- Home

- »

- Electronic Devices

- »

-

Emergency Lighting Market Size, Industry Report, 2033GVR Report cover

![Emergency Lighting Market Size, Share & Trends Report]()

Emergency Lighting Market (2026 - 2033) Size, Share & Trends Analysis Report By Component (Hardware, Software, Service), By Light (Fluorescent, LED, Incandescent), By Power System, By End Use (Residential, Commercial, Industrial), By Region, And Segment Forecasts

Market Size, 2025

$7.8BMarket Estimate, 2026

$8.1BMarket Forecast, 2033

$12.4BCAGR, 2026–2033

6.2%Emergency Lighting Market Summary

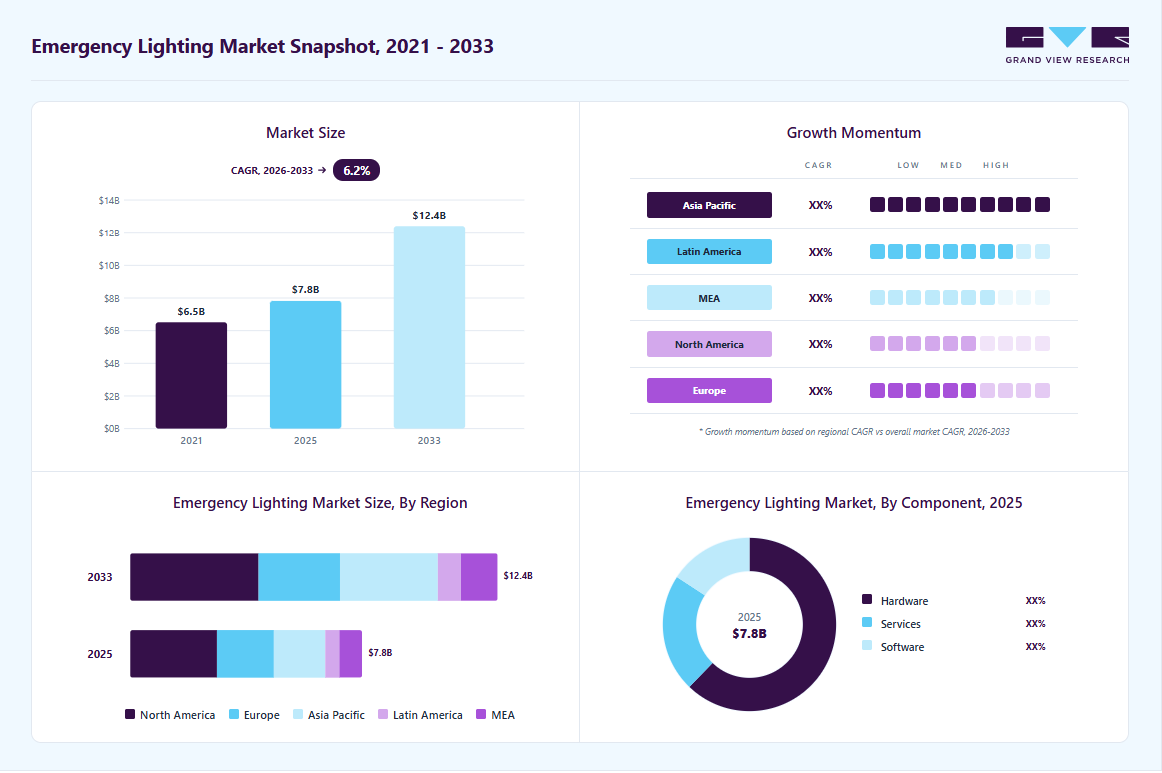

The global emergency lighting market size was valued at USD 7.8 billion in 2025 and is projected to grow from USD 8.1 billion in 2026 to USD 12.4 billion by 2033, at a CAGR of 6.2% from 2026 to 2033. The market in North America dominated with a revenue share of 37.4% in 2025. The adoption of better safety standards and the incorporation of smart technologies are significant market growth drivers.

