- Home

- »

- Communications Infrastructure

- »

-

Edge Data Center Market Size And Share Report, 2026-2033GVR Report cover

![Edge Data Center Market (2026 - 2033)Report]()

Edge Data Center Market (2026 - 2033)

Size, Share & Trends Analysis Report By Component (Solution, Service), By Facility Size (Small & Medium, Large), By End Use (BFSI, Government, Healthcare And Lifesciences), By Region, And Segment Forecasts

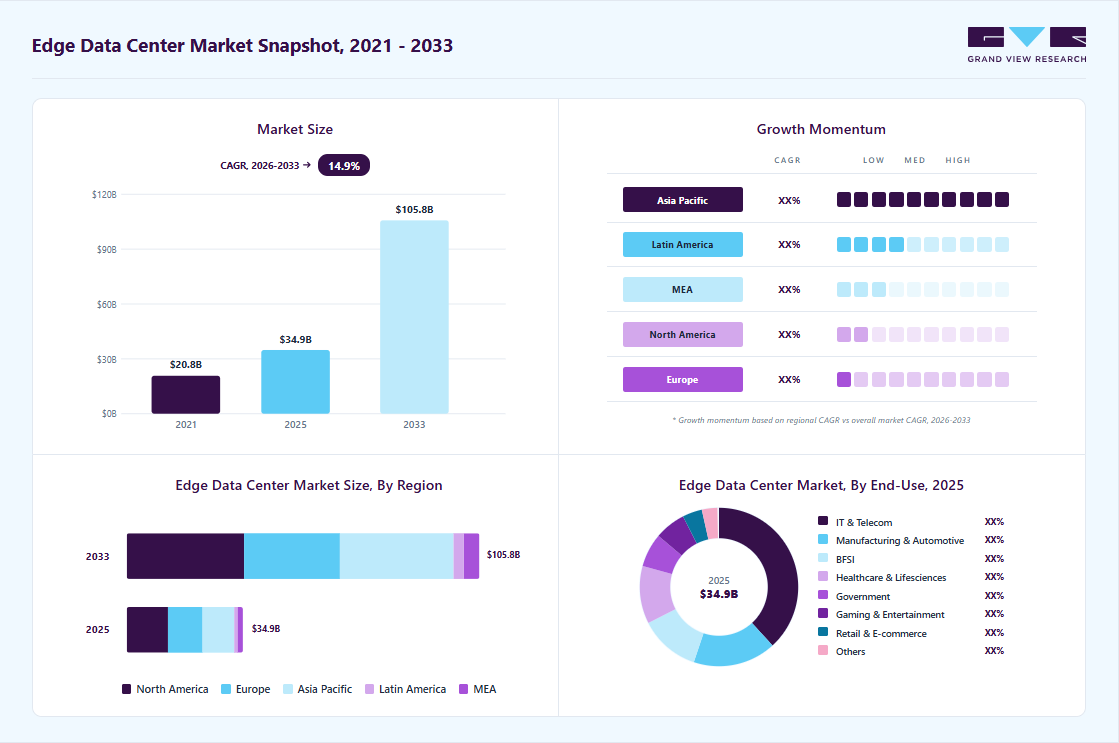

Market Size, 2025

$34.8BMarket Estimate, 2026

$40.0BMarket Forecast, 2033

$105.8BCAGR, 2026–2033

14.9%Edge Data Center Market Summary

The global edge data center market size was valued at USD 34.8 billion in 2025 and is projected to grow from USD 40.0 billion in 2026 to USD 105.8 billion by 2033, at a CAGR of 14.9% from 2026 to 2033. The market in North America dominated with a revenue share of 35.5% in 2025. The growth is attributed to the rising adoption of emerging technologies such as the Internet of Things (IoT), big data, artificial intelligence, cloud computing, streaming services, and 5G across various industries, which generate massive volumes of network data and place increasing performance and computing demands on data centers.

Key Market Trends & Insights

- By component: Solution segment held the largest market share of 87.0% in 2025.

- By facility size: Large facility segment held the largest market share in 2025.

