- Home

- »

- Electronic & Electrical

- »

-

Connected TV Market Size And Share Report, 2026 - 2033GVR Report cover

![Connected TV Market Size, Share & Trends Report]()

Connected TV Market (2026 - 2033) Size, Share & Trends Analysis Report By Screen Size (Less Than 30 Inches, 30 To 50 Inches, 50 To 70 Inches, Above 70 Inches), By Technology (LED, OLED), By Distribution Channel (Online, Offline), By Region, And Segment Forecasts

Market Size, 2025

$290.5BMarket Estimate, 2026

$318.6BMarket Forecast, 2033

$757.6BCAGR, 2026–2033

13.2%Connected TV Market Summary

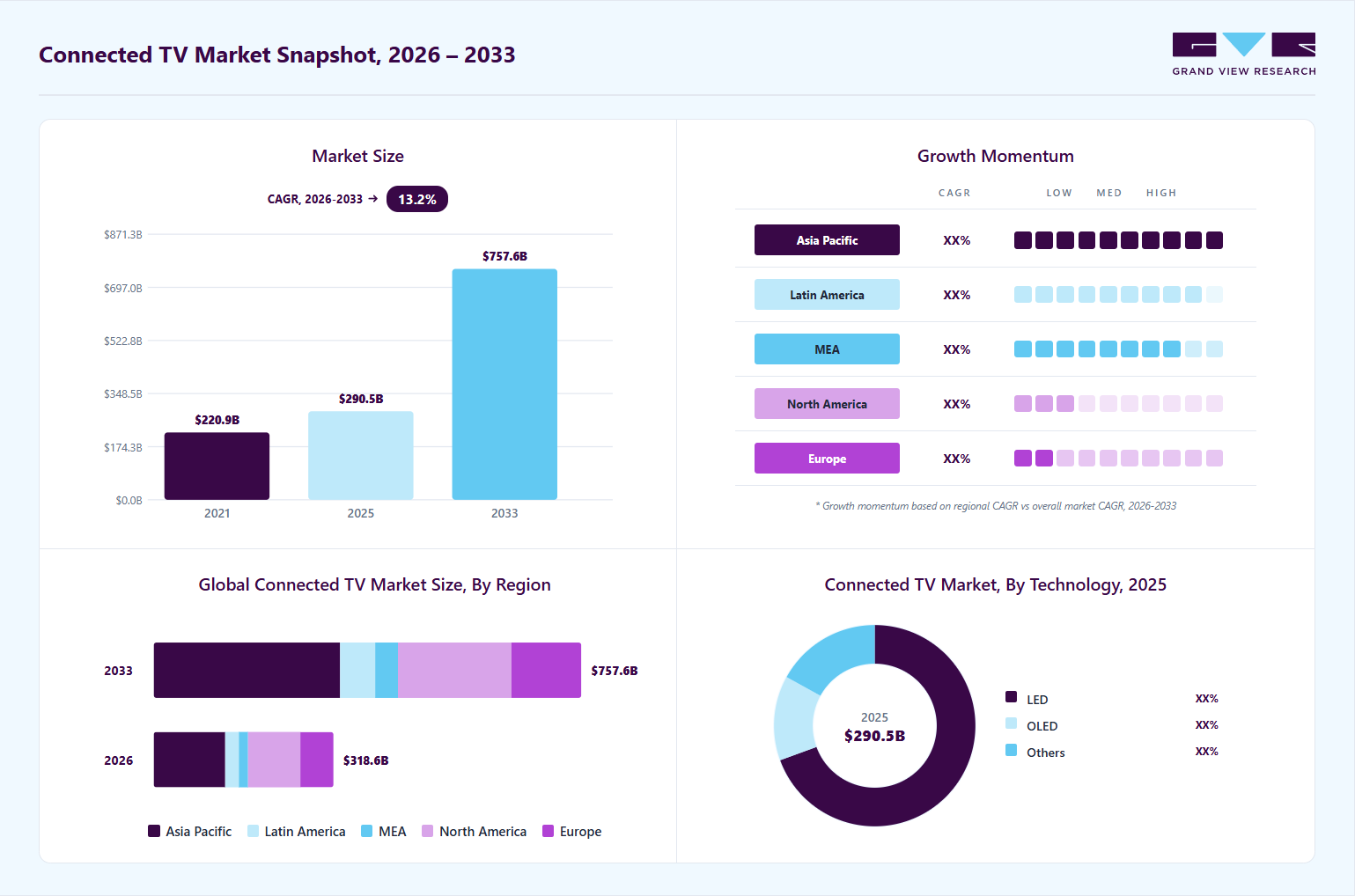

The global connected TV market size was valued at USD 290.5 billion in 2025 and is projected to grow from USD 318.6 billion in 2026 to USD 757.6 billion by 2033, at a CAGR of 13.2% from 2026 to 2033. Asia Pacific dominated the global market with the largest revenue share of 39.1% in 2025. The global connected TV industry’s growth is driven by the rapid shift in consumer viewing behavior toward streaming-first entertainment and the growing preference for seamless, internet-enabled home media experiences.

Key Market Trends & Insights

- By screen size: Screen size of 30 to 50 inches accounted for the largest revenue share of 56.7% in 2025.

- By technology: LED segment accounted for the largest revenue share of 69.4% in 2025.

- By distribution channel: Sale of connected TV through online channels led the market with the largest revenue share of 58.4% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (39.1% revenue share, 2025)

- By country: Growth of the connected TV market in Asia Pacific was led by China and India.

Market Size & Forecast

- Market size in 2025: USD 290.5 Billion

- Estimated market size in 2026: USD 318.6 Billion

- Projected market size by 2033: USD 757.6 Billion

- CAGR (2026-2033): 13.2%

Households are spending more time on subscription video platforms, live streaming, and app-based content, which is accelerating demand for televisions that integrate built-in connectivity, smart operating systems, and access to diverse digital services. Consumers are upgrading from traditional broadcast-focused sets to connected TVs that support on-demand libraries, personalized recommendations, and multi-device content sharing, making