Key Market Trends & Insights

- By component: The hardware segment held the largest revenue share of 62.2% in 2025.

- By light: The LED segment held the largest revenue share in 2025.

- By power system: The self-contained power system segment held the largest revenue share in 2025.

Regional Highlights

- Largest regional market: North America (37.4% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 7.8 Billion

- Estimated market size in 2026: USD 8.1 Billion

- Projected market size by 2033: USD 12.4 Billion

- CAGR (2026-2033): 6.2%

As global safety regulations become stricter, there is an increasing demand for advanced emergency lighting solutions that comply with these enhanced standards, ensuring greater safety and reliability during power outages and emergencies, driven by the need for reliable solutions alongside the growing importance of the emergency lighting battery market.")

The integration of smart technologies such as IoT-enabled systems and automated monitoring is improving the performance and efficiency of emergency lighting. These technologies allow real-time monitoring, easier maintenance, better energy efficiency, and enhanced user control. IoT-enabled LED emergency lights are becoming a major growth driver for the market, as they support automated control and proactive maintenance. By enabling smooth communication between lighting systems and centralized control platforms, IoT technology helps ensure reliable and efficient operation during emergency situations.

The increasing number of natural disasters is driving market growth, as communities and organizations realize the importance of reliable emergency lighting during emergencies. Events such as hurricanes, earthquakes, and floods often cause power failures and damage infrastructure, making dependable lighting essential for safety and smooth evacuation. This growing awareness is increasing investments in advanced emergency lighting solutions that provide consistent illumination, better visibility, and faster response during crises. As a result, the rise in natural disasters is supporting market growth by encouraging better preparedness and resilience.

At the same time, the growing adoption of smart buildings is increasing the demand for emergency lighting systems that can easily connect with building management systems. These advanced systems support features such as automated testing, real-time monitoring, and predictive maintenance, improving reliability during emergencies. Remote monitoring and control help enhance safety, lower maintenance costs, and improve energy efficiency.

In addition, strict government safety regulations and building codes are further driving the market for emergency lighting systems. Regulatory authorities across regions mandate the installation and regular maintenance of emergency lighting in commercial buildings, industrial facilities, healthcare centers, and public infrastructure to ensure occupant safety. Compliance with these regulations is pushing building owners and facility managers to invest in reliable and advanced emergency lighting solutions, thereby supporting consistent market growth.

Market Dynamics

The growth of the emergency lighting market is driven by increased construction activity and large-scale infrastructure expansion across commercial, residential, industrial, and public sectors. Every newly constructed office building, hospital, school, airport, shopping center, warehouse, and apartment complex must incorporate emergency lighting systems to comply with fire and building safety regulations. As governments and private developers invest in smart cities, transportation networks, healthcare facilities, and industrial parks, demand for compliant exit signs, backup luminaires, and centralized emergency lighting systems rises in parallel. Modern construction projects are also increasingly specifying LED-based and self-testing emergency lighting systems to improve energy efficiency and simplify maintenance, further expanding market opportunities for manufacturers and solution providers.

For instance, in March 2026, according to the U.S. Census Bureau Construction Spending Program, total U.S. construction spending was estimated at a seasonally adjusted annual rate of more than USD 2 trillion, reflecting sustained investment across residential, commercial, healthcare, educational, and public infrastructure projects. This continued expansion in building activity highlights the large volume of new facilities requiring life-safety systems such as emergency lighting to comply with fire and building regulations.

As office buildings, hospitals, schools, airports, warehouses, and transportation hubs are constructed and renovated, developers are required to install emergency lighting systems, illuminated exit signs, and backup power-supported luminaires to ensure safe evacuation during power outages and emergencies. Consequently, rising construction expenditure and infrastructure development directly turn into increased demand for emergency lighting products and related monitoring solutions worldwide.

