- Home

- »

- Advanced Interior Materials

- »

-

Energy Materials Market Size And Share Report, 2026-2033GVR Report cover

![Energy Materials Market Size, Share & Trends Report]()

Energy Materials Market (2026 - 2033) Size, Share & Trends Analysis Report By Material Type (Metals & Alloys, Battery & Electrochemical Materials, Polymers & Composites), By Application (Renewable Power Generation, Energy Storage Systems, Transmission & Distribution Infrastructure), By Region, And Segment Forecasts

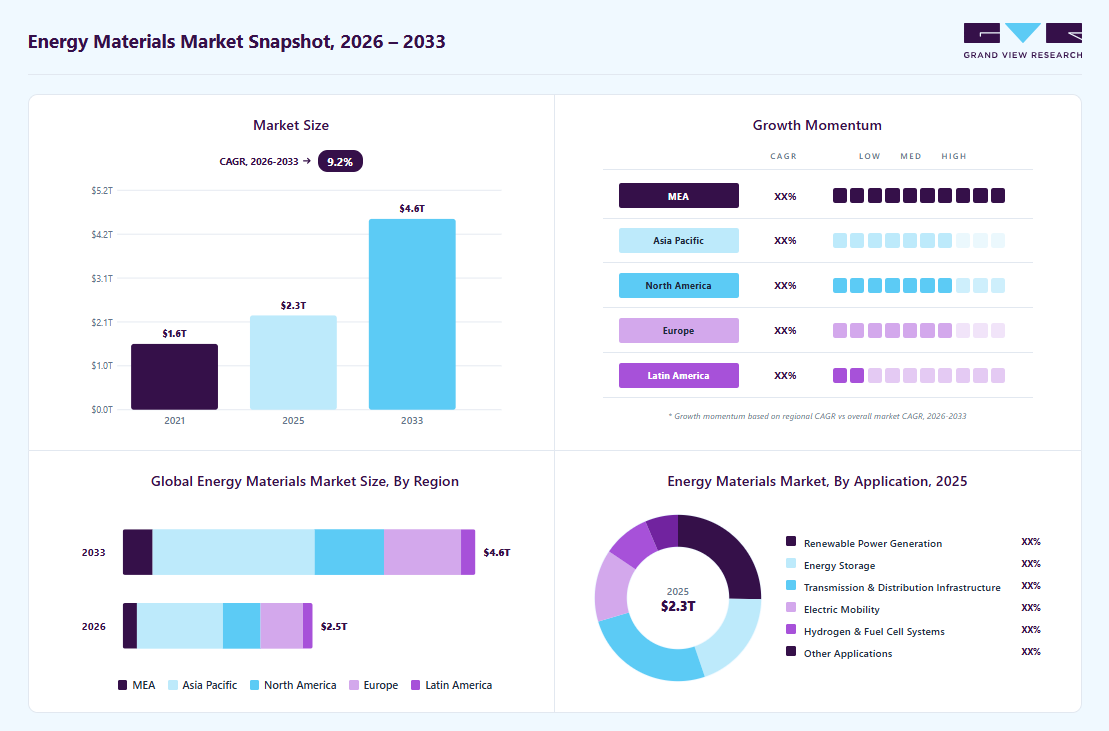

Market Size, 2025

$2.3TMarket Estimate, 2026

$2.5TMarket Forecast, 2033

$4.6TCAGR, 2026–2033

9.2%Energy Materials Market Summary

The global energy materials market size was valued at USD 2.3 trillion in 2025 and is projected to grow from USD 2.5 trillion in 2026 to USD 4.6 trillion by 2033, at a CAGR of 9.2% from 2026 to 2033. The Asia Pacific held the largest share of 45.2% of the global market in 2025. Increasing grid modernization investments are accelerating demand for advanced conductive, insulating, and thermal management materials.

Key Market Trends & Insights

- By material type: Battery & electrochemical materials segment is expected to grow at a CAGR of 9.4% from 2026 to 2033.

- By application: Energy storage systems segment is expected to grow at a CAGR of 10.4% from 2026 to 2033.

Regional Highlights

- Largest regional market: Asia Pacific (45.2% revenue share, 2025)

- By country: The energy materials industry in India is expected to grow at the fastest CAGR of 11.9% from 2026 to 2033.