- By end use: IT & telecom segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: North America (35.5% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 34.8 Billion

- Estimated market size in 2026: USD 40.0 Billion

- Projected market size by 2033: USD 105.8 Billion

- CAGR (2026-2033): 14.9%

The ability of edge data centers to provide localized processing and storage resources is a key driver of market growth, as it significantly reduces latency and enhances performance by bringing data computation closer to the source of generation. This proximity enables real-time data analysis and faster response times, which are critical for latency-sensitive applications such as autonomous vehicles, smart manufacturing, telemedicine, and augmented reality. As businesses increasingly rely on time-critical operations and seek to improve user experience, the demand for decentralized infrastructure like edge data centers is accelerating, positioning them as essential components in modern digital ecosystems.")

Edge data centers are increasingly driving market growth by offering robust edge-to-cloud orchestration and enhanced security for distributed, low-latency applications. Key trend is the integration of secure access service edge (SASE) architectures, which combine WAN capabilities and cloud-based security at the network edge. This reduces latency by avoiding long backhauls to centralized data centers, while implementing identity-driven, real-time policy enforcement and micro-segmentation to protect data and applications at their origin. Consequently, as IoT, autonomous systems, and smart-city deployments expand, the demand for localized, optimized edge sites continues to drive investment in platforms that seamlessly manage workloads across edge and core environments.

For instance, in October 2025, OpenAI, Oracle Corporation, and SoftBank Group announced plans to develop five additional AI data center sites in the U.S. as part of the Stargate infrastructure initiative. With these new facilities alongside the flagship site in Abilene and ongoing collaborations with CoreWeave, the project’s total planned capacity is approaching 7 gigawatts, supported by investments exceeding USD 400 billion over the next three years. The expansion places the initiative on track to achieve its broader target of USD 500 billion in funding and 10 gigawatts of capacity by the end of 2025, ahead of its original timeline. While hyperscale facilities provide centralized training and high-performance compute, they simultaneously increase demand for decentralized edge nodes to support low-latency AI inferencing, real-time data processing, and bandwidth optimization closer to end users.

Market Dynamics

AI-optimized edge infrastructure refers to the deployment of high-performance computing resources at distributed edge data centers to support real-time AI workloads. Operators are increasingly integrating GPU-enabled servers to accelerate AI inference tasks, such as image recognition, predictive analytics, and autonomous decision-making, closer to data sources. To manage rising thermal loads from dense compute, advanced cooling technologies like direct-to-chip and liquid cooling are being adopted. High-density power systems ensure stable energy delivery for intensive workloads. This combination enables low-latency processing, reduces data transmission to centralized clouds, and improves efficiency for applications such as smart cities, industrial automation, autonomous vehicles, and 5G-enabled services across distributed environments.

Key players in the market are focusing on launching AI-focused edge data centers to stay ahead. For instance, in April 2026, Prime Group, Microsoft, and Hanwha announced they would build a nationwide network of edge data centers integrated with battery energy storage systems to enable real-time AI inference. The project leverages distributed infrastructure close to users, using existing real estate and energy assets to deliver low-latency, energy-efficient AI computing at scale across the United States.

High power consumption and grid constraints are major challenges for edge data centers, especially as compute density increases, particularly with AI and GPU-driven workloads. Edge facilities often operate in urban or semi-urban locations where local power infrastructure is already stressed or limited. As a result, securing a sufficient and reliable electricity supply becomes difficult, delaying deployment timelines. High-performance servers, cooling systems, and networking equipment significantly increase energy demand, often exceeding the capacity of regional grids to efficiently support them. In some locations, operators may face restrictions on capacity expansion or be required to undertake costly upgrades. These limitations also push the adoption of alternative solutions such as battery storage and renewable integration to stabilize power availability.

Market Concentration & Characteristics

The edge data center market is moderately concentrated, with a mix of global colocation providers, hyperscalers, telecom operators, and specialized edge infrastructure companies competing across regional and local markets. Major players such as Equinix, Digital Realty, EdgeConneX, Amazon Web Services, and Vapor IO hold significant market share due to their extensive infrastructure footprint, strong connectivity ecosystems, and partnerships with telecom and cloud providers. The market is characterized by high capital intensity, rising demand for localized computing, and strong barriers to entry stemming from power availability, network connectivity, real estate acquisition, and operational expertise.

