- Home

- »

- Plastics, Polymers & Resins

- »

-

Cold Chain Packaging Market Size, Share Report, 2026-2033GVR Report cover

![Cold Chain Packaging Market Size, Share & Trends Report]()

Cold Chain Packaging Market (2026 - 2033) Size, Share & Trends Analysis Report By Material (EPS, PUR), By Product (Insulated Containers, Insulated Pallet Shippers,Vacuum Insulated Panels, Gel Packs), By End-use, By Region, And Segment Forecasts

Market Size, 2025

$33.7BMarket Estimate, 2026

$38.3BMarket Forecast, 2033

$93.1BCAGR, 2026–2033

13.5%Cold Chain Packaging Market Summary

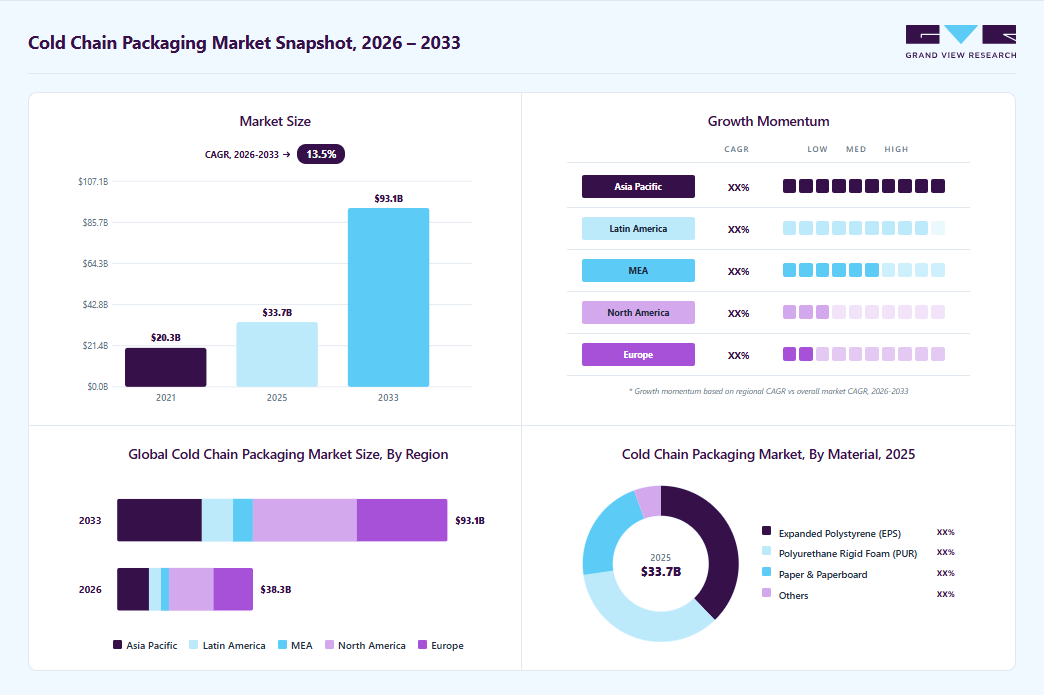

The global cold chain packaging market size was estimated at USD 33.7 billion in 2025 and is projected to grow from USD 38.3 billion in 2026 to USD 93.1 billion by 2033, at a CAGR of 13.5% from 2026 to 2033. North America held the largest market share of over 32.0% of the global cold chain packaging market in 2025. The market is driven by the rapid growth of biopharmaceuticals, vaccines, and temperature-sensitive healthcare logistics requiring reliable thermal protection.

Key Market Trends & Insights

- By material: Expanded polystyrene (EPS) segment dominated the market, accounting for over 38.0% revenue share in 2025.

- By product: Insulated containers segment dominated the market, accounting for over 41.0% in 2025.

- By end use: Fish, meat & seafood segment dominated in 2025, accounting for over 19.0% of total market share.

Regional Highlights

- Largest regional market: North America (over 32.0% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR of 15.0%, 2026-2033)

- By country: The U.S. dominated the North American market in 2025.

Market Size & Forecast

- Market size in 2025: USD 33.7 Billion

- Estimated market size in 2026: USD 38.3 Billion

- Projected market size by 2033: USD 93.1 Billion

- CAGR (2026-2033): 13.5%

It is also fueled by expanding global food trade, e-commerce grocery delivery, and stricter regulations for the safe transport of perishable products. The cold chain packaging industry is primarily driven by the rapid expansion of temperature-sensitive healthcare products, including vaccines, biologics, insulin, and specialty pharmaceuticals. With the rise of personalized medicine and complex biologic drugs, maintaining strict thermal stability during transportation has become critical. Regulatory bodies such as the FDA and WHO enforce stringent cold chain compliance, pushing pharmaceutical manufacturers and logistics providers to invest in validated, high-performance packaging solutions.

