- Home

- »

- Automotive & Transportation

- »

-

Cold Chain Market Size, Share & Growth Report, 2026-2033GVR Report cover

![Cold Chain Market (2026 - 2033)Report]()

Cold Chain Market (2026 - 2033)

Size, Share & Trends Analysis Report By Type (Storage, Transportation), By Temperature Range, By Application (Food & Beverages, Pharmaceuticals), By Region, And Segment Forecasts

Market Size, 2025

$371.1BMarket Estimate, 2026

$437.5BMarket Forecast, 2033

$1,611.0BCAGR, 2026–2033

20.5%Cold Chain Market Summary

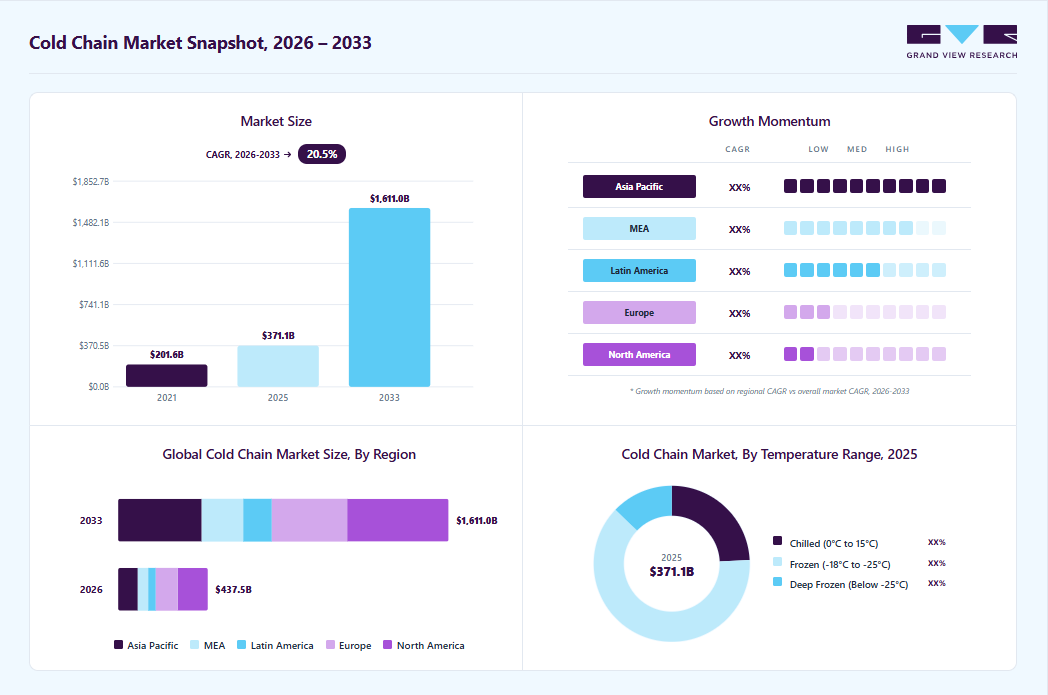

The global cold chain market size was valued at USD 371.1 billion in 2025 and is projected to grow from USD 437.5 billion in 2026 to USD 1,611.0 billion by 2033, at a CAGR of 20.5% from 2026 to 2033. North America dominated the cold chain market with the largest revenue share of 33.3% in 2025. Changes in consumer preferences and growing e-commerce sales are expected to drive the market.

Key Market Trends & Insights

- By type: Storage segment dominated the overall cold chain market with a revenue share of 51.8% in 2025.

- By temperature range: Frozen segment led the market with the largest revenue share of 53.4% in 2025.

- By application: Food & beverages segment led the market with the largest revenue share of 76.8% in 2025.

