- Home

- »

- Distribution & Utilities

- »

-

Fault Current Limiter Market Size & Share Report, 2025-2030GVR Report cover

![Fault Current Limiter Market (2025 - 2030)Report]()

Fault Current Limiter Market (2025 - 2030)

Size, Share & Trends Analysis Report By Type (Superconducting, Non-Superconducting), By Voltage Range, By End-use (Power Stations, Oil & Gas), By Region, And Segment Forecasts

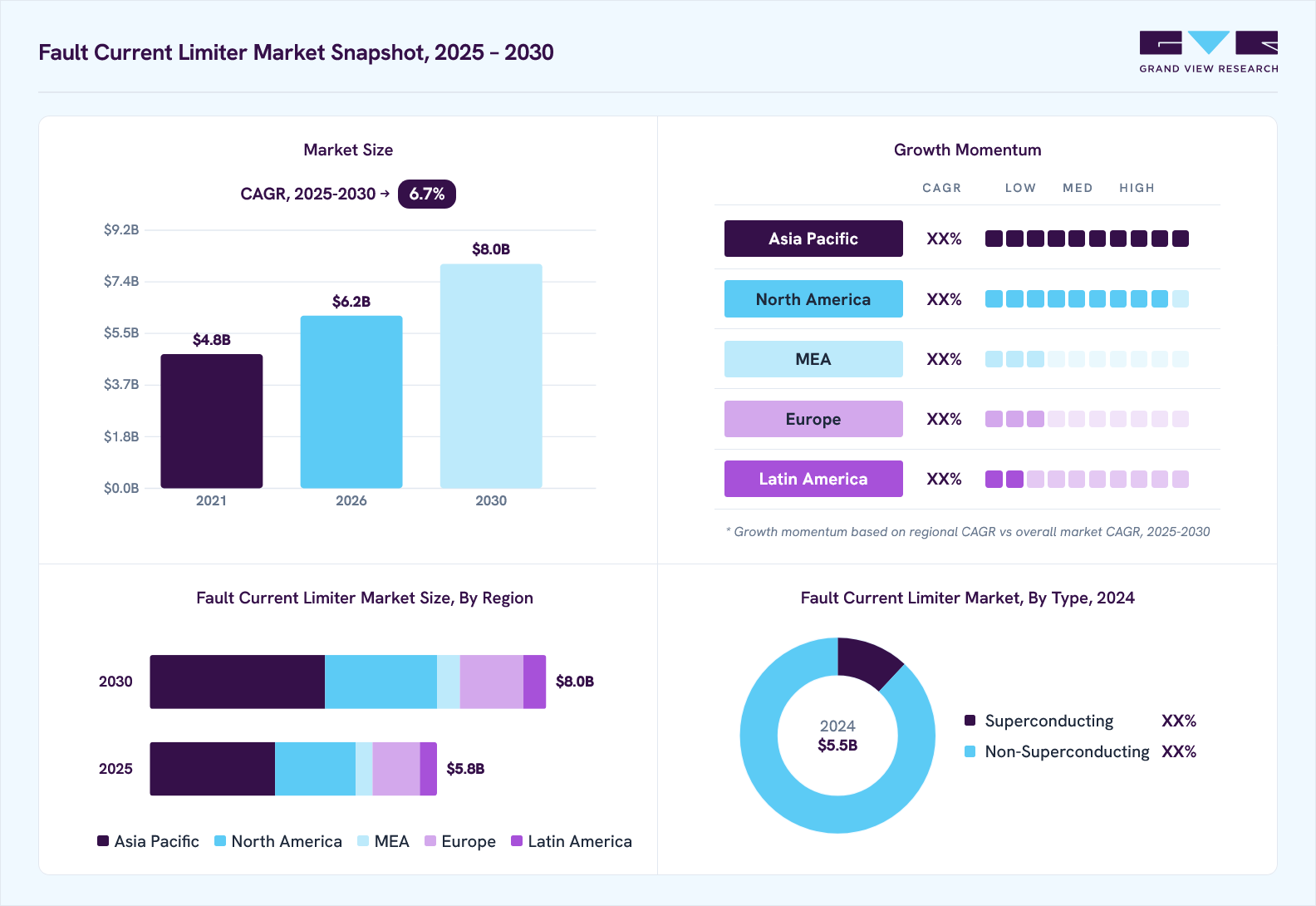

Market Size, 2024

$5.5BMarket Estimate, 2026

$6.2BMarket Forecast, 2030

$8.0BCAGR, 2025–2030

6.7%Fault Current Limiter Market Summary

The global fault current limiter market size was valued at USD 5.5 billion in 2024 and is projected to grow from USD 6.2 billion in 2026 to USD 8.0 billion by 2030, at a CAGR of 6.7% from 2025 to 2030. Asia Pacific dominated the market, accounting for a revenue share of 43.5% in 2024. The global market is shaped by several key trends, with technological advancements at the forefront.