Intense price competition from low-cost regional and unorganized manufacturers is a significant restraint in the emergency lighting market. Numerous local companies, particularly in Asia Pacific, Latin America, and parts of the Middle East and Africa, offer low-priced emergency lighting products that meet only basic functional requirements. These manufacturers often operate with lower overhead costs and limited investment in research, certification, and after-sales support, allowing them to sell products at substantially lower prices than established global brands. As a result, multinational companies face considerable pricing pressure, which can reduce profit margins and make it more difficult to differentiate premium products based on advanced features such as self-testing, wireless monitoring, and extended battery life.

This pricing pressure is especially pronounced in cost-sensitive customer segments, including small commercial buildings, residential complexes, and public-sector projects where procurement decisions are often driven primarily by upfront cost rather than long-term reliability or maintenance benefits. In some cases, buyers may choose lower-cost products even if they offer shorter lifespans or limited compliance documentation. This intensifies competition and can slow the adoption of higher-value intelligent emergency lighting systems. Consequently, established manufacturers must balance competitive pricing with ongoing investments in innovation, certification, and service capabilities, which can constrain overall profitability and market expansion.

The integration of Internet of Things (IoT) technologies and smart building solutions is creating a transformative opportunity for the emergency lighting market. IoT-enabled emergency lighting systems allow for real-time monitoring of system health, battery performance, and lamp functionality, enabling predictive maintenance and reducing the need for manual inspections. This enhances operational efficiency, ensures compliance with safety regulations, and minimizes downtime, which is particularly critical in large commercial, industrial, and healthcare facilities across the region.

The government investments in smart building infrastructure are creating significant opportunities for the adoption of advanced technologies, including energy-efficient emergency lighting systems. For instance, in the United Arab Emirates (UAE), the government has committed to investing USD 163.3 billion by 2050 to meet the growing energy demand and ensure sustainable growth for the country's economy. This initiative underscores the dedication to integrating smart technologies into its infrastructure to promote energy efficiency and sustainability. As governments continue to prioritize sustainability and modernization, the integration of smart building solutions is expected to play a pivotal role in shaping the future of urban development in the region.

Market Concentration & Characteristics

The emergency lighting market is fragmented, with numerous global and regional manufacturers competing on product reliability, regulatory compliance, pricing, and technological features. Key companies such as Signify, Eaton, Legrand, Schneider Electric, and Acuity Brands hold strong positions due to their established brands and extensive distribution networks; however, no single company commands a dominant market share. The presence of many specialized and regional suppliers across Europe, Asia Pacific, and North America sustains a highly competitive environment and keeps market concentration relatively low.

The degree of innovation in the emergency lighting market is high, driven by continuous advancements in lighting efficiency, battery performance, and intelligent monitoring capabilities. Manufacturers are increasingly integrating LED technology, lithium-ion batteries, wireless connectivity, and automated self-testing features to improve energy efficiency, extend product lifespan, and reduce maintenance costs. Innovations such as cloud-based monitoring platforms and IoT-enabled emergency lighting systems allow facility managers to conduct real-time diagnostics and ensure regulatory compliance more efficiently. In addition, the development of aesthetically integrated luminaires and adaptive systems that support both emergency and general lighting functions is expanding adoption across modern smart buildings. These technological improvements are accelerating product replacement cycles and strengthening competition among market participants.

Component Insights

The hardware segment dominated the market and accounted for the largest revenue share in 2025. The increasing awareness of safety and emergency preparedness across commercial, industrial, and residential sectors is significantly driving the growth of this segment, alongside the rising importance of the market as a critical enabler of reliable backup power systems. Regulatory mandates and strict building codes are enforcing the installation of emergency lighting systems, thereby increasing demand for hardware components such as LED lighting fixtures, control systems, and emergency lighting batteries. In addition, the growing replacement of traditional lighting systems with energy-efficient LED-based emergency lighting hardware is supporting segment growth, as LEDs offer longer lifespan, lower power consumption, and reduced maintenance needs. Furthermore, continuous advancements in battery technologies and the expansion of the emergency lighting battery market are enhancing system reliability and performance, thereby strengthening overall hardware demand.

