- Home

- »

- IT Services & Applications

- »

-

Data Center Testing Market Size & Share Report, 2026-2033GVR Report cover

![Data Center Testing Market (2026 - 2033)Report]()

Data Center Testing Market (2026 - 2033)

Size, Share & Trends Analysis Report By Service Type (Functional Testing, Performance Testing), By Deployment (Cloud, On-premise), By End Use (IT and Telecom, Healthcare), By Region, And Segment Forecasts

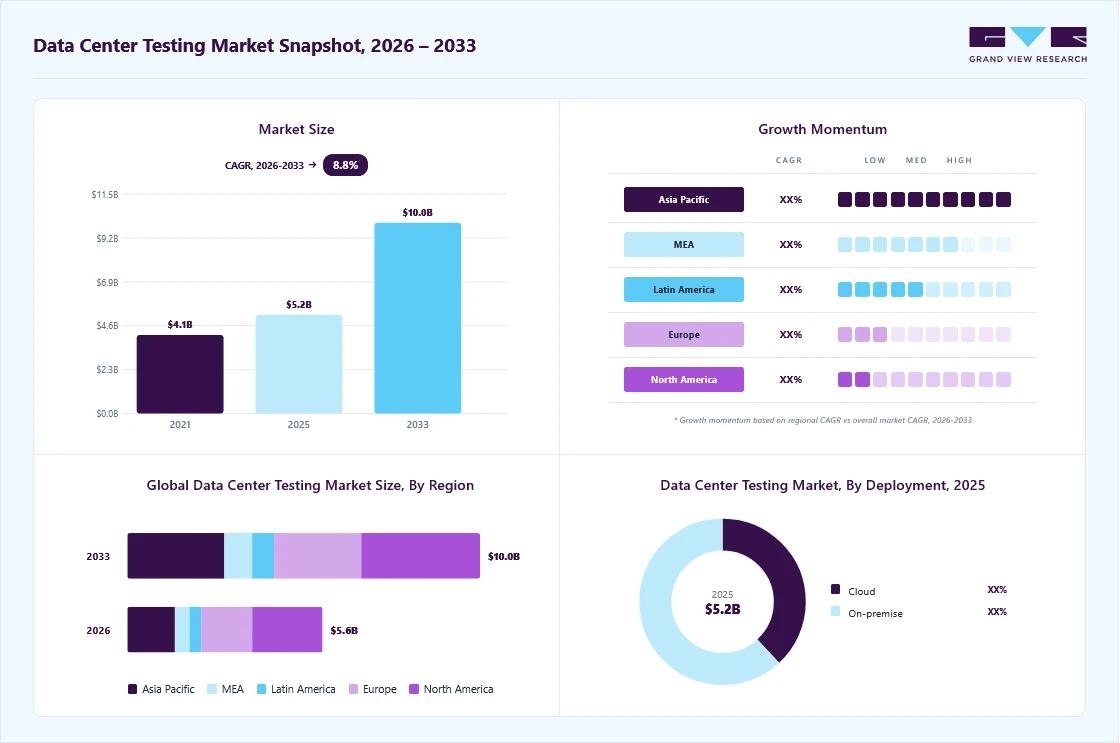

Market Size, 2025

$5.2BMarket Estimate, 2026

$5.6BMarket Forecast, 2033

$10.0BCAGR, 2026–2033

8.8%Data Center Testing Market Summary

The global data center testing market size was valued at USD 5.2 billion in 2025 and is projected to grow from USD 5.6 billion in 2026 to USD 10.0 billion by 2033, at a CAGR of 8.8% from 2026 to 2033. The market in North America dominated with a revenue share of 36.4% in 2025. The market has expanded steadily over the past decade due to growing reliance on cloud computing, enterprise colocation, hyperscale campuses, AI workloads, and digital services that require uninterrupted uptime.

Key Market Trends & Insights

- By service type: Network testing segment held the largest market share of 30.6% in 2025.

- By deployment: On-premise segment held the largest market share in 2025.

- By end use: IT & telecom segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: North America (36.4% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 5.2 Billion

- Estimated market size in 2026: USD 5.6 Billion

- Projected market size by 2033: USD 10.0 Billion

- CAGR (2026-2033): 8.8%

The rapid global expansion of cloud computing and hyperscale data centers will drive market growth. Leading cloud providers are investing heavily in new facilities and regional zones to meet rising demand from enterprises shifting workloads to the cloud. Each new data center must undergo extensive testing before operations begin, including validation of electrical infrastructure, backup generators, UPS systems, cooling performance, automation controls, and network reliability. These tests help ensure uninterrupted uptime, operational efficiency, and compliance with service-level agreements. As hyperscale facilities become larger, denser, and more technologically complex, operators increasingly rely on specialized testing companies with expertise in commissioning, integrated systems validation, and performance assurance, thereby driving sustained market growth worldwide.")