Key Market Trends & Insights

- The China fault current limiter market held significant share in the Asia Pacific region in 2024.

- By type, the non-superconducting fault current limiter segment held the largest revenue share of 88.0% in 2024.

- By voltage, the high-voltage segment held the largest revenue share in 2024.

- By end use, the power stations end-use segment held the largest revenue share in 2024.

- By end use, the power stations segment is expected to grow at a CAGR of 6.2% over the forecast period.

Market Size & Forecast

- Market size in 2024: USD 5.5 Billion

- Projected market size by 2030: USD 8.0 Billion

- CAGR (2025-2030): 6.7%

- Asia Pacific: Largest market in 2024

One significant trend is the growing adoption of superconducting fault current limiters (SFCLs), which use superconducting materials to limit fault currents with high efficiency and minimal energy loss. The rising demand for reliable and resilient power systems drives the Fault Current Limiter (FCL) market. FCLs are critical components that protect electrical networks from damage caused by excessive fault currents, which can result from short circuits or equipment failures. The need for advanced fault current management technologies is increasing as power grids become more complex, particularly with the integration of renewable energy.")

Growing urbanization and the push toward electrification in sectors such as transportation are placing additional strain on power infrastructure. FCLs play a crucial role by swiftly limiting excessive current during fault conditions, thereby safeguarding equipment and maintaining system stability without disrupting the power supply. Another significant factor boosting market growth is the global trend toward smart grid development and modernization. Ongoing innovations in superconducting and solid-state technologies are making FCLs more compact, energy-efficient, and economically viable, accelerating their adoption in utility, industrial, and commercial applications worldwide.

The rising incidence of electrical faults and blackouts is prompting companies to invest in advanced protection systems like fault current limiters. The growing demand for uninterrupted power supply in critical spaces such as data centers, hospitals, and manufacturing plants is further driving the adoption of FCL. The emergence of microgrids and distributed energy systems also creates a favorable environment for FCLs, as these decentralized setups require robust fault management to ensure efficient and stable operation.

The global shift towards sustainability and renewable energy is influencing the market growth. The integration of renewable energy sources, such as wind and solar, into existing power grids presents unique challenges, including variability in power generation and the need for robust protection systems to manage potential faults. Fault current limiters are critical in mitigating these challenges by ensuring that faults do not cause extensive damage or disrupt power supply. As countries worldwide accelerate their transition to cleaner energy, the demand for fault current limiters is expected to grow, supporting a more stable and resilient energy infrastructure that can accommodate diverse and renewable energy sources.

Market Concentration & Characteristics

The global market is characterized by its rapid growth, driven primarily by the increasing demand for enhanced power grid reliability and safety. As power grids expand and become more interconnected, the risk of fault currents due to short circuits and other electrical faults has risen, necessitating the adoption of advanced technologies to protect infrastructure.

The Fault Current Limiter (FCL) market growth is moderate, and the pace of growth is accelerating. The market is characterized by high innovation, particularly in superconducting and solid state FCLs. Companies are investing in R&D to develop compact, energy-efficient, and digitally integrated FCLs suitable for smart grids and EV infrastructure. Breakthroughs in superconducting materials, cryogenic systems, and power electronics continue to push technological boundaries, making innovation a key competitive factor.

The market is marked by regional diversity, with significant growth observed in areas undergoing rapid industrialization and infrastructure development, such as the Asia-Pacific region. Countries like China, India, and Japan are key markets due to their substantial investments in upgrading power infrastructure and integrating renewable energy sources. Meanwhile, developed regions like North America and Europe are focusing on grid modernization and resilience, driving demand for advanced fault current limiter solutions to maintain grid stability and meet regulatory standards. Overall, the global market is dynamic, shaped by technological innovation, regional developments, and a growing emphasis on reliable and efficient power distribution systems.

