- Home

- »

- Next Generation Technologies

- »

-

Connectivity Module Market Size & Share Report, 2026-2033GVR Report cover

![Connectivity Module Market (2026 - 2033)Report]()

Connectivity Module Market (2026 - 2033)

Size, Share & Trends Analysis Report By Connectivity Technology (Cellular Modules, Cellular LPWA Modules, GNSS Modules), By Product, By End Use, By Region, And Segment Forecasts

Market Size, 2025

$79.7BMarket Estimate, 2026

$87.9BMarket Forecast, 2033

$181.9BCAGR, 2026–2033

11.0%Connectivity Module Market Summary

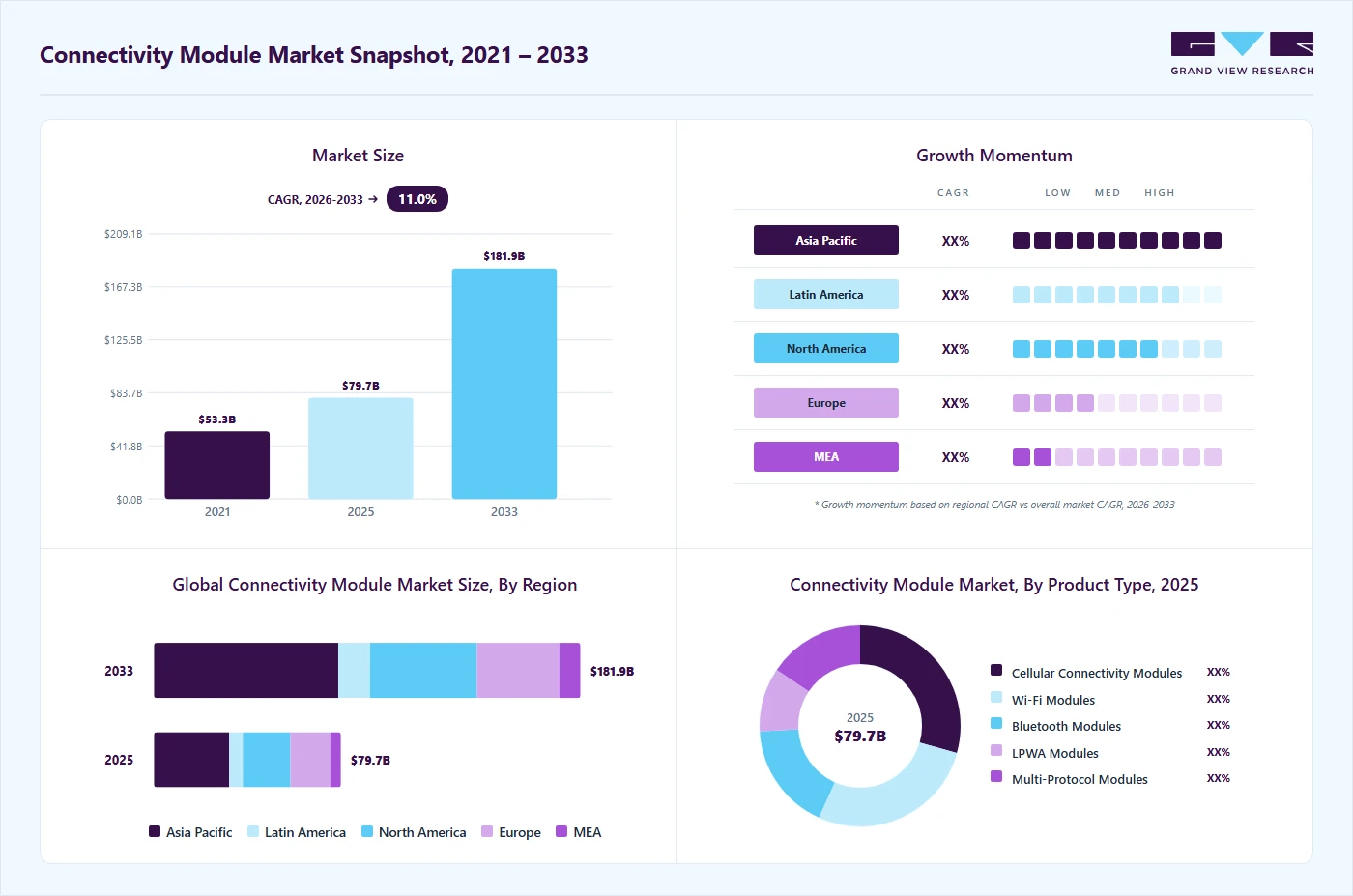

The global connectivity module market size was valued at USD 79.7 billion in 2025 and is projected to grow from USD 87.9 billion in 2026 to USD 181.9 billion by 2033, at a CAGR of 11.0% from 2026 to 2033. The market in Asia Pacific dominated with a revenue share of 40.2% in 2025. The industry is growing rapidly due to the rising demand for seamless wireless communication across devices and industrial systems.

