- Home

- »

- Medical Devices

- »

-

Ejection Fraction Market Size & Share, Industry Report, 2033GVR Report cover

![Ejection Fraction Market Size, Share & Trends Report]()

Ejection Fraction Market (2026 - 2033) Size, Share & Trends Analysis Report By Application (Urology, General Surgery, Gynecology), By Technology (Ultrasound Based, Magnetic Resonance Based, CT Based), By Device, By End Use, By Region, And Segment Forecasts

- Report Summary

- Table of Contents

- Segmentation

- Methodology

- Download FREE Sample

-

Download Sample Report

Download Sample Report

- Buy Now

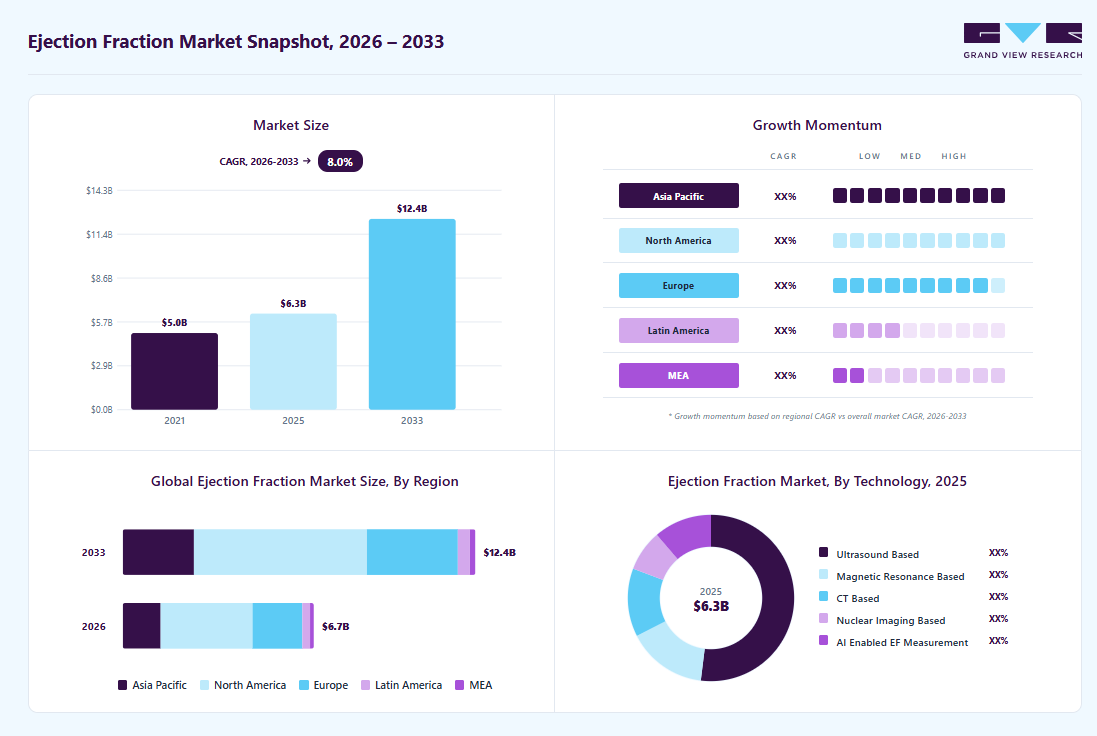

Market Size, 2025

$6.3BMarket Estimate, 2026

$6.7BMarket Forecast, 2033

$12.4BCAGR, 2026–2033

8.0%Ejection Fraction Market Summary

The global ejection fraction market size was estimated at USD 6.3 billion in 2025 and is projected to reach USD 12.4 billion by 2033, growing at a CAGR of 8.0% from 2026 to 2033. The market is driven by the rising prevalence of heart failure and other cardiovascular diseases, which increase the need for regular and precise ejection fraction assessment.

Key Market Trends & Insights

- North America ejection fraction market dominated the global market in 2025 and accounted for the largest revenue share of 48.2%.

- U.S. ejection fraction market is anticipated to register the fastest growth rate during the forecast period.

- By device type, the echocardiography systems segment held the largest revenue share of 41.3% in 2025.

- By technology, the ultrasound based segment held the largest revenue share in 2025.