Market Size & Forecast

- Market size in 2025: USD 2.3 Trillion

- Estimated market size in 2026: USD 2.5 Trillion

- Projected market size by 2033: USD 4.6 Trillion

- CAGR (2026-2033): 9.2%

Utilities are upgrading transmission, distribution, and storage infrastructure to integrate renewables, directly expanding the addressable market for high-performance energy materials. The energy materials market is increasingly shaped by the global transition to decarbonized power systems and electrification.")

Demand for advanced materials for batteries, solar cells, fuel cells, and thermoelectric is rising as countries set aggressive renewable energy targets and battery storage deployments accelerate. Innovations such as structural battery composites and nanostructured materials further propel this trend by enabling higher performance and multifunctional applications across transport, grid storage, and consumer electronics.

Drivers, Opportunities & Restraints

A primary driver for this market is the rapid expansion of electrification across transport and power sectors. Growth in electric vehicle adoption and utility-scale energy storage increases demand for high-performance materials such as next-generation cathodes, solid-state electrolytes, and graphene-enhanced components. Supportive government policies and incentives for clean energy infrastructure investment reinforce capital flows into energy materials R&D and production capacity, reinforcing sustained industry growth.

There is a significant opportunity in emerging and frontier technologies that address current limitations in energy conversion and storage. Materials enabling solid-state batteries, high-density supercapacitors, and thermoelectric generation present clear potential to broaden market applications. Expansion into untapped regions such as Asia-Pacific and Latin America also offers market players avenues to diversify revenue streams and capitalize on the growing energy demand driven by rapid urbanization.

A major restraint is persistent supply chain vulnerability for critical raw materials. Concentration in refining and processing of lithium, cobalt, nickel, and rare earth elements poses risks of supply disruptions and price volatility. These constraints are compounded by high manufacturing costs, environmental permitting barriers, and scalability challenges for advanced materials, collectively hindering commercialization and delaying wider adoption.

Market Concentration & Characteristics

The market growth stage is high, and growth is accelerating. The market exhibits fragmentation, with key players dominating the industry landscape. Major companies such as Contemporary Amperex Technology Co., Limited (CATL), LG Energy Solution, Ltd., Panasonic Holdings Corporation, Samsung SDI Co., Ltd., Albemarle Corporation, Umicore SA, Johnson Matthey plc, Sociedad Química y Minera de Chile S.A. (SQM), BASF SE, Sumitomo Metal Mining Co., Ltd., and others play a significant role in shaping the market dynamics. These leading players often drive innovation in the market by introducing new products, technologies, and materials to meet the industry's evolving demands.

The energy materials market is characterized by rapid innovation driven by performance, cost, and sustainability imperatives. Developers are advancing solid-state electrolytes, silicon-graphene anodes, and high-nickel cathodes to improve energy density, safety, and lifecycle. Breakthroughs in nanomaterials and coatings are enhancing conductivity and corrosion resistance in grid components. Innovation is also accelerating circularity with recycling-ready chemistries. These developments are increasingly differentiating suppliers and shortening time-to-commercialization in key segments such as batteries and renewable energy systems.

Product substitutes in the energy materials market are reshaping competitive dynamics. For instance, lithium iron phosphate and sodium-ion chemistries are emerging as lower-cost alternatives to traditional nickel-cobalt-aluminum cathodes in certain EV and storage applications. Advanced composites are replacing heavier metal components in infrastructure to reduce losses and installation costs. Polymers and organic conductors are gaining attention as potential substitutes for select metal alloys in niche conductive applications. These shifts influence material selection, supply chain strategies, and cost-competitive positioning across end markets.

Material Type Insights

The metals & alloys segment dominated the market with a revenue share of 54.6% in 2025, and is projected to grow at a 9.6% CAGR from 2026 to 2033. The segment is driven by escalating demand for conductive and structural materials that support renewable energy infrastructure and electrification. Copper demand is rising alongside the rapid expansion of grid upgrades and EV charging networks, as its conductivity remains critical for efficient power transmission. Nickel and aluminum alloys are also gaining traction due to their strength, weight, and thermal performance advantages. These factors together elevate investment in high-performance metal supply chains across utilities and manufacturers.

