- Home

- »

- IT Services & Applications

- »

-

Distributed Cloud Market Size And Share Report, 2026-2033GVR Report cover

![Distributed Cloud Market Size, Share & Trends Report]()

Distributed Cloud Market (2026 - 2033) Size, Share & Trends Analysis Report By Application (Edge Computing, Content Delivery), By Service (Data Security, Data Storage), By Enterprise Size, By End-use, By Region, And Segment Forecasts

Market Size, 2025

$5.1BMarket Estimate, 2026

$6.1BMarket Forecast, 2033

$26.5BCAGR, 2026–2033

23.3%Distributed Cloud Market Summary

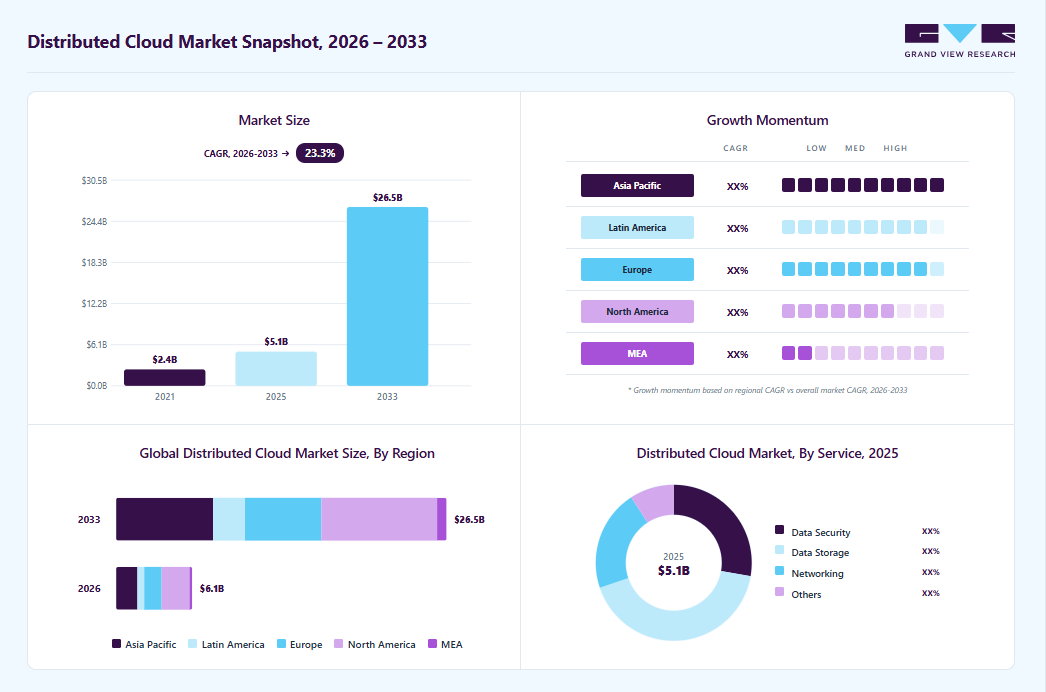

The global distributed cloud market size was valued at USD 5.1 billion in 2025 and is projected to grow from USD 6.1 billion in 2026 to USD 26.5 billion by 2033, at a CAGR of 23.3% from 2026 to 2033. The market in North America dominated with a revenue share of 36.9% in 2025. The market growth is driven by rising demand for low-latency computing, the increasing adoption of edge computing, the rapid rollout of 5G networks, and the growing need for data sovereignty and regulatory compliance.

Key Market Trends & Insights

- By application: Edge computing segment led the market with the largest revenue share of 42.9% in 2025.

- By service: Data storage segment accounted for the largest market revenue share in 2025.

- By enterprise size: SMEs segment is expected to grow at the fastest CAGR during the forecast period.

- By end-use: BFSI segment accounted for the largest revenue share in 2025.

Regional Highlights

- Largest regional market: North America (36.9% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- The distributed cloud industry in the U.S. held the largest revenue share in 2025.