")

In addition, the booming global food and beverage supply chain, particularly for fresh produce, dairy, seafood, and frozen foods, is also positively impacting the industry outlook. Consumers increasingly demand year-round availability of perishable products, supported by international trade and modern retail formats. This has intensified the need for reliable insulated packaging, gel packs, and refrigerant systems that preserve freshness, extend shelf life, and reduce food waste during long-distance distribution.

The rise of e-commerce and direct-to-consumer delivery models is also accelerating demand for cold chain packaging. Online grocery platforms, meal-kit services, and home delivery of pharmaceuticals require compact, efficient, and cost-effective packaging that can maintain required temperatures through last-mile logistics. Reflecting this innovation push, in January 2026, Dawsongroup tcs USA launched in the U.S., introducing its high-performance modular cold chain system, Superbox, which provides ultra-precise temperature control, real-time monitoring, redundancy, and FDA/GMP compliance under a flexible leasing model that enables “logistics-on-demand” scaling.

Moreover, sustainability and material innovation are reshaping the competitive landscape. Companies are increasingly developing recyclable, biodegradable, and reusable cold chain packaging to meet environmental regulations and corporate ESG goals. Advances in phase change materials (PCMs), smart temperature-monitoring packaging, and reusable shipper systems are enabling longer duration performance while reducing waste and total logistics costs, making cold chain packaging a strategic priority across industries.

Market Concentration & Characteristics

A key characteristic of the industry is its strong focus on innovation and performance differentiation. Companies compete on the basis of insulation efficiency, temperature-hold duration, lightweight design, and the integration of smart monitoring technologies such as real-time sensors and data loggers. Advanced materials like phase change materials (PCMs), vacuum insulated panels (VIPs), and reusable systems are increasingly adopted to meet both operational efficiency and sustainability goals.

The industry also exhibits growing demand volatility and scalability needs due to the expansion of e-commerce, direct-to-patient pharmaceutical delivery, and emergency logistics. This has accelerated the adoption of flexible service models such as leasing and “packaging-as-a-service,” enabling customers to scale capacity without high upfront capital investment. Players are increasingly offering modular, reusable, and rental-based packaging systems to address cost pressures and unpredictable shipment volumes.

Material Insights

The expanded polystyrene (EPS) segment dominated the market in 2025, accounting for over 38.0% revenue share, primarily due to its excellent thermal insulation performance, lightweight nature, and cost-effectiveness for high-volume shipments. EPS is widely used in pharmaceutical and food logistics because it provides reliable temperature protection during transit while remaining easy to mold into customized packaging formats. In addition, its established supply chain availability and compatibility with both single-use and insulated shipper applications have reinforced its strong market penetration.

Paper & paperboard is expected to register the highest growth rate of 14.8% during the forecast period, driven by rising sustainability mandates and increasing demand for recyclable alternatives to traditional plastic-based cold chain packaging. Companies across pharmaceuticals and food logistics are adopting fiber-based insulated shippers and paper-derived thermal liners to reduce environmental impact and meet ESG commitments. In addition, advancements in coated paper technologies and hybrid paper insulation solutions are improving moisture resistance and thermal performance, accelerating adoption in temperature-sensitive distribution.

Product Insights

The insulated containers segment accounted for over 41.0% in 2025, driven by their critical role in ensuring reliable temperature control for high-value pharmaceutical, biologics, and perishable food shipments. These containers provide superior thermal protection, extended hold times, and compatibility with refrigerants such as gel packs and phase change materials, making them essential for long-distance and last-mile delivery. Their widespread adoption is further supported by stringent regulatory compliance requirements and the growing need for validated, reusable, and high-performance cold chain solutions.

The vacuum insulated panels (VIPs) segment is projected to grow at the fastest CAGR of 14.2% over the forecast period, driven by the rising demand for ultra-high thermal efficiency packaging in pharmaceutical and biologics distribution. VIPs offer significantly longer temperature hold times with thinner, lightweight designs compared to traditional insulation materials, making them ideal for high-value, long-duration shipments. Their adoption is further supported by the expansion of global vaccine supply chains, premium cold chain logistics, and increasing focus on reducing packaging size, waste, and transportation costs.