The battery & electrochemical materials segment is anticipated to expand at a 9.4% CAGR over the forecast period. The battery & electrochemical materials are underpinned by accelerating adoption of lithium-ion and next-generation chemistries across electric vehicles and stationary storage systems. Growth in energy storage capacity and production of lithium-based materials continues to shape industry dynamics, even as chemistry preferences evolve toward lithium iron phosphate for cost and lifecycle benefits. Expanding cell manufacturing capacities in Asia, Europe, and the U.S. also reinforces this driver by strengthening regional value chains and reducing reliance on legacy producers.

Application Insights

The transmission & distribution infrastructure segment dominated the market across applications, accounting for 25.7% of revenue in 2025, and is forecasted to grow at a 9.0% CAGR from 2026 to 2033. Investment in Transmission & Distribution Infrastructure is a core driver of demand for advanced energy materials. Utilities globally are modernizing networks to accommodate higher loads from renewables, distributed generation, and electrified transport. This requires substantial volumes of high-conductivity metals, advanced insulating composites, and durable alloys to enhance reliability and reduce losses. Public and private spending on grid resilience and smart grid technologies is expanding the addressable market for materials that deliver long service life and operational efficiency.

The energy storage systems segment is expected to grow at a 10.4% CAGR over the forecast period in the automotive energy materials glazing market. The energy storage systems segment is propelled by the rapid scale-up of grid-scale battery deployments to support intermittent renewable generation. Utility and commercial storage installations are expanding capacity at record rates to stabilize grids, balance supply and demand, and provide ancillary services. Rising interest in secondary and repurposed battery applications is also creating new supply channels for energy storage materials. These factors collectively expand the materials market to meet diverse storage application needs across regions.

Regional Insights & Trends

The Asia Pacific energy materials industry held the largest revenue share of 45.2% in 2025. The region is expected to grow at a CAGR of 9.5% over the forecast period. Asia Pacific’s energy materials demand is powered by its dominant role in global battery manufacturing and renewable energy deployment. China, Japan, and South Korea lead in lithium-ion battery production, raw-material processing, and technological innovation. Rapid electrification, coupled with supportive industrial policies, expands uptake of advanced materials for EVs, grid storage, and renewable infrastructure.

Energy material market in China is dominant in the energy materials ecosystem stems from its extensive manufacturing scale, strong export capabilities, and strategic integration of resources. The nation produces a majority of global battery cells and refines most of the critical minerals used in energy applications. Rapid expansion of battery energy storage systems and EV production fuels domestic and global material demand. Export growth enhances China’s influence on pricing and supply dynamics, underpinning its central role in the global energy transition.

North America Energy Materials Market Trends

Demand in North America is driven by strong policy support and investment in clean energy infrastructure. Federal incentives such as the U.S. Inflation Reduction Act and Canada’s clean energy mandates are expanding domestic production of battery and energy storage materials. Automotive OEMs and energy firms are accelerating gigafactory and material processing projects to localize supply chains. High adoption of EVs and grid-scale storage creates sustained demand for advanced materials. Technology innovation hubs further reinforce regional market growth.

U.S. Energy Materials Market Trends

In the U.S., market momentum is anchored in comprehensive federal support and robust industrial R&D. Significant capital flows into battery material production and advanced energy materials innovation are stimulated by tax incentives and clean energy standards. The country’s expansive EV market, combined with large-scale renewable installations, is driving demand for cathode, anode, and electrolyte materials. Partnerships between domestic automakers and material suppliers strengthen regional capacity and reduce dependency on imports.

Europe Energy Materials Market Trends

Europe’s driver for energy materials is anchored in ambitious decarbonization targets and regulatory frameworks that prioritize local sourcing and sustainability. Renewable energy mandates and electrification policies stimulate demand for advanced materials in battery production, grid infrastructure, and storage systems. Investment in domestic supply chains, including lithium projects and gigafactories, aims to reduce reliance on external suppliers.

Key Energy Materials Company Insights

The energy materials industry is highly competitive, with several key players dominating the landscape. Major companies include Contemporary Amperex Technology Co., Limited (CATL), LG Energy Solution, Ltd., Panasonic Holdings Corporation, Samsung SDI Co., Ltd., Albemarle Corporation, Umicore SA, Johnson Matthey plc, Sociedad Química y Minera de Chile S.A. (SQM), BASF SE, and Sumitomo Metal Mining Co., Ltd. The energy materials industry is characterized by a competitive landscape with several key players driving innovation and market growth. Major companies in this sector are investing heavily in research and development to enhance the performance, cost-effectiveness, and sustainability of their products.