Market Size & Forecast

- Market size in 2025: USD 5.1 Billion

- Estimated market size in 2026: USD 6.1 Billion

- Projected market size by 2033: USD 26.5 Billion

- CAGR (2026-2033): 23.3%

Organizations are shifting from centralized cloud models to distributed architectures to improve performance, enhance data security, and support real-time applications. Strong growth in edge computing is one of the key driving factors for the growth of the distributed cloud industry. Enterprises are increasingly deploying computing resources closer to data sources such as IoT devices and smart systems to enable faster processing and real-time decision-making. This trend is particularly important for applications like autonomous systems, industrial automation, and smart cities, where latency and speed are critical.")

The integration of artificial intelligence (AI) with distributed cloud infrastructure is driving market growth. Businesses are adopting distributed cloud models to support AI workloads across multiple locations, allowing better resource utilization and faster insights. Distributed architectures also improve system resilience by reducing dependency on centralized data centers and enabling intelligent processing across networks.

Data sovereignty and regulatory compliance are becoming critical drivers. Governments and organizations are focusing on ensuring that data is stored and processed within specific geographic boundaries. Distributed cloud solutions help meet these requirements by enabling localized data processing while maintaining centralized control, making them highly suitable for regulated industries such as finance and healthcare.

In addition, the growing adoption of multi-cloud and hybrid cloud strategies is supporting the expansion of the global market. Enterprises are increasingly using multiple cloud environments to improve flexibility, reduce vendor lock-in, and optimize costs. Distributed cloud platforms enable seamless integration across different environments, allowing businesses to manage workloads efficiently and scale operations as needed.

Moreover, the market is characterized by rapid technological advancements, increasing enterprise adoption, and strong demand for flexible and scalable cloud solutions. With the continued growth of digital transformation, AI, and connected technologies, distributed cloud is expected to play a critical role in modern IT infrastructure, enabling faster, more secure, and efficient data processing across industries.

Market Dynamics

The growing adoption of edge computing and low-latency applications is driving the market growth, as many modern workloads require data to be processed close to where it is generated rather than being sent to centralized cloud data centers. Applications such as industrial automation, predictive maintenance, autonomous systems, video analytics, and retail intelligence depend on near real-time processing to support rapid decision-making and uninterrupted operations. Distributed cloud platforms extend cloud infrastructure to factories, stores, hospitals, and remote sites, enabling organizations to reduce latency, minimize bandwidth costs, and maintain consistent performance even in environments with intermittent connectivity. As enterprises increasingly deploy mission-critical applications that demand immediate responses and localized processing, demand for distributed cloud solutions continues to rise.

For instance, in April 2026, Google Cloud announced new capabilities for Google Distributed Cloud and highlighted a customer example from Samsung SDS. According to the announcement, Samsung SDS stated that running Gemini locally on Google Distributed Cloud improved its manufacturing operations by enabling real-time predictive maintenance and quality control while avoiding cloud latency. This shows how manufacturers are adopting distributed cloud to support edge-based AI and low-latency analytics directly within production environments, reinforcing edge computing as a key driver of market growth.

Hardware maintenance at edge locations is a significant restraint in the distributed cloud industry, because distributed cloud architectures extend computing infrastructure to factories, retail stores, telecom sites, hospitals, oil fields, and other geographically dispersed environments that often lack dedicated IT personnel. Unlike centralized data centers, where specialized teams can rapidly monitor and service equipment, edge nodes may operate in remote or harsh conditions that expose servers, networking devices, and storage systems to dust, vibration, temperature fluctuations, and power instability. When hardware components fail, organizations may experience delays in diagnosis, repair, or replacement, increasing the risk of downtime for latency-sensitive applications such as industrial automation, video analytics, and point-of-sale systems. These maintenance challenges raise operational complexity and can reduce the perceived attractiveness of large-scale distributed cloud deployments.

The cost implications of maintaining hardware across hundreds or thousands of distributed sites can also be substantial. Organizations may need to stock spare parts, contract local field service providers, implement remote monitoring tools, and design systems with redundancy to minimize disruptions. Coordinating preventive maintenance and software updates across a broad geographic footprint further increases administrative burden and support costs. For enterprises evaluating distributed cloud, these ongoing operational requirements can lengthen payback periods and make alternative deployment models more attractive. As a result, concerns about servicing and managing hardware at edge locations can slow adoption and act as a meaningful constraint on overall market growth.

