- Home

- »

- Next Generation Technologies

- »

-

Smart TV Market Size, Share & Growth Report, 2026-2033GVR Report cover

![Smart TV Market (2026 - 2033)Report]()

Smart TV Market (2026 - 2033)

Size, Share & Trends Analysis Report By Resolution (4K UHD TV, HDTV, Full HD TV, 8K TV), By Screen Size, By Operating System (Android TV, Tizen, WebOS, Roku, Other), By Distribution Channel, By Technology, By Region, And Segment Forecasts

Market Size, 2025

$247.0BMarket Estimate, 2026

$270.8BMarket Forecast, 2033

$673.5BCAGR, 2026–2033

13.9%Smart TV Market Summary

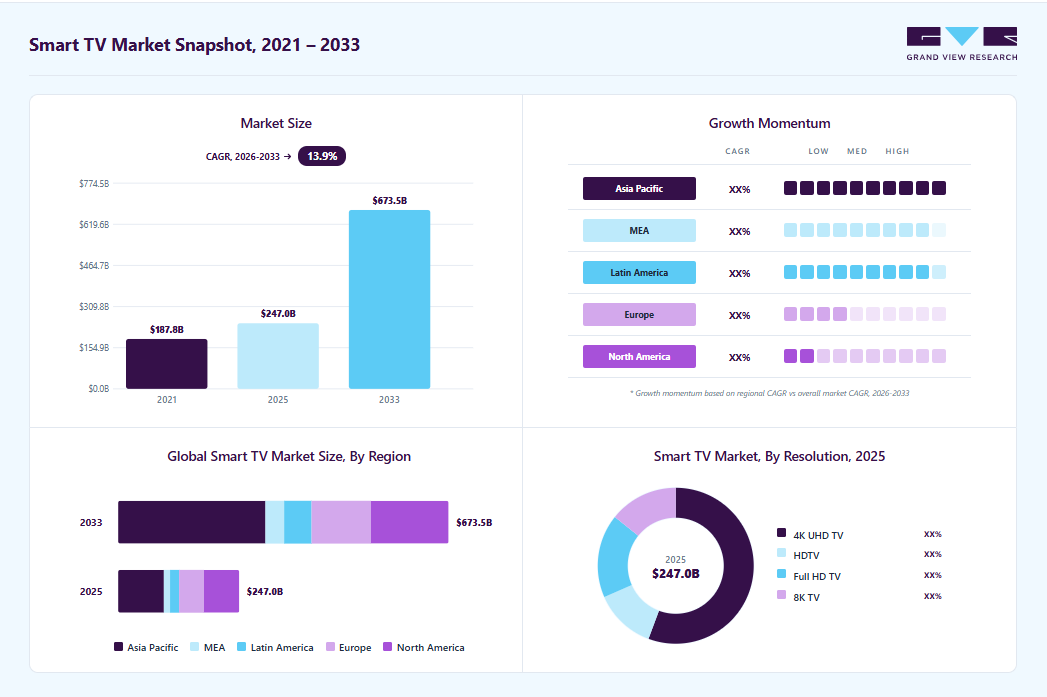

The global smart TV market size was valued at USD 247.0 billion in 2025 and is projected to grow from USD 270.8 billion in 2026 to USD 673.5 billion by 2033, at a CAGR of 13.9% from 2026 to 2033. The market in Asia Pacific dominated with a revenue share of 40.0% in 2025. The market growth is driven by the increasing penetration of high-speed internet and OTT streaming platforms, rising consumer demand for immersive entertainment, and growing preference for connected home ecosystems.

Key Market Trends & Insights

- By distribution channel: Online segment held the largest market share of 58.0% in 2025.

- By resolution: 4k ultra high definition (UHD) segment held the largest market share of 56.0% in 2025.

- By technology: LED segment held the largest market share of 50.0% in 2025.

- By operating system: Android TV segment held the largest market share of 43.0% in 2025.

- By screen size: 46 to 55-inch segment held the largest market share of 36.0% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (40.0% revenue share, 2025)

- By country: China held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 247.0 Billion

- Estimated market size in 2026: USD 270.8 Billion

- Projected market size by 2033: USD 673.5 Billion

- CAGR (2026-2033): 13.9%

Technological advancements in display, AI-powered content recommendation, and voice-enabled assistants enable personalized viewing and enhanced user experience, further accelerating the smart TV industry growth. The increasing integration of streaming services, internet connectivity, and entertainment features is significantly driving smart TV market growth. Smart TVs combine access to OTT platforms, gaming, and social media within a single device, enabling seamless content consumption and enhanced user convenience. Advancements in high-definition display technologies, such as 4K and 8K resolutions, are further improving viewing quality and stimulating consumer demand. Expanding internet penetration across developing regions, coupled with declining manufacturing costs and improved affordability, is encouraging widespread adoption globally, thereby accelerating smart TV industry expansion.")