The software segment is anticipated to register the fastest CAGR during the forecast period, driven by the increasing adoption of smart technologies and the growing demand for energy-efficient solutions. This segment includes software for managing, monitoring, and controlling emergency lighting systems, ensuring they function optimally during power outages or emergencies. Advancements in Internet of Things (IoT) technologies, which enable real-time monitoring and control of lighting systems through connected devices, drive the growth of the software segment. The fully automated system offers real-time status updates for all monitored buildings, displayed on a digital floor plan, enhancing safety and aiding in maintenance planning.

Light Insights

The LED segment accounted for the largest revenue share in 2025, due to the increasing demand for energy-efficient lighting solutions. LEDs consume significantly less power compared to traditional incandescent and fluorescent bulbs, which has led to widespread adoption in both residential and commercial sectors. Moreover, advancements in LED technology have resulted in improved brightness, longer lifespan, and reduced costs, making them more accessible and appealing to a broader market.

The fluorescent segment is expected to grow at a significant CAGR during the forecast period, due to the ongoing urbanization and infrastructural development across various regions. As cities expand and new commercial complexes, residential buildings, and industrial facilities are constructed, the need for effective emergency lighting systems becomes paramount. Fluorescent lights, known for their energy efficiency and long lifespan, are often preferred in these installations, further boosting the market for fluorescent emergency lighting.

Power System Insights

The self-contained power system segment accounted for the largest revenue share in 2025. Innovations in battery technology, such as the development of long-lasting and energy-efficient lithium-ion batteries, have significantly improved the reliability and performance of these systems. In addition, advancements in LED lighting technology have enhanced the efficiency and lifespan of emergency lighting solutions, making self-contained systems more useful to end-users. Furthermore, the ease of installation and reduced dependency on centralized power infrastructure make self-contained power systems a preferred choice across commercial and residential buildings, supporting their widespread adoption and contributing to segment growth.

The hybrid power system segment is anticipated to grow at the fastest CAGR during the forecast period, driven by the increasing frequency of power outages and the rising need for reliable emergency lighting solutions across residential and commercial buildings. The growing relevance of the emergency lighting battery market is further supporting this segment, as batteries play a crucial role in storing and supplying backup power within hybrid systems. These systems, which combine traditional power sources with renewable energy options such as solar and wind, offer enhanced reliability and sustainability, ensuring that emergency lighting remains operational during power failures. In addition, advancements in energy storage technologies and the expansion of the emergency lighting battery market are improving system efficiency, durability, and performance. As a result, hybrid power systems are gaining traction as a resilient and energy-efficient solution for modern emergency lighting infrastructure.

End Use Insights

The commercial segment accounted for the largest revenue share in 2025. The increasing focus on workplace safety and compliance with fire safety regulations is pushing businesses to invest in advanced emergency lighting systems. In addition, technological advancements, such as the development of energy-efficient LED lights and smart lighting solutions, are enhancing the effectiveness and appeal of emergency lighting products. The increasing adoption of green building practices and energy-efficient solutions also contributes to market growth, as businesses seek to reduce operational costs and environmental impact.

The industrial segment is expected to grow at the fastest CAGR during the forecast period. The increase in industrial activities, especially in emerging economies, is driving the demand for emergency lighting systems. As new industrial facilities are established, the need for comprehensive safety measures, including emergency lighting, becomes necessary. There is a heightened awareness among industrial operators regarding the importance of workplace safety. This awareness is fueling investments in emergency lighting systems to ensure that employees have safe routes during emergencies.

Regional Insights

North America Emergency Lighting Market Trends

North America emergency lighting industry accounted for a revenue share of over 37.4% of the global market in 2025. The growing use of smart technologies in buildings is helping drive market growth in the region. As more smart buildings adopt IoT-based devices and automated systems, there is an increasing demand for advanced emergency lighting solutions. These systems provide features such as real-time monitoring, automatic testing, and predictive maintenance, which improve safety and efficiency. In addition, the strong focus on energy efficiency and sustainability is increasing demand, as modern emergency lighting systems consume less energy and are more environmentally friendly.