- By application, the heart failure management segment held the largest revenue share in 2025.

- By end use, the hospitals segment held the largest revenue share in 2025.

Market Size & Forecast

- 2025 Market Size: USD 6.3 Billion

- 2033 Projected Market Size: USD 12.4 Billion

- CAGR (2026-2033): 8.0%

- North America: Largest market in 2025

- Asia Pacific: Fastest growing market

Advances in non-invasive imaging technologies, such as AI-enabled echocardiography and cardiac MRI, are improving measurement accuracy and workflow efficiency. Growing adoption of remote monitoring solutions and integration with hospital information systems are enabling continuous patient management and early detection of cardiac deterioration, further developing the use of EF monitoring devices.")

Market Drivers

Rising Burden of Heart Failure and Cardiomyopathy Driving EF Monitoring Demand

The global rise in heart failure, cardiomyopathy, and related cardiovascular disorders is significantly increasing the demand for accurate and repeatable ejection fraction (EF) monitoring. EF remains a cornerstone metric for evaluating left ventricular function and is critical for identifying disease severity, guiding treatment selection, and monitoring progression over time. As cardiovascular disease prevalence increases across aging populations and high-risk cohorts, EF assessment has become an essential component of both acute and chronic cardiac care pathways. According to the American Heart Association, ejection fraction is a key determinant in diagnosing heart failure phenotypes, stratifying patient risk, and determining eligibility for pharmacological, device-based, or interventional therapies. EF thresholds are directly referenced in major clinical guidelines, making routine and reliable EF assessment indispensable across hospitals, outpatient cardiology clinics, and increasingly, primary care settings.

Clinical Thresholds and Interpretation of Ejection Fraction Values

Ejection Fraction (EF) values are clinically categorized into defined ranges that correlate with cardiac function and disease severity. These thresholds enable standardized diagnosis and consistent decision-making across care settings. A normal EF typically ranges from 55% to 70%, indicating preserved systolic function. EF values between 41% and 49% are considered mildly reduced and may signal early-stage heart disease or subclinical dysfunction. An EF below 40% is commonly associated with heart failure with reduced ejection fraction (HFrEF) and cardiomyopathy, while abnormally high EF values (above ~75%) can be indicative of hypertrophic cardiomyopathy or restrictive pathologies.

Role of EF in Diagnosis, Prognosis, and Therapy Optimization

EF plays a central role in determining prognosis and guiding therapy selection, including the initiation of guideline-directed medical therapy, device implantation, or interventional procedures. Serial EF measurements are also critical for evaluating treatment response and disease progression, reinforcing the need for reliable, repeatable monitoring technologies.

Innovations and Advancements in Non-Invasive Imaging Technologies

Innovations in non-invasive imaging, including AI-assisted echocardiography, 3D echocardiography, and cardiac MRI, are enhancing the precision and reliability of ejection fraction measurements. These technologies reduce operator dependency, provide faster results, and support more informed clinical decision making, driving wider adoption among healthcare providers. Continuous improvements in software algorithms and automated analysis tools are lowering error rates and enabling more standardized assessments across clinical settings.In April 2024, Eko Health received FDA clearance for its Low EF AI, developed with Mayo Clinic, enabling the detection of low ejection fraction in 15 seconds during routine physical exams using an AI-enabled stethoscope. Clinical validation demonstrated high accuracy (AUROC up to 0.98 in specific cohorts), enabling rapid identification of heart failure and cardiomyopathy and improving early intervention and access to care.

“The ability to identify a hidden, potentially life-threatening heart condition using a tool that primary care and subspecialist clinicians are familiar with — the stethoscope — can help us prevent hospitalizations and adverse events,”

-Dr. Chair of the Department of Cardiovascular Medicine at Mayo Clinic in Rochester

Integration of EF Monitoring into Routine and Point-of-Care Clinical Practice

Integration of EF monitoring with hospital information systems and telemedicine platforms is enabling continuous patient management. Remote monitoring allows early detection of cardiac deterioration, reduces hospital readmissions, and improves patient outcomes, encouraging clinicians and healthcare institutions to adopt EF monitoring solutions more broadly.In December 2025, Heart Failure Solutions completed the first inhuman use of its PeriCut system, a minimally invasive device designed to treat patients with heart failure with preserved ejection fraction (HFpEF). The FDA-approved early feasibility study aims to evaluate safety, hemodynamic improvements, and functional outcomes, offering a novel option alongside guideline-directed medical therapy for this high need patient population.