Key Energy Materials Companies:

The following key companies have been profiled for this study on the energy materials market.

- Contemporary Amperex Technology Co., Limited (CATL)

- LG Energy Solution, Ltd.

- Panasonic Holdings Corporation

- Samsung SDI Co., Ltd.

- Albemarle Corporation

- Umicore SA

- Johnson Matthey plc

- Sociedad Química y Minera de Chile S.A. (SQM)

- BASF SE

- Sumitomo Metal Mining Co., Ltd.

Recent Developments

-

In June 2025, CATL announced a USD 6 billion manufacturing complex to scale cathode and nickel processing. Once operational, the site is projected to target 142,000 tons of nickel and 30,000 tons of cathode output annually, plus battery-recycling throughput.

-

In November 2024, Dragonfly Energy partnered with Bruker to accelerate battery materials development. The collaboration combines Dragonfly’s cell know-how with Bruker’s analytical tools to speed materials scale-up and reduce development cycle times.

Energy Materials Market Report Scope

Report Attribute

Details

Market size in 2025

USD 2.3 trillion

Estimated market size in 2026

USD 2.5 trillion

Projected market size by 2033

USD 4.6 trillion

Growth rate

CAGR of 9.2% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion/trillion, Volume in Kilotons, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, competitive landscape, growth factors, and trends

Global Energy Materials Market Report Segmentation

Material type, application, region

Regional scope

North America; Europe; Asia Pacific; Central & South America; Middle East & Africa

Country Scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; China; India; Japan; Australia; South Korea; Brazil; Argentina; Saudi Arabia; UAE; South Africa

Key companies profiled

Contemporary Amperex Technology Co. Limited (CATL); LG Energy Solution, Ltd.; Panasonic Holdings Corporation; Samsung SDI Co., Ltd.; Albemarle Corporation; Umicore SA; Johnson Matthey plc; Sociedad Química y Minera de Chile S.A. (SQM); BASF SE; Sumitomo Metal Mining Co., Ltd.

Customization scope

Free report customization (equivalent to up to 8 analyst working days) with purchase. Addition or alteration to country, regional & segment scope

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Energy Materials Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends across sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the energy materials market report based on material type, application, and region:

-

Material Type Outlook (Volume, Kilotons; Revenue, USD Billion, 2021 - 2033)

-

Metals & Alloys

-

Battery & Electrochemical Materials

-

Polymers & Composites

-

Other materials

-

-

Application Outlook (Volume, Kilotons; Revenue, USD Billion, 2021 - 2033)

-

Renewable Power Generation

-

Energy Storage Systems

-

Transmission & Distribution Infrastructure

-

Electric Mobility

-

Hydrogen & Fuel Cell Systems

-

Other Applications

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Central & South America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

South Africa

-

-

Frequently Asked Questions About This Report

The global energy materials market size was valued at USD 2.3 trillion in 2025 and is projected to grow from USD 2.5 trillion in 2026.

The global energy materials market is expected to grow at a CAGR of 9.2% from 2026 to 2033, reaching USD 4.6 trillion.

Key factors include increasing grid modernization investments are accelerating demand for advanced conductive, insulating, and thermal management materials.

Asia Pacific dominated with a 45.2% revenue share in 2025.

Middle East & Africa is the fastest-growing region over the forecast period.

the metals & alloys held the largest revenue share of 54.6% in 2025, while battery & electrochemical materials is the significant-growing segment.

The transmission & distribution infrastructure holds the largest market share of 25.7% in 2025, while energy storage systems is the significant-growing segment.

Key players include Contemporary Amperex Technology Co. Limited (CATL); LG Energy Solution, Ltd.; Panasonic Holdings Corporation; Samsung SDI Co., Ltd.; Albemarle Corporation; Umicore SA; Johnson Matthey plc; Sociedad Química y Minera de Chile S.A. (SQM); BASF SE; Sumitomo Metal Mining Co., Ltd.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.