End Use Insights

The fish, meat & seafood segment dominated in 2025, accounting for over 19.0% of total market share, due to the highly perishable nature of these products and their strict temperature requirements throughout transportation and storage. Rising global consumption of protein-rich diets, expanding international seafood trade, and growth in frozen and chilled food distribution have significantly increased demand for reliable insulated packaging solutions. In addition, stringent food safety regulations and the need to prevent spoilage, contamination, and quality loss have reinforced the segment’s leading position in cold chain packaging adoption.

The pharmaceutical segment is expected to register a CAGR of 16.0% over the forecast period, driven by the rapid growth of biologics, vaccines, cell & gene therapies, and other temperature-sensitive drugs requiring strict cold chain compliance. Increasing global healthcare spending, expansion of clinical trials, and rising direct-to-patient delivery models are accelerating demand for advanced insulated packaging and real-time monitoring solutions. In addition, stringent regulatory standards such as FDA, GMP, and GDP are pushing pharmaceutical companies to adopt high-performance, validated cold chain packaging systems.

Regional Insights

North America dominated the cold chain packaging market in 2025, accounting for over 32.0% of global market share, driven by its advanced pharmaceutical cold chain packaging and biologics manufacturing base, strong frozen and processed food supply chains, and high adoption of temperature-controlled logistics technologies. The region benefits from stringent regulatory compliance standards (FDA, GDP), which accelerate demand for validated and high-performance pharmaceutical and general cold chain packaging solutions. In addition, the rapid expansion of e-commerce grocery delivery, direct-to-patient pharmaceutical shipments, and investments in reusable and sustainable cold chain systems have reinforced North America’s market leadership.

U.S. Cold Chain Packaging Market Trends

The cold chain packaging market in the U.S. plays a dominant role, driven by its leadership in biopharmaceutical innovation, large-scale vaccine distribution, and strong demand for temperature-sensitive specialty drugs. The country has one of the most advanced cold chain logistics ecosystems, supported by stringent FDA and GMP compliance requirements that push adoption of validated, high-performance packaging solutions. In addition, the rapid growth of direct-to-patient pharmaceutical delivery, meal-kit services, and online grocery platforms is accelerating demand for insulated shippers, smart monitoring technologies, and sustainable cold chain packaging systems across the U.S.

Asia Pacific Cold Chain Packaging Market Trends

The cold chain packaging market in the Asia Pacific is projected to expand at the fastest CAGR of 15.0% over the forecast period, driven by surging demand for temperature-sensitive pharmaceuticals, biologics, and perishable foods across rapidly developing economies. Expansion of modern cold storage infrastructure, rising e-commerce grocery deliveries, and increasing exports of frozen and chilled products are accelerating the adoption of advanced cold chain packaging solutions, particularly in the pharmaceuticals cold chain logistics market. In addition, governments’ focus on food safety, regulatory compliance, and sustainable logistics is further propelling growth in insulated containers, vacuum insulated panels, and smart monitoring packaging systems throughout the region.

China cold chain packaging market is a major growth hub in the Asia Pacific market, driven by its booming pharmaceutical manufacturing sector, increasing vaccine production, and rising demand for biologics and specialty drugs. The country’s expanding middle-class consumption of fresh seafood, meat, dairy, and frozen foods is fueling investment in modern cold chain logistics and high-performance packaging solutions. Government initiatives to improve food safety, build cold storage infrastructure, and support e-commerce grocery and direct-to-consumer delivery models are further accelerating the adoption of insulated containers, vacuum insulated panels, and sustainable packaging materials across China.

Europe Cold Chain Packaging Market Trends

The cold chain packaging market in Europe is a key market, characterized by stringent regulatory standards (EU GDP, EMA guidelines) and a strong focus on sustainability and circular economy practices. The region is witnessing significant adoption of reusable cold chain packaging, driven by pharmaceutical and food logistics companies aiming to reduce environmental impact, lower total lifecycle costs, and comply with strict waste reduction policies. Advanced modular systems, insulated containers, and smart monitoring technologies are increasingly deployed across Europe, enabling multiple-use cycles while maintaining precise temperature control and regulatory compliance.

Key Cold Chain Packaging Company Insights

The competitive environment of the market is highly dynamic and moderately concentrated, driven by both established global players and innovative regional specialists. Key companies, such as ThermoSafe, Cold Chain Technologies, Pelican BioThermal, Dawsongroup, and CSafe, compete on the basis of thermal performance, regulatory compliance, sustainability, and smart monitoring capabilities. Innovation in reusable packaging, vacuum insulated panels, and modular systems is a key differentiator, while strategic collaborations with pharmaceutical manufacturers, food distributors, and logistics providers enhance market reach. Price competitiveness, rapid response to temperature-sensitive shipment demands, and investments in R&D for advanced materials and real-time tracking solutions further intensify market rivalry.