Funding and Strategic Investments in EF Monitoring and Heart Failure Technologies

Date

Company

Description

In September 2025

Axon Therapies

Secured USD 32M Series A financing to advance minimally invasive therapies for heart failure including HFpEF and HFrEF (impacting monitoring & treatment).

In July 2025

Ultromics

Raised USD 55M Series C to scale its FDA-cleared AI echo platform that detects heart failure (including HFpEF) earlier and more accurately.

In December 2025

Ultromics (Go Red for Women Venture Fund)

Strategic investment by the American Heart Association’s Go Red for Women Venture Fund to promote use of Ultromics’ EchoGo Heart Failure AI tool, particularly for detecting HFpEF an EF-related diagnostic challenge.

In June 2024

Eko Health Inc.

Raised USD 41 M Series D to expand AI-driven heart and lung disease detection, including algorithms for low ejection fraction detection in routine exams. This enhances early EF screening tools using AI.

Market Concentration & Characteristics

The ejection fraction monitoring market exhibits a high degree of technological innovation, driven by the integration of AI-enabled imaging, automated analysis, and cloud-based data platforms into cardiac care workflows. Devices are evolving toward faster, more accurate, and standardized EF assessments, with enhanced interoperability across hospital systems and remote monitoring solutions. In July 2024, the FDA granted breakthrough device designation to Restore Medical’s ContraBand system for treating patients with heart failure with reduced ejection fraction (HFrEF) who remain symptomatic despite guideline-directed therapy.

Mergers and acquisitions activity is moderate, primarily focused on startups offering differentiated technologies such as AI-assisted echocardiography, portable EF monitors, and telecardiology platforms. Strategic acquisitions expand product portfolios, accelerate development cycles, and provide access to new customer segments in hospital and outpatient settings, supporting long-term revenue growth.

The regulatory landscape imposes stringent oversight, with rigorous device classification, safety protocols, and compliance standards for digital and software components. Approval pathways necessitate multi-phase clinical validation, post-market surveillance, and adherence to interoperability and cybersecurity requirements. Emerging frameworks for AI-enabled EF monitoring tools further complicate compliance, requiring firms to balance innovation with risk mitigation and documentation carefully.

Service expansion is moderate, as vendors increasingly provide value-added solutions such as cloud based analytics, predictive maintenance, remote monitoring support, and integration with electronic health records. These offerings enhance operational efficiency, optimize patient management, and support adoption in smaller hospitals, outpatient clinics, and telemedicine networks.

Regional expansion is significant, with companies actively targeting underserved markets across Asia Pacific, the Middle East, and Latin America. Approaches include localized training programs, regulatory partnerships, and in-market technical support to facilitate adoption, reduce barriers to entry, and accelerate global penetration of EF monitoring solutions.

Device Type Insights

The echocardiography systems segment accounted for the largest revenue share of 41.3% in 2025. This dominance is attributed to the increasing incidence of heart failure and the key player's technologically advanced product launches. For instance, in August 2025, GE HealthCare recently introduced the Vivid Pioneer, its most advanced ultra-premium cardiovascular ultrasound platform to date, developed to elevate cardiac imaging performance and clinical efficiency. The system has been fully redesigned to deliver exceptional image quality across 2D, 4D, and color flow modalities, while integrating intelligent automation to simplify workflows and support more confident diagnostic decision making. With both CE Mark approval and U.S. FDA 510(k) clearance secured, the Vivid Pioneer is positioned for broad clinical adoption in advanced echocardiography and cardiovascular care settings.

The cardiac CT systems segment is anticipated to grow at the fastest CAGR over the forecast period, driven by the rising incidence of heart failure and the launch of technologically advanced products by key players. For instance, in March 2025, GE HealthCare introduced the Revolution Vibe CT system, an advanced cardiac imaging platform designed to deliver consistent, high-quality heart images in a single heartbeat, even in complex cases such as patients with atrial fibrillation or significant coronary calcification. The system integrated multiple AI-driven technologies, including ECG-less cardiac imaging, TrueFidelity deep-learning reconstruction, SnapShot Freeze motion correction, and automated workflow tools to support faster, more precise diagnoses. Combining high-performance imaging with intelligent automation, the Revolution Vibe improved patient comfort while helping clinicians achieve greater efficiency and diagnostic confidence in cardiac CT examinations.