In terms of market characteristics, the industry is highly technology-driven and rapidly evolving, fueled by the growth of 5G, AI inferencing, IoT deployments, autonomous systems, and real-time analytics applications. The market is witnessing rising adoption of modular and prefabricated edge facilities, AI-optimized infrastructure, liquid cooling systems, and sustainable energy solutions. In addition, the industry is characterized by strong telecom integration, distributed deployment models, increasing investments from hyperscalers and private equity firms, and long-term enterprise contracts, creating relatively high customer retention once edge infrastructure is deployed.

Component Insights

The solution segment captured the largest share of 87.0% in the edge data center market in 2025, primarily by delivering comprehensive, software-driven, fully integrated infrastructure tailored for distributed computing environments. Enterprises are increasingly favoring turnkey deployments that unify compute, storage, networking, power, and cooling into pre-engineered modules, enabling rapid on-site scalability, simplified lifecycle management, and more efficient resource utilization than piecemeal or legacy setups. These all-in-one solutions ease the deployment of edge use cases such as AI inference, IoT analytics, and real-time 5G workloads, offering plug-and-play functionality with centralized orchestration across hybrid environments. For instance, in May 2025, Dell Technologies introduced its software‑driven disaggregated infrastructure initiative encompassing PowerProtect All‑Flash and PowerScale storage, PowerStore ransomware detection, and the Dell Automation Platform with NativeEdgeto automate and secure private cloud and edge operations. By decoupling computing, storage, and networking while integrating full-stack software automation, Dell enables organizations to provision edge clusters swiftly, respond to changing workloads, and maintain cyber-resilient operations with minimal manual effort.

The service segment is expected to grow at the fastest CAGR during the forecast period, due to the increasing complexity of deploying and managing distributed edge infrastructure, which is driving demand for specialized services such as installation, integration, remote monitoring, maintenance, and lifecycle management. As enterprises expand their edge deployments to support latency-sensitive applications across multiple locations, they are relying on managed service providers (MSPs) and system integrators to ensure operational continuity, cybersecurity, and regulatory compliance without the need for extensive in-house IT teams.

Facility Size Insights

The large facility segment dominated the market and accounted for the largest revenue share in 2025, as hyperscale campuses and regional edge hubs offer the space, power, and connectivity essential for high-density workloads, AI inference, 5G backhaul, and IoT analytics. These facilities enable operators to consolidate multiple distributed applications, enhance efficiency, and deliver low-latency, secure performance while scaling rapidly to meet enterprise and cloud-provider demands. For instance, in June 2025, Amazon announced a USD 10 billion investment in a new AI and cloud data center campus in North Carolina.

Small and medium-sized facilities are expected to grow at the fastest CAGR during the forecast period, driven by the rapid expansion of edge computing use cases that require localized, low-latency processing in urban, remote, and underserved regions. These facilities offer a flexible, cost-effective alternative to large-scale data centers, enabling faster deployment and easier integration for retail, manufacturing, healthcare, and smart city applications. As enterprises and telecom providers increasingly adopt micro data centers to support 5G rollouts, AI-enabled IoT devices, and content delivery networks closer to end-users, demand for compact yet scalable infrastructure is surging.

End Use Insights

The IT & telecom segment dominated the market and accounted for the largest revenue share in 2025, due to its pivotal role in rolling out low-latency, high-bandwidth infrastructure essential for 5G, AI, and IoT services. Telecom operators and IT firms are deploying edge data centers to offload traffic from core networks, support real-time analytics, and accelerate new service launches. Additionally, the IT and telecom sector is increasingly repurposed by its extensive network infrastructure, such as central offices, cell towers, and exchanges, into localized edge computing hubs to support high-speed data delivery and real-time services. For instance, in May 2025, BT Group announced plans to expand into edge computing by converting existing towers and telephone exchanges into micro edge data centers, leveraging its vast physical footprint to host distributed compute closer to end users.