Key Cold Chain Packaging Companies:

The following key companies have been profiled for this study on the cold chain packaging market.

- Cold Chain Technologies

- Cryopak

- Thermosafe

- Dawsongroup

- SOFRIGAM

- CSafe

- Peli BioThermal LLC

- Sealed Air

- CoolPac

- Nordic Cold Chain Solutions

- Inmark Global Holdings, LLC

- Envirotainer

- DGP Intelsius LLC

- TemperPack

- Polar Tech Industries

Recent Developments

-

In January 2026, Hydropac launched its upgraded HydroFreeze water-based ice packs for pharmaceuticals and temperature-sensitive shipments, offering 50% faster freezing and 110% longer thaw protection than previous versions, while outperforming many gel-based alternatives in slow thawing to reduce product spoilage risks.

-

In December 2025, Veritiv launched TempSafe PalletShield, the biopharmaceutical cold-chain industry’s first pre-qualified pallet shipper made from curbside-recyclable materials, providing over five days of validated thermal protection for high-volume payloads while reducing waste and disposal costs compared to traditional EPS and PUR systems.

Cold Chain Packaging Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 33.7 billion

Estimated Market size in 2026

USD 38.3 billion

Projected Market size by 2033

USD 93.1 billion

Growth rate

CAGR of 13.5% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Material, product, end use, region

Regional Scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; France; UK; Italy; Spain; China; India; Japan; South Korea; Australia; Brazil; Argentina; Saudi Arabia; UAE; South Africa

Key companies profiled

Cold Chain Technologies; Cryopak; Thermosafe; Dawsongroup; SOFRIGAM; CSafe; Peli BioThermal LLC; Sealed Air; CoolPac; Nordic Cold Chain Solutions; Inmark Global Holdings, LLC; Envirotainer; DGP Intelsius LLC; TemperPack; Polar Tech Industries

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail of customized purchase options to meet your exact research needs. Explore purchase options

Global Cold Chain Packaging Market Report Segmentation

This report forecasts revenue growth at the regional and country levels and provides an analysis of the latest industry trends and opportunities in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global cold chain packaging market report based on material, product, end use, and region:

-

Material Outlook (Revenue, USD Million, 2021 - 2033)

-

Expanded Polystyrene (EPS)

-

Polyurethane Rigid Foam (PUR)

-

Paper & Paperboard

-

Others

-

-

Product Outlook (Revenue, USD Million, 2021 - 2033)

-

Insulated Containers

-

Insulated Pallet Shippers

-

Vacuum Insulated Panels

-

Gel Packs

-

Others

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Fish, Meat & Seafood

-

Dairy Products

-

Processed Food

-

Others

-

Pharmaceuticals

-

Fruits & Vegetables

-

Bakery & Confectionaries

-

Fruit & Pulp Concentrates

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

France

-

UK

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

South Africa

-

-

Frequently Asked Questions About This Report

The global cold chain packaging market size was estimated at USD 33.7 billion in 2025 and is expected to reach USD 38.3 billion in 2026.

Key factors that are driving the cold chain packaging market growth include growing emphasis on regulatory compliance of pharmaceutical products and increased demand for frozen food products.

North America dominated the cold chain packaging market with a share over 32.0% in 2025. This is attributable to the growing demand for processed and frozen foods as a result of the growing population, as well as the changing lifestyles of people in the region.

Some key players operating in the cold chain packaging market include Cold Chain Technologies; Cryopak; Thermosafe; Dawsongroup; SOFRIGAM; CSafe; Peli BioThermal LLC; Sealed Air; CoolPac; Nordic Cold Chain Solutions; Inmark Global Holdings, LLC; Envirotainer; DGP Intelsius LLC; TemperPack; and Polar Tech Industries.

Asia Pacific is the fastest-growing region over the forecast period, with a projected CAGR of 15.0%.

The insulated containers segment held the largest revenue share of over 41.0% in 2025, while vacuum insulated panels (VIPs) is the fastest-growing segment.

Fish, meat & seafood segment dominated with over 19.0% of total market share in 2025, while pharmaceuticals is the fastest-growing end use segment.

The global cold chain packaging market is expected to grow at a compound annual growth rate of 13.5% from 2026 to 2033 to reach USD 93.1 billion by 2033.

About the Author(s)

Plastics, Polymers & Resins Research Team

Bulk Chemicals · Plastics, Polymers & ResinsThis report was authored by the plastics, polymers & resins research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the plastics, polymers & resins segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.