U.S. Emergency Lighting Market Trends

The U.S. emergency lighting industry is expected to grow significantly from 2026 to 2033, driven by strict safety regulations and building codes enforced by agencies such as the Occupational Safety and Health Administration (OSHA) and the National Fire Protection Association (NFPA). These regulations mandate the installation of reliable emergency lighting systems across commercial, industrial, and residential buildings, significantly supporting the growth of the U.S. emergency lighting industry. In addition, increasing investments in infrastructure modernization and smart building technologies are further accelerating demand, ensuring occupant safety during power outages and emergency situations while strengthening the overall U.S. emergency lighting industry outlook.

Asia Pacific Emergency Lighting Market Trends

The Asia Pacific emergency lighting industry is growing steadily at a significant CAGR from 2026 to 2033due to the rapid urbanization and industrialization in emerging economies such as China, India, and Southeast Asian countries. As these regions experience substantial economic growth, there is an increased demand for commercial and residential infrastructure, which in turn increases the need for reliable emergency lighting solutions. Governments in these countries are also implementing strict safety regulations and building codes, mandating the installation of emergency lighting systems in new constructions and existing buildings.

China emergency lighting industry accounted for a significant share of the Asia Pacific market in 2025, driven by rapid urbanization, strict safety regulations, and infrastructure expansion. The country’s increasing construction of commercial buildings, residential complexes, and public infrastructure is increasing demand for emergency and exit lighting solutions, as adherence to building and fire safety codes becomes more rigorous. The shift from traditional fluorescent systems to energy‑efficient LED emergency lighting is a notable trend, supported by growing awareness of fire safety and compliance requirements.

Australia emergency lighting industry accounted for a significant share of the regional market in 2025, driven by strict building safety regulations and strong compliance requirements across commercial and public infrastructure. The Australia market is witnessing steady growth due to increasing investments in smart buildings, infrastructure modernization, and urban development projects across major cities. In addition, the rising adoption of energy-efficient LED-based emergency lighting systems and integration of smart monitoring technologies are further supporting the expansion of the Australia market. Growing awareness regarding workplace safety, particularly in sectors such as healthcare, mining, and commercial real estate, is also contributing to increased installations. Furthermore, the Australia emergency lighting industry is benefiting from the need for reliable backup systems in response to power outages and emergency preparedness initiatives, reinforcing demand for advanced and compliant lighting solutions.

Europe Emergency Lighting Market Trends

The Europe emergency lighting industry is anticipated to register a significant CAGR from 2026 to 2033, due to the increasing adoption of energy-efficient and environmentally sustainable technologies. This has led to a growing preference for LED-based emergency lighting systems, which offer significant energy savings, longer lifespan, and reduced environmental impact compared to traditional lighting solutions. Furthermore, the integration of smart technologies in building management systems is enhancing the functionality and efficiency of emergency lighting. Smart emergency lighting solutions, equipped with IoT capabilities, enable automated testing, real-time monitoring, and predictive maintenance, ensuring optimal performance and compliance with safety standards. Such technological advancement is driving the demand for innovative emergency lighting solutions across the European market.

The emergency lighting industry in the UK is expected to grow rapidly in the coming years. A key trend is the strengthening of national safety standards and regulatory frameworks that are shaping how emergency lighting systems are designed, installed, and maintained. In November 2025, the British Standards Institution (BSI) released the updated BS 5266‑1:2025 code of practice, expanding guidance beyond traditional escape lighting to include local area and standby lighting, and aligning with the latest European standards to improve clarity and safety outcomes. This revision reflects a broader industry and government push toward enhancing fire safety and compliance across commercial, public, and high‑risk buildings, encouraging organizations to adopt stronger and well‑documented emergency lighting practices.

Key Emergency Lighting Company Insights

Some of the key companies operating in the market, include ABB, Signify Holding, Honeywell International Inc., General Electric, Emerson Electric Co., Hubbell, and Legrand.The companies are focusing on various strategic initiatives, including new product development, partnerships & collaborations, and agreements to gain a competitive advantage over their rivals. The following are some instances of such initiatives.

