The region is emerging as the fastest-growing market, supported by rising investments in SaaS and PaaS platforms that enable scalable and flexible integration capabilities. In addition, the surge in real-time data integration needs across industries such as BFSI, manufacturing, and retail is accelerating demand for advanced integration tools. Governments and enterprises in countries like India, China, and Japan are also promoting cloud-first strategies and data localization frameworks, further boosting adoption. The growing use of API management, iPaaS solutions, and low-code integration tools is enhancing operational efficiency and reducing deployment complexity.

China cloud integration software market held a significant share in 2025, driven by rapid AI integration, hybrid cloud adoption, and increasing enterprise demand for multi-cloud management solutions. Enterprises in China increasingly adopt hybrid and private cloud environments, creating demand for integration platforms that enable seamless data synchronization and interoperability across systems. In addition, the surge in AI workloads and data-intensive applications is accelerating the need for scalable integration tools to connect cloud services, databases, and analytics platforms. Government-led initiatives and data localization requirements are further pushing organizations toward secure cloud integration frameworks and localized ecosystems.

The cloud integration software market in Japan held a significant share in 2025, driven by rapid digital transformation (DX) initiatives and the urgent need to modernize legacy IT systems associated with the “2025 IT cliff,” which is accelerating demand for integration platforms (iPaaS) and middleware solutions. The market is further supported by increasing adoption of hybrid and multi-cloud environments, requiring seamless data integration, interoperability, and API management across distributed systems. Government-led policies such as the “cloud-by-default” strategy and data sovereignty requirements are encouraging enterprises to deploy secure, locally compliant integration solutions.

India cloud integration software market is expanding rapidly, driven by rapid digital transformation, rising hybrid and multi-cloud adoption, and increasing demand for real-time data integration across enterprise applications. Businesses are increasingly adopting API-led connectivity and iPaaS (integration platform as a service) to streamline operations and enable scalable, flexible IT environments. In addition, government-led data localization policies and investments in data center infrastructure are encouraging enterprises to deploy integrated cloud solutions within India. The surge in AI adoption and analytics-driven decision-making is further accelerating demand for intelligent integration tools that enable seamless data flow across systems.

Europe Cloud integration software Market Trends

The cloud integration software market in Europe is growing significantly from 2025 to 2033. The region’s strong focus on digital transformation initiatives and the EU’s Digital Single Market strategy is accelerating enterprise adoption of cloud-based integration platforms. In addition, the rise of multi-cloud and hybrid cloud environments is creating demand for seamless interoperability and data migration solutions across diverse systems. Growing emphasis on data sovereignty and local cloud infrastructure is further pushing organizations to adopt compliant integration tools tailored to regional requirements.

The cloud integration software market in the UK is expected to grow rapidly in the coming years, supported by strong digital transformation, multi-cloud adoption, and increasing demand for real-time data integration across enterprises. Increasing adoption of hybrid and multi-cloud architectures among UK organizations to avoid vendor lock-in and improve flexibility is a key factor boosting demand for integration tools. The growing use of API-led connectivity, AI-driven analytics, and low-code integration platforms is further accelerating deployment across industries.

Germany cloud integration software market held a significant market share in 2025, driven by strong digital transformation, Industry 4.0 adoption, and increasing demand for real-time data integration across manufacturing and enterprise systems. Organizations are prioritizing GDPR compliance, data sovereignty, and secure data exchange, leading to higher adoption of integration tools that ensure regulatory alignment and localized data processing. In addition, the rapid use of AI, IoT, and big data analytics is increasing the need for scalable integration solutions to manage complex data environments efficiently.

Key Cloud Integration Software Company Insights

Some of the key companies operating in the market include Alibaba Cloud, Amazon Web Services, Inc., Boomi, LP, Cloud Software Group, Inc., Informatica, International Business Machines Corp, Microsoft Corporation, among others are some of the leading participants in the cloud integration software market.

-

In December 2025, Al Jazeera Media Network partnered with Google Cloud to launch “The Core,” an AI-integrated journalism model. The initiative leverages generative AI and cloud platforms to integrate workflows, enhance data processing, and streamline content production across its global news operations. This development will boost the cloud integration software market by driving the adoption of AI-enabled workflow integration in the media industry.

-

In November 2025, Salesforce completed the acquisition of Informatica to strengthen its cloud integration and data management capabilities. Integration enhances data connectivity, governance, and unified analytics, supporting scalable AI-driven operations and enabling enterprises to leverage integrated, high-quality data across applications and systems.

-

In December 2024, Cleo released a 2024 update to Cleo Integration Cloud, introducing procurement automation, accelerated partner onboarding, and a Supplier Relationship Manager. The enhancements improve supply chain orchestration, enable real-time data integration, and strengthen end-to-end visibility for enterprises across manufacturing, retail, and logistics sectors.

Key Cloud Integration Software Companies:

The following key companies have been profiled for this study on the cloud integration software market.