connected TV one of the most dynamic categories within the broader consumer electronics landscape. Purchase decisions in the connected TV (CTV) market are increasingly shaped by performance expectations and long-term digital usability rather than screen size alone. Buyers now evaluate factors such as streaming speed, app ecosystem compatibility, voice control integration, and software update reliability when selecting products.")

Premium connected TVs are gaining traction due to advancements in OLED and QLED display technology, higher refresh rates, AI-based picture optimization, and immersive audio features that enhance home viewing quality. Consumers also expect smooth interface navigation, low-latency casting, and consistent platform support across major streaming providers, positioning operating systems and user experience as key differentiators.

At the same time, affordability and tiered product segmentation continue to influence adoption across emerging and developed markets. Mid-range models are expanding rapidly as brands offer feature-rich connected TVs with 4K resolution, integrated voice assistants, and gaming-ready specifications at accessible price points. Demand is also rising for compact connected TVs suited to secondary rooms and urban apartments, reinforcing category diversification beyond flagship living-room screens. Manufacturers are competing through differentiated smart ecosystems, content partnerships, and frequent technology refresh cycles that sustain replacement demand.

Retail and distribution dynamics are evolving quickly as connected TV purchases become increasingly influenced by digital discovery and online comparison behavior. Consumers rely heavily on streaming performance reviews, display benchmarking content, and influencer-led setup demonstrations before committing to higher-ticket purchases. Direct-to-consumer channels, e-commerce platforms, and bundled subscription offers are increasingly driving conversions, while brands are strengthening post-sale engagement through software upgrades, integrated content services, and smart-home compatibility. As entertainment consumption becomes more connected, personalized, and platform-driven, connected TVs are emerging as a central gateway device within the modern digital household.