Key Market Trends & Insights

- By connectivity technology: Short-range modules segment held the largest market share of 48.3% in 2025.

- By product: Cellular connectivity modules segment held the largest market share of 29.3% in 2025.

- By end use: Consumer electronics segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (40.2% revenue share, 2025)

- By country: China held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 79.7 Billion

- Estimated market size in 2026: USD 87.9 Billion

- Projected market size by 2033: USD 181.9 Billion

- CAGR (2026-2033): 11.0%

Key technologies driving this growth include cellular (4G/5G/LTE), Wi‑Fi, Bluetooth, and LPWAN, supporting IoT, automotive, and industrial applications. Adoption is strongest in consumer electronics, smart manufacturing, automotive telematics, and healthcare monitoring. The growing adoption of compact, energy-efficient, and versatile connectivity modules is driving the connectivity module market. Increasing demand for IoT devices across consumer, industrial, and automotive sectors is fueling this trend. Manufacturers are developing modules with multiple LTE bands, eSIM, and flexible interfaces to simplify integration. Single-SKU solutions help reduce inventory and logistics challenges, lowering operational costs.")

Faster development cycles and improved device performance are encouraging wider deployment of IoT solutions. Many companies are actively innovating and launching such advanced modules. The market is expanding rapidly due to these evolving connectivity needs. For instance, in January 2026, Fibocom Wireless Inc., a provider of IoT wireless communication modules and AI solutions in China, launched its global LTE Cat.1 bis module, the LE271-GL, offering compact, low-power, and single-SKU connectivity for worldwide IoT applications. The module supports global LTE bands, multiple interfaces, eSIM, and low-power modes, enabling fast and stable connections, as well as flexible secondary development for diverse IoT deployments.

The connectivity module market is seeing a trend toward ready-to-integrate, pre-certified, and energy-efficient IoT modules, simplifying development and deployment for manufacturers. Many companies are actively developing and launching such modules to reduce regulatory hurdles, lower R&D costs, and enable faster time-to-market, making it easier for OEMs to launch connected devices. Energy-efficient designs extend battery life, improving performance and appeal across consumer, industrial, and automotive applications. Flexible integration options and support for multiple connectivity standards increase the versatility of IoT devices. Local design and production ensure modules meet both domestic and global requirements, supporting wider adoption. For instance, in January 2026, L&T Semiconductor Technologies (LTSCT) entered India’s Cellular IoT module market, launching pre-certified 4G modules for smart devices. Based on Qualcomm QCM2290 and enhanced with proprietary firmware, these modules offer power-efficient, reliable connectivity, simplified integration, and faster development cycles for both domestic and global markets.

Increasing demand from both consumers and enterprises is driving the adoption of connected solutions across various sectors. Consumers are seeking smart home devices, wearable technology, and connected appliances that offer convenience, automation, and real-time data access. Enterprises are deploying IoT solutions for industrial automation, asset tracking, logistics, and energy management to improve operational efficiency. The need for seamless connectivity across devices and platforms is creating a strong demand for reliable connectivity modules. Businesses are investing in smart infrastructure, including connected vehicles and smart meters, to enhance productivity and customer experience. The growing adoption of cloud computing and data analytics is fueling the integration of connected devices to deliver real-time insights. Enterprises are also prioritizing scalable, energy-efficient, and pre-certified modules to reduce development time and costs. Consumer demand for personalization, automation, and remote monitoring is further accelerating module adoption.

Connectivity Technology Insights

The short-range modules segment dominated the connectivity module type industry in 2025, accounting for a 48.3% share, due to their widespread use in consumer electronics, smart home devices, and industrial automation. Their low power consumption and compact design make them ideal for a variety of applications. These modules support protocols like Wi-Fi, Bluetooth, and Zigbee, enabling reliable local connectivity. Ease of integration and cost-effectiveness further drive adoption among OEMs. Growing demand for connected devices in smart homes, wearables, and IoT sensors reinforces their market dominance. Short-range modules remain a preferred choice for versatile and scalable IoT deployments.

Cellular LPWA modules are experiencing growth due to their ability to provide wide-area coverage with low power consumption. These modules support technologies such as NB-IoT and LTE-M, enabling reliable connectivity for IoT devices. They are increasingly used in applications including smart meters, asset tracking, and smart city infrastructure. Long battery life and low operational costs make them suitable for large-scale deployments. Expanding IoT adoption across utilities, agriculture, and industrial sectors is driving demand.