The rising cost of data center downtime is a major driver for the market growth. Even short outages can disrupt online retail transactions, banking systems, hospital operations, cloud services, and communication networks, resulting in significant revenue losses and damaging customer trust. In highly digital industries, uninterrupted availability is critical, making reliability a top priority. To reduce these risks, organizations are increasing investments in preventative testing, integrated systems testing, backup power validation, and failover simulations. These measures help detect hidden weaknesses in infrastructure before they cause operational failures. As businesses move from reactive maintenance practices to proactive resilience planning, demand for regular testing services continues to grow, expanding global market opportunities.

A Ponemon Institute study of 41 data centers found that the average outage lasted 1.7 hours and cost approximately USD 505,502 per incident, equal to about USD 4,911 per minute of downtime. These findings highlight the significant financial impact of service interruptions. In addition, Eaton’s Downtime Cost Calculator estimates that a colocation data center under a typical operating scenario could incur losses of USD 335,497 during an outage. These costs include lost sales revenue, reduced employee productivity, mission-critical data loss, brand damage, and potential service-level agreement penalties, emphasizing why uptime and preventative infrastructure management are critical for data center operators.

Market Dynamics

The rapid adoption of hybrid cloud and edge computing infrastructure is significantly driving the market growth. Enterprises are increasingly deploying workloads across on-premises facilities, public clouds, colocation sites, and edge locations to improve scalability, reduce latency, and support real-time applications. This distributed architecture increases the complexity of managing and validating network performance, security, interoperability, and uptime across multiple environments. As a result, organizations are investing in continuous testing, remote monitoring, and automated validation solutions to ensure seamless operations and minimize downtime. The expansion of IoT, 5G networks, AI applications, and content delivery services is further accelerating the need for scalable, cloud-based, and automated testing solutions across geographically dispersed data center infrastructures.

Modern data centers involve highly complex environments that integrate hybrid cloud infrastructure, AI workloads, liquid-cooling systems, cybersecurity frameworks, and high-speed networking technologies. Testing and validating these advanced systems requires professionals with specialized expertise in network performance analysis, thermal management, security assessment, automation, and compliance testing.

However, the industry faces a limited availability of trained engineers and commissioning experts capable of managing such sophisticated infrastructures. This skills gap can delay deployment timelines, slow commissioning processes, increase operational risks, and raise labor costs for service providers. As data center architectures continue evolving rapidly, continuous workforce training and technical upskilling have become increasingly critical for market growth.

Market Concentration & Characteristics

The data center testing industry is moderately concentrated, with a mix of global testing equipment providers, network validation specialists, and data center commissioning service firms dominating the competitive landscape. Large players such as Rohde & Schwarz, Keysight Technologies, Spirent Communications, VIAVI Solutions, and Siemens hold significant market share due to their strong technology portfolios, global service capabilities, and expertise in network, performance, thermal, and security testing for hyperscale and enterprise data centers.

The data center testing industry is highly technology-driven and innovation-intensive, with increasing adoption of AI-enabled testing, automated diagnostics, digital twin simulation, high-speed network validation (400G/800G), and liquid cooling performance testing. The industry is further characterized by strong demand from hyperscale cloud providers, telecom operators, BFSI organizations, and colocation facilities requiring continuous uptime assurance and cybersecurity validation. Strategic partnerships, regional expansion, and mergers & acquisitions are shaping competition, while smaller niche players focus on customized testing services and commissioning support for edge and modular data centers.

Service Type Insights

The network testing segment led the market with the largest revenue share of 30.6% in 2025, primarily due to the expansion of cloud and hyperscale data centers. These large facilities operate complex network environments that connect thousands of servers, storage systems, and users across multiple locations. To maintain seamless performance, every new deployment requires extensive testing of routing paths, traffic distribution, bandwidth capacity, redundancy systems, and failover mechanisms. Network testing ensures stable connectivity, low latency, and uninterrupted service availability. As cloud providers continue to invest in larger, more advanced hyperscale campuses worldwide, demand for specialized network testing solutions and services is increasing significantly.

The security testing segment is expected to grow at the fastest CAGR during the forecast period, due to the rising frequency of cyberattacks. Data centers store critical enterprise and customer information, making them attractive targets for ransomware, malware, DDoS attacks, insider misuse, and credential theft. To reduce these risks, operators are increasing investments in vulnerability assessments, penetration testing, security audits, and threat simulation services that help identify weaknesses before attackers exploit them.