-

Acuity Brands is a global provider of lighting and building management solutions, designing and manufacturing innovative indoor and outdoor lighting products and controls for commercial, industrial, residential, and infrastructure lighting types. Headquartered in Atlanta, Georgia, the company operates across North America, Europe, and Asia and markets lighting solutions under brands such as Lithonia Lighting, Holophane, Gotham, and Winona. The company also has a strong presence in the emergency lighting industry, offering LED-based emergency fixtures, exit signs, and integrated emergency lighting control systems for enhanced safety and regulatory compliance.

-

Signify Holding is a global company in lighting, delivering innovative and sustainable lighting products, systems, and services for homes, businesses, and cities. Formerly part of Philips, the company operates in more than 70 countries and focuses on energy-efficient, connected lighting solutions, including LED lighting and smart controls. Signify’s portfolio includes Philips Hue, Interact IoT platforms, and professional lighting systems that enhance user experience and sustainability. In the emergency lighting space, Signify offers advanced LED-based emergency fixtures and connected systems, such as cloud-linked monitoring and compliance platforms, to improve reliability, safety, and efficiency in critical situations.

Key Emergency Lighting Companies:

The following key companies have been profiled for this study on the emergency lighting market.

- ABB

- ACUITY BRANDS, INC.

- Beghelli S.p.A.

- Cooper Lighting LLC.

- Eaton

- Emerson Electric Co.

- General Electric

- Honeywell International Inc.

- Hubbell

- LEDVANCE GmbH

- Legrand

- Panasonic Corporation

- Schneider Electric

- Signify Holding

- Zumtobel Group

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weakness

Mature Players: Signify; Eaton; Legrand; Schneider Electric; Acuity Brands; ABB Ltd.

- Maintain broad portfolios covering exit signs, emergency luminaires, central battery systems, and smart monitoring software.

- Invest heavily in LED efficiency, lithium-ion batteries, wireless diagnostics, and automated self-testing technologies.

- Leverage global manufacturing footprints, strong distributor networks, and established relationships with contractors and facility managers.

- Strong brand recognition and proven product reliability in mission-critical life-safety applications.

- Ability to deliver integrated building solutions combining emergency lighting, fire safety, and energy management systems.

- Extensive certification capabilities and technical support resources.

- Premium pricing can limit competitiveness in cost-sensitive markets.

- Large organizational structures may slow product customization and decision-making.

- Higher compliance and R&D costs pressure margins.

Emerging Players: Mackwell Group; Ventilux; LuxIntelligent; Beghelli S.p.A.

- Focus on niche applications such as healthcare, transportation, industrial facilities, and architecturally integrated emergency lighting.

- Develop flexible OEM and private-label manufacturing partnerships.

- Expand distribution through electrical wholesalers and online channels.

- Competitive pricing and faster response to local market needs.

- Greater flexibility in customization and shorter product development cycles.

- Ability to target underserved customer segments.

- Limited global distribution and lower brand visibility.

- Smaller R&D budgets constrain advanced technology development.

- Fewer certifications and compliance resources for international expansion.

Recent Developments

-

In September 2025, Ovia expanded its emergency lighting offerings by adding the Orbik brand to its portfolio. The move gives Ovia the rights to distribute the established Orbik emergency lighting solutions, strengthening its range of products for commercial, industrial, and residential safety applications. This strategic step enhances Ovia’s market presence and commitment to delivering reliable, energy-efficient emergency lighting solutions worldwide.

-

In June 2025, Signify launched its new Interact wireless emergency lighting system, a cloud-based solution that allows building managers to control, monitor, test, and generate compliance reports for both general and emergency lighting from a single secure dashboard. The system automates function and duration tests, delivers health status alerts, and simplifies maintenance while supporting regulatory compliance, helping reduce operational complexity and costs.

-

In May 2025, LiteTrace launched EmerLite, a new wireless emergency lighting testing and compliance platform. The system uses Bluetooth mesh technology and connects with the Keilton+autani ecosystem to automate emergency lighting tests, eliminate manual procedures, and provide real-time status monitoring, instant maintenance alerts, and digital compliance reports via a mobile app and cloud storage. This solution supports battery backups, emergency drivers, and exit/signage lights, helping commercial facilities save time and lower testing costs.