In addition, growth opportunities in the smart TV market are expanding rapidly across emerging economies where rising internet penetration and accelerating digital adoption are reshaping consumer entertainment habits. Increasing demand for on-demand streaming content is encouraging manufacturers to introduce affordable, feature-rich Smart TVs tailored for price-sensitive consumers. The growing popularity of cloud gaming services is further broadening the market, as smart TVs evolve into versatile platforms catering to a global gaming audience, thereby driving sustained market growth.

Furthermore, manufacturers are intensifying investments in research and development to strengthen their competitive positioning amid rising demand for interactive and immersive home entertainment solutions. Leading brands are collaborating with major streaming platforms to offer exclusive content access and optimized user interfaces directly through smart TVs. By expanding product portfolios across multiple price segments and prioritizing innovation in screen and display technologies, vendors are targeting both premium and budget-conscious consumers. The expansion of distribution networks and increased reliance on e-commerce channels are enhancing product accessibility in the smart TV industry.

Moreover, continuous technological innovation is redefining the smart TV industry, with advancements such as HDR, Quantum Dot, and OLED technologies significantly improving picture quality, color accuracy, and viewing realism. The integration of AI-driven features enables voice-based control, intelligent content recommendations, and personalized viewing experiences, enhancing user engagement. These innovations are reinforcing the role of smart TVs as essential components of the modern digital ecosystem, accelerating overall market expansion.

Operating System Insights

The Android TVs segment accounted for the largest market share of over 43% in 2025, driven by the open ecosystem, compatibility with various applications, and user-friendly interface. Android TV’s access to the Google Play Store enables users to download a wide range of apps, games, and streaming services, adding to its appeal. The interface’s familiarity also makes it an attractive choice for users already accustomed to Android devices. Android TVs have gained traction across multiple price points, providing consumers with flexibility and convenience. These factors drive the growth of the Android TVs segment in the market.

The Roku segment is expected to register the fastest CAGR of 14.4% from 2026 to 2033. The growth is driven by Roku’s focus on delivering a simplified, user-friendly interface that enhances accessibility for a wide consumer base. Its broad compatibility with leading streaming platforms, combined with an intuitive remote and platform design, supports seamless content consumption for non-tech-savvy users. Roku’s affordable ecosystem and strategic partnerships with smart TV manufacturers are strengthening its market presence, thereby supporting sustained growth within the smart TV industry.

Resolution Insights

The 4K Ultra High Definition (UHD) segment accounted for the largest market share in 2025. The increasing demand for high-resolution displays that deliver clearer and more immersive viewing experiences is fueling market growth. Streaming platforms, gaming, and even social media videos are now frequently offered in 4K, making it an attractive choice for consumers looking for high-quality visuals. The prices of 4K UHD TVs have significantly improved affordability, enabling wider consumer adoption and reinforcing the segment’s strong market penetration and sustained growth.

The full HD TVs segment is expected to register the fastest CAGR from 2026 to 2033, owing to the offer of a high-quality viewing experience at a more affordable price than 4K models. Full HD remains a popular choice for consumers in regions with limited internet bandwidth, where 4K streaming may not be feasible. Full HD Smart TVs provide an optimal balance of quality and price, especially for budget-conscious consumers who want smart features without necessarily needing ultra-high resolutions. This segment appeals to a diverse range of customers and remains particularly strong in emerging markets.

Screen Size Insights

The 46 to 55-inch segment accounted for the largest market share in 2025. This size range is popular among consumers looking for a large screen that fits comfortably in both small and medium-sized rooms, making it ideal for households that want an immersive viewing experience without requiring extra space. Manufacturers have responded by offering an array of options within this segment, including various resolutions and features, which has further solidified their popularity in the smart TV market.

The above 65-inch segment is expected to register a significant CAGR from 2026 to 2033, driven by the increasing demand for larger screens for enhanced viewing experiences such as theaters. These TVs are particularly popular among high-end consumers and home entertainment enthusiasts who prioritize immersive experiences. With improvements in picture quality and the increasing affordability of larger screen sizes. The rising popularity of in-home streaming, gaming, and the integration of smart home features, making the above 65-inch segment an area of considerable growth in the smart TV market.

