- Home

- »

- Organic Chemicals

- »

-

Ferrous Sulfate Market Size And Share Report, 2026-2033GVR Report cover

![Ferrous Sulfate Market Size, Share & Trends Report]()

Ferrous Sulfate Market (2026 - 2033) Size, Share & Trends Analysis Report By Product (Anhydrous, Monohydrate, Heptahydrate), By Form (Solid, Liquid), By Application (Water & Wastewater Treatment, Agriculture, Animal Feed Additives, Pharmaceuticals & Nutraceuticals), By Region, And Segment Forecasts

Market Size, 2025

$2.4BMarket Estimate, 2026

$2.5BMarket Forecast, 2033

$3.3BCAGR, 2026–2033

4.0%Ferrous Sulfate Market Summary

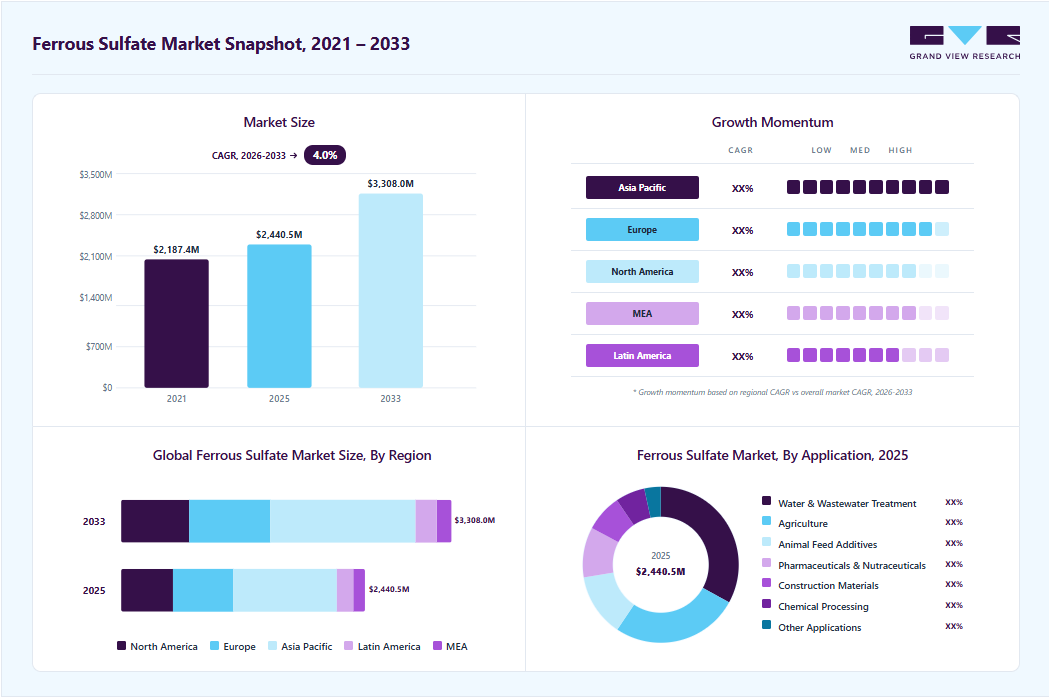

The global ferrous sulfate market size was valued at USD 2.4 billion in 2025 and is projected to grow from USD 2.5 billion in 2026 to USD 3.3 billion by 2033, at a CAGR of 4.0% from 2026 to 2033.Asia Pacific held the largest share of the market in 2025, accounting for 42.5% of revenue. The market is expanding steadily due to rising demand for cost-effective water treatment chemicals and micronutrient fertilizers.

Key Market Trends & Insights

- By product: Ferrous sulfate heptahydratesegment dominated the market, with a revenue share of 66.4% in 2025.

- By form: Solid segment held the largest market share of 84.4% in 2025..

- By application: Water and wastewater treatment segment led the market with the largest revenue share of 33.0% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (42.5% revenue share, 2025)

- The ferrous sulfate market in China dominated the Asia Pacific region.