Deployment Insights

The on-premise segment accounted for the largest market revenue share in 2025. On-premises deployment remains dominant in Tier-3 and Tier-4 data centers where direct physical access to testing equipment is necessary. Critical functions such as optical signal integrity measurement, power quality monitoring, and electromagnetic compatibility testing depend on specialized hardware, supporting continued investment in on-site solutions. Government, defense, and financial facilities with air-gapped environments also prefer on-premises systems due to regulatory restrictions on cloud-connected platforms. Established vendors such as Tektronix, Anritsu, and Rohde & Schwarz benefit through hardware sales, calibration services, software upgrades, and equipment refresh cycles as technologies advance.

The cloud segment is expected to grow at the fastest CAGR during the forecast period. Scalability and on-demand test environments are key growth drivers for the cloud segment in the data center testing industry. Cloud testing allows operators to quickly deploy virtual environments for load testing, disaster recovery exercises, and performance simulations without investing in physical infrastructure. Resources can be increased or reduced instantly based on project requirements, improving flexibility and cost efficiency. This makes cloud testing highly suitable for fast-changing and capacity-driven data center operations.

End Use Insights

The IT & telecom segment accounted for the largest market revenue share in 2025. Telecom companies are investing significantly in next-generation connectivity infrastructure to support faster speeds, higher bandwidth, and improved user experiences. These network upgrades increase reliance on data centers to handle traffic management, subscriber information, and edge computing workloads. As a result, operators require extensive testing of uptime, low-latency performance, backup systems, and network resiliency. This ensures uninterrupted service delivery, strong customer satisfaction, and reliable performance across increasingly complex telecom ecosystems.

The healthcare segment is expected to grow at the fastest CAGR during the forecast period, due to the increasing need for zero downtime and patient safety. Even brief IT disruptions can affect access to patient records, diagnostic systems, pharmacy operations, appointment scheduling, and emergency services. To prevent such risks, hospitals are investing in backup power validation, failover simulations, and integrated systems testing. These measures help ensure continuous operations, reliable care delivery, and patient safety.

Regional Insights

North America dominated the global data center testing market with the largest market share of 36.4% in 2025. North America remains the global leader in hyperscale infrastructure, led by major cloud providers such as AWS, Microsoft, Google, and Meta. Continuous investment in new campuses and AI-ready facilities creates strong demand for commissioning, electrical validation, cooling tests, and network resiliency assessments before launch. Recent large AI leasing and build announcements in the U.S. highlight ongoing capacity expansion.

U.S. Data Center Testing Market Trends

The data center testing market in the U.S. accounted for the largest market revenue share in North America in 2025. The country is seeing rapid development of AI-focused data centers requiring dense compute environments, GPU clusters, liquid cooling, and higher power loads. These advanced facilities require specialized testing of thermal, power quality, and integrated systems. The U.S. AI data center market is forecast to grow strongly in the long term, supporting demand for testing.

Europe Data Center Testing Market Trends

The data center testing market in Europe is anticipated to register at a considerable CAGR from 2026 to 2033, driven by strong investment in hyperscale and cloud data centers as demand for digital services, enterprise cloud migration, and AI computing rises. New facilities across markets such as Germany, the UK, Ireland, Spain, and the Nordics require commissioning, electrical validation, cooling performance tests, and network resiliency checks before operations begin.

The UK data center testing market is expected to grow rapidly in the coming years. The UK remains one of Europe’s leading data center hubs, attracting continuous investment from global cloud providers such as AWS, Microsoft, Google, and Oracle. Growing enterprise cloud adoption and digital transformation are driving new campus developments and regional expansions. Every new facility requires commissioning, electrical validation, cooling tests, and network resiliency assessments, increasing demand for data center testing services.

The data center testing market in Germany is gaining substantial momentum due to the stringent environmental and efficiency regulations for infrastructure. Operators must optimize cooling systems, energy usage, and heat recovery performance. This drives demand for airflow analysis, recommissioning, thermal optimization, and power usage effectiveness (PUE) testing.

Asia Pacific Data Center Testing Market Trends

The data center testing market in the Asia Pacific is projected to witness at the fastest CAGR of 10.7% from 2026 to 2033. Countries such as India, Indonesia, Malaysia, Thailand, Vietnam, and the Philippines are becoming major destinations for new data center capacity. Lower costs, supportive policies, and rising internet penetration are encouraging greenfield developments that require complete testing before launch.