Regional Highlights

- Largest regional market: North America (33.3% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 371.1 Billion

- Estimated market size in 2026: USD 437.5 Billion

- Projected market size by 2033: USD 1,611.0 Billion

- CAGR (2026-2033): 20.5%

An increasing number of organized retail stores in developing economies is leading to the growing demand for cold chain solutions. Rising investment in cold chains and government initiatives to minimize food waste are expected to boost market growth. The growing adoption of technologies such as RFID and automation in cold chain applications provides significant growth opportunities for the market. The World Trade Organization (WTO) and bilateral free trade agreements, such as the European Union Free Trade Agreement (FTA) and the North America Free Trade Agreement (NAFTA), have created opportunities for exporters in the U.S. and Europe to increase trade for perishable foods in a manner that is free of import duties.The refrigerated storage market in developing economies is driven by a shift from carbohydrate-rich diets to protein-rich foods, owing to rising consumer awareness. Countries such as China are expected to portray a significant growth rate over the coming years due to a consumer-led economic transition. With growing technological advancements in warehouse management and refrigerated transportation, the market will likely expand in developing economies.

")

Increasing IT spending in cold storage logistics drives the growth of the cold chain market by facilitating better inventory management and improving the overall efficiency of cold chain supply systems. By investing in advanced technologies such as cloud computing, IoT, and RFID, cold storage operators can track and monitor their inventory in real time, reducing the risk of food waste, spoilage, and product recalls. The rising demand for temperature-sensitive products has emphasized the need for real-time cold chain monitoring.

Furthermore, several countries have strict regulations governing the transportation and storage of perishable food products to ensure food safety and quality. Compliance with these regulations often requires a robust cold chain system, which can be achieved with the help of IT systems. IT systems are critical in complying with these regulations as they provide real-time monitoring of temperature and humidity levels, location tracking, and data analytics.

Furthermore, several countries have strict regulations governing the transportation and storage of perishable food products to ensure food safety and quality. Compliance with these regulations often requires a robust cold chain system, which can be achieved with the help of IT systems. IT systems are critical in complying with these regulations as they provide real-time monitoring of temperature and humidity levels, location tracking, and data analytics. For instance, temperature monitoring devices such as data loggers, sensors, and RFID tags can be used to collect and transmit temperature data, which can be analyzed to ensure compliance. For example, the United States Food and Drug Administration (FDA), through the Food Safety Modernization Act (FSMA), and the European Union, through the European Union Food Hygiene Regulations have established stringent regulations for the storage and transportation of perishable food products. Both regulatory bodies mandate that all food products be transported and stored in a temperature-controlled environment and that temperature data must be collected and analyzed to ensure adherence to the regulations.

Market Dynamics

The cold chain market is driven by the growing demand for temperature-controlled storage and transportation of perishable goods, increasing global trade of food products, pharmaceuticals, and biologics, and stringent regulations regarding product safety and quality. Businesses are increasingly investing in advanced cold storage facilities, refrigerated transportation, and monitoring technologies to maintain product integrity throughout the supply chain. Industries such as food & beverages, pharmaceuticals, chemicals, and agriculture rely on cold chain infrastructure to minimize spoilage, ensure regulatory compliance, and extend product shelf life. Technological advancements such as IoT-enabled monitoring systems, automation in cold warehouses, real-time tracking solutions, and energy-efficient refrigeration technologies are further enhancing cold chain efficiency. However, high infrastructure and operating costs, energy consumption concerns, and logistical complexities continue to influence market growth.

Market Dynamics

The increasing consumption of perishable food products and the expanding pharmaceutical industry are major factors driving the cold chain market. Rising consumer demand for fresh fruits, vegetables, dairy products, seafood, meat products, and frozen foods has significantly increased the need for reliable cold storage and refrigerated transportation solutions. In parallel, the growing production and distribution of vaccines, biologics, specialty drugs, and other temperature-sensitive pharmaceuticals require stringent temperature control throughout the supply chain.