Technology Insights

The ultrasound based segment dominated the market with the largest revenue share of 52.0% in 2025. Ultrasound based EF measurement is rapidly shifting toward automated, point-of-care use through built in auto EF software in both handheld and cart-based systems, enabling faster cardiac assessment beyond traditional echo labs. According to a ResearchGate article published in July 2025, a real-world clinical evaluation involving 150 emergency department patients found that automated EF outputs from a mid-range cart-based ultrasound system and a handheld ultrasound device operated by novice users were comparable. The auto EF software successfully generated EF values in about 73% of cases on the cart-based system and around 52% on the handheld device, with a strong agreement between platforms. The study revealed that modern ultrasound systems reliably deliver EF measurements in routine clinical environments, supporting wider adoption of ultrasound-based EF assessment across acute and outpatient care.

The endoscopic robotic segment is anticipated to grow at the fastest CAGR over the forecast period. Artificial intelligence is transforming how ejection fraction is quantified by enabling fully automated, accurate measurements that rival standard imaging techniques. According to the MDPI article published in July 2025, a comparative study evaluating an AI-assisted handheld ultrasound device equipped with an autoEF algorithm, where EF values obtained by the AI tool closely matched those from cardiac magnetic resonance imaging, the gold standard, with a median of 55 % versus 57 % and a robust correlation. This establishes that AI-enabled EF measurement can produce highly reliable results rapidly at the bedside, supporting clinicians in making faster and more objective cardiac assessments.

Application Insights

The heart failure management segment dominated the market with the largest revenue share of 37.1% in 2025. Heart failure management has increasingly shifted toward precision care, combining guideline-directed medical therapy with advanced pharmacological and device interventions to improve patient outcomes and reduce hospitalizations. Traditional approaches, such as optimizing beta-blockers, ACE inhibitors, mineralocorticoid receptor antagonists, and sodium glucose cotransporter 2 (SGLT2) inhibitors, remain foundational, but recent advances are expanding therapeutic options for patients across the ejection fraction spectrum. For instance, in July 2025, the U.S. FDA approved finerenone (Kerendia) for patients with heart failure and left ventricular ejection fraction ≥ 40 %, based on the FINEARTS-HF trial, which showed a 16 % reduction in the risk of cardiovascular death and total heart failure events compared with placebo. This approval introduces a new avenue for managing heart failure with preserved or mildly reduced EF as part of a comprehensive care strategy that integrates drug therapy with real-time monitoring and personalized patient support.

The oncology cardiac monitoring segment is anticipated to grow at the fastest CAGR over the forecast period. Oncology cardiac monitoring is a critical part of cancer care because several anticancer treatments can damage heart function, particularly by reducing left ventricular ejection fraction (LVEF). Modern cardio-oncology focuses on routine monitoring, especially through transthoracic echocardiography, to detect early cardiac changes and enable timely protective interventions. According to the NCBI article published in June 2025, a feasibility trial involving 190 women with HER2-positive breast cancer followed a tailored cardiac monitoring approach using imaging every six months along with symptom-triggered scans over nearly 18 months. Only 0.5% of patients developed asymptomatic cardiac dysfunction, and 0 cases of symptomatic heart failure or cardiovascular death were reported, highlighting the effectiveness of personalized, ultrasound-based cardiac surveillance in oncology care.

End Use Insights

The hospitals segment dominated the market, accounting for 58.8% of revenue in 2025. Hospitals are the main users of advanced cardiac imaging and ejection fraction (EF) assessment tools, supporting acute care and complex heart evaluations. Cardiology departments and emergency units routinely use echocardiography, cardiac CT, and monitoring systems to measure EF and guide treatment decisions. For instance, in December 2025, the American Heart Association invested in an AI-driven echocardiography platform to improve the detection of heart failure with preserved EF (HFpEF) in hospital settings, primarily to address diagnostic challenges and reduce missed cases in women. This initiative supports AI models that analyze routine echo images more accurately and quickly than traditional interpretation, assisting cardiologists identify subtle cardiac dysfunction earlier and improve patient outcomes. Such hospital deployments illustrate how advanced imaging enhanced with AI strengthens diagnostic precision and workflow efficiency in busy clinical environments.