Market Dynamics

The expansion of Free Ad-Supported Streaming Television (FAST) platforms is emerging as a major driver of growth in the global connected TV market, as consumers increasingly shift toward cost-effective streaming options with free access to premium content. According to Nielsen’s 2024 The Gauge Report, streaming accounted for more than 47% of total TV viewing time in the U.S. in 2024, with FAST services such as Peacock, Tubi, and Roku Channel recording strong audience growth. The growing popularity of ad-supported streaming ecosystems is accelerating demand for smart TVs with integrated streaming platforms, advanced advertising capabilities, and seamless internet connectivity.

Growing consumer concerns about data privacy and connected TV tracking are emerging as a significant restraint for the global connected TV market, particularly as smart TVs increasingly collect viewing behavior, voice interactions, and device usage data for targeted advertising. According to a Pew Research Center Data Privacy Survey in 2023, nearly 72% of consumers believe companies collect too much personal data, while 78% expressed low confidence in how businesses use their information. Additionally, increasing regulatory scrutiny through frameworks such as the EU’s GDPR and evolving U.S. state privacy laws is creating compliance challenges for connected TV manufacturers, streaming platforms, and advertisers operating within data-driven smart TV ecosystems.

Consumer Insights

Households are increasingly purchasing connected TVs not simply as screens, but as central entertainment gateways that provide direct access to subscription platforms, ad-supported streaming services, and live digital sports content. Demand is driven by consumers who want seamless integration with major apps such as Netflix, Prime Video, Disney+, YouTube, and regional OTT platforms, without relying on external streaming sticks or set-top boxes. Younger buyers, especially those aged 18-35, are strongly influencing this shift, favoring connected TVs with built-in smart operating systems such as Google TV, Roku TV, Fire TV, and Samsung Tizen that enable personalized content recommendations, faster navigation, and multi-device casting across the home ecosystem.

Consumers frequently report dissatisfaction with lagging interfaces, limited app availability, inconsistent firmware updates, or smart features that degrade over time, making operating system support and processing speed critical purchase factors. Manufacturers are responding with more powerful chipsets, AI-based upscaling engines, voice-enabled controls, and deeper integration with smart assistants like Alexa and Google Assistant. At the premium end, technological competition is intensifying through OLED, Mini-LED, and QLED displays that offer superior contrast, high brightness, and cinema-grade picture performance, alongside gaming-ready specifications such as HDMI 2.1, variable refresh rates, and low-latency modes that appeal to console and cloud-gaming users.

Entry-level consumers typically purchase affordable 4K smart TVs designed around core streaming functionality, while higher-income households increasingly invest in large-format OLED flagships, immersive Dolby Atmos audio support, and design-forward lifestyle TVs positioned as premium living-room centerpieces. Retail and distribution dynamics are also evolving rapidly, with brands competing through online-exclusive models, bundled streaming subscriptions, extended warranty offers, and direct-to-consumer smart TV launches that reduce reliance on traditional electronics chains. As content ecosystems expand and personalized streaming becomes the dominant mode of entertainment, connected TVs are emerging as one of the most strategically important devices in the global digital home, combining display innovation with platform-led user experience.

Screen Size Insights

The 30 to 50 inches screen size segment led the connected TV industry, accounting for the largest revenue share of 56.7% in 2025, supported by its position as the most commonly purchased screen size worldwide. This category remains highly attractive because it matches the needs of mainstream households, delivering an immersive streaming experience while fitting comfortably into bedrooms, apartments, and mid-sized living areas. Growth is being reinforced by the increasing shift toward smart TVs as the default home entertainment device, with consumers expecting built-in access to major streaming platforms, voice control, and upgraded display features. The continued rollout of affordable 4K and HDR-enabled models in this size band is further strengthening adoption, as buyers seek sharp picture quality and connected functionality without moving into the higher price tiers of large-format screens.