Type Insights

The non-superconducting fault current limiter segment held the largest revenue share of 88.0% in 2024. This dominance is primarily due to their proven reliability, lower cost, and widespread applicability across various power systems. Unlike superconducting fault current limiters, which require advanced materials and cooling systems, non-superconducting fault current limiters use more conventional technology, making them easier to integrate into existing grid infrastructure without extensive modifications. Their lower initial costs and minimal maintenance requirements make them attractive for utilities and industries looking to enhance their grid protection without significant capital expenditure. These characteristics have led to broad adoption across developed and developing regions, where upgrading and protecting aging infrastructure remains a top priority.

This category includes solid-state, inductive, and resistive FCLs, which are widely adopted due to their cost-effectiveness, technical simplicity, and proven reliability in conventional grid systems. Non-superconducting FCLs are especially preferred in developing regions where budget constraints and limited infrastructure make advanced technologies less feasible. Key trends in this segment include advancements in solid-state FCLs using power electronics and semiconductor-based switching, enabling faster response times and improved integration with smart grid systems. Manufacturers also focus on enhancing thermal management and compactness to cater to the growing needs of urban and industrial power networks.

The Superconducting Fault Current Limiter (SFCL) segment is expected to record the fastest CAGR of 7.5% from 2025 to 2030. As power grids become more complex with the integration of renewable energy sources and the expansion of urban infrastructure, the need for effective fault current management is becoming more critical. Non-superconducting fault current limiters are well-positioned to meet this demand due to their ability to handle a wide range of fault current levels and provide consistent performance in diverse environmental conditions. In addition, their compatibility with existing grid systems and ease of deployment make them a preferred choice for utilities aiming to enhance their network resilience quickly. As a result, the non-superconducting segment is likely to maintain its strong market presence and continue driving market growth.

Voltage Range Insights

The high-voltage segment held the largest revenue share in 2024. This segment's significant presence is primarily driven by the increasing demand for robust protection solutions in high-voltage power systems, which are integral to long-distance power transmission and large-scale industrial applications. As global energy consumption continues to rise, there is a growing need to expand and upgrade high-voltage transmission networks to accommodate greater loads and ensure efficient power distribution. High-voltage fault current limiters are essential in these systems as they protect critical infrastructure from the potentially catastrophic effects of fault currents, helping to maintain system stability and prevent widespread outages.

The medium-voltage segment is expected to record the fastest CAGR, driven by the expanding use of distributed energy resources (DERs) and microgrids and increasing industrial automation. These medium-voltage FCLs are used in secondary distribution networks, commercial facilities, and localized energy systems, where protection from medium-level fault currents is critical. Technological advancements are focused on building compact, modular FCL models with easier installation and integration into existing switchgear systems. As utilities and industries aim to improve operational flexibility and reduce outage risks, medium-voltage FCLs are becoming an essential component of modern power distribution architecture.

End-use Insights

The power stations end-use segment held the largest revenue share in 2024. This significant share is primarily due to the critical role of fault current limiters in enhancing the safety and reliability of power stations, which are central to generating and distributing electricity. Power stations, whether thermal, nuclear, or renewable, are highly susceptible to faults that can significantly damage equipment, cause extensive downtime, and lead to substantial financial losses. By integrating fault current limiters, power stations can protect their electrical infrastructure from the damaging effects of excessive fault currents, maintaining continuous operation and ensuring a stable power supply to the grid. The need to safeguard against faults becomes even more crucial as power generation facilities expand to meet rising global energy demands, further driving the adoption of fault current limiters in this segment.

The automotive segment is expected to grow over the forecast period, driven by the rapid electrification of vehicles and the evolution of high-voltage EV architectures. As electric vehicles (EVs) adopt higher voltage platforms, the risk of electrical faults increases, making fault current protection critical for safety and system longevity. Using FCLs in EVs and EV charging infrastructure helps manage fault currents efficiently and protect batteries, inverters, and onboard chargers. The development of compact, solid-state FCLs that can be integrated into electric drivetrains and fast-charging stations contributes to the segment's growth. With the global push for green mobility and increasing government support for EV adoption, the demand for advanced protection technologies in the automotive sector is expected to grow rapidly, contributing significantly to the overall FCL market expansion.