Market Size & Forecast

- Market size in 2025: USD 2.4 Billion

- Estimated market size in 2026: USD 2.5 Billion

- Projected market size by 2033: USD 3.3 Billion

- CAGR (2026-2033): 4.0%

Its dual role as an environmental treatment agent and agricultural input creates stable, recurring consumption across essential sectors with limited substitution risk and strong regulatory alignment. Demand for ferrous sulfate continues to strengthen as wastewater treatment facilities require reliable coagulants for phosphate removal and sludge conditioning. Regulatory emphasis on cleaner discharge standards increases the need for iron based treatment chemicals that deliver predictable performance at competitive cost. Unlike many specialty chemicals, ferrous (Iron II) sulfate benefits from established process familiarity, straightforward storage, and scalable production. This combination supports consistent procurement cycles and long term supply agreements, which provide structural stability to the market.")

Agricultural applications also reinforce market expansion. Soil iron deficiency remains a recurring agronomic challenge, particularly in high intensity cropping systems. Iron II sulfate serves as an accessible micronutrient source that improves chlorophyll formation and crop vigor. Its affordability compared to chelated alternatives supports volume driven adoption in broad acre farming. Demand from animal feed and nutritional supplements adds another layer of stability, as iron fortification remains essential in maintaining livestock productivity and human health standards.

Market Dynamics

The ferrous sulfate market was driven by increasing utilization in water treatment and agricultural nutrient applications. Municipal and industrial water treatment facilities increasingly adopted ferrous sulfate for phosphate removal, odor control, and wastewater purification due to its cost efficiency and effectiveness in reducing contaminants. Growing investments in wastewater infrastructure and stricter environmental discharge standards further supported product demand across utility and industrial sectors.

Demand from the agriculture industry also strengthened market growth, particularly for soil conditioning and micronutrient supplementation. Ferrous sulfate continued to gain wider adoption in fertilizers and crop nutrition products to address soil iron deficiency and improve crop productivity. The expansion of agricultural activities and the increasing focus on improving soil health supported long-term consumption in emerging farming economies.

The market faced challenges due to fluctuations in raw material availability and production costs associated with steel pickling and iron processing operations. Variability in steel industry output directly affected the consistency of ferrous sulfate supply, creating pricing pressure for manufacturers and end users. Transportation and logistics costs also affected profitability, particularly in bulk industrial applications.

Ferrous sulfate requires controlled storage and handling conditions due to its moisture sensitivity and tendency to oxidize. Product degradation during storage reduced shelf stability and increased operational complexity for distributors and industrial users. These limitations increased inventory management costs and reduced the efficiency of long-distance transportation in certain regions.

Market Concentration & Characteristics

The ferrous sulfate market exhibits moderate concentration, with a mix of integrated chemical producers and regional manufacturers operating alongside smaller specialty suppliers. This structure exists because production is often linked to established industrial processes, enabling large companies to leverage scale efficiencies, while localized demand for water treatment and agriculture allows regional players to remain competitive.

The market is characterized by price sensitivity, standardized product specifications, and stable long term demand patterns. These characteristics arise because iron II sulfate is widely used in essential applications where performance requirements are well defined and substitution options are limited. Buyers typically prioritize reliability, regulatory compliance, and consistent supply over product differentiation, which reinforces steady procurement cycles and predictable consumption behavior.

Product Insights

Ferrous sulfate heptahydrate led the market in 2025 with 66.4% of total revenue due to its widespread availability and cost efficiency. The material is commonly produced as a co product in established industrial processes, enabling competitive pricing and high volume supply. Its suitability for water treatment and agricultural soil applications supports consistent bulk consumption. The crystalline form dissolves easily, making it practical for dosing and blending. These functional advantages, combined with lower processing requirements compared to other forms, reinforce its dominant commercial position.

Anhydrous ferrous sulfate is projected to grow at a CAGR of 4.6% from 2026 to 2033, outpacing other hydrate forms due to its higher iron concentration and lower moisture content. The absence of water improves storage stability and reduces transportation weight per unit of active iron, enhancing cost efficiency in controlled formulations. Demand is increasing in chemical processing, specialty applications, and precision dosing systems where moisture sensitivity matters. As industries focus on optimized formulations and material efficiency, anhydrous grades are gaining incremental adoption.

Form Insights

The solid segment dominated the ferrous sulfate market in 2025, representing 84.4% of total revenue, due to its broad suitability across agriculture, feed additives, pharmaceuticals, and industrial processing. Solid forms such as crystals, granules, and powders offer longer shelf life and easier storage compared to liquid solutions, reducing handling complexity for bulk buyers. They also support flexible downstream use since solids can be transported economically and dissolved at the point of application. This versatility and cost advantage sustain strong purchasing volumes across multiple end use industries.