Connected TVs above 70 inches are anticipated to grow at the fastest CAGR of 13.8% from 2026 to 2033. Demand is rising among consumers who prioritize theater-like experiences at home, particularly for premium streaming content, live sports, and immersive gaming. This segment is benefiting from increased affordability of ultra-large screens, alongside strong innovation in Mini-LED backlighting, OLED contrast performance, and AI-enhanced upscaling that improves picture quality at scale. Manufacturers are also positioning these models as flagship products through integrated surround sound technologies, voice-led smart platforms, and design-forward slim profiles, making above-70-inch connected TVs one of the most dynamic growth areas in the global market.

Technology Insights

LED connected TV led the connected TV market, accounting for the largest revenue share of 69.4% in 2025. LED-based models remain the most widely adopted display technology because they offer an effective balance of picture quality, energy efficiency, and affordability across mainstream consumer segments. These TVs are available across a broad range of screen sizes and price tiers, making them accessible to both first-time buyers and replacement buyers. LED connected TVs also benefit from strong performance improvements, such as 4K resolution, HDR support, and integrated smart operating systems that provide seamless access to streaming platforms.

The OLED connected TV market segment is projected to grow at the fastest CAGR of 15.1% from 2026 to 2033, driven by rising consumer demand for premium viewing experiences and next-generation display performance. Consumers increasingly prefer OLED models for their ability to deliver perfect blacks, superior contrast, and vibrant color accuracy, making them especially attractive for high-end streaming, cinematic content, and immersive gaming. Features such as ultra-thin panel design, wide viewing angles, AI-enhanced picture processing, and support for Dolby Vision and high refresh rates are highly valued in this segment. Premium brands such as LG, Sony, and Samsung are strengthening demand through flagship OLED lineups that combine cutting-edge display technology with advanced smart TV platforms and luxury home entertainment positioning.

Distribution Channel Insights

The sale of connected TV through online channels led the market with the largest revenue share of 58.4% in 2025. Buyers increasingly rely on e-commerce platforms to explore a wider range of brands, compare specifications, and evaluate performance through expert reviews, user ratings, and video-based display demonstrations. Online channels are especially attractive for connected TVs due to frequent price promotions, exclusive model availability, and bundled offers that include streaming subscriptions or extended warranties. Convenience factors such as home delivery, installation support, easy return policies, and flexible financing options are further accelerating online adoption, particularly among younger households and value-conscious buyers seeking feature-rich smart TVs at competitive prices.

Offline sales of connected TV are projected to grow at the substantial CAGR of 13.3% from 2026 to 2033. Physical retail continues to play a major role in connected TV purchasing, as consumers prefer to view screen clarity, compare display technologies, and assess size suitability in person before making a high-value investment. Electronics stores and large-format retailers support this demand through live product demonstrations, side-by-side brand comparisons, and expert staff guidance across LED, QLED, and OLED model ranges. Immediate availability, installation support, and bundled warranty services further strengthen the preference for the offline channel, making in-store purchasing the dominant route for connected TV sales globally.

Regional Insights

Asia Pacific Connected TV Market Trends

The Asia Pacific connected TV industry is expected to grow at a CAGR of 14.7% from 2026 to 2033. Growth is being led by China and India, where households are increasingly purchasing connected TVs as the primary gateway to OTT platforms such as iQIYI, Tencent Video, Hotstar, and Netflix, alongside YouTube-driven content consumption. Strong demand is also visible in Japan and South Korea, where premium upgrades toward OLED and gaming-optimized models are accelerating replacement cycles. Across Southeast Asia, affordability remains a key driver, with Xiaomi, TCL, Hisense, and Samsung expanding mid-priced 4K smart TV portfolios through aggressive online distribution.

The connected TV market in China led Asia Pacific in 2025, spurred by the country’s massive installed base of smart TVs and the rapid expansion of OTT platforms such as Tencent Video, iQIYI, and Youku. China also accounted for the highest connected TV advertising spend in the region, driven by large-scale adoption of programmatic advertising and integration of e-commerce features within streaming ecosystems.