The ambulatory care centers segment is anticipated to grow at the fastest CAGR over the forecast period. Ambulatory care centers are increasingly incorporating point-of-care cardiac imaging and ejection fraction (EF) assessment into routine outpatient workflows to improve early detection and ongoing management of heart failure. With the shift toward value-based care and reduced hospital admissions, these centers are adopting portable ultrasound systems and simplified EF measurement tools that allow rapid cardiac evaluation during follow-up visits. This trend enables quicker treatment adjustments, improves ongoing care for chronic heart patients, and limits hospital imaging referrals, leading to greater efficiency and convenience in outpatient cardiac management.

Table 3: Top 5 U.S. States by Number of Ambulatory Surgical Centers (ASCs) in 2025

Sr

State

Number of ASCs

1

California

896

2

Florida

517

3

Texas

497

4

Georgia

423

5

Maryland

347

Source: Ambulatory Surgery Center Association & GVR

Regional Insights

North America dominated the ejection fraction market, accounting for 48.2% of revenue in 2025, driven by rising heart failure incidence, technological advancements, and government initiatives. According to AHA article published in May 2025, with more than 6 million population currently living with the condition. Every year, over one million new cases are diagnosed among adults aged 55 years and older, reflecting the strong link between aging and declining cardiac function. Ejection fraction (EF) plays a key role in diagnosing and classifying heart failure; the rising incidence directly increases the demand for EF assessment through echocardiography and other cardiac imaging technologies. Early detection and continuous monitoring of EF enable better disease management, improved treatment decisions, and reduced risk of hospitalization, reinforcing the importance of EF focused diagnostics in the region.

U.S. Ejection Fraction Market Trends

The U.S. dominated the ejection fraction market in the North America region in 2025, driven by the rising heart failure prevalence and the technologically advanced product launches by the key players. For instance, in July 2025, Tempus ECG-Low EF (Tempus AI, Inc.) received U.S. FDA 510(k) clearance for AI software that analyzes resting 12-lead ECGs to identify signs associated with low left ventricular ejection fraction (LVEF ≤40%), enabling clinicians flag patients at risk of reduced EF.

"With Tempus ECG-Low EF, we’re adding another powerful tool to the hands of clinicians to help them identify patients at risk for serious cardiovascular conditions much earlier in their care journey. Detection of LVEF is essential for undiagnosed patients, and this technology enables us to deliver that capability at scale to transform patient care. The addition of a second FDA-cleared Tempus ECG-AI solution reflects our continued commitment to advancing AI-driven cardiology."

- Brandon Fornwalt, MD, PhD, Senior Vice President of Cardiology at Tempus.

Europe Ejection Fraction Market Trends

The ejection fraction market in Europe is expected to grow significantly over the forecast period, driven by government initiatives to improve cardiac care, high adoption of technologically advanced imaging systems, and increasing prevalence of heart failure and related cardiovascular disorders. Cross-border collaborations and investment in healthcare infrastructure are also supporting market growth.

The ejection fraction industry in the UK is expected to grow significantly during the forecast period,supported bythe rising incidence of heart failure and the technologically advanced product launches. According to the NCBI article published in September 2025, in the UK, heart failure represents a significant and growing cardiovascular burden, with over one million people currently living with the condition and close to 200,000 new cases diagnosed each year. This growing patient population underscores the need for accurate, routine assessment of ejection fraction (EF).

The ejection fraction industry in Germany is expected to grow significantly during the forecast period, driven by the rising incidence of heart failure and the technologically advanced product launches. According to a Cardiovascular Medicine GmbH article published in February 2026, heart failure remains a significant and growing public health concern in Germany, especially among older adults. There are approximately 130,000 new cases of symptomatic heart failure diagnosed each year, reflecting a high incidence rate within the population. This ongoing burden fuels market growth.