Distribution Channel Insights

The online segment accounted for the largest market share in 2025, owing to the convenience and variety available through e-commerce platforms. Consumers are increasingly turning to online channels to compare brands, models, and prices before purchasing, which allows them to find the best deals. Online platforms also frequently offer discounts, customer reviews, and quick delivery options, enhancing the appeal of online shopping for smart TVs. This trend has been accelerated by the rise of online-exclusive brands and models, making online platforms a major sales channel in the smart TV industry.

The offline segment is expected to register significant CAGR from 2026 to 2033. This growth is fueled by offline sales channels, particularly for high-end models, including OLED, QLED, and MicroLED models. Many consumers still prefer the tactile experience of visiting a physical store, where they can see the display quality firsthand and receive guidance from sales staff. Smart TVs, which use advanced display technology for enhanced clarity and sleek design, appeal to consumers seeking premium experiences and are often showcased in-store. Offline channels remain relevant, especially for high-end purchases that benefit from in-person consultation and demonstration.

Technology Insights

The LED technology segment dominates the smart TV market in 2025, owing to its energy efficiency, brightness, and affordability. LED smart TVs offer sharp picture quality and vibrant colors, making them suitable for most viewing environments. Their long lifespan and relatively lower production costs make LED TVs accessible to a wide range of consumers. The versatility of LED technology allows for various screen sizes, which has enabled manufacturers to cater to different consumer needs, contributing to its strong market presence.

The OLED segment is expected to register the fastest CAGR from 2026 to 2033. The growth is driven by consumers seeking superior picture quality and contrast ratios. OLED technology, which offers deeper blacks and a wider color range than LED, is highly appealing for users prioritizing visual quality. This segment is particularly favored among high-end consumers, as OLED TVs deliver a cinematic experience that enhances home entertainment. As OLED technology continues to improve, it is expected to drive segmental growth in the market.

Regional Insights

North America smart TV market accounted for a share of over 29% in 2025, driven by high household penetration of broadband internet, widespread adoption of OTT streaming platforms, and strong consumer spending on premium home entertainment systems. The rapid shift away from traditional cable services toward on-demand streaming, coupled with early adoption of advanced display technologies such as 4K, OLED, and QLED, is supporting sustained market growth across residential applications in the region.

U.S. Smart TV Market Trends

The U.S. smart TV market accounted for a share of over 89% in 2025, driven by the strong presence of leading streaming platforms, high disposable income, and rapid adoption of connected home ecosystems. Consumers increasingly prefer smart TVs with integrated voice assistants, AI-based content recommendations, and gaming capabilities. The growing popularity of cloud gaming services and smart home integration is further strengthening demand across the country.

Europe Smart TV Market Trends

The Europe Smart TV market is expected to grow at a CAGR of over 12% from 2026 to 2033, owing to rising demand for energy-efficient consumer electronics and increasing penetration of digital broadcasting and OTT services. Advancements in display technologies, along with growing consumer preference for high-resolution content and immersive viewing experiences, are driving adoption. Regional emphasis on sustainability and energy labeling standards is also influencing purchasing decisions.

Smart TV market in Germany is expected to grow significantly in the coming years, driven by high consumer preference for premium electronics, advanced display quality, and energy-efficient devices. Strong broadband infrastructure and widespread use of streaming platforms support market expansion. Additionally, German consumers show strong demand for large-screen smart TVs with superior picture quality and integrated smart home connectivity.

The UK smart TV market is rapidly expanding, supported by the strong adoption of streaming services, increasing cord-cutting trends, and rising demand for smart entertainment solutions. Government-backed broadband expansion initiatives and the growing popularity of subscription-based video-on-demand platforms are accelerating smart TV adoption. Integration of voice control, personalized content discovery, and gaming features is further enhancing consumer interest.

Asia Pacific Smart TV Market Trends

The smart TV market in Asia Pacific accounted for the largest revenue share of over 40% in 2025. The Asia Pacific smart TV market is expected to grow at the fastest CAGR of over 16% from 2026 to 2033, driven by rapid urbanization, an expanding middle-class population, and rising internet penetration. Increasing affordability of Smart TVs, along with growing consumption of digital content and online streaming, is accelerating adoption. Government-led digitalization initiatives and expanding e-commerce platforms are further supporting regional growth.

Smart TV market in China is driven by strong domestic manufacturing capabilities, aggressive pricing strategies, and rapid adoption of AI-enabled and IoT-connected devices. High penetration of local streaming platforms, combined with government support for smart home ecosystems, is accelerating Smart TV adoption. Chinese brands are increasingly integrating advanced display technologies and voice-enabled features to cater to tech-savvy consumers.