The expansion of sovereign cloud and national data infrastructure represents a major opportunity in the distributed cloud industry as governments and regulated industries increasingly require sensitive data to remain within specific jurisdictions and under clearly defined operational controls. Countries around the world are introducing stricter regulations related to data residency, privacy, cybersecurity, and digital sovereignty, prompting organizations to seek cloud solutions that combine the scalability and automation of public cloud with localized deployment and governance. Distributed cloud platforms are well-suited to these requirements because they enable cloud services to be deployed within national borders, in dedicated government facilities, or in isolated on-premises environments while maintaining centralized management and consistent security policies. This creates strong demand among public sector agencies, financial institutions, healthcare providers, and critical infrastructure operators that must comply with strict regulatory mandates.

The opportunity extends beyond software to include national investments in secure digital infrastructure, sovereign AI platforms, and domestic cloud ecosystems. Cloud providers can partner with governments, telecom operators, and local data center companies to build country-specific cloud regions and managed environments tailored to regulatory and security requirements. These deployments often involve long-term contracts, high switching costs, and expansion into adjacent services such as cybersecurity, data analytics, and AI. As more nations prioritize digital independence and localized control over critical data and applications, the development of sovereign cloud environments is expected to become a major growth avenue for distributed cloud vendors worldwide.

Market Concentration & Characteristics

The distributed cloud industry is concentrated, with competition dominated by a handful of global hyperscale cloud providers that possess the capital, technical expertise, and geographic footprint required to deliver cloud services across distributed and edge environments. Companies such as AWS, Microsoft Azure, Google Cloud, Oracle, and IBM leverage extensive global infrastructure, advanced security capabilities, and comprehensive platform services to support mission-critical enterprise workloads. Their ability to invest billions of dollars in data centers, edge nodes, and AI-ready infrastructure creates substantial barriers to entry and enables them to maintain strong control over market share. As a result, while specialized vendors and telecom providers participate in niche use cases, the overall market remains highly concentrated around established cloud leaders.

The degree of innovation in the distributed cloud industry is very high. Vendors are rapidly developing technologies that extend public cloud capabilities to on-premises environments, edge locations, and sovereign cloud deployments while maintaining centralized management and consistent security policies. Innovations in Kubernetes orchestration, confidential computing, AI workload distribution, and automated workload placement are enabling organizations to run applications closer to data sources and end users. In addition, advancements in zero-trust security, observability, and infrastructure-as-code are improving scalability and operational efficiency. Continuous product launches and strategic investments by hyperscale providers make innovation one of the most important competitive factors shaping the global market.

Application Insights

The edge computing segment led the market with the largest revenue share of 42.9% in 2025. This dominance is primarily driven by the increasing demand for low-latency data processing, rising deployment of real-time applications, and the rapid expansion of 5G networks. Enterprises are increasingly adopting edge computing to process data closer to the source, reducing network congestion and improving system performance. In addition, the growing use of smart devices, industrial automation, and AI-enabled applications is accelerating the adoption of distributed cloud infrastructure at the edge, enabling faster decision-making and enhanced operational efficiency across industries.

The Internet of Things segment is anticipated to grow at the fastest CAGR during the forecast period, driven by the exponential increase in connected devices and the need for efficient data management across distributed environments. The integration of IoT with distributed cloud enables seamless data collection, processing, and analytics across multiple locations, supporting use cases such as smart cities, connected healthcare, and intelligent manufacturing. Furthermore, the rising demand for real-time insights, improved device connectivity, and scalable cloud solutions is encouraging organizations to adopt distributed cloud models to support IoT ecosystems, thereby fueling segment growth.

Service Insights

The data storage segment accounted for the largest market revenue share in 2025, driven by the rapid growth in data generation across enterprises, increasing adoption of data-intensive applications, and the rising need for scalable and flexible storage solutions. Organizations are leveraging distributed cloud storage to manage large volumes of structured and unstructured data across multiple locations while ensuring high availability and reliability. In addition, the growing demand for real-time data access, backup and disaster recovery solutions, and cost-efficient storage infrastructure is further supporting the dominance of this segment.

The data security segment is expected to register at the fastest CAGR from 2026 to 2033, driven by the increasing concerns over data breaches, rising cyber threats, and strict regulatory requirements for data protection. As organizations adopt distributed cloud environments, the need to secure data across multiple locations becomes critical, leading to higher demand for advanced security solutions such as encryption, identity access management, and threat detection. Furthermore, the growing focus on data privacy, compliance with regional regulations, and the expansion of cloud-based services are key factors accelerating the growth of the data security segment.