Cold chain systems help preserve product quality, reduce spoilage, and ensure compliance with food safety and pharmaceutical regulations. Additionally, the growth of e-commerce grocery delivery services and international trade of perishable products is increasing the need for advanced cold chain infrastructure. As supply chains become more globalized and product quality requirements become more stringent, demand for efficient cold chain solutions continues to accelerate.

Despite strong growth prospects, the cold chain market faces several challenges related to high capital investments and operational complexities. Establishing and maintaining cold storage facilities, refrigerated transportation fleets, and temperature-monitoring systems require substantial financial resources. Energy costs associated with refrigeration equipment represent a significant portion of operational expenses, particularly in regions with high electricity costs. In addition, maintaining consistent temperature conditions across multiple transportation and storage stages can be challenging, especially in developing regions with inadequate infrastructure. Equipment failures, power outages, and transportation delays can lead to product spoilage and financial losses.

The cold chain market presents significant opportunities through the rapid growth of pharmaceutical logistics, automation, and digital supply chain technologies. The increasing demand for temperature-sensitive vaccines, biologics, cell and gene therapies, and specialty medicines is driving investments in advanced pharmaceutical cold chain infrastructure. Regulatory requirements for product traceability and temperature compliance are further supporting market expansion. The adoption of smart cold chain solutions, including IoT sensors, real-time temperature monitoring, predictive analytics, and cloud-based tracking platforms, is creating new opportunities for enhanced visibility and operational efficiency. Additionally, the development of automated cold warehouses, energy-efficient refrigeration systems, and sustainable logistics practices is improving supply chain performance while reducing operational costs.

Analyst Perspective

The cold chain market continues to benefit from growing demand for temperature-controlled storage and transportation of perishable food products, pharmaceuticals, biologics, and other sensitive goods. However, rising energy costs, infrastructure constraints, and increasing sustainability requirements are influencing the pace and direction of market expansion. In response, industry participants are investing in automated cold storage facilities, energy-efficient refrigeration systems, and digitally connected supply chain solutions to improve operational efficiency and reduce product losses. Technologies such as IoT-enabled temperature monitoring, real-time tracking, warehouse automation, and predictive analytics are gaining traction to enhance visibility, compliance, and reliability across cold chain operations.

Type Insights

Based on type, the market is segmented into storage, and transportation. The storage segment led the market with the largest revenue share of 51.8% in 2025. The growth can be attributed to an increasing preference for packaged foods across the globe. Consumers changing dietary patterns and lifestyles are driving the demand for frozen foods. This is expected to boost the demand for storage solutions. Moreover, market players are expanding their storage capacities to meet cold storage needs. At the same time, the cold chain equipment market is also gaining better momentum.

Cold chain systems are crucial for supplying healthcare and food & beverage products. Demand for cold chain transportation solutions such as refrigerated containers and vehicles to safely transport temperature-sensitive goods is expected to drive the transportation segment over the forecast period.

Efficient cold storage management greatly depends on software and hardware components used for monitoring purposes. Hardware components include data loggers, remote temperature sensors, RFID devices, networking devices, and telematics devices. The stringent regulatory environment in the pharmaceutical industry surrounding the maintenance of product quality has positively influenced the adoption of cold chain temperature monitoring solutions.

Temperature Range Insights

Based on temperature range, the market is segmented into chilled (0°C to 15°C), frozen (-18°C to -25°C), and deep-frozen (below -25°C). The frozen segment led the market with the largest revenue share of 53.4% in 2025. Poultry, cakes & bread, and meat need freezing temperatures to remain fresh. This is driving the need for frozen cold chain solutions to preserve the quality of perishable food & beverage and pharmaceutical products. Moreover, the wide availability of cold chain storage and transportation solutions for frozen temperature ranges drives the segment’s growth.

The chilled (0°C to 15°C) segment is expected to grow at a notable CAGR over the forecast period. To remain fresh, many vegetables, fruits, and meat require chilled temperature ranges, usually between 2°C to 4°C, during transportation. Chilled temperature storage of perishable products such as dairy products prevents deterioration, increasing shelf life. Maintaining the quality of perishable goods and minimizing wastage is driving the segment's growth.