The Japan smart TV market is growing steadily, driven by consumer demand for high-quality display technologies, compact yet feature-rich designs, and advanced connectivity options. Strong adoption of 4K and 8K content, along with the integration of Smart TVs into connected home environments, is supporting market growth. The country’s advanced broadband infrastructure and preference for premium electronics further reinforce demand.

Key Smart TV Company Insights

Some of the key players operating in the market include Samsung Electronics Co., Ltd., and LG Electronics Inc., among others.

-

Samsung Electronics Co., Ltd. operates across multiple business segments, including consumer electronics, IT & mobile communications, and device solutions. The company offers a comprehensive portfolio of smart TVs ranging from entry-level models to premium QLED, Neo QLED, and OLED televisions, serving residential consumers globally. Samsung integrates advanced technologies such as AI-powered upscaling, voice assistants, and smart home connectivity through its Tizen platform. The company maintains strong manufacturing, distribution, and service in the smart TV industry.

-

LG Electronics Inc. operates through business segments including home appliances & air conditioning, home entertainment, vehicle component solutions, and business solutions. LG is a leading provider of smart TVs, with a strong focus on OLED and NanoCell display technologies. The company leverages its proprietary webOS platform to deliver AI-enabled content recommendations, voice control, and seamless smart home integration. LG has established a robust global sales and service network, catering to both premium and mid-range consumer segments.

Hisense International and TCL Electronics Holdings Limited are some of the emerging market participants in the smart TV market.

-

Hisense International specializes in the development and manufacturing of consumer electronics and home appliances, with a growing focus on smart TV solutions. The company offers competitively priced smart TVs featuring ULED, Mini-LED, and 4K/8K display technologies, targeting cost-conscious and mid-range consumers. Hisense serves residential and commercial customers, and is expanding its global footprint through strategic sponsorships, partnerships, and investments in display innovation.

-

TCL Electronics Holdings Limited focuses on the design, manufacturing, and distribution of smart TVs and display solutions. The company is known for its vertically integrated operations and strong capabilities in panel manufacturing through its CSOT subsidiary. TCL offers Smart TVs powered by Android TV and Google TV platforms, integrating AI-based features, voice assistants, and IoT connectivity. The company is rapidly expanding its presence across emerging and developed markets by offering feature-rich televisions at competitive price points.

Key Smart TV Companies:

The following key companies have been profiled for this study on the smart TV market.

- Haier Inc.

- Hisense International

- Intex Technologies

- Koninklijke Philips N.V

- LG Electronics Inc

- Panasonic Corporation

- Samsung Electronics Co. Ltd

- Sansui Electric Co. Ltd

- Sony Corporation

- TCL Electronics Holdings Limited

- Toshiba Visual Solutions (TVS Regza Corporation)

Recent Development

-

In January 2026, Samsung Electronics Co., Ltd. announced its AI-driven Companion to AI Living vision at CES 2026, unveiling a new 130-inch micro RGB TV and a suite of AI-powered smart home devices designed to integrate intelligent display, personalized content interaction, and smart appliances into a seamless ecosystem. This announcement underscores Samsung’s commitment to advancing AI integration and premium large-screen viewing experiences within the smart TV industry.

-

In January 2026, LG Electronics Inc. showcased cutting-edge OLED TVs, including the flagship OLED evo G6 with a brighter panel and enhanced gaming capabilities, as well as the ultra-thin Wallpaper OLED models and the world’s first 4K 120Hz cloud gaming TVs. These product launches highlight LG’s strategic push into premium display technology and next-generation entertainment features.

-

TCL Electronics Holdings Limited unveiled its next-gen X11L SQD mini-LED TV at CES 2026, featuring advanced color technologies, high contrast performance, Dolby Vision support, and game-ready capabilities, positioning the company to compete strongly in premium large-screen segments. This launch reinforces TCL’s strategic focus on premium display innovation. It strengthens its competitive position in the high-end smart TV market, catering to rising demand for immersive home entertainment experiences.

Smart TV Market Report Scope

Report Attribute

Details

Market size in 2025

USD 247.0 billion

Estimated market size in 2026

USD 270.8 billion

Projected market size by 2033

USD 673.5 billion

Growth rate

CAGR of 13.9% from 2026 to 2033

Base Year of estimation

2025

Actual data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Volume in Thousand Units, Revenue in USD Million/Billion, and CAGR from 2026 to 2033