Enterprise Size Insights

The large enterprises segment accounted for the largest market revenue share in 2025. This dominance is driven by their strong financial capabilities, high volume of data generation, and early adoption of advanced cloud technologies. Large organizations are increasingly deploying distributed cloud solutions to enhance operational efficiency, support complex workloads, and ensure data compliance across multiple geographic regions. In addition, the need for low-latency processing, strong disaster recovery, and secure data management is further encouraging large enterprises to invest heavily in distributed cloud infrastructure.

The SMEs segment is expected to register at the fastest CAGR from 2026 to 2033, driven by the growing need for cost-effective and scalable cloud solutions. Small and medium-sized enterprises are increasingly adopting distributed cloud models to improve business agility, reduce IT infrastructure costs, and access advanced technologies such as AI and analytics. Furthermore, the rising availability of pay-as-you-go pricing models, increasing digital transformation initiatives, and the need for enhanced data security and flexibility are key factors supporting the rapid growth of this segment.

End-use Insights

The BFSI segment accounted for the largest market revenue share in 2025, driven by the increasing need for secure and compliant data management, rising adoption of digital banking services, and the growing volume of real-time financial transactions. Financial institutions are leveraging distributed cloud solutions to enhance data processing speed, improve customer experience, and ensure regulatory compliance across different regions. In addition, the rising threat of cyberattacks, demand for fraud detection systems, and the need for high availability and disaster recovery capabilities are further accelerating the adoption of distributed cloud in the BFSI sector.

The manufacturing segment is anticipated to register at the fastest CAGR during the forecast period. This growth is driven by the rapid adoption of Industry 4.0 technologies, increasing use of IoT-enabled devices, and the growing need for real-time data analytics on production floors. Distributed cloud enables manufacturers to process data closer to machinery and equipment, improving operational efficiency and reducing downtime. Furthermore, the rising demand for predictive maintenance, automation, and smart factory solutions, along with the need for low-latency connectivity and scalable infrastructure, is fueling the growth of distributed cloud adoption in the manufacturing sector.

Regional Insights

North America dominated the global distributed cloud market with the largest revenue share of 36.9% in 2025. This dominance is primarily driven by the strong presence of leading cloud service providers such as Amazon Web Services, Microsoft, and Google Cloud, along with high adoption of advanced technologies across enterprises. The region benefits from well-established IT infrastructure, early adoption of edge computing, and increasing investments in 5G networks and AI-driven applications. In addition, the growing demand for low-latency services, strong focus on data security, and strict regulatory frameworks are encouraging organizations to adopt distributed cloud solutions, thereby supporting market growth in North America.

U.S. Distributed Cloud Market Trends

The distributed cloud market in the U.S. accounted for the largest market revenue share in North America in 2025. This growth is driven by rapid digital transformation across industries, increasing deployment of edge computing solutions, and rising demand for real-time data processing. The U.S. market is supported by the country’s strong ecosystem of technology providers, high cloud adoption rates, and continuous investments in next-generation technologies such as AI, IoT, and 5G. Furthermore, the presence of large enterprises, increasing cybersecurity concerns, and strict data compliance requirements are accelerating the adoption of distributed cloud solutions across sectors in the U.S., further driving the market growth in the U.S.

Asia Pacific Distributed Cloud Market Trends

The distributed cloud market in the Asia Pacific is expected to grow at the fastest CAGR during the forecast period. This growth is driven by the rapid expansion of digital economies, increasing internet penetration, and strong government initiatives supporting cloud adoption across emerging markets. Countries across the region are investing heavily in smart city projects and digital infrastructure, which is accelerating the deployment of distributed cloud solutions. In addition, the rising number of small and medium enterprises adopting cloud-based platforms, growing e-commerce activities, and increasing demand for localized data processing to support diverse and geographically dispersed populations are key factors fueling market growth in the Asia Pacific.

The China distributed cloud market is projected to grow significantly during the forecast period. This growth is primarily driven by the country’s strong push toward domestic cloud ecosystem development and increasing focus on data localization policies. The expansion of large-scale industrial digitalization, particularly in sectors such as manufacturing and logistics, is encouraging the adoption of distributed cloud to support real-time operations. Furthermore, the presence of major domestic cloud providers such as Alibaba Cloud, Huawei Cloud, and Tencent Cloud, along with increasing investments in advanced computing infrastructure and national digital transformation strategies, is significantly contributing to market growth in China.