North America Connected TV Market Trends

The North America connected TV (CTV) industry accounted for a revenue share of 29.5% in 2025. Households in the region place significant emphasis on advanced viewing performance, platform reliability, and seamless access to major OTT services, driving steady replacement and upgrade cycles across both mid-range LED and premium OLED models. The market also benefits from high disposable incomes, strong adoption of large-screen formats, and widespread integration of voice assistants and smart-home connectivity within TV platforms. A mature retail environment, spanning big-box electronics chains, brand-owned stores, and highly developed e-commerce channels, continues to reinforce North America’s position as one of the most commercially significant markets for connected TVs globally.

U.S. Connected TV Market Trends

The U.S. connected TV industry is expected to grow at a CAGR of 11.4% from 2026 to 2033. Consumers in the U.S. are upgrading connected TVs primarily for seamless access to services such as Netflix, YouTube TV, Prime Video, and live sports streaming, making smart platform performance a key purchase driver. Demand is especially strong for Google TV, Roku TV, and Fire TV-powered models, which dominate household adoption due to their broad app ecosystems and intuitive interfaces. The market is also being shaped by high penetration of large-screen purchases, where buyers increasingly invest in OLED and Mini-LED displays for cinematic viewing and gaming-ready specifications such as HDMI 2.1 and high refresh rates.

Europe Connected TV Market Trends

The connected TV industry in Europe is expected to grow at a CAGR of 11.3% from 2026 to 2033. Households across Western and Northern Europe place high importance on picture quality, energy efficiency, and reliable access to major OTT services such as Netflix, Prime Video, Disney+, and local broadcaster streaming apps. Replacement cycles are being driven by upgrades to 4K HDR, OLED, and Mini-LED models, particularly in markets such as Germany, the UK, France, and the Nordics. The market also benefits from increasing adoption of voice-enabled interfaces, multi-room smart-home connectivity, and gaming-oriented features that enhance the connected viewing experience.

The connected TV market in Germany led Europe in 2025. According to PwC Germany Entertainment & Media Outlook, Germany’s television and TV advertising market generated €10.5 billion (USD 10.9 billion) in revenue in 2024, making it the largest TV market in Europe and the fifth-largest globally. The country’s strong connected TV growth is supported by high smart TV penetration, increasing consumption of ad-supported streaming platforms, and expanding broadcaster video-on-demand services, positioning Germany as a key hub for CTV advertising and digital video innovation in Europe.

The UK connected TV market is projected to grow lucratively from 2026 to 2033. According to the IAB UK Digital Adspend Report 2024, connected TV and broadcaster video-on-demand (BVOD) advertising were among the fastest-growing digital video segments in the country, supported by widespread smart TV adoption and increasing streaming consumption. The UK’s advanced streaming ecosystem, high household internet penetration, and strong demand for ad-supported video platforms have positioned the country as a major hub for connected TV advertising growth across Europe.

Central and South America Connected TV Market Trends

The connected TV industry in Central and South America is expected to grow at a CAGR of 14.2% from 2026 to 2033, driven by the rapid shift from traditional broadcast consumption to OTT-first viewing, with users increasingly relying on app-based ecosystems rather than linear TV schedules. This is further reinforced by strong integration between smart TV operating systems and regional streaming platforms, enabling seamless content discovery, localized recommendations, and bundled subscription models. In addition, aggressive pricing of entry-level smart TVs tailored for mass-market households is accelerating the replacement of legacy television sets with connected devices across both urban and semi-urban regions.

Middle East and Africa Connected TV Market Trends

The connected TV industry in Middle East and Africa is expected to grow at a CAGR of 13.8% from 2026 to 2033. Consumers in the region are increasingly shifting toward OTT-first and mobile-cast viewing habits, where entertainment consumption is driven by app-based streaming ecosystems rather than traditional satellite or cable television. This behavior is being reinforced by the rapid localization of content libraries, with regional Arabic, Turkish, and African productions gaining prominence on major streaming platforms, improving engagement and retention. In addition, the rising availability of affordable smart TVs bundled with pre-installed streaming applications is accelerating the replacement of legacy TV systems, particularly in urban households across GCC countries and key African metropolitan markets.

