- Home

- »

- Advanced Interior Materials

- »

-

Coolant Distribution Unit Market Size Report, 2026-2033GVR Report cover

![Coolant Distribution Unit Market (2026 - 2033)Report]()

Coolant Distribution Unit Market (2026 - 2033)

Size, Share & Trends Analysis Report By Type (In-Rack CDU, In-Row CDU, Floor-Mounted/Standalone CDU), By Cooling (Air-Cooled, Water-Cooled, Hybrid), By Cooling Capacity (Below 100 kW), By End Use, By Region, And Segment Forecasts

Market Size, 2025

$1.6BMarket Estimate, 2026

$1.8BMarket Forecast, 2033

$7.1BCAGR, 2026–2033

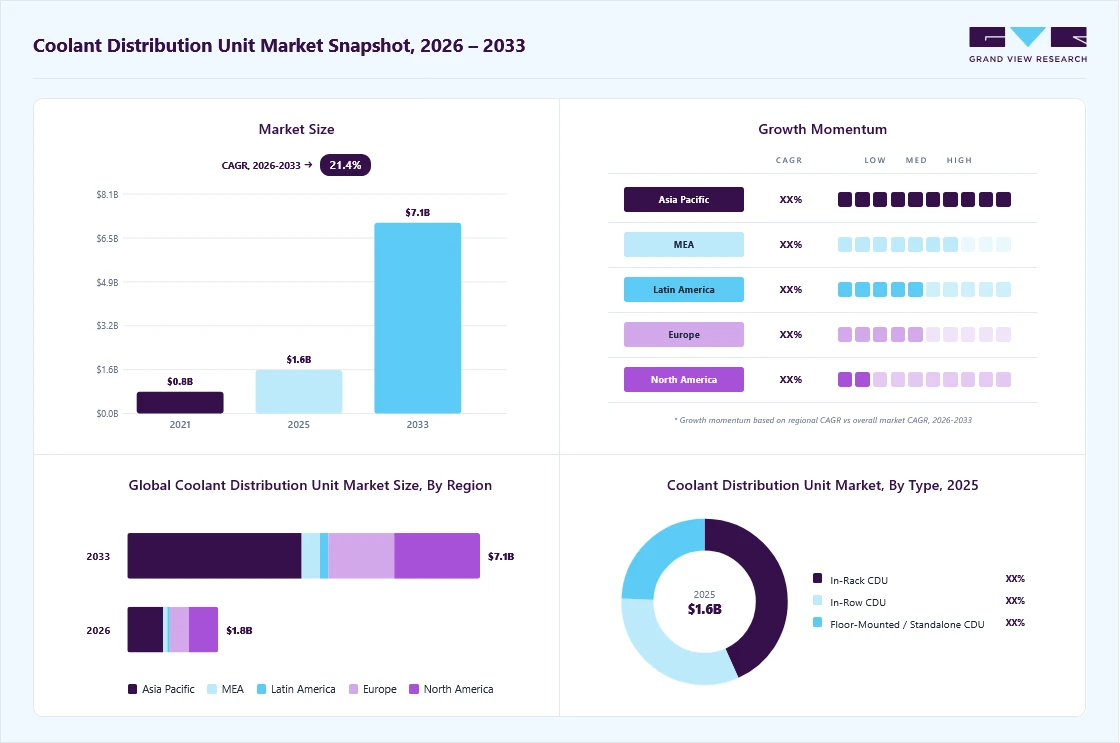

21.4%Coolant Distribution Unit Market Summary

The global coolant distribution unit market size was valued at USD 1.6 billion in 2025 and is projected to grow from USD 1.8 billion in 2026 to USD 7.1 billion by 2033, at a CAGR of 21.4% from 2026 to 2033. The Asia Pacific market held the largest share of 37.9% of the global market in 2025. The primary driving factor for the market is the rapid expansion of high-density data centers and AI-driven computing workloads, which significantly increase heat generation and power density within server environments.

Key Market Trends & Insights

- By type: The In-rack CDUs dominated the market and accounted for 43.3% share in 2025.

- By cooling: The air-cooled CDU systems dominated the market in 2025 and accounted for 48.1% share.

- By cooling capacity: The 100-500 kW cooling capacity segment dominated the market and accounted for 46.4% share in 2025.