The distributed cloud market in India is expected to grow at a significant CAGR during the forecast period. The India market is being driven by rapid digital transformation, expanding 5G infrastructure, and strong government initiatives such as Digital India that are accelerating cloud adoption across industries. Increasing deployment of AI, IoT, and data-intensive applications in sectors such as banking, healthcare, manufacturing, and e-commerce is further strengthening the India market, as organizations seek low-latency, scalable, and locally compliant cloud solutions.

Europe Distributed Cloud Market Trends

The distributed cloud market in Europe is anticipated to grow at a steady CAGR from 2026 to 2033, driven by the region’s strong focus on data privacy frameworks such as General Data Protection Regulation and increasing adoption of sovereign cloud strategies. Enterprises in Europe are prioritizing distributed cloud to maintain greater control over sensitive data while ensuring interoperability across borders, which is contributing to the market growth. In addition, the rising focus on green and energy-efficient data infrastructure, along with collaborative initiatives to build regional cloud ecosystems, is supporting the steady expansion of distributed cloud adoption across Europe, further accelerating the Europe market.

The UK distributed cloud market is driven by the country’s accelerating shift toward cloud-native development and increasing demand for flexible IT architectures across industries. Organizations in the UK are leveraging distributed cloud to support remote and hybrid work environments, improve application resilience, and enable faster deployment of digital services. Furthermore, the growing fintech ecosystem, expansion of digital public services, and rising investments in advanced connectivity infrastructure are key factors contributing to the market growth in the UK

The distributed cloud market in France is expected to grow at a significant CAGR during the forecast period. The France market is being driven by strong government support for digital sovereignty initiatives, increasing investments in AI and edge computing, and strict data protection requirements under GDPR. Rising adoption of cloud solutions across sectors such as manufacturing, healthcare, and financial services is further accelerating the France market, as organizations seek secure, low-latency, and locally compliant infrastructure solutions.

The Italy distributed cloud market is being driven by increasing adoption of Industry 4.0 technologies, growing investments in smart manufacturing, and rising demand for low-latency infrastructure to support AI and IoT applications. Strong emphasis on data sovereignty, GDPR compliance, and digital modernization across sectors such as manufacturing, healthcare, and financial services is further accelerating the Italy market.

The distributed cloud market in Germany is being driven by the country’s strong industrial base, widespread adoption of Industry 4.0, and increasing deployment of edge computing in automotive, manufacturing, and logistics applications. Growing investments in sovereign cloud infrastructure, advanced cybersecurity frameworks, and industrial AI are further accelerating the Germany market, as enterprises seek highly secure, low-latency, and resilient cloud solutions to support mission-critical operations.

Middle East & Africa Distributed Cloud Market Trends

The distributed cloud market in the Middle East and Africa is expected to grow at a significant CAGR during the forecast period. The GCC market is being driven by rapid digital transformation, expanding smart city initiatives, and substantial investments in data centers and 5G infrastructure across countries such as Saudi Arabia, the UAE, and Qatar. Increasing adoption of AI, IoT, and real-time analytics in sectors such as energy, government, healthcare, and financial services is further accelerating the GCC market, while supporting broader distributed cloud adoption across the Middle East and Africa.

Key Distributed Cloud Company Insights

Some prominent players in the distributed cloud industry include Alibaba Group, Amazon Web Services, Inc., Cisco Systems, Inc., F5, Inc., Google, Oracle Corporation, among others.

-

Google is a global technology company and a subsidiary of Alphabet Inc., offering a wide range of digital products and cloud computing services through its Google Cloud division. The company provides Infrastructure-as-a-Service (IaaS), Platform-as-a-Service (PaaS), data analytics, artificial intelligence, and machine learning solutions to enterprises worldwide. In the global market, Google has established a strong presence through its Google Distributed Cloud (GDC) portfolio, which enables organizations to extend Google Cloud infrastructure and AI capabilities to on-premises environments, edge locations, and disconnected (air-gapped) environments.