Application Insights

Based on application, the market is segmented into pharmaceuticals, food & beverages, and others. The food & beverages segment led the market with the largest revenue share of 76.8% in 2025. Technological developments in the storage, packaging, and processing of seafood are anticipated to boost the growth of this segment. However, processed food is projected to grow significantly over the forecast years owing to continued innovations in packaging materials. Advancements in packaging materials increase the shelf life of foods. This has increased the sales of processed foods over the past few years.

The pharmaceuticals segment is expected to register significant growth over the forecast period. High product demand in the pharmaceuticals segment can be attributed to its importance in maintaining the efficacy and safety of pharmaceuticals. The cold chain in the pharmaceutical industry is driven by stringent regulatory norms, such as Goods Distribution Practices (GDP) in the European Union (EU). These regulations are a shift witnessed in governments across the world toward standardizing regulations globally for better transportation systems for healthcare-related products.

Regional Insights

North America dominated the cold chain market with the largest revenue share of 33.3% in 2025. It will retain the dominant position throughout the forecast period as the region has significant growth opportunities for the companies planning to invest in the long haul. Increasing penetration of connected devices and a large consumer base are also expected to fuel market growth over the forecast period.

U.S. Cold Chain Market Trends

The cold chain market in the U.S. held the largest share in the North America region in 2025. The U.S. cold chain market is driven by various factors, including changing consumer preferences, increasing demand for fresh and frozen foods, and the growth of e-commerce. One of the major drivers of the U.S. cold chain market is the increasing demand for fresh and frozen foods. Consumers are increasingly seeking fresh, healthy, and locally sourced foods and are willing to pay a premium price for high-quality products. This has increased the demand for cold chain logistics services as companies seek to ensure that their products are delivered to consumers in optimal condition.

Europe Cold Chain Market Trends

The Europe cold chain market was identified as a lucrative region in 2025. Demand is being driven by rising consumption of perishable foods, stringent pharmaceutical regulations, and a growing emphasis on sustainability across the supply chain. The EU’s regulatory landscape, especially regarding food safety (e.g., EU Regulation 852/2004) and pharmaceutical transport (e.g., GDP guidelines) has encouraged greater investments in temperature-controlled logistics infrastructure. Additionally, the market is benefiting from the modernization of cold storage facilities, integration of IoT-enabled monitoring systems, and increasing cross-border trade in perishables and biologics. Countries such as Germany, the Netherlands, and France are leading adoption, supported by strong logistics infrastructure, advanced retail networks, and export-oriented agri-food sectors.

The UK cold chain industry is expected to grow rapidly in the coming years. Key drivers include the expansion of online grocery and meal delivery services, growth in temperature-sensitive pharmaceutical logistics (especially post-Brexit), and increasing demand for traceability and compliance with national food safety standards.

Asia Pacific Cold Chain Market Trend

Asia Pacific is anticipated to register the highest growth over the forecast period, owing to increasing government investments in logistics infrastructure development and penetration of Warehouse Management Systems (WMS). The growing awareness of the importance of food safety among consumers in the Asia Pacific region, particularly when it comes to perishable goods, is leading to greater demand for cold chain logistics.

The China cold chain market is a major contributor to the Asia Pacific regional market. The market growth in China is attributed to factors such as technological advancements in the packaging, processing, and storage of seafood products. Rising demand and growing cold chain infrastructure development have made China a top market for cold chains. China is undergoing a rapid transition from a construction- & manufacturing-led economy to a consumer-led economy. Rising innovations in the pharmaceutical sector in China are also expected to boost the demand for cold chain solutions. Another major factor driving the market includes the rapid expansion of biopharma in the region.

Key Cold Chain Company Insights

Some of the key players operating in the market include Americold Logistics LLC, LINEAGE LOGISTICS HOLDING, LLC, Burris Logistics, and Wabash National Corporation, among others.