Product Insights

Cellular communication modules dominated the market in 2025, due to their reliable, wide-area communication capabilities. They are widely used in automotive, industrial, and consumer IoT applications, providing consistent connectivity across diverse environments. Support for 4G, LTE, and 5G networks ensures high-speed, stable, and low-latency data transmission. Compatibility with multiple LTE bands and global networks enables easy deployment across regions. OEMs prefer these modules for scalable solutions and for critical applications that require robust performance. Advanced security features and integrated network management tools further boost their adoption.

LPWA modules are experiencing rapid growth in the connectivity module market due to their low power consumption and long-range communication capabilities. They are widely used in applications such as smart metering, asset tracking, and smart city infrastructure. These modules enable devices to operate for extended periods on limited battery power, reducing maintenance costs. The increasing adoption of IoT solutions across the industrial and utility sectors is further driving demand. LPWA modules are gaining strong traction as a cost-effective and scalable connectivity option.

End Use Insights

Consumer electronics dominated the market in 2025 due to the widespread adoption of smart devices, wearables, and home automation products. These devices rely on reliable, low-latency connectivity to deliver seamless user experiences. Compact, energy-efficient modules simplify integration into small consumer gadgets. Growing demand for connected appliances, entertainment systems, and personal devices further drives module adoption. OEMs benefit from pre-certified and ready-to-integrate solutions that reduce development time and costs.

The automotive and telematics sector is growing rapidly as vehicles adopt connected solutions for navigation, safety, and fleet management. Connectivity modules enable real-time data transmission, remote diagnostics, and vehicle-to-everything (V2X) communication. Rising demand for electric and autonomous vehicles is accelerating the deployment of advanced modules. OEMs prefer scalable, high-performance modules to support complex connected vehicle ecosystems. Modules with long-range and low-power features improve efficiency and reduce operational costs. Consequently, the automotive and telematics sector is emerging as a significant growth driver in the connectivity module market.

Regional Insights

The Asia Pacific connectivity module industry held the largest share of 40.2% in 2025. The region’s growth is driven by rapid industrialization and expanding IoT adoption across key economies. Strong demand from consumer electronics, automotive, and industrial sectors supports widespread deployment of connectivity modules. Increasing investments in smart cities and digital infrastructure further accelerate market expansion. Asia Pacific continues to lead the market.

The connectivity module industry in China holds a significant share in the global market due to its strong manufacturing base and large-scale IoT adoption. The country benefits from high demand across consumer electronics, industrial automation, and smart city projects. The rapid expansion of 4G and 5G infrastructure supports widespread deployment of connectivity modules. Government initiatives promoting digital transformation and domestic production further strengthen market growth.

North America Connectivity Module Market Trends

The connectivity module industry in North America is driven by strong adoption of IoT technologies across industrial, automotive, and consumer sectors. The region benefits from advanced 5G infrastructure, enabling high-speed and low-latency connectivity. There is a growing shift toward multi-protocol and high-performance modules to support scalable applications. Increasing demand for connected vehicles, smart infrastructure, and industrial automation is accelerating module deployment.

U.S. Connectivity Module Market Trends

The U.S. connectivity module industry is driven by strong adoption of industrial IoT, connected vehicles, and smart infrastructure. There is a shift toward advanced technologies, such as 5G and eSIMs, to support scalable, efficient connectivity. Increasing demand for enterprise and consumer IoT applications is accelerating module deployment across sectors. As a result, the market continues to grow with a focus on innovation and high-performance connectivity solutions.

Europe Connectivity Module Market Trends

The connectivity module industry in Europe is driven by strong adoption of IoT solutions across industrial automation, automotive, and smart infrastructure sectors. The region benefits from advanced telecom networks and increasing deployment of 5G technologies. Strict regulatory standards and data security requirements influence the development of high-quality connectivity modules. The growing demand for connected vehicles and smart city initiatives is accelerating the deployment of modules.

Key Connectivity Module Company Insights

Some of the key companies in the connectivity module industry include Fibocom Wireless Inc., Huawei Technologies Co., Ltd., and Murata Manufacturing Co., Ltd. Among others. Organizations are focusing on increasing their customer base to gain a competitive edge in the industry. Therefore, key players are taking several strategic initiatives, such as mergers and acquisitions, and partnerships with other major companies.

-

Fibocom Wireless Inc. continues to expand its connectivity module portfolio with a focus on advanced 4G, 5G, and LPWA solutions. The company is developing compact and energy-efficient modules to support IoT applications across industries. It is also enhancing modules with multi-band support and eSIM capabilities for easier global deployment. The integration of edge AI features is being improved to enable smarter, more efficient devices. Ongoing product launches and technological advancements strengthen its position in the connectivity module market.

-

Huawei Technologies Co., Ltd. is advancing its connectivity modules with a strong focus on 5G and next-generation IoT solutions. The company is developing high-performance modules to support smart cities, industrial automation, and connected devices. It is also working on improving energy efficiency and network reliability in its module offerings. Enhanced security features and scalable architectures are being integrated into its solutions. Continuous innovation in wireless communication technologies supports its growth in the connectivity module industry.