-

Oracle Corporation is a global technology company specializing in enterprise software, database solutions, and cloud computing services. Through its Oracle Cloud Infrastructure (OCI), the company offers a comprehensive portfolio of Infrastructure-as-a-Service (IaaS), Platform-as-a-Service (PaaS), and Software-as-a-Service (SaaS) solutions, including data management, AI, analytics, and enterprise applications. In the market, Oracle has positioned itself as a key player by delivering a “distributed cloud” model that enables organizations to run more than 150 cloud and AI services across public cloud regions, customer data centers, and edge locations with consistent performance and security. Its offerings include public cloud, dedicated cloud regions, hybrid cloud, and sovereign cloud solutions.

Key Distributed Cloud Companies:

The following key companies have been profiled for this study on the distributed cloud market.

- Alibaba Group

- Amazon Web Services, Inc.

- Cisco Systems, Inc.

- Equinix Inc.

- F5, Inc.

- Hewlett Packard Enterprise Development LP

- Huawei Cloud Computing Technologies Co., Ltd.

- IBM Corporation

- Microsoft Corporation

- Oracle Corporation

- Rackspace Technology

- Salesforce, Inc.

- Tencent Cloud

- Broadcom (VMware)

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weakness

Mature Players: AWS; Microsoft; Google; IBM; Oracle; Alibaba Group; Huawei Cloud

- Build global hyperscale cloud infrastructure combined with distributed edge zones, local zones, and hybrid cloud extensions.

- Develop AI-native distributed cloud orchestration platforms focused on automation, optimization, and predictive workload management.

- Develop partnerships with telecom providers, data center operators, and SaaS ecosystems for edge expansion.

- Strong global presence with massive hyperscale infrastructure and extensive data center networks enabling low-latency distributed cloud delivery.

- Strong vertical integration and compliance-ready solutions tailored for regulated industries.

- Strong enterprise lock-in through integrated platforms, ecosystems, and bundled SaaS/PaaS/IaaS offerings.

- Increasing regulatory scrutiny and concerns around vendor dominance and data sovereignty issues.

- Heavy reliance on enterprise capex cycles leads to demand volatility.

Emerging Players: Koidra Inc.; Intellias; Softweb Solutions Inc.; Synnefa, Inc.; Optimal Labs Limited

- Focus on niche vertical use cases such as IoT, smart agriculture, industrial automation, and telecom edge computing.

- Partner with telecom operators, system integrators, and cloud providers to expand reach.

- Strong specialization enables deep customization for targeted industry problems.

- Ability to innovate faster than legacy vendors in distributed cloud software layers.

- Limited global infrastructure footprint compared to hyperscalers.

- Narrow service portfolios limit the ability to serve full enterprise cloud stacks.

Recent Developments

-

In April 2026, Google expanded its Google Distributed Cloud capabilities at its Cloud Next 2026 event by strengthening support for hybrid and multi-environment deployments, enabling enterprises to run applications and data workloads seamlessly across on-premises data centers, edge locations, and cloud environments. The company also enhanced its distributed cloud ecosystem through new partnerships and integrations (such as expanded data infrastructure and security solutions in air-gapped environments), aimed at supporting AI-driven workloads, sovereign cloud requirements, and application modernization across distributed environments.

-

In April 2026, Oracle Corporation partnered with Amazon Web Services to improve how their cloud platforms work together. This collaboration enables faster and more secure connections between Oracle Cloud Infrastructure (OCI) and AWS, making it easier for businesses to run applications and transfer data across both clouds. It also simplifies multi-cloud operations by reducing the need to manage multiple network providers, helping companies operate more efficiently.

-

In March 2026, Google completed its acquisition of Wiz, a leading cloud and AI security platform, integrating it into Google Cloud to strengthen its security capabilities across multi-cloud environments. Wiz will continue to operate as a separate brand while providing security solutions that help organizations protect applications and data across different cloud platforms. This acquisition enhances Google Cloud’s ability to support secure, scalable, and AI-driven workloads in distributed and multi-cloud environments.

-

In October 2025, International Business Machines Corporation partnered with Bharti Airtel to enhance Airtel Cloud by integrating IBM’s hybrid cloud, AI, and infrastructure capabilities. The collaboration enables enterprises in India to access advanced cloud services, including AI-ready systems and secure infrastructure, while supporting mission-critical workloads across industries such as banking, healthcare, and government.