- Alibaba Cloud

- Amazon Web Services, Inc.

- Boomi, LP

- Cloud Software Group, Inc.

- Informatica

- International Business Machines corp.

- Microsoft Corporation

- Oracle

- Red Hat, Inc

- Salesforce, Inc.

- Tencent Cloud

- VMware, Inc.

- WORKATO

- Zapier Inc.

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: Amazon Web Services (AWS); Microsoft Corporation; Oracle; International Business Machines (IBM); Salesforce, Inc.; Informatica

- Focus on expanding cloud ecosystems through continuous platform enhancement and AI-driven integration capabilities.

- Strengthening enterprise customer relationships through strategic partnerships, acquisitions, and industry-specific solutions.

- Strong global customer base and established enterprise credibility across industries.

- Broad product portfolios combining cloud infrastructure, analytics, API management, and integration services.

- Higher implementation costs and deployment complexity for some enterprise customers.

- Large platform ecosystems can create operational complexity and longer deployment cycles.

Emerging Players: Boomi, LP; Workato; Zapier Inc.; Tencent Cloud

- Focus on automation, low-code/no-code integration, and simplified deployment models.

- Expand market presence through ecosystem partnerships and cloud-native integration capabilities.

- Faster innovation cycles and greater flexibility in addressing evolving customer requirements.

- User-friendly integration platforms that reduce technical complexity and implementation time.

- Lower enterprise penetration compared to established technology leaders.

- Limited global reach or narrower product portfolios in certain regions and industries.

Cloud Integration Software Market Report Scope

Report Attribute

Details

Market size in 2025

USD 7.1 billion

Estimated market size in 2026

USD 8.0 billion

Projected market size by 2033

USD 20.5 billion

Growth rate

CAGR of 14.4% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Type, enterprise size, end-use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Thailand; Brazil; UAE; Saudi Arabia; South Africa

Key companies profiled

Alibaba Cloud; Amazon Web Services, Inc.; Boomi, LP; Cloud Software Group, Inc.; Informatica; International Business Machines corp.; Microsoft Corporation; Oracle; Red Hat, Inc; Salesforce, Inc.; Tencent Cloud; VMware, Inc.; WORKATO; Zapier Inc.

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Cloud Integration Software Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global cloud integration software market report based on type, enterprise size, end-use, and region.

-

Type Outlook (Revenue, USD Billion, 2021 - 2033)

-

Infrastructure as a Service (IaaS)

-

Software as a Service (SaaS)

-

Platform as a Service (PaaS)

-

-

Enterprise Size Outlook (Revenue, USD Billion, 2021 - 2033)

-

Large Enterprises

-

Cloud

-

Small and Medium Sized Enterprises (SMEs)

-

-

End-use Outlook (Revenue, USD Billion, 2021 - 2033)

-

IT & Telecom

-

BFSI

-

Healthcare

-

Retail and E-Commerce

-

Manufacturing

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

Thailand

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Europe-focused cloud integration software market with country-level breakdown

- Added country-wise analysis for key European markets such as Germany, UK, France, and Nordics

- Expanded segmentation by industry adoption across BFSI, healthcare, and manufacturing in Europe

- Enabled precise understanding of regional demand differences and compliance-driven adoption patterns

- Supported market entry and expansion strategy for Europe-specific investments

- Helped identify high-growth countries within Europe for targeted sales and partnerships

Inclusion of additional key global players beyond the standard vendor list

- Expanded competitive landscape to include emerging players in iPaaS and API management segments

- Included recent market entrants focusing on AI-driven integration platforms

- Provided a more complete competitive benchmarking view beyond dominant vendors

- Helped identify acquisition targets and niche innovation leaders

Country-specific players in Germany and France

- Added Germany and France-specific key offering cloud integration services

- Enabled identification of localized competitors not visible in global vendor lists

Frequently Asked Questions About This Report

The infrastructure as a service (IaaS) segment led with a 41.3% revenue share in 2025, while platform as a service (PaaS) is the fastest-growing segment.

The large enterprises held the largest revenue share in 2025.

North America dominated with a 35.4% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

The global cloud integration software market size was valued at USD 7.1 billion in 2025 and is expected to reach USD 8.0 billion in 2026.

The global cloud integration software market is expected to grow at a compound annual growth rate of 14.4% from 2026 to 2033 to reach USD 20.5 billion by 2033.

The IT & telecom segment accounted for the largest market share in 2025.

Key players include Alibaba Cloud, Amazon Web Services, Inc., Boomi, LP, Cloud Software Group, Inc., Informatica, International Business Machines Corp., Microsoft Corporation, Oracle, Red Hat, Inc, Salesforce, Inc., Tencent Cloud, VMware, Inc., WORKATO, Zapier Inc., and others.

Factors such as seamless integration of applications, data, and processes across cloud and on-premises systems, supporting real-time data exchange and unified operations, are driving the growth of the cloud integration software market.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.