The Japan data center testing market is expected to grow rapidly in the coming years. Japan is accelerating the deployment of AI infrastructure, including high-density GPU clusters and advanced compute campuses. AI-ready facilities require liquid-cooling validation, thermal performance testing, power-quality monitoring, and integrated systems testing. Pilot projects involving liquid-cooled AI servers highlight the need for specialized testing solutions.

The data center testing market in China held a substantial market share in the Asia Pacific in 2025. China is one of the world’s largest and fastest-growing data center markets, supported by strong investments from Alibaba Cloud, Tencent Cloud, Huawei Cloud, Baidu AI Cloud, and telecom operators. China’s data center market is projected to grow significantly through 2033, creating strong demand for commissioning, electrical validation, cooling tests, and network resiliency services for new facilities.

Key Data Center Testing Company Insight

Key players operating in the data center testing industry are Spirent Communications, VIAVI Solutions, EXFO, Keysight Technologies, Rohde & Schwarz, Schneider Electric, Eaton, Siemens, ABB, Intertek Group, UL Solutions, WSP Global, AECOM, Aggreko, and ABM Industries.

Companies are focusing on various strategic initiatives, including new product development, partnerships & collaborations, and agreements to gain a competitive advantage over their rivals.

Key Data Center Testing Companies:

The following key companies have been profiled for this study on the data center testing market.

- ABB

- ABM Industries

- AECOM

- Aggreko

- Calnex Solutions

- EXFO

- Intertek Group

- Keysight Technologies

- Rohde & Schwarz

- NetScout

- Siemens

- Spirent Communications

- UL Solutions

- VIAVI Solutions

- WSP Global

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: Keysight Technologies; Spirent Communications; VIAVI Solutions; Rohde & Schwarz; Anritsu; Cisco Systems - Expanding AI-driven and automated testing platforms for hyperscale and edge data centers

- Investing in high-speed Ethernet validation, liquid cooling testing, and cybersecurity testing capabilities

- Strengthening global presence through acquisitions, strategic partnerships, and cloud-native testing solutions

- Offering integrated testing portfolios covering network, optical, performance, and compliance validation.

- Strong global customer base across hyperscalers, telecom operators, and enterprise data centers

- Comprehensive end-to-end testing portfolios with advanced automation and analytics capabilities

- High switching costs due to deep integration with customer infrastructure and workflows

- Significant R&D investments enabling leadership in AI, 5G, 400G/800G Ethernet, and hybrid cloud testing.

- High dependence on large enterprise and telecom spending cycles

- Premium pricing limits penetration among small and mid-sized data center operators

- Complex product ecosystems may require specialized training and support

- Regulatory scrutiny and integration challenges associated with mergers and acquisitions.

Emerging Players: Veryx Technologies; NetScout; Calnex Solutions - Focusing on niche testing areas such as AI workload validation, software-defined networking (SDN), edge infrastructure testing, and automated remote diagnostics

- Providing flexible SaaS-based and cloud-native testing solutions with faster deployment models

- Expanding regional commissioning and compliance testing services for modular and colocation data centers

- Leveraging AI and analytics to improve predictive maintenance and continuous monitoring capabilities.

- Faster innovation cycles and greater flexibility in addressing emerging customer requirements

- Competitive pricing and customized solutions for regional operators and mid-sized enterprises

- Strong specialization in targeted technologies such as optical networking, synchronization testing, and cloud-native automation

- Ability to quickly adapt solutions for edge and distributed infrastructure environments.

- Limited global reach and lower brand recognition compared to established vendors

- Smaller R&D budgets restrict large-scale product development and global expansion

- Dependence on partnerships and channel networks for broader market penetration

- Difficulty competing for large hyperscale and government contracts dominated by major players.

Recent Development

-

In April 2026, VIAVI Solutions announced a new investment in its PCIe 7.0 protocol analysis testing platform, expanding its Xgig product family with analyzers, exercisers, and high-performance interposers. The platform is designed to support next-generation applications such as AI, hyperscale data centers, cloud computing, and quantum systems. Operating at 128 GT/s, PCIe 7.0 doubles the bandwidth of PCIe 6.0, helping developers improve product performance and reduce troubleshooting time.

-

In June 2025, UL Solutions launched a new testing and certification service for immersion cooling fluids used in AI-driven data centers. The offering helps operators improve safety, thermal performance, and sustainability by validating fluids used to prevent overheating in high-density IT equipment. The program tests critical properties, including autoignition temperature, flash point, and dielectric breakdown voltage. It supports the growing demand for energy-efficient cooling alternatives amid rising global data center power consumption.