Report coverage

Revenue and demand forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Resolution, screen size, operating system, distribution channel, technology, and region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Austria; Belgium; Czech Republic; Denmark; Finland; France; Germany; Iceland; Ireland; Italy; Netherlands; Norway; Poland; Spain; Sweden; Switzerland; UK; Australia; China; Hong Kong; India; Indonesia; Japan; Malaysia; New Zealand; Philippines; Singapore; South Korea; Taiwan; Thailand; Vietnam; Brazil; Argentina; Chile; Saudi Arabia; UAE; South Africa; Egypt; Israel; Nigeria

Key companies profiled

Haier Inc; Intex Technologies; Koninklijke Philips N.V.; LG Electronics; Panasonic Corporation; Samsung Electronics Co. Ltd; Sansui Electric Co. Ltd; Sony Corporation; TCL Electronics Holdings Limited; Toshiba Visual Solutions; Hisense International

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope. Global Smart TV Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and analyzes the latest market trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global smart TV market report based on resolution, screen size, operating system, distribution channel, technology, and region:

-

Operating System Outlook (Volume, Thousand Units; Revenue, USD Million, 2021 - 2033)

-

Android TV

-

Tizen

-

WebOS

-

Roku

-

Other

-

-

Resolution Outlook (Volume, Thousand Units; Revenue, USD Million, 2021 - 2033)

-

4K UHD TV

-

HDTV

-

Full HD TV

-

8K TV

-

-

Screen Size Outlook (Volume, Thousand Units; Revenue, USD Million, 2021 - 2033)

-

Below 32 inches

-

32 to 45 inches

-

46 to 55 inches

-

56 to 65 inches

-

Above 65 inches

-

-

Distribution Channel Outlook (Volume, Thousand Units; Revenue, USD Million, 2021 - 2033)

-

Online

-

Offline

-

-

Technology Outlook (Volume, Thousand Units; Revenue, USD Million, 2021 - 2033)

-

OLED

-

QLED

-

LED

-

Others

-

-

Regional Outlook (Volume, Thousand Units; Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Austria

-

Belgium

-

Czech Republic

-

Denmark

-

Finland

-

France

-

Germany

-

Iceland

-

Ireland

-

Italy

-

Netherlands

-

Norway

-

Poland

-

Spain

-

Sweden

-

Switzerland

-

UK

-

-

Asia Pacific

-

Australia

-

China

-

Hong Kong

-

India

-

Indonesia

-

Japan

-

Malaysia

-

New Zealand

-

Philippines

-

Singapore

-

South Korea

-

Taiwan

-

Thailand

-

Vietnam

-

-

Latin America

-

Brazil

-

Argentina

-

Chile

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

Egypt

-

South Africa

-

Israel

-

Nigeria

-

-

Frequently Asked Questions About This Report

Asia Pacific dominated with a 40.0% revenue share in 2025.

The online segment dominated the market and accounted for the largest revenue share of 58.0% in 2025.

The LED segment led with a 50.0% revenue share in 2025, while OLED is the fastest-growing technology.

Android TVs segment held the largest share (over 43.0%) in 2025, while Roku is the fastest-growing operating system.

The global smart TV market size was valued at USD 247.0 billion in 2025 and is estimated at USD 270.8 billion for 2026.

The global smart TV market is expected to grow at a CAGR of 13.9% from 2026 to 2033, reaching USD 673.5 billion by 2033.

Key players include Haier Inc; Intex Technologies; Koninklijke Philips N.V.; LG Electronics; Panasonic Corporation; Samsung Electronics Co. Ltd; Sansui Electric Co. Ltd; Sony Corporation; TCL Electronics Holdings Limited; Toshiba Visual Solutions; Hisense International.

The smart TV market is witnessing growth is driven by the increasing penetration of high-speed internet and OTT streaming platforms, rising consumer demand for immersive entertainment, and growing preference for connected home ecosystems. Technological advancements in display, AI-powered content recommendation, and voice-enabled assistants enable personalized viewing and enhanced user experience, further accelerating the smart TV industry growth.

The 46 to 55-inch segment accounted for the largest market share of 36.0% in 2025. This size range is popular among consumers looking for a large screen that fits comfortably in both small and medium-sized rooms, making it ideal for households that want an immersive viewing experience without requiring extra space. Manufacturers have responded by offering an array of options within this segment, including various resolutions and features, which has further solidified their popularity in the smart TV market.

The 4K Ultra High Definition (UHD) segment accounted for the largest market share of 56.0% in 2025. The increasing demand for high-resolution displays that deliver clearer and more immersive viewing experiences is fueling market growth. Streaming platforms, gaming, and even social media videos are now frequently offered in 4K, making it an attractive choice for consumers looking for high-quality visuals. The prices of 4K UHD TVs have significantly improved affordability, enabling wider consumer adoption and reinforcing the segment’s strong market penetration and sustained growth.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.