Key Connected TV Company Insights

The connected TV market is highly competitive, characterized by the presence of major global streaming platforms, smart TV manufacturers, ad-tech providers, and regional broadcasters. Key players are differentiating themselves through advanced programmatic advertising capabilities, exclusive content partnerships, AI-driven audience targeting, and integrated ad-supported streaming services, while broadcasters and OTT platforms continue expanding connected TV inventories to enhance viewer engagement and monetization opportunities.

-

Samsung Electronics is a global leader in the connected TV market, leveraging its extensive smart TV portfolio, proprietary Tizen operating system, and strong global distribution network to maintain a dominant industry position. In 2025, the company continued expanding its connected TV ecosystem through AI-powered smart TVs, integrated streaming services, and advanced advertising solutions via Samsung Ads. Samsung’s visual display business recorded steady growth driven by rising demand for premium OLED and large-screen connected TVs.

-

LG Electronics is recognized for its premium connected TV offerings and advanced OLED display technologies. The company focuses on enhancing user experience through its webOS smart TV platform, personalized content discovery, and strategic partnerships with global OTT and streaming providers. In 2025, LG strengthened its position in the connected TV industry through increased adoption of OLED and UHD smart TVs, while expanding its ad-supported smart TV ecosystem and connected TV advertising capabilities globally.

Key Connected TV Companies

The following key companies have been profiled for this study on the connected TV market.

-

Samsung Electronics

-

LG Electronics

-

Sony Corporation

-

Panasonic Corporation

-

Philips

-

TCL Technology

-

Xiaomi Corporation

-

Hisense Group

-

Sharp Electronics

-

Roku

-

Skyworth

-

Haier Group

Recent Developments

-

In March 2025, Former executives from Xiaomi and Flipkart launched Lumio, a new brand aiming to disrupt India’s highly competitive smart TV market. The company is positioning itself as a consumer-focused challenger, emphasizing better performance, a cleaner software experience, and stronger value in the mid-range connected TV segment. Lumio plans to leverage the founders’ deep expertise in India’s electronics and e-commerce ecosystems to build differentiated smart TV offerings that address common consumer pain points around speed, usability, and content-driven viewing.

-

In March 2025, Samsung launched its 2025 Neo QLED TV lineup in the U.S., highlighting major upgrades driven by its new Samsung Vision AI technology. The new models are designed to deliver more personalized and intelligent viewing through features such as real-time picture and sound optimization, enhanced upscaling for sharper content, and smarter interaction capabilities. Samsung is positioning Vision AI as a key step toward making TVs more adaptive home entertainment hubs, combining premium Mini-LED display performance with AI-powered enhancements that improve both everyday streaming and high-end cinematic experiences.

-

In April 2024, Sony Corporation launched its new BRAVIA connected TV lineup, including the BRAVIA 9, BRAVIA 8, BRAVIA 7, and BRAVIA 3 models featuring Google TV integration, Mini-LED and OLED display technologies, AI-powered picture optimization, and immersive cinematic audio capabilities. The launch strengthened Sony’s position in the connected TV market by enhancing streaming experiences and integrating advanced smart home and content ecosystem features across its premium smart TV portfolio.

Connected TV Market Report Scope

Report Attribute

Details

Market size in 2025

USD 290.5 billion

Estimated Market size in 2026

USD 318.6 billion

Projected Market size by 2033

USD 757.6 billion

Growth rate

CAGR of 13.2% from 2026 to 2033

Actuals

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Screen size, technology, distribution channel, region

Regional scope

North America; Europe; Asia Pacific; Central & South America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; China; Japan; India; Australia & New Zealand; South Korea; Brazil; UAE

Key companies profiled

Samsung Electronics; LG Electronics; Sony Corporation; Panasonic Corporation; Philips; TCL Technology; Xiaomi Corporation; Hisense Group; Sharp Electronics; Roku; Skyworth; Haier Group