-

Americold Logistics LLC is a U.S.-based temperature-controlled warehousing and transportation company that serves the food industry. The company offers solutions such as producer solutions and retailer solutions. Under producer solutions, the company offers dedicated facilities, public refrigerated warehouses, port facilities, automation, and integrated consolidation programs. Under retailer solutions, the company offers integrated consolidation programs, i-3PL supply chains, system integration services, port facilities, automation, and network optimization study. The company makes significant investments in technology to stay ahead of the competition. The company has a presence across regions including APAC and the Americas.

-

LINEAGE LOGISTICS HOLDING, LLC provides warehousing and logistics solutions to users in various industries. The company’s solutions consist of temperature controlled public warehousing facilities for storing multiple food commodities, including pork, beef, poultry, bakery products, fruits & vegetables, seafood, ice creams, and vegetables. It also provides port-centric cold chain facilities on the East and West Coasts to serve containerized markets and break bulk.

Key Cold Chain Companies

The following are the leading companies in the cold chain market.

-

Americold Logistics, Inc.

-

LINEAGE LOGISTICS HOLDING, LLC

-

United States Cold Storage

-

Burris Logistics

-

Wabash National Corporation

-

NewCold

-

Sonoco ThermoSafe (Sonoco Products Company)

-

United Parcel Service of America, Inc.

-

A.P. Moller - Maersk

-

NICHIREI CORPORATION

-

Tippmann Group

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (Americold Logistics, Inc.; Lineage Logistics Holding, LLC; United States Cold Storage; Burris Logistics; NewCold; Tippmann Group; Nichirei Corporation)

Expand temperature-controlled warehousing networks through facility acquisitions, capacity expansions, and strategic partnerships

Invest in warehouse automation, robotics, and digital monitoring technologies to improve operational efficiency and storage utilization

Extensive cold storage infrastructure and nationwide/global distribution networks.

Long-standing relationships with major food producers, retailers, pharmaceutical companies, and distributors

High capital requirements for facility development, maintenance, and modernization

Significant exposure to energy costs and refrigeration-related operating expenses

Emerging & Specialized Players (Wabash National Corporation; Sonoco ThermoSafe; UPS Healthcare; A.P. Moller–Maersk and other specialized cold chain solution providers)

Focus on specialized cold chain segments such as refrigerated transportation, temperature-controlled packaging, pharmaceutical logistics, and integrated end-to-end cold chain solutions

Develop smart monitoring, real-time tracking, and sustainable refrigeration technologies to enhance service differentiation

High flexibility and ability to address niche cold chain requirements across healthcare, food, and international trade sectors.

Strong expertise in transportation equipment, temperature-controlled packaging, and global logistics networks

Limited cold storage asset ownership compared to large warehouse operators

Greater dependence on specific end-use sectors such as pharmaceuticals or transportation services

Recent Developments

-

In October 2025, Carrier Transicold used Intermodal Europe 2025 to showcase its newest container-refrigeration technologies focused on efficiency, sustainability and reliability. The company highlighted the OptimaLINE system, now past 25,000 units sold, and the EverFRESH® controlled-atmosphere technology that slows ripening and protects high-value perishables during long voyages. Together, these systems provide exporters and shipping lines with better cargo quality, lower energy use, and greater operational flexibility.

-

In November 2024, Lineage, Inc. announced the acquisition of Coldpoint's assets, a Kansas City-based provider of cold storage and transportation solutions. This strategic move expands Lineage's footprint in the Kansas City area, enhances its services along the protein corridor with direct rail access to U.S. ports, and integrates Coldpoint's 621,000-square-foot facility with advanced intermodal capabilities into its global network.

-

In November 2024, CJ Logistics America opened a state-of-the-art, 270,000-square-foot cold storage warehouse in Georgia, U.S., strategically located near major highways and railways in a key poultry production region. Equipped with advanced refrigeration and blast freezing systems, the facility offers tailored storage solutions for various products, including proteins, bakery items, and finished goods, with 30,000 racked pallet positions and on-site USDA inspection capabilities. This investment reinforces CJ Logistics America's commitment to delivering premium cold chain solutions to leading global brands.