The manufacturing and automotive segment is expected to grow at the fastest CAGR during the forecast period, due to the increasing adoption of Industry 4.0 technologies such as AI-driven robotics, predictive maintenance, digital twins, and autonomous systems, which require ultra-low latency, high-bandwidth data processing at the edge. Edge data centers enable real-time monitoring, quality control, and operational decision-making directly on factory floors or in connected vehicle environments without relying on distant cloud infrastructure. As manufacturers and automotive OEMs pursue smart factory transformation and vehicle-to-everything (V2X) connectivity, demand for localized, resilient computing infrastructure continues to surge. Moreover, edge computing supports mission-critical safety applications and optimizes supply chain visibility, making it a cornerstone of next-generation industrial and automotive systems.

Regional Insights

The North America edge data center industry accounted for the largest market share of 35.5% in 2025, driven by rapid 5G rollouts, high penetration of cloud and IoT technologies, and robust investments from hyperscalers and telecom providers. The region is witnessing accelerated deployment of regional edge hubs to support real-time applications such as autonomous driving, remote diagnostics, and video streaming, especially in the U.S. and Canada. Additionally, tech giants like Amazon, Microsoft, and Google are expanding their edge infrastructure to reduce latency for AI workloads and content delivery.

U.S. Edge Data Center Market Trends

The edge data center industry in the U.S. is expected to grow significantly at a CAGR of 13.8% from 2026 to 2033, driven by aggressive AI workload deployment, hyperscalers, and cloud providers continuing to build out edge campuses. Additionally, federal initiatives are streamlining approvals for edge facilities. For instance, the U.S. Department of Energy opened 16 federal sites, including Los Alamos, Sandia, and Oak Ridge, for data center development, specifically to accelerate AI infrastructure growth on federal lands.

Europe Edge Data Center Market Trends

The edge data center industry in Europe reflects a surge in modular and prefabricated edge solutions, driven by 5G expansion, IoT adoption, and EU sustainability goals. Companies are backing energy-efficient infrastructure, such as liquid-cooling and district-heating reuse initiatives, in line with the European Green Deal.

The UK edge data center industry is experiencing rapid advancement, driven by massive investments and supportive policy measures that are transforming its digital infrastructure landscape. Additionally, Segro and Pure Data Centres have formed a joint venture in west London to build a fully fitted, hyperscaler-ready edge facility that includes advanced cooling, cabling, and power systems, marking a significant move toward premium edge campuses.

The edge data center industry in Germany is gaining substantial momentum, driven by strategic investments from global tech leaders and stringent national regulations that prioritize data sovereignty and sustainability. For instance, in March 2026, Hochtief, a German construction company, commenced development of a new timber-based edge data center for Yexio in Dorfen. The facility is designed to deliver localized compute capacity and edge services to customers across the Erding region, with operations expected to begin in the third quarter of 2027.

Asia Pacific Edge Data Center Market Trends

The edge data center industry in the Asia Pacific is projected to witness the fastest CAGR of 17.3% from 2026 to 2033, fueled by government-backed infrastructure programs and hyperscaler-led investments. In addition, policymakers are actively incentivizing edge deployments through subsidies for modular micro-data centers, spectrum allocation for private 5G networks, and sustainability mandates part of broader efforts such as China’s “New Infrastructure” agenda and India’s Digital India initiative. Therefore, as digitalization accelerates across APAC from smart cities and e-commerce to industrial AI and remote computing, the combination of strategic investment, regulatory support, and hyperscaler deployments is creating an environment for explosive edge data center growth.

The Japan edge data center industry is gaining strong momentum, driven by government digital transformation and large-scale private investments. Besides, key drivers are the surge in demand for low-latency, high-bandwidth applications, especially 5G, IoT, and real-time AI workloads, fueling deployments of edge infrastructure.

The edge data center industry in China held a substantial market share in 2025, driven by mega investments in AI infrastructure, 5G expansion, and provincial-level support for computing capacity enhancements. In addition, national initiatives, such as the East‑to‑West data computing strategy, are promoting edge deployments in underdeveloped regions to ensure widespread low‑latency connectivity, while sustainability goals, such as Tencent Cloud's commitment to run on 100% renewable energy by 2030, are influencing infrastructure development.