The power stations segment is expected to grow at a CAGR of 6.2% over the forecast period, fueled by several factors, including the global push for energy transition and the increasing reliance on diverse energy sources. As the energy sector shifts towards renewable energy and adopts newer technologies, there is a growing emphasis on upgrading existing power infrastructure to handle more complex and variable power flows. Power stations must be equipped with advanced fault current management solutions to accommodate the integration of renewables and the challenges associated with grid stability and protection. In addition, the need to modernize aging power plants in developed regions and develop new power generation facilities in emerging economies is creating a steady demand for fault current limiters. These devices help ensure operational efficiency and safety, reinforcing their importance in power stations worldwide and driving sustained growth in this market segment.

Regional Insights

North America fault current limiter market is expected to grow at a CAGR of 6.8% over the forecast period, driven by increasing investments in smart grid technology and the modernization of electrical infrastructure. With the region's aging power grid systems and rising electricity demand, there is a heightened need for advanced solutions to manage fault currents and enhance grid reliability. In addition, the integration of renewable energy sources and the expansion of distributed generation are contributing to the rising adoption of FCLs to protect grid components from potential damage caused by fault currents. Technological advancements in FCL design, such as the development of superconducting and solid-state limiters, are also expected to bolster market growth, offering utilities more efficient and cost-effective solutions to manage fault currents. As utilities focus on enhancing grid resilience and reducing outage times, the demand for FCLs in North America is likely to continue its upward trend.

U.S. Fault Current Limiter Market Trends

The U.S. fault current limiter market held the largest share in North America in 2024 due to its extensive transmission network, high energy consumption, and strong federal and state-level initiatives to modernize the power grid. Utilities in the U.S. are actively investing in smart grid technologies and advanced fault protection systems to reduce outage risks and improve energy efficiency. With a strong focus on integrating renewable energy sources and developing smart grid technologies, the U.S. market is expected to experience steady growth, supported by regulatory mandates aimed at improving grid resilience and safety.

Europe Fault Current Limiter Market Trends

The fault current limiter market in Europe is expanding due to stringent regulations on grid safety and the ongoing transition to renewable energy sources. Countries across the region are focused on upgrading their electrical infrastructure to meet climate goals and improve energy efficiency. The integration of fault current limiters is crucial for managing the variability and complexity of power flows associated with renewable energy integration. As Europe continues to advance its smart grid initiatives and increase investments in green energy projects, the demand for fault current limiters is expected to grow significantly.

The France fault current limiter market is characterized by its robust energy infrastructure and a strong commitment to nuclear and renewable energy. As a leading producer of nuclear energy, France requires reliable fault current management solutions to protect its nuclear power plants and associated infrastructure. In addition, the country's increasing investments in renewable energy sources, particularly offshore wind, are driving the need for advanced grid protection technologies. Fault current limiters play a vital role in ensuring the stability and safety of France's electrical network, supporting its energy transition goals.

Asia Pacific Fault Current Limiter Market Trends

This dominance is largely driven by the rapid industrialization and urbanization occurring across key countries like China, India, Japan, and South Korea, which are significantly expanding their power infrastructure to meet the growing energy demands. The region’s focus on enhancing grid reliability and safety has led to substantial investments in advanced technologies, including fault current limiters, to protect electrical networks from the risks associated with increased fault currents. Moreover, the Asia Pacific region is experiencing a surge in renewable energy projects, which necessitate the integration of sophisticated fault management solutions to ensure stable and efficient power distribution.

The China fault current limiter market held significant share in the Asia Pacific region in 2024. In China, the fault current limiter market is expanding rapidly due to the country's ambitious plans for grid modernization and renewable energy integration. As the world's largest producer and consumer of electricity, China faces significant challenges in managing fault currents in its vast and diverse electrical network. The government’s focus on building a strong and resilient power infrastructure, coupled with substantial investments in renewable energy projects, is driving demand for advanced fault current limiters. China's commitment to reducing carbon emissions and increasing energy efficiency is likely to further stimulate market growth.

Middle East & Africa Fault Current Limiter Market Trends

The fault current limiter market in the Middle East & Africa is expected to grow rapidly over the forecast period. The market in the Middle East & Africa is gaining traction as countries invest in expanding and modernizing their power grids. With a strong emphasis on diversifying energy sources and improving grid stability, especially in countries with rapid urban growth, there is a growing need for reliable fault current management solutions. In addition, the increasing deployment of renewable energy projects, particularly in solar and wind, is driving demand for fault current limiters to manage the unique challenges posed by integrating these energy sources into the grid.