Cold Chain Market Report Scope

Report Attribute

Details

Market size in 2025

USD 371.1 billion

Estimated market size in 2026

USD 437.5 billion

Projected market size by 2033

USD 1,611.0 billion

Growth rate

CAGR of 20.5% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Type, temperature range, application, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Germany; U.K; France; China; India; Japan; South Korea; Australia; Brazil; Mexico; KSA; UAE; South Africa

Key companies profiled

Americold Logistics, Inc.; LINEAGE LOGISTICS HOLDING, LLC; United States Cold Storage; Burris Logistics; Wabash National Corporation; NewCold; Sonoco ThermoSafe (Sonoco Products Company); United Parcel Service of America, Inc.; A.P. Moller - Maersk; NICHIREI CORPORATION; Tippmann Group

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Cold Chain Market Report Segmentation

This report forecasts revenue growths at global, regional, and country levels and provides an analysis of the industry trends in each of the sub-segments from 2021 to 2033. For the purpose of this study, Grand View Research has segmented the global cold chain market based on type, temperature range, application, and region:

-

Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Storage

-

Facilities/Services

-

Refrigerated Warehouse

-

Private & Semi-Private

-

Public

-

-

Cold Room

-

-

Equipment

-

Blast freezer

-

Walk-in Cooler and Freezer

-

Deep Freezer

-

Others

-

-

-

Transportation

-

By Mode

-

Road

-

Sea

-

Rail

-

Air

-

-

By Offering

-

Refrigerated vehicles

-

Refrigerated containers

-

-

-

-

Temperature Range Outlook (Revenue, USD Million, 2021 - 2033)

-

Chilled (0°C to 15°C)

-

Frozen (-18°C to -25°C)

-

Deep-frozen (Below -25°C)

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Food & Beverages

-

Fruits & Vegetables

-

Fruit Pulp & Concentrates

-

Dairy Products

-

Milk

-

Butter

-

Cheese

-

Ice cream

-

Others

-

-

Fish, Meat, and Seafood

-

Processed Food

-

Bakery & Confectionary

-

Others

-

-

Pharmaceuticals

-

Vaccines

-

Blood Banking

-

Others

-

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Spain

-

Italy

-

Norway

-

Netherlands

-

Switzerland

-

Russia

-

-

Asia Pacific

-

China

-

Japan

-

India

-

Singapore

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

Kingdom of Saudi Arabia (KSA)

-

UAE

-

South Africa

-

-

Research Methodology

Segment Definition

Segment - Type

Revenue capture definition

Storage

This segment includes infrastructure used to store temperature-sensitive products under controlled conditions across the cold chain. It covers refrigerated warehouses, cold rooms, and specialized equipment such as blast freezers, walk-in coolers/freezers, and deep freezers used to preserve product quality and extend shelf life.

Transportation

This segment comprises logistics solutions used for moving temperature-sensitive goods while maintaining required thermal conditions. It includes refrigerated transport across road, sea, rail, and air, supported by refrigerated vehicles and containers to ensure uninterrupted cold chain integrity during transit.

Segment - Temperature Range

Revenue capture definition

Chilled (0°C to 15°C)

This segment includes temperature range that is used for storing fresh and perishable products such as dairy, fruits, vegetables, and beverages. It slows microbial growth without freezing the product, thereby maintaining freshness and short-term shelf life.

Frozen (-18°C to -25°C)

This range is commonly used for long-term storage of frozen food products such as meat, seafood, and processed foods. It preserves product quality by fully freezing moisture content and significantly reducing microbial and enzymatic activity.

Deep-frozen (Below -25°C)

This ultra-low temperature range is used for highly sensitive products requiring extended preservation, including specialty foods, pharmaceuticals, and certain biotech materials. It ensures maximum shelf stability by minimizing all biological and chemical activity.