Asia Pacific Ejection Fraction Market Trends

The Asia Pacific ejection fraction industry is expected to register the fastest growth rate over the forecast period, driven by increasing healthcare access, rising cardiovascular disease incidence, and the rapid adoption of advanced imaging technologies in hospitals and cardiac specialty centers. Growing awareness and affordability of EF monitoring solutions are accelerating market penetration.

China ejection fraction market is anticipated to register considerable growth during the forecast period. This is driven by government healthcare initiatives, expanding hospital networks, and rising heart failure disease burden. According to the NCBI article published in October 2025, China recorded an estimated 14.3 million people living with heart failure in 2023, reflecting a dramatic rise of over 208.4% compared to levels three decades ago. This sharp increase highlights the expanding cardiovascular disease burden in the country, driven by population aging, urbanization, and lifestyle-related risk factors. The growing number of heart failure patients significantly fuels the need for accurate diagnosis and continuous monitoring, particularly through ejection fraction (EF) assessment, which is essential for classifying heart failure type, guiding therapy, and improving long-term clinical outcomes across China’s healthcare system.

The ejection fraction industry in India isexpected to grow significantly over the forecast period, driven by the rising incidence of heart failure and the launch of technologically advanced products. According to the Research Gate article published in August 2025, heart failure represents a growing cardiovascular concern, with an estimated prevalence of around 1% of the total population, translating to approximately 8-10 million individuals living with the condition. Growing cases of hypertension, diabetes, coronary artery disease, and an aging population are expanding the heart failure patient pool. This is increasing demand for ejection fraction (EF) assessment, making echocardiography and advanced cardiac imaging essential tools for diagnosis and treatment across hospitals and cardiac care centers.

Latin America Ejection Fraction Market Trends

The Latin America ejection fraction industry is expected to witness considerable growth over the forecast period. This is attributed to improvements in healthcare infrastructure, increased availability of advanced imaging technologies, and the rising incidence of heart failure and other cardiac conditions. Strategic partnerships and increasing investment and funding are enhancing market access.

Ejection fraction industry in Brazil is anticipated to register considerable growth during the forecast period with rising hospital investments in cardiac care, adoption of non-invasive EF monitoring devices, growing awareness of cardiovascular disease management among patients and clinicians and increasing incidence of heart failure. According to the Arq. Bras. Cardiol. article published in July 2025, the heart failure poses a significant and age-dependent health burden, with prevalence estimated at about 1.1% among adults aged 18 years and older, rising sharply to approximately 3.3% in individuals over 60 years of age. This strong increase with aging reflects the growing impact of cardiovascular risk factors and the country's longer life expectancy, thus boosting market growth.

Middle East And Africa Ejection Fraction Market Trends

Ejection fraction market in MEA is anticipated to grow significantly over the forecast period, driven by rising healthcare expenditure, the expansion of cardiac specialty hospitals, and the growing adoption of advanced EF monitoring technologies in urban centers.

South Africa ejection fraction industry is anticipated to register considerable growth during the forecast period asthe country focuses on upgrading cardiac care infrastructure, integrating AI-assisted imaging systems, and rising heart failure incidence drives the growth of the market. According to the South African Family Practice article published in June 2025, the burden of heart failure is particularly severe within the broader context, where chronic heart failure carries the highest fatality rate globally at around 34%, nearly double the worldwide average of 16.5%. This elevated mortality reflects late diagnosis, limited access to specialized cardiac care, and a high prevalence of untreated cardiovascular risk factors boost the growth of the market.

Key Ejection Fraction Company Insights

Key participants in the ejection fraction industry are focusing on devising innovative business growth strategies, such as expanding their product portfolios, partnerships and collaborations, mergers and acquisitions, and expanding their business footprints.

Key Ejection Fraction Companies:

The following key companies have been profiled for this study on the ejection fraction market.

- GE HealthCare

- Koninklijke Philips

- Siemens Healthineers

- Canon Medical Systems

- Fujifilm Healthcare

- Mindray Medical International Ltd.

- Samsung Medison Co., Ltd.

- Esaote SPA

- Butterfly Network, Inc.

- Terason Division Teratech Corporation.