The liquid segment is forecast to expand at a CAGR of 4.3% from 2026 to 2033, driven by increasing adoption in municipal and industrial water treatment operations. Liquid ferrous sulfate improves dosing accuracy and reduces preparation time, making it suitable for automated treatment systems. It also minimizes dust generation and handling losses associated with powders, improving operational safety. As wastewater treatment plants focus on process efficiency and consistent chemical feed performance, demand for liquid formulations is rising. This shift supports faster growth despite liquids holding a smaller revenue base in 2025.

Application Insights

The water and wastewater treatment segment accounted for 33.0% of total revenue in 2025, making it the leading application area for iron II sulfate. Its strong position reflects consistent demand for phosphate removal, odor control, and sludge conditioning in municipal and industrial treatment systems. Iron II sulfate remains a preferred coagulant due to its cost efficiency and reliable performance in reducing contaminants. Treatment facilities operate on continuous procurement cycles, which ensures recurring consumption. Regulatory compliance requirements further reinforce sustained demand, supporting the segment’s dominant revenue contribution.

The pharmaceuticals and nutraceuticals segment is projected to expand at a CAGR of 4.7% from 2026 to 2033, outpacing other application areas. Iron II sulfate is widely used in oral iron supplements and therapeutic formulations to address iron deficiency. Increasing health awareness and preventive supplementation practices are strengthening demand for regulated, high purity grades. Compared to bulk industrial uses, this segment generates higher value per unit volume, contributing to faster revenue growth. Ongoing product innovation in dosage forms and fortified products further supports sustained expansion through the forecast period.

Regional Insights

Asia Pacific accounted for 42.5% of global revenue in 2025 due to its strong demand from water treatment, agriculture, and industrial chemical processing. The region has a large base of fertilizer consumption and expanding wastewater management needs, supporting steady use of iron II sulfate. In addition, the presence of large scale chemical and titanium dioxide industries improves product availability and cost competitiveness, strengthening adoption across bulk end use sectors.

China ferrous sulfate market holds a significant position in the global market due to its large scale chemical manufacturing base and strong fertilizer consumption. Extensive industrial effluent treatment requirements sustain demand for iron based coagulants. The presence of major titanium dioxide and steel production operations enhances availability of ferrous sulfate as a co product, improving cost competitiveness. Continued investment in wastewater infrastructure and agricultural productivity supports both volume expansion and sustained domestic consumption.

North America Ferrous Sulfate Market Trends

The North America ferrous sulfate market is driven primarily by established municipal wastewater infrastructure and steady demand from agriculture and industrial processing. A significant portion of consumption comes from regulated water treatment facilities that require reliable coagulants for phosphate and odor control. The region also benefits from stable chemical manufacturing capacity and well developed distribution networks, ensuring consistent product availability. Demand from animal feed and specialty chemical applications contributes to incremental volume growth, supporting moderate but steady market expansion.

U.S. ferrous sulfate market represents the core of the North American market due to its large municipal water treatment footprint and structured environmental compliance framework. Public utilities rely on iron based salts for nutrient removal and sludge conditioning, creating recurring procurement cycles. The country also has established domestic production linked to industrial by products, supporting competitive pricing and supply security. In addition, consistent demand from agriculture and pharmaceutical supplement manufacturing strengthens the overall consumption base.

Europe Ferrous Sulfate Market Trends

Europe is forecast to expand at a CAGR of 3.8% from 2026 to 2033, supported by stable demand from municipal wastewater treatment and industrial discharge control. The region’s strict environmental standards encourage continued use of iron based coagulants for phosphate removal and sludge conditioning. Growth is also supported by consistent demand for agricultural micronutrients and pharmaceutical grade iron supplements. A mature chemical supply chain and focus on sustainable material utilization further reinforce market expansion.

Germany ferrous sulfate market demand is closely tied to its advanced wastewater treatment systems and strong environmental standards. The country emphasizes phosphorus removal and efficient sludge management, supporting sustained coagulant usage. Germany’s mature chemical industry also facilitates stable supply and integration into industrial applications such as material processing and construction additives. Agricultural micronutrient demand remains consistent, particularly in specialized crop production, reinforcing balanced and stable market growth.