Segment - Application

Revenue capture definition

Food & Beverages

Bhis segment includes temperature-controlled storage and logistics for perishable and semi-perishable food products. It covers the entire cold chain for products such as fruits, vegetables, dairy, meat, seafood, frozen foods, bakery, and confectionery items to maintain freshness, safety, and shelf life.

Pharmaceuticals

This segment includes temperature-controlled storage and transportation of healthcare and life science products requiring strict environmental conditions to maintain efficacy and safety.

Others

This segment includes all remaining temperature-sensitive products outside food and pharmaceutical applications. It typically covers chemicals, industrial materials, and specialty goods requiring controlled storage and transportation environments.

Estimation Model

Demand Opportunity Layer

Digital Access Layer

Implementation Layer

Monetisation Layer

Temperature Controlled Storage Requirements?

Infrastructure Coverage?

What infrastructure is actively deployed

How much revenue is generated?

Establish the total pool of products, industries, and supply chains that depend on cold chain infrastructure to preserve quality, safety, and shelf life..

Identify products and industries with sufficient infrastructure, regulatory requirements, and economic viability to utilize cold storage and refrigerated transportation.

Estimate actual cold chain capacity and service deployment by evaluating installed infrastructure, operational utilization rates, and investment activity.

Convert deployed cold chain capacity into market revenue using service pricing, equipment sales, leasing models, and operational spending.

Delivered Customizations

This report has been delivered with the following In-depth customizations

CLIENT REQUEST

CUSTOMIZATION DELIVERED

VALUE ADDS

Cold Chain Market Overview

Assessment of global demand for cold chain solutions across food & beverages, pharmaceuticals, chemicals, and industrial goods.

Analysis of key growth drivers such as rising demand for temperature-sensitive products, expansion of organized retail & e-commerce grocery delivery, and increasing pharmaceutical cold chain requirements (vaccines, biologics).Identified high-growth application areas such as frozen food logistics, pharma cold chain distribution, last-mile refrigerated delivery, and vaccine cold storage.

Technology & Product Innovation Analysis

Evaluation of refrigerated storage systems, reefer trucks & containers, cold rooms, temperature monitoring systems, and IoT-enabled cold chain solutions.

Highlighted innovation-led growth opportunities in smart cold chain logistics, digital temperature monitoring platforms, and sustainable refrigeration technologies

Competitive Landscape Assessment

Benchmarking of leading players including cold chain logistics providers, refrigerated storage manufacturers, and temperature-controlled transport companies.

Identified competitive positioning gaps in end-to-end integrated cold chain solutions, last-mile refrigerated logistics, and pharma-grade compliance capabilities

Frequently Asked Questions About This Report

North America held the largest revenue share of more than 33.3% in 2025. It will retain the dominant position throughout the forecast period as the region has significant growth opportunities for the companies planning to invest for the long haul. Increasing penetration of connected devices and a large consumer base are also expected to fuel market growth over the forecast period.

The global cold chain market was estimated at USD 371.1 billion in 2025 and is expected to reach USD 437.5 billion in 2026.

The storage segment accounted for the largest revenue share of more than 51.0% in 2025 in the cold chain market owing to an increasing preference for packaged foods globally.

The global cold chain market is expected to progress at a compound annual growth rate of 20.5% from 2026 to 2033 to reach USD 1611.0 billion in 2033.

Asia Pacific is the fastest-growing region over the forecast period.

The frozen segment dominated the market in 2025 with a share of 53.4% and is the fastest growing segment.

The food & beverages segment dominated the market in 2025 with a share of 76.8%.

The U.K. cold chain market dominated the market in Europe in 2025 with a share of 15.5%.

About the Author(s)

Automotive & Transportation Research Team

Technology · Automotive & TransportationThis report was authored by the automotive & transportation research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the automotive & transportation segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.