Key Edge Data Center Company Insights

Key players operating in the edge data center industry are 365 Data Centers, Amazon Web Services (AWS), American Tower Corporation, and AtlasEdge Data Centres, among others. Companies are focusing on various strategic initiatives, including new product development, partnerships & collaborations, and agreements to gain a competitive advantage over their rivals. The following are some instances of such initiatives.

-

In November 2025, Cisco Systems Inc. launched its Unified Edge platform to extend data center capabilities to edge environments, enabling real-time applications and AI inferencing at the point of data generation. Positioned as a first-to-market solution, it integrates compute, networking, and storage into a single system supported by a broad partner ecosystem, delivering modular, AI-ready performance. The platform also streamlines large-scale deployments, offers end-to-end observability, and embeds security across all layers to safeguard distributed edge infrastructure.

-

In May 2025, Dell unveiled its AI Factory and expanded PowerEdge/PowerScale hardware to support AI workloads at both core and edge locations. The company also announced partnerships with Google Gemini for on-prem AI deployment and Cohere for secure AI integration, emphasizing decentralized edge compute and sustainable innovation.

-

In February 2025, Veea and Vapor IO launched a strategic collaboration to deliver turnkey AI-as-a-Service and federated learning solutions leveraging Vapor IO’s Zero Gap AI platform and private 5G infrastructure designed for smart manufacturing, municipal projects, and multi-site enterprises.

Key Edge Data Center Companies:

The following key companies have been profiled for this study on the edge data center market.

- 365 Data Centers

- Amazon Web Services (AWS)

- American Tower Corporation

- AtlasEdge Data Centres

- Cisco Systems

- DartPoints

- Dell Inc.

- Digital Realty Trust

- EdgeConneX Inc.

- Equinix, Inc.

- Flexential Corporation

- Fujitsu Limited

- Google LLC

- Hewlett Packard Enterprise Company

- Vapor IO, Inc.

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weakness

Mature Players: Equinix; Digital Realty; Vertiv; Hewlett Packard Enterprise; AWS, Cisco Systems

- Leveraging established hyperscaler, telecom, and enterprise relationships to scale distributed edge deployments

- Expanding modular and prefabricated edge infrastructure portfolios for faster deployment

- Investing heavily in AI-ready edge infrastructure, including liquid cooling, GPU-ready racks, and remote orchestration

- Expanding through telecom partnerships and carrier-neutral interconnection hubs

- Developing modular, prefabricated, and rapidly deployable micro data center solutions.

- Strong global interconnection ecosystems and enterprise customer base

- Deep financial strength enabling large-scale infrastructure investments

- Mature operational expertise in mission-critical data center environments

- High cost structure limits flexibility in low-margin edge deployments

- Legacy infrastructure and complex systems slow down rapid innovation cycles

- Heavy reliance on long-term enterprise contracts reduces agility in fast-moving AI-edge use cases.

Emerging Players: EdgeConneX; Vapor IO; StackPath; NTT Global Data Centers

- Building highly distributed, telecom-integrated edge micro data centers near 5G towers and urban clusters

- Focus on low-latency use cases such as gaming, CDN, autonomous systems, and real-time analytics

- Adopting modular “edge-as-a-service” models with rapid deployment capability

- Partnering with telcos and municipalities for distributed infrastructure access

- Targeting niche high-growth verticals like smart cities and industrial IoT.

- Faster deployment cycles and high flexibility in infrastructure design

- Strong proximity advantage to end users, enabling ultra-low latency performance

- Ability to innovate quickly around specific edge workloads and use cases.

- Limited global scale compared to hyperscalers and colocation giants

- Dependence on telecom partnerships for site access and connectivity

- Higher funding sensitivity and constrained capital for large-scale expansion.