Latin America Ferrous Sulfate Market Trends

The Latin America market is influenced by expanding municipal wastewater projects and growing agricultural activity. Iron II sulfate is widely used as a micronutrient in crop cultivation, particularly in regions with intensive farming practices. Improvements in industrial discharge standards are gradually increasing demand for coagulants in treatment facilities. While the market base is smaller compared to developed regions, infrastructure development and agricultural modernization support gradual growth momentum.

Middle East & Africa Ferrous Sulfate Market Trends

The Middle East and Africa market is shaped by increasing focus on water resource management and agricultural productivity. Many countries are strengthening wastewater treatment capacity to improve environmental protection and water reuse practices. Iron II sulfate is adopted in municipal and industrial treatment systems due to its cost effectiveness. Expanding fertilizer use to enhance crop yields in arid and semi-arid conditions also contributes to steady demand growth across the region.

Key Ferrous Sulfate Company Insights

The two key dominant manufacturers in the market are Venator Materials PLC and KRONOS Worldwide, Inc.

-

Venator Materials PLC is a global chemical producer with integrated operations linked to titanium dioxide manufacturing, from which ferrous sulfate is generated as a co product. The company benefits from established process infrastructure and large scale production capabilities. Its portfolio supports applications in water treatment, agriculture, and industrial processing, reinforcing its position through operational efficiency and diversified end use integration.

-

KRONOS Worldwide, Inc. operates large scale pigment manufacturing facilities where iron based sulfate materials are generated through controlled processing streams. The company leverages its vertically integrated production model to maintain consistent output quality. Its ferrous sulfate portfolio serves environmental treatment and industrial applications, supported by strong manufacturing expertise and long standing presence in inorganic chemical production.

Key Ferrous Sulfate Companies:

The following key companies have been profiled for this study on the ferrous sulfate market.

- Crown Technology, Inc.

- Rech Chemical Co. Ltd.

- Venator Materials PLC

- Coogee Chemicals Pty Ltd

- Chemland Group

- Pencco, Inc.

- KRONOS Worldwide, Inc.

- Kemira Oyj

- Guangxi Jintao Titanium Co. Ltd.

- Hong Yield Chemical Industrial Co., Ltd.

- Kemira Oyj

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weakness

Mature Players: Kemira Oyj; Venator Materials PLC; KRONOS Worldwide, Inc.; Pencco, Inc.; Coogee Chemicals Pty Ltd.

- Mature players focused on strengthening supply agreements with water treatment, agriculture, and industrial customers.

- Companies emphasized large-scale production integration with titanium dioxide and steel processing operations to improve raw material efficiency.

- Strategic investments were directed toward product quality improvement and environmental compliance across industrial applications.

- Mature participants benefited from strong manufacturing infrastructure and stable raw material sourcing capabilities.

- Broad customer presence across water treatment, fertilizers, pigments, and industrial chemicals strengthened market positioning.

- Established distribution channels and technical expertise supported consistent product supply and quality assurance.

- Dependence on steel and titanium dioxide industry by-products exposed operations to raw material supply fluctuations.

- Environmental compliance and waste management requirements increased operational costs.

- Large production structures reduced flexibility in addressing smaller regional demand variations.

Emerging Players: Crown Technology, Inc.; Rech Chemical Co. Ltd.; Chemland Group; Guangxi Jintao Titanium Co. Ltd.; Hong Yield Chemical Industrial Co., Ltd.

- Emerging companies concentrated on cost-competitive production and regional market expansion.

- Focus remained on supplying ferrous sulfate for agriculture, wastewater treatment, and industrial processing applications.

- Companies increasingly relied on localized distribution partnerships and export-focused strategies.

- Regional manufacturers benefited from lower operating costs and flexible production capabilities.

- Faster response to local customer requirements supported stronger regional relationships.

- Competitive pricing strengthened penetration in cost-sensitive agricultural and industrial segments.

- Limited international presence and weaker brand recognition restricted global expansion opportunities.

- Lower investment capacity in advanced processing and environmental technologies limited premium product development.

- Dependence on regional industrial activity increased exposure to local economic fluctuations.

Recent Developments

-

In October 2025, Agrigem introduced Easy Flow Soluble Iron Sulphate