- By end use: The data center segment dominated the CDU market in 2025 and accounted for 36.7% share.

Regional Highlights

- Largest regional market: Asia Pacific (37.9% revenue share, 2025)

- By country: The China held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 1.6 Billion

- Estimated market size in 2026: USD 1.8 Billion

- Projected market size by 2033: USD 7.1 Billion

- CAGR (2026-2033): 21.4%

Traditional air cooling systems are reaching their efficiency limits, prompting operators to adopt liquid cooling solutions supported by CDUs for precise thermal management. Another key driver is the increasing emphasis on energy efficiency, sustainability, and operational cost optimization across IT and industrial environments. Liquid cooling enabled by CDUs reduces energy consumption and improves heat transfer efficiency compared to conventional cooling methods, supporting regulatory and corporate sustainability targets. Rising electricity costs and carbon reduction initiatives encourage operators to invest in advanced thermal management technologies that lower power usage effectiveness (PUE). In addition, the expansion of edge data centers, digital transformation across industries, and growing investments in next-generation infrastructure continue to broaden the market scope and drive CDU adoption globally.")

Market Concentration & Characteristics

The coolant distribution unit (CDU) industry shows a moderately consolidated structure, where a limited number of specialized liquid cooling providers hold strong technological expertise, while several broader thermal management and HVAC companies participate through adjacent solutions. Leading players differentiate themselves through advanced engineering capabilities, integration with direct-to-chip cooling, and customized solutions for high-density environments. At the same time, emerging vendors and niche manufacturers are entering the market with modular and scalable CDU designs, increasing competitive diversity.

The coolant distribution unit (CDU) industry is characterized by a high level of innovation driven by the shift toward liquid cooling for AI, HPC, and high-density computing environments. Vendors are focusing on modular CDU designs, intelligent monitoring systems, and improved heat exchange efficiency to support next-generation workloads. Integration with direct-to-chip and immersion cooling technologies is accelerating product development and differentiation. Continuous innovation is also centered on scalability, energy optimization, and simplified deployment within existing data center infrastructures.

Regulatory frameworks related to energy efficiency, environmental sustainability, and data center emissions are influencing CDU adoption and design standards. Governments and industry bodies are encouraging lower power consumption and reduced carbon footprints, which supports the transition from traditional air cooling to liquid-based solutions. Compliance with safety standards, water management regulations, and operational reliability requirements also shapes product engineering. These regulations drive manufacturers to develop efficient, safe, and environmentally responsible cooling distribution systems.

End user demand is highly concentrated within data centers, IT & telecom operators, and high-performance computing environments where thermal density is rapidly increasing. Hyperscale cloud providers and colocation facilities represent key customers due to their large-scale infrastructure investments and need for efficient cooling solutions. Industrial and manufacturing applications are gradually adopting CDUs as automation and digitalization expand. The growing reliance on AI infrastructure further strengthens demand concentration among technology-driven enterprises.

Drivers, Opportunities & Restraints

The coolant distribution unit (CDU) industry is primarily driven by the rapid growth of AI workloads, hyperscale data centers, and high-density computing environments that require advanced thermal management solutions. Increasing rack power densities are pushing operators to adopt liquid cooling systems supported by CDUs for improved efficiency and reliability. Rising demand for energy-efficient infrastructure and lower operating costs is encouraging investment in liquid-based cooling technologies. In addition, the shift toward sustainable data center operations is accelerating CDU adoption across global markets.

Significant opportunities exist with the expansion of edge computing, next-generation AI infrastructure, and high-performance computing deployments that require scalable liquid cooling solutions. The increasing adoption of direct-to-chip and immersion cooling technologies creates demand for flexible and modular CDU designs. Emerging markets investing in digital infrastructure and cloud expansion are opening new growth avenues for manufacturers. Integration of smart monitoring, automation, and predictive maintenance features also provides opportunities for differentiation and long-term value creation.

High initial installation costs and complexity of integrating liquid cooling systems into existing facilities can slow CDU adoption among smaller operators. Concerns related to water management, leak risks, and maintenance requirements may limit deployment in certain environments. Lack of standardized infrastructure across older data centers can increase retrofitting challenges and capital investment needs. In addition, limited technical expertise in liquid cooling implementation may act as a barrier for some end users transitioning from traditional air cooling systems.