Edge Data Center Market

Report Attribute

Details

Market size in 2025

USD 34.8 billion

Estimated market size in 2026

USD 40.0 billion

Projected market size by 2033

USD 105.8 billion

Growth rate

CAGR of 14.9% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Component, facility size, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East and Africa

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; Kingdom of Saudi Arabia; South Africa

Key companies profiled

365 Data Centers; Amazon Web Services (AWS); American Tower Corporation; AtlasEdge Data Centres; Cisco Systems; DartPoints; Dell Inc.; Digital Realty Trust; EdgeConneX Inc.; Equinix, Inc.; Flexential Corporation; Fujitsu Limited; Google LLC; Hewlett Packard Enterprise Company; Vapor IO, Inc.

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Edge Data Center Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global edge data center market report based on component, facility size, end use, and region.

-

Component Outlook (Revenue, USD Billion, 2021 - 2033)

-

Solution

-

Hardware

-

Software

-

-

Service

-

Professional

-

Managed

-

-

-

Facility Size Outlook (Revenue, USD Billion, 2021 - 2033)

-

Large Facility

-

Small and Medium-Sized Facility

-

-

End Use Outlook (Revenue, USD Billion, 2021 - 2033)

-

IT and Telecom

-

BFSI

-

Healthcare and Lifesciences

-

Manufacturing & Automotive

-

Government

-

Gaming and Entertainment

-

Retail and E-commerce

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Edge data center market opportunity assessment for an infrastructure provider

Assessment of edge data center demand across the Asia Pacific region

Benchmarking of key operators in the region

Evaluation of deployment models, including micro edge, metro edge, and modular prefabricated facilities

Identified high-growth edge infrastructure segments and countries with realistic near-term adoption

Highlighted practical adoption drivers, including latency reduction, bandwidth optimization, and AI inferencing

Identified realistic expansion opportunities in telecom and industrial edge environments

Customized cross-segmentation analysis for the edge data center market by component and end use

Evaluated demand by end-user industries such as telecom, manufacturing, healthcare, retail, logistics, etc.

Assessed infrastructure requirements, including GPU density, liquid cooling, edge networking, and remote management

Mapped edge compute adoption maturity across enterprise and telecom buyers

Identified sectors with the strongest commercial deployment activity

Highlighted use cases with achievable ROI and scalable deployment economics

Supported go-to-market prioritization for edge infrastructure vendors

Regional edge data center expansion and investment opportunity assessment

Analysis of edge infrastructure growth across the Middle East & Latin America regions

Evaluation of government digital infrastructure initiatives and private investment activity

Assessment of regional power availability, connectivity ecosystems, and land constraints

Benchmarking of emerging edge clusters near metro and secondary city markets

Identified practical infrastructure upgrade opportunities for edge operators

Supported positioning around energy efficiency and operational resilience

Highlighted realistic deployment requirements for AI-ready edge facilities

Provided insights into evolving customer requirements for scalable edge infrastructure

Frequently Asked Questions About This Report

Key factors driving the edge data center market growth include the rising adoption of emerging technologies such as the Internet of Things (IoT), big data, artificial intelligence, cloud computing, streaming services, and 5G across various industries, which generate massive volumes of network data and place increasing performance and computing demands on data centers.

The solution segment led with a 87.0% revenue share in 2025, while the service segment is the fastest-growing.

The large facility segment held the largest revenue share in 2025, while the small and medium-sized segment is the fastest-growing.

The IT & telecom segment held the largest revenue share in 2025, while the manufacturing and automotive segment is the fastest-growing.

The global edge data center market size was valued at USD 34.8 billion in 2025 and is estimated at USD 40.0 billion for 2026.

The global edge data center market is expected to grow at a CAGR of 14.9% from 2026 to 2033, reaching USD 105.8 billion by 2033.

North America dominated with a 35.5% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

Key players include 365 Data Centers; Amazon Web Services (AWS); American Tower Corporation; AtlasEdge Data Centres; Cisco Systems; DartPoints; Dell Inc.; Digital Realty Trust; EdgeConneX Inc.; Equinix, Inc.; Flexential Corporation; Fujitsu Limited; Google LLC; Hewlett Packard Enterprise Company; Vapor IO, Inc.

About the Author(s)

Communications Infrastructure Research Team

Technology · Communications InfrastructureThis report was authored by the communications infrastructure research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the communications infrastructure segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.