-

In April 2025, Aggreko expanded its North American data center testing portfolio by launching a 500 kW liquid-cooled resistive load bank designed for commissioning and testing liquid-to-liquid cooling systems. The solution helps operators verify that server racks remain within optimal thermal limits, reducing inefficiencies and downtime. It features corrosion-resistant construction, 5 kW load-step resolution, scalable networking of up to 200 units, and portable deployment. The launch supports growing demand for AI and high-density data center cooling infrastructure.

Data Center Testing Market Report Scope

Report Attribute

Details

Market size in 2025

USD 5.2 billion

Estimated market size in 2026

USD 5.6 billion

Projected market size by 2033

USD 10.0 billion

Growth rate

CAGR of 8.8% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2026 to 2033

Report Installation Type

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Service type, deployment, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; Saudi Arabia; South Africa

Key companies profiled

ABB; ABM Industries; AECOM; Aggreko; Calnex Solutions; EXFO; Intertek Group; Keysight Technologies; Rohde & Schwarz; NetScout; Siemens; Spirent Communications; UL Solutions; VIAVI Solutions; WSP Global

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Data Center Testing Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented global data center testing market report based on service type, deployment, end use, and region.

-

Service Type Outlook (Revenue, USD Billion, 2021 - 2033)

-

Functional Testing

-

Performance Testing

-

Security Testing

-

Network Testing

-

Others

-

-

Deployment Outlook (Revenue, USD Billion, 2021 - 2033)

-

Cloud

-

On-premise

-

-

End Use Outlook (Revenue, USD Billion, 2021 - 2033)

-

IT and Telecom

-

BFSI

-

Healthcare

-

Government

-

Retail

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Delivered Customization

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

AI infrastructure and hyperscale data center testing opportunity assessment for a testing solutions provider

Assessed demand for AI data center testing across hyperscale, colocation, and enterprise facilities

Analyzed adoption trends for liquid cooling validation, GPU cluster benchmarking, and 400G/800G network testing

Benchmarked key testing vendors based on automation capabilities, thermal testing expertise, and service portfolios

Identified fastest-growing AI and hyperscale testing segments

Supported product positioning for next-generation testing platforms

Highlighted investment opportunities in AI infrastructure commissioning and validation

Customized segmentation analysis for the Data Center Testing Market by testing type and end user

Analyzed regional demand for edge data center validation and hybrid cloud testing services

Evaluated customer requirements for continuous monitoring, remote diagnostics, and cybersecurity testing

Assessed competitive landscape and partnership opportunities

Identified high-growth verticals and testing applications

Highlighted End Use industries with the highest spending potential

Supported targeted go-to-market and expansion strategies

Regional expansion strategy assessment for a network testing equipment manufacturer

Analyzed adoption trends for high-speed Ethernet testing, fiber validation, and AI workload performance testing across APAC and Middle East markets

Assessed regional infrastructure investments, cloud expansion projects, and colocation growth

Evaluated distributor and channel partner landscape

Identified priority expansion markets with strong hyperscale investments

Supported channel partner selection and regional sales strategy

Highlighted growth opportunities in emerging AI-ready data center ecosystems

Frequently Asked Questions About This Report

The global data center testing market size was valued at USD 5.2 billion in 2025 and is estimated at USD 5.6 billion for 2026.

North America accounted for the largest market share of 36.4% in 2025 in the data center testing market, led by major cloud providers such as AWS, Microsoft, Google, and Meta. Continuous investment in new campuses and AI-ready facilities creates strong demand for commissioning, electrical validation, cooling tests, and network resiliency assessments before launch.

Key players include ABB; ABM Industries; AECOM; Aggreko; Calnex Solutions; EXFO; Intertek Group; Keysight Technologies; Rohde & Schwarz; NetScout; Siemens; Spirent Communications; UL Solutions; VIAVI Solutions; WSP Global.

The key factors driving the growth of the market include growing reliance on cloud computing, enterprise colocation, hyperscale campuses, AI workloads, and digital services that require uninterrupted uptime.

Asia Pacific is the fastest-growing region over the forecast period.

Network testing segment led with a 30.6% revenue share in 2025, while security testing is the fastest-growing service type.

The on-premise segment held the largest revenue share in 2025, while cloud is the fastest-growing deployment.

IT & telecom segment held the largest revenue share in 2025, while healthcare is the fastest-growing segment.

The global data center testing market is expected to grow at a CAGR of 8.8% from 2026 to 2033, reaching USD 10.0 billion by 2033.

About the Author(s)

IT Services & Applications Research Team

Technology · IT Services & ApplicationsThis report was authored by the it services & applications research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the it services & applications segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.