The Saudi Arabia fault current limiter market is evolving as the country undertakes major initiatives to transform its power sector under its Vision 2030 strategy. With a focus on diversifying energy sources and enhancing grid reliability, Saudi Arabia is investing in advanced technologies to support the expansion of its power infrastructure. The development of large-scale renewable energy projects, such as solar and wind farms, necessitates the use of fault current limiters to ensure grid stability and safety. As the country continues to modernize its grid and integrate new energy sources, the demand for fault current limiters is expected to grow steadily.

Key Fault Current Limiter Company Insights

The market is fragmented, characterized by the presence of numerous players ranging from well-established multinational corporations to smaller specialized companies. This fragmentation is due to the diverse applications and technologies within the market, such as superconducting and non-superconducting fault current limiters, each catering to different segments of the power industry. In addition, regional variations in power grid infrastructure and differing regulatory environments contribute to the fragmented nature of the market, with different players focusing on specific regions or types of fault current limiter technology. As a result, no single company dominates the global market, allowing for competitive dynamics and opportunities for new entrants and technological innovations. Key companies are adopting several organic and inorganic growth strategies, such as facility expansion, mergers & acquisitions, and joint ventures, to maintain and expand their market share.

-

American Superconductor specializes in advanced superconducting technologies and has pioneered Superconducting Fault Current Limiters (SFCLs) for utility grids. The company continues to focus on expanding its smart grid product portfolio and has engaged in strategic collaborations to enhance grid reliability and efficiency.

-

Nexans, a key player in the FCL space, drives through its innovation in superconducting technologies tailored for the rail and power sectors. The company invests in R&D to commercialize advanced current-limiting solutions for high-demand urban and industrial electrical networks.

Key Fault Current Limiter Companies:

The following are the leading companies in the fault current limiter market. These companies collectively hold the largest market share and dictate industry trends.

- Rongxin Power Electronic Co., Ltd.

- Applied Materials, Inc.

- American Superconductor

- Alsto

- Nexans

- Superconductor Technologies Inc.

- ABB

- Alstom SA

- Zenergy Power Inc.

- Siemens

Recent Developments

-

In July 2024, Nexperia announced the latest additions to its power device portfolio: NPS3102A and NPS3102B electronic fuses (eFuses).

-

In June 2024, Nexans and SNCF Réseau announced a strategic alliance to deploy the world’s first superconducting fault current limiter for the rail sector.

-

In February 2024, COSEL Co., Ltd. launched a PDA series of AC/DC power supply, which includes inrush current limiting and further enhances reliability for industrial applications.

Fault Current Limiter Market Report Scope

Report Attribute

Details

Market size in 2024

USD 5.5 billion

Estimated market size in 2026

USD 6.2 billion

Projected market size by 2030

USD 8.0 billion

Growth Rate

CAGR of 6.7% from 2025 to 2030

Base year for estimation

2024

Historical data

2018 - 2023

Forecast period

2025 - 2030

Report updated

June 2025

Quantitative units

Revenue in USD million and CAGR from 2025 to 2030

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Type, voltage range, end-use, and region

Regional scope

North America, Europe, Asia Pacific, Latin America, MEA

Country scope

U.S.; Canada; Mexico; Germany; France; UK; Italy; Spain; Russia; China; India; Japan; South Korea; Brazil; Argentina; Saudi Arabia; South Africa; UAE

Key companies profiled

Rongxin Power Electronic Co., Ltd.; Applied Materials, Inc.; American Superconductor; Alsto; Nexans; Superconductor Technologies Inc.; ABB; Alstom SA, Zenergy Power Inc.; Siemens

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Fault Current Limiter Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2018 to 2030. For this study, Grand View Research has segmented the global fault current limiter market report based on type, voltage range, end use, and region:

-

Type Outlook (Revenue, USD Million, 2018 - 2030)

-

Superconducting

-

Non-Superconducting

-

-

Voltage Range Outlook (Revenue, USD Million, 2018 - 2030)

-

High

-

Medium

-

Low

-

-

End Use Outlook (Revenue, USD Million, 2018 - 2030)

-

Power Stations

-

Oil & Gas

-

Automotive

-

Paper Mills

-

Chemicals

-

Steel & Aluminum

-

-

Regional Outlook (Revenue, USD Million, 2018 - 2030)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

Russia

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

South Africa

-

UAE

-

-

About the Author(s)

Distribution & Utilities Research Team

Energy & Power · Distribution & UtilitiesThis report was authored by the distribution & utilities research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the distribution & utilities segment of the energy & power industry. All findings are based on proprietary energy & power databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.