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options Global Connected TV Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends and opportunities in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global connected TV market report based on screen size, technology, distribution channel, and region:

-

Screen Size Outlook (Revenue, USD Billion, 2021 - 2033)

-

Less than 30 inches

-

30 to 50 inches

-

50 to 70 inches

-

Above 70 inches

-

-

Technology Outlook (Revenue, USD Billion, 2021 - 2033)

-

LED

-

OLED

-

Others

-

-

Distribution Channel Outlook (Revenue, USD Billion, 2021 - 2033)

-

Online

-

Offline

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

Japan

-

India

-

Australia & New Zealand

-

South Korea

-

-

Central & South America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Connected TV Advertising & Viewer Monetization Analysis

Developed a tailored assessment of the connected TV advertising ecosystem, including analysis of FAST platform expansion, programmatic ad adoption, viewer engagement metrics, AVOD monetization models, and advertiser spending patterns across key regional markets. The study also evaluated audience targeting capabilities, ad inventory growth, and evolving measurement frameworks influenced by privacy regulations and effectiveness.

Enables stakeholders to understand evolving connected TV monetization strategies, identify high-growth advertising formats and revenue pools, assess competitive positioning within ad-supported streaming ecosystems, and optimize investment decisions across digital video and programmatic advertising channels.

Smart TV Operating System & Ecosystem Competitiveness Assessment

Delivered a customized evaluation of smart TV operating system dynamics, including platforms such as Tizen, webOS, Google TV, Roku OS, and Fire TV across app ecosystem strength, interface performance, content partnerships, software update cycles, and smart-home integration capabilities. The analysis further assessed platform stickiness, cross-device interoperability, and ecosystem expansion strategies adopted by major manufacturers.

Provides actionable insights into platform competitiveness, ecosystem differentiation, and long-term software sustainability, helping clients identify strategic technology partnerships, evaluate operating system adoption trends, and align product development initiatives with evolving connected entertainment preferences.

Connected TV Consumer Usage & Multi-Screen Behavior Study

Conducted a focused assessment of connected TV consumption behavior, including streaming duration trends, second-screen engagement, gaming usage patterns, content discovery preferences, and household-level device interaction across demographics and income groups. The study also analyzed binge-viewing trends, subscription stacking behavior, and user migration from traditional pay-TV services toward connected streaming ecosystems.

Supports strategic planning for streaming providers, smart TV manufacturers, and advertisers by quantifying evolving consumer engagement patterns, identifying emerging content consumption behaviors, evaluating opportunities in multi-screen advertising environments, and strengthening audience retention and platform optimization strategies.

Frequently Asked Questions About This Report

The global connected TV market was valued at USD 290.5 billion in 2025 and is expected to reach USD 318.6 billion in 2026.

The global connected TV market is expected to grow at a CAGR of 13.2% from 2026 to 2033 to reach USD 757.6 billion by 2033.

Asia Pacific dominated with a 39.1% revenue share in 2025.

Some of the key players operating in the market include Samsung Electronics; LG Electronics; Sony Corporation; Panasonic Corporation; Philips; TCL Technology; Xiaomi Corporation; Hisense Group; Sharp Electronics; Roku; Skyworth; Haier Group

Key factors include the rapid shift in consumer viewing behavior toward streaming-first entertainment and the growing preference for seamless, internet-enabled home media experiences.

The 30 to 50 inches screen size segment held the highest market share of 56.7% in 2025, while connected TVs above 70 inches is the fastest-growing segment.

The LED connected TV led the connected TV segment held the highest market share of 69.4%% in 2025, while OLED connected TV is the fastest-growing segment.

The sale of connected TV through online channels segment led with a 58.4% revenue share in 2025, while offline sales of connected TV is the fastest-growing segment.

About the Author(s)

Electronic & Electrical Research Team

Consumer Goods · Electronic & ElectricalThis report was authored by the electronic & electrical research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the electronic & electrical segment of the consumer goods industry. All findings are based on proprietary consumer goods databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.