Key Connectivity Module Companies:

The following key companies have been profiled for this study on the connectivity module market.

- Fibocom Wireless Inc.

- Huawei Technologies Co., Ltd.

- Murata Manufacturing Co., Ltd.

- Nordic Semiconductor

- Quectel Wireless Solutions

- Sequans Communications

- Sierra Wireless (Semtech Corporation)

- SIMCom Wireless Solutions

- Telit Cinterion

- u-blox Holding AG

Recent DevelopmentsIn March 2026, Fibocom Wireless Inc. showcased an expanded product portfolio integrating AI with wireless connectivity. The portfolio includes AI-powered CPEs, smart retail solutions, and a 5G Smart Android dongle to enhance intelligent connectivity across applications.

-

In October 2025, Quectel Wireless Solutions, an IoT solutions provider in China, collaborated with SM Electronic Technologies Pvt. Ltd. to showcase end-to-end IoT solutions at the India Mobile Congress. The collaboration highlighted integrated hardware, software, and services to simplify IoT deployment and accelerate time-to-market for device manufacturers.

-

In November 2024, u-blox Holding AG, a Swiss provider of wireless and positioning solutions, collaborated with Nordic Semiconductor, headquartered in Trondheim, to develop advanced wireless modules. This collaboration led to the launch of the NORA-B2 series, which integrates Nordic’s nRF54L15 SoC, enabling ultra-low-power, multi-protocol connectivity and reducing development complexity for IoT applications.

Connectivity Module Market Report Scope

Report Attribute

Details

Market size in 2025

USD 79.7 billion

Market size value in 2026

USD 87.9 billion

Revenue forecast in 2033

USD 181.9 billion

Growth rate

CAGR of 11.0% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive sector, growth factors, and trends

Segment scope

Connectivity technology, product, end use, region

Region scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; Japan; India; Australia; South Korea; Brazil; KSA; UAE; South Africa

Key companies profiled

Fibocom Wireless Inc.; Huawei Technologies Co., Ltd.; Murata Manufacturing Co., Ltd.; Nordic Semiconductor; Quectel Wireless Solutions; Sequans Communications; Sierra Wireless (Semtech Corporation); SIMCom Wireless Solutions; Telit Cinterion; u-blox Holding AG

Customization scope

Free report customization (equivalent up to 8 analysts’ working days) with purchase. Addition or alteration to country, regional & segment scope

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Connectivity Module Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends and opportunities in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global connectivity module market report in terms of connectivity technology, product, end use and region.

-

Connectivity Technology Outlook (Revenue, USD Billion, 2021 - 2033)

-

Cellular Modules

-

Cellular LPWA Modules

-

Non-Cellular LPWAN Modules

-

Short-Range Modules

-

GNSS Modules

-

-

Product Outlook (Revenue, USD Billion, 2021 - 2033)

-

Cellular Communication Modules

-

Wi-Fi Modules

-

Bluetooth Modules

-

LPWA Modules

-

Multi-Protocol Modules

-

-

End Use Outlook (Revenue, USD Billion, 2021 - 2033)

-

Consumer Electronics

-

Industrial IoT & Automation

-

Automotive & Telematics

-

Smart Cities & Infrastructure

-

Healthcare & Wearables

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

Australia

-

South Korea

-

-

Latin America

-

Brazil

-

-

Middle East & Africa (MEA)

-

KSA

-

UAE

-

South Africa

-

-

Frequently Asked Questions About This Report

The short-range modules segment accounted for the largest revenue share of 48.3% in 2025.

The cellular communication modules segment led with a 29.3% revenue share in 2025.

The consumer electronics segment dominated the market and accounted for the largest revenue share in 2025.

The global connectivity module market size was valued at USD 79.7 billion in 2025 and is estimated at USD 87.9 billion for 2026.

The global connectivity module market is expected to grow at a CAGR of 11.0% from 2026 to 2033, reaching USD 181.9 billion by 2033.

Asia Pacific dominated the connectivity module market with a share of 40.2% in 2025, driven by strong electronics manufacturing, widespread IoT adoption, expanding telecom infrastructure, and increasing deployment of connected devices across industries.

Key players include Fibocom Wireless Inc.; Huawei Technologies Co., Ltd.; Murata Manufacturing Co., Ltd.; Nordic Semiconductor; Quectel Wireless Solutions; Sequans Communications; Sierra Wireless (Semtech Corporation); SIMCom Wireless Solutions; Telit Cinterion; u-blox Holding AG.

Key factors driving the market growth include increasing adoption of connected devices, expansion of telecom infrastructure, advancements in IoT technologies, and rising demand for high-speed data connectivity.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.