Emergency Lighting Market Report Scope

Report Attribute

Details

Market size in 2025

USD 7.8 billion

Estimated market size in 2026

USD 8.1 billion

Projected market size by 2033

USD 12.4 billion

Growth rate

CAGR of 6.2% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Component, light, power system, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; Saudi Arabia; South Africa

Key companies profiled

ABB; ACUITY BRANDS, INC.; Beghelli S.p.A.; Cooper Lighting LLC.; Eaton; Emerson Electric Co.; General Electric; Honeywell International Inc.; Hubbell; LEDVANCE GmbH; Legrand; Panasonic Corporation; Schneider Electric; Signify Holding; Zumtobel Group

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Emergency Lighting Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global emergency lighting market report based on component, light, power system, end use, and region.

-

Component Outlook (Revenue, USD Million, 2021 - 2033)

-

Hardware

-

Software

-

Services

-

-

Light Outlook (Revenue, USD Million, 2021 - 2033)

-

Fluorescent

-

LED

-

Incandescent

-

Others

-

-

Power System Outlook (Revenue, USD Million, 2021 - 2033)

-

Self-Contained Power System

-

Central Power System

-

Hybrid Power System

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Commercia

-

Industrial

-

Residential

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Middle East & Africa emergency lighting market analysis with detailed country-level analysis for the U.S., Saudi Arabia, South Africa, Qatar, and Egypt

Delivered a region-specific assessment covering market size, growth forecasts competitive landscape, and comprehensive market analysis.

Provided detailed country-level analysis for the U.S., Saudi Arabia, South Africa, Qatar, and Egypt, including construction trends, infrastructure investments, and adoption patterns.

Identified the most prime countries for expansion and investment.

Highlighted regulatory and building code requirements influencing product adoption.

Provided strategic insights on distributor partnerships and market-entry opportunities.

Regulatory and standards impact assessment

Analyzed major standards and codes including NFPA 101, OSHA, UL 924, EN 1838, IEC 60598-2-22, and regional fire safety regulations.

Evaluated how changes in compliance requirements affect product specifications and replacement demand.

Identified compliance-driven growth opportunities.

Reduced regulatory uncertainty for product launches.

Smart emergency lighting and connected systems opportunity analysis

Assessed adoption of IoT-enabled monitoring, automated self-testing, cloud-based diagnostics, and wireless control systems.

Evaluated demand across smart buildings, hospitals, airports, and industrial facilities.

Identified premium technology segments with above-average growth.

Highlighted opportunities for recurring software and service revenue.

Frequently Asked Questions About This Report

The global emergency lighting market size was estimated at USD 7.8 billion in 2025 and is expected to reach USD 8.1 billion in 2026.

As global safety regulations become more stringent, there is a rising demand for advanced emergency lighting solutions that comply with these enhanced standards, ensuring greater safety and reliability during power outages and emergencies.

The global emergency lighting market is expected to grow at a compound annual growth rate of 6.2% from 2026 to 2033 to reach USD 12.4 billion by 2033.

The hardware segment accounted for the largest market share of 62.2% in 2025.

Key players include ABB; ACUITY BRANDS, INC.; Beghelli S.p.A.; Cooper Lighting LLC.; Eaton; Emerson Electric Co.; General Electric; Honeywell International Inc.; Hubbell; LEDVANCE GmbH; Legrand; Panasonic Corporation; Schneider Electric; Signify Holding; Zumtobel Group

LED held the largest revenue share in 2025.

The self-contained power system held the largest share in 2025 and hybrid power system is the fastest-growing.

North America dominated with a 37.4% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

About the Author(s)

Electronic Devices Research Team

Semiconductors & Electronics · Electronic DevicesThis report was authored by the electronic devices research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the electronic devices segment of the semiconductors & electronics industry. All findings are based on proprietary semiconductors & electronics databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.