- iCardio.ai

Recent Developments

-

In November 2025, Vasa Therapeutics received FDA Fast Track designation for VS-041, an investigational oral therapy targeting heart failure with preserved ejection fraction (HFpEF), aiming to address fibroinflammation in high-risk patients identified by serum endotrophin. The designation allows for expedited development, frequent FDA communication, and potential priority review, supporting precision medicine approaches in HFpEF management.

-

In July 2025, the U.S. FDA approved KERENDIA (finerenone) for adults with heart failure and left ventricular ejection fraction ≥40% following Priority Review, expanding treatment options for ~3.7 million high-risk patients. The approval is based on Phase III FINEARTS-HF trial results showing a 16% reduction in cardiovascular death and total heart failure events when added to standard care.

-

In June 2025, Ancora Heart enrolled 250 patients in the CORCINCH-HF trial to evaluate the AccuCinch Transcatheter Left Ventricular Restoration System for HFrEF, with six month data supporting FDA approval and total enrollment planned for 400.

Ejection Fraction Market Report Scope

Report Attribute

Details

Market size value in 2026

USD 6.7 billion

Revenue forecast in 2033

USD 12.4 billion

Growth rate

CAGR of 8.0% from 2026 to 2033

Actual data

2021 - 2025

Forecast data

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Device type, technology, application, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; Italy; Spain; Denmark; Sweden; Norway; China; Japan; India; Australia; South Korea; Thailand; Brazil; Argentina; South Africa; Saudi Arabia; UAE; Kuwait

Key companies profiled

GE HealthCare; Koninklijke Philips; Siemens Healthineers; Canon Medical Systems; Fujifilm Healthcare; Mindray Medical International Ltd.; Samsung Medison Co., Ltd.; Esaote SPA; Butterfly Network, Inc.; Terason Division Teratech Corporation;

iCardio.ai.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Ejection Fraction Market Report Segmentation

This report forecasts revenue growth and provides, at the global, regional, and country levels, an analysis of the latest trends in each of the sub-segments from 2021 to 2033. For this report, Grand View Research has segmented the global ejection fraction market report based on device type, technology, application, and region:

-

Device Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Echocardiography Systems

-

2D echocardiography

-

3D/4D echocardiography

-

Doppler imaging systems

-

-

Cardiac MRI Systems

-

Cardiac CT Systems

-

Nuclear Imaging Systems (MUGA scanners)

-

Implantable Cardiac Devices (ICD, CRT, VAD)

-

Cardiac Monitoring Devices & Wearables

-

-

Technology Outlook (Revenue, USD Million, 2021 - 2033)

-

Ultrasound Based

-

Magnetic Resonance Based

-

CT Based

-

Nuclear Imaging Based

-

AI Enabled EF Measurement

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Heart Failure Management

-

Cardiomyopathy & Ischemic Heart Disease

-

Valvular Heart Disease

-

Oncology Cardiac Monitoring

-

Surgical & Critical Care Assessment

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Hospitals

-

Ambulatory Care Centers

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

Japan

-

China

-

India

-

Australia

-

South Korea

-

Thailand

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Frequently Asked Questions About This Report

The global ejection fraction market size was estimated at USD 6.3 billion in 2025 and is expected to reach USD 6.7 billion in 2026.

The global ejection fraction market is expected to grow at a compound annual growth rate of 8.0% from 2026 to 2033 to reach USD 12.4 billion by 2033.

North America dominated the ejection fraction market, accounting for 48.2% of revenue in 2025, driven by rising heart failure incidence, technological advancements, and government initiatives.

Some key players operating in the ejection fraction market include GE HealthCare; Koninklijke Philips; Siemens Healthineers; Canon Medical Systems; Fujifilm Healthcare; Mindray Medical International Ltd.; Samsung Medison Co., Ltd.; Esaote SPA; Butterfly Network, Inc.; Terason Division Teratech Corporation, iCardio.ai.

The market is driven by the rising prevalence of heart failure and other cardiovascular diseases, which increase the need for regular and precise ejection fraction assessment. Advances in non-invasive imaging technologies, such as AI-enabled echocardiography and cardiac MRI, are improving measurement accuracy and workflow efficiency.

About the Author(s)

Medical Devices Research Team

Healthcare · Medical DevicesThis report was authored by the medical devices research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the medical devices segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Share this report with your colleague or friend.

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.