Distributed Cloud Market Report Scope

Report Attribute

Details

Market size in 2025

USD 5.1 billion

Estimated market size in 2026

USD 6.1 billion

Projected market size by 2033

USD 26.5 billion

Growth rate

CAGR of 23.3% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Application, service, enterprise size, end-use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; Saudi Arabia; South Africa

Key companies profiled

Alibaba Group; Amazon Web Services, Inc.; Cisco Systems, Inc.; Equinix Inc.; F5, Inc.; Google; Hewlett Packard Enterprise Development LP; Huawei Cloud Computing Technologies Co., Ltd.; IBM Corporation; Microsoft Corporation; Oracle Corporation; Rackspace Technology; Salesforce, Inc.; Tencent Cloud; Broadcom (VMware)

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Distributed Cloud Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global distributed cloud market report based on application, service, enterprise size, end-use, and region:

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Edge Computing

-

Content Delivery

-

Internet of Things

-

Others

-

-

Service Outlook (Revenue, USD Million, 2021 - 2033)

-

Data Security

-

Data Storage

-

Networking

-

Others

-

-

Enterprise Size Outlook (Revenue, USD Million, 2021 - 2033)

-

Large Enterprises

-

SMEs

-

-

End-use Outlook (Revenue, USD Million, 2021 - 2033)

-

BFSI

-

Healthcare

-

Retail & E-Commerce

-

Manufacturing

-

IT & Telecom

-

Energy & Utilities

-

Media & Entertainment

-

Government & Defense

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Delivered Customization

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Sovereign cloud and regulatory impact assessment

Review of data residency, privacy, cybersecurity, and sector-specific compliance requirements influencing distributed cloud adoption.

Comparative analysis of sovereign cloud initiatives and government digital infrastructure programs across key regions.

Assessment of how compliance requirements shape deployment and localization strategies.

Clarified regulatory barriers and market-entry requirements.

Supported compliance-focused product positioning.

Identified policy-driven opportunities in government and regulated sectors.

Technology roadmap and innovation trend analysis

Assessment of developments in edge orchestration, Kubernetes management, confidential computing, AI-driven workload optimization, and zero-trust security.

Analysis of product launches, strategic partnerships, and emerging architectural models.

Review of commercialization readiness and customer adoption use cases.

Helped align product strategy with emerging technologies.

Identified innovation areas with strong enterprise demand.

Supported long-term R&D and investment decisions.

Multi-cloud interoperability and integration assessment

Evaluation of how distributed cloud platforms integrate with AWS, Azure, Google Cloud, VMware, Kubernetes, and enterprise security tools.

Analysis of workload portability, observability, and policy management requirements.

Identification of interoperability gaps and integration priorities.

Clarified technical differentiators and integration requirements.

Supported roadmap decisions for open and hybrid architectures.

Reduced barriers to enterprise adoption.

Frequently Asked Questions About This Report

The global distributed cloud market size was valued at USD 5.1 billion in 2025 and is estimated at USD 6.1 billion for 2026.

The global distributed cloud market is expected to grow at a CAGR of 23.3% from 2026 to 2033, reaching USD 26.5 billion.

Key factors include rising demand for low-latency computing, increasing adoption of edge computing, rapid rollout of 5G networks, and growing need for data sovereignty and regulatory compliance.

The edge computing led with a 42.9% revenue share in 2025, while Internet of Things is the fastest-growing application.

Data storage held the largest revenue share in 2025, while data security is the fastest-growing service.

BFSI held the largest share (over 22%) in 2025, while manufacturing is the fastest-growing segment.

Large enterprises held the largest revenue share in 2025, while SMEs is the fastest-growing enterprise.

Key players include Alibaba Group; Amazon Web Services, Inc.; Cisco Systems, Inc.; Equinix Inc.; F5, Inc.; Google; Hewlett Packard Enterprise Development LP; Huawei Cloud Computing Technologies Co., Ltd.; IBM Corporation; Microsoft Corporation; Oracle Corporation; Rackspace Technology; Salesforce, Inc.; Tencent Cloud; VMware, Inc.

North America dominated with a 36.9% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

About the Author(s)

IT Services & Applications Research Team

Technology · IT Services & ApplicationsThis report was authored by the it services & applications research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the it services & applications segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.