Type Insights

In-rack CDUs dominated the market and accounted for 43.3% share in 2025, due to their ability to deliver precise cooling directly within server racks, supporting high-density and AI-driven workloads. Their compact design reduces coolant distribution distance, improving thermal efficiency and minimizing energy loss. Data center operators prefer in-rack solutions for scalability and easier integration with direct-to-chip liquid cooling systems. Increasing demand for space optimization and higher rack power density further strengthens the adoption of in-rack CDUs.

The floor-mounted or standalone CDUs are witnessing rapid growth as large-scale data centers require centralized cooling distribution for multiple racks or zones. These systems provide higher capacity and flexibility, making them suitable for hyperscale environments and expanding liquid cooling deployments. Operators are adopting standalone units to simplify infrastructure upgrades and support future scalability. Rising investments in new data center construction and large AI clusters are accelerating demand for high-capacity standalone CDU solutions.

Cooling Insights

Air-cooled CDU systems dominated the market in 2025 and accounted for 48.1% share, due to their simpler installation, lower initial investment, and compatibility with existing data center infrastructure. Many facilities continue to rely on air-assisted cooling to manage moderate thermal loads while gradually transitioning toward liquid cooling technologies. These systems are preferred in environments where water-based cooling integration is limited or requires significant retrofitting. Operational familiarity and reduced complexity also contribute to the strong adoption of air-cooled configurations.

Hybrid cooling systems are emerging as the fastest-growing segment as they combine the advantages of air and liquid cooling to handle increasing heat loads efficiently. Data centers are adopting hybrid CDUs to balance performance, energy efficiency, and operational flexibility during the transition toward full liquid cooling. These systems enable gradual upgrades without major infrastructure changes, making them attractive for both new and existing facilities. Growing demand for adaptable cooling strategies in AI and high-performance computing environments is driving rapid growth in hybrid solutions.

Cooling Capacity Insights

The 100-500 kW cooling capacity segment dominated the market and accounted for 46.4% share in 2025, due to its suitability for medium to high-density data center deployments and enterprise-scale liquid cooling applications. This capacity range provides an optimal balance between performance, scalability, and operational efficiency, making it widely adopted across colocation and enterprise facilities. Many operators prefer this range as it supports gradual infrastructure upgrades without excessive capital investment. Its flexibility for both in-row and standalone CDU configurations further strengthens its market leadership.

The above 500 kW segment is witnessing the fastest growth driven by hyperscale data centers, AI clusters, and high-performance computing environments requiring advanced thermal management. Increasing rack power density and large-scale GPU deployments demand higher-capacity cooling distribution systems capable of handling extreme heat loads. Operators are investing in large CDU units to improve efficiency and support future expansion. Rapid construction of mega data centers and growing adoption of liquid cooling technologies are accelerating demand in this high-capacity segment.

End Use Insights

The data center segment dominated the CDU market in 2025 and accounted for 36.7% share due to the rapid increase in hyperscale facilities, cloud computing expansion, and rising demand for high-density server environments. Growing adoption of AI, machine learning, and high-performance computing workloads has significantly increased heat loads, driving the need for advanced liquid cooling solutions. CDUs play a critical role in maintaining thermal stability and improving energy efficiency within modern data centers. Continuous investments in new data center construction and upgrades further strengthen this segment’s leadership.

The IT & telecom segment is experiencing significant growth as network infrastructure expands to support 5G deployment, edge computing, and digital transformation initiatives. Increasing data traffic and higher processing requirements are pushing telecom operators to adopt more efficient cooling technologies. CDUs help manage thermal challenges in compact and high-performance telecom environments where space and efficiency are critical. The growing demand for reliable, scalable infrastructure to support real-time data processing is accelerating adoption within this sector.

Regional Insights

The North America coolant distribution unit (CDU) industry is experiencing significant growth at CAGR of 16.6% over the forecast period, driven by high adoption of AI workloads, advanced cloud computing infrastructure, and strong investments from hyperscale data center operators. The region benefits from early adoption of liquid cooling technologies and continuous innovation in thermal management solutions. Increasing demand for energy-efficient data center operations and sustainability initiatives is accelerating CDU deployment. Expansion of edge data centers and high-density computing environments further supports market growth.

U.S. Coolant Distribution Unit (CDU) Market Trends

The coolant distribution unit (CDU) industry in the U.S. dominated the North American CDU market due to the strong presence of hyperscale data centers, leading cloud service providers, and rapid adoption of AI-driven infrastructure. High investment in high-performance computing and advanced liquid cooling technologies has accelerated CDU deployment across major data center hubs. The need to manage increasing rack power density and improve energy efficiency continues to drive demand.

Canada coolant distribution unit (CDU) industry is witnessing steady growth driven by expansion of data center facilities supported by favorable climate conditions and increasing digital infrastructure investments. Rising demand for sustainable and energy-efficient cooling solutions is encouraging adoption of liquid cooling systems including CDUs. Growth in cloud services, telecom networks, and enterprise digitalization is contributing to market expansion. Government focus on clean energy and environmentally responsible operations further supports CDU adoption across the country.

Europe Coolant Distribution Unit (CDU) Market Trends

Europe coolant distribution unit (CDU) industry is witnessing steady growth due to strict energy efficiency regulations and increasing focus on sustainable data center operations. Operators are adopting CDU-based liquid cooling to reduce power consumption and meet carbon reduction targets. The region’s strong emphasis on green data centers and renewable energy integration is encouraging advanced cooling technologies. Rising investments in AI research and digital infrastructure development also contribute to market expansion.

The coolant distribution unit (CDU) industry in the UK dominated the CDU market in Europe due to strong data center investments, growing cloud adoption, and increasing deployment of high-density computing infrastructure. Major colocation hubs and hyperscale facilities are driving demand for advanced liquid cooling solutions to improve energy efficiency. The country’s focus on sustainability and strict energy regulations encourages adoption of CDU-supported cooling systems. Continuous expansion of AI and digital services further strengthens market leadership.

Spain coolant distribution unit (CDU) industry is emerging as a growing market driven by rising investments in new data center construction and expanding digital infrastructure. Increasing interest from hyperscale operators and colocation providers is supporting adoption of liquid cooling technologies. Favorable renewable energy initiatives and focus on efficient cooling solutions are encouraging CDU deployment. The country’s strategic location as a connectivity hub between Europe and other regions is also contributing to market growth.

Asia Pacific Coolant Distribution Unit (CDU) Market Trends

Asia Pacific coolant distribution unit (CDU) industry dominated the global coolant distribution unit (CDU) industry and accounted for 37.9% share in 2025, due to rapid expansion of hyperscale data centers, growing digitalization, and strong investments in cloud infrastructure across countries such as China, Japan, India, and South Korea. Increasing adoption of AI technologies and high-performance computing is driving demand for advanced liquid cooling solutions. Government support for digital transformation and smart infrastructure further strengthens market growth. The presence of large manufacturing ecosystems and technology hubs also supports regional leadership.

The coolant distribution unit (CDU) industry in China dominated the Asia Pacific CDU market due to large-scale expansion of hyperscale data centers, strong investments in AI infrastructure, and rapid growth in cloud computing services. Increasing deployment of high-performance computing systems has accelerated demand for advanced liquid cooling solutions. Government initiatives supporting digital economy development and smart infrastructure further strengthen market growth. The presence of major technology companies and manufacturing capabilities also contributes to the country’s leadership.

India coolant distribution unit (CDU) industry is witnessing strong growth driven by increasing data center construction, rapid digital transformation, and rising demand for cloud and telecom services. Growing adoption of AI applications and high-density IT infrastructure is encouraging the use of liquid cooling technologies such as CDUs. Government initiatives promoting digitalization and data localization policies are supporting infrastructure investments. Expansion of edge computing and enterprise digital adoption is further accelerating market growth.

Middle East & Africa Coolant Distribution Unit (CDU) Market Trends

The Middle East and Africa coolant distribution unit (CDU) industry is showing growing potential due to increasing investments in data center development, smart city initiatives, and digital infrastructure modernization. High ambient temperatures and energy efficiency concerns are encouraging the adoption of advanced cooling solutions such as CDUs. Governments and private investors are focusing on technology-driven economic diversification, which supports infrastructure expansion. Rising demand for cloud services and enterprise digitalization is further driving market growth.

South Africa coolant distribution unit (CDU) industry is emerging as a growing market for coolant distribution units due to increasing investments in data center infrastructure and rising demand for cloud and digital services. Expansion of colocation facilities and growing adoption of high-performance computing environments are driving the need for advanced cooling solutions. The country’s focus on energy efficiency and operational reliability is encouraging the adoption of liquid cooling technologies. In addition, improving connectivity and digital transformation initiatives are supporting CDU market growth.

Latin America Coolant Distribution Unit (CDU) Market Trends

Latin America coolant distribution unit (CDU) industry is gradually emerging as a growth market as digital transformation and cloud adoption increase across key economies. Expansion of regional data center infrastructure and rising internet penetration are creating demand for efficient cooling solutions. Companies are investing in modern facilities that incorporate advanced thermal management technologies, including liquid cooling systems. Growing awareness of energy efficiency and operational cost optimization is supporting CDU adoption in the region.

The coolant distribution unit (CDU) industry in Brazil is witnessing steady growth driven by expanding data center investments and increasing adoption of cloud and digital services. Rising demand for high-density computing and improved thermal management solutions is encouraging the shift toward liquid cooling technologies. Growth in telecom infrastructure and enterprise digital transformation is further supporting market expansion. In addition, increasing focus on energy efficiency and operational cost optimization is contributing to CDU adoption across the country.

Key Coolant Distribution Unit Company Insights

Some of the key players operating in the market include Vertiv Holdings Co., CoolIT Systems, and Delta Electronics, Inc.

-

Vertiv develops advanced coolant distribution units (CDUs) designed for high-density computing environments, supporting direct-to-chip liquid cooling and scalable thermal management for AI and hyperscale data centers. Its CDU solutions are integrated with precision cooling platforms, enabling efficient heat transfer and improved operational reliability. The company also operates across several related verticals including power management systems, uninterruptible power supply (UPS) solutions, thermal management infrastructure, integrated rack systems, and data center monitoring software. Vertiv provides end-to-end digital infrastructure solutions combining cooling, power, and management technologies. Its strong presence across edge computing, enterprise data centers, and telecom infrastructure strengthens its role within liquid cooling ecosystems.

-

CoolIT Systems focuses on liquid cooling technologies with specialized CDU platforms that enable precise coolant delivery for high-performance computing and AI-driven workloads. Its solutions emphasize direct liquid cooling, improving energy efficiency and supporting higher rack power densities compared to traditional cooling methods. Beyond CDUs, the company operates in verticals such as direct-to-chip cooling modules, cold plate design, system integration services, and thermal management solutions for enterprise servers and hyperscale deployments. CoolIT also collaborates with OEM partners to integrate cooling solutions into server and infrastructure platforms. The company’s expertise spans data center cooling innovation, performance optimization, and advanced thermal engineering.

Key Coolant Distribution Unit Companies:

The following key companies have been profiled for this study on the coolant distribution unit (CDU) market.

- Vertiv Holdings Co.

- CoolIT Systems

- NIDEC CORPORATION

- ifm electronic gmbh

- Motivair Corporation

- Delta Electronics, Inc.

- Johnson Controls.

- NMB Technologies Corporation (a MinebeaMitsumi Group company)

- nVent

- JETCOOL Technologies Inc

- DCX POLSKA SP. Z O.O.

- FläktGroup

- Trane

- Carrier

- AIREDALE INTERNATIONAL AIR CONDITIONING LTD

- Super Micro Computer, Inc.

Recent Developments

-

In January 2026, DCX introduced a high capacity 8MW coolant distribution unit designed for large-scale AI and high-density data center cooling. The system supports warm-water cooling to enhance energy efficiency and reduce dependence on chillers. It is built for facility-level deployment, enabling centralized liquid cooling across data halls. The solution focuses on scalable performance and simplified cooling infrastructure for advanced computing environments.

-

In September 2025, Flex introduced a modular rack-level coolant distribution unit designed to deliver scalable, high-performance liquid cooling for AI, HPC, and hyperscale data center workloads. The solution allows flexible deployment from 2 to 6 CDUs per rack, supporting capacity scaling up to 1.8 MW as cooling needs increase. Its modular architecture enables incremental expansion without major infrastructure changes, helping operators optimize space and efficiency. The design supports adaptive cooling strategies while reducing energy waste and simplifying upgrades.

Coolant Distribution Unit (CDU) Market Report Scope

Report Attribute

Details

Market size in 2025

USD 1.6 billion

Estimated market size in 2026

USD 1.8 billion

Projected market size by 2033

USD 7.1 billion

Growth Rate

CAGR of 21.4% from 2026 to 2033

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Type, cooling, cooling capacity, end use, region

Regional scope

North America, Europe, Asia Pacific, Latin America, Middle East & Africa

Country scope

U.S.; Canada; Mexico; UK; Germany; France; Spain; Italy; China; Japan; India; Australia; South Korea; Brazil; Argentina; UAE; Saudi Arabia; South Africa

Key companies profiled

Vertiv Holdings Co.; CoolIT Systems; NIDEC CORPORATION; ifm electronic gmbh; Motivair Corporation; Delta Electronics, Inc.; Johnson Controls; NMB Technologies Corporation (a MinebeaMitsumi Group company); nVent; JETCOOL Technologies Inc; DCX POLSKA SP. Z O.O.; FläktGroup; Trane; Carrier; AIREDALE INTERNATIONAL AIR CONDITIONING LTD; Super Micro Computer, Inc.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Coolant Distribution Unit (CDU) Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global coolant distribution unit market report based on type, cooling, cooling capacity, end use, and region:

-

Type Outlook (Revenue, USD Million, 2021 - 2033)

-

In-Rack CDU

-

In-Row CDU

-

Floor-Mounted / Standalone CDU

-

-

Cooling Outlook (Revenue, USD Million, 2021 - 2033)

-

Air-Cooled

-

Water-Cooled

-

Hybrid

-

-

Cooling Capacity Outlook (Revenue, USD Million, 2021 - 2033)

-

Below 100 kW

-

100-500 kW

-

Above 500 kW

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

IT & Telecom

-

Data Centers

-

Manufacturing & Industrial

-

Healthcare

-

BFSI

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

France

-

Italy

-

Spain

-

UK

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East and Africa

-

Saudi Arabia

-

UAE

-

South Africa

-

-

Frequently Asked Questions About This Report

The in-rack CDUs segment led with a 43.3% revenue share in 2025, while the floor-mounted or standalone CDUs segment is the fastest-growing.

The air-cooled CDU systems segment led with a 48.1% revenue share in 2025, while the hybrid cooling systems segment is the fastest-growing.

The 100-500 kw cooling capacity segment led with a 46.4% revenue share in 2025, while the above 500 kw segment is the fastest-growing.

Data center segment held the largest share (over 36.0%) in 2025, while the IT & telecom segment is experiencing significant growth.

The global coolant distribution unit market size was estimated at USD 1.6 billion in 2025 and is expected to be USD 1.8 billion in 2026.

The global coolant distribution unit market, in terms of revenue, is expected to grow at a compound annual growth rate of 21.4% from 2026 to 2033 to reach USD 7.1 billion by 2033.

Asia Pacific dominated the coolant distribution unit (CDU) market and accounted for 37.9% share in 2025, due to rapid expansion of hyperscale data centers, growing digitalization, and strong investments in cloud infrastructure across countries such as China, Japan, India, and South Korea. Increasing adoption of AI technologies and high-performance computing is driving demand for advanced liquid cooling solutions.

Some of the key players operating in the global coolant distribution unit market include Vertiv Holdings Co.; CoolIT Systems; NIDEC CORPORATION; ifm electronic gmbh; Motivair Corporation; Delta Electronics, Inc.; Johnson Controls; NMB Technologies Corporation (a MinebeaMitsumi Group company); nVent; JETCOOL Technologies Inc; DCX POLSKA SP. Z O.O.; FläktGroup; Trane; Carrier; AIREDALE INTERNATIONAL AIR CONDITIONING LTD; Super Micro Computer, Inc.

The global coolant distribution unit (CDU) market is driven by rising adoption of high-density computing, AI workloads, and hyperscale data center expansion requiring advanced liquid cooling solutions. Increasing focus on energy efficiency, sustainability goals, and reducing power consumption is accelerating the shift from traditional air cooling to liquid-based systems. Additionally, growing investments in high-performance computing, edge data centers, and next-generation digital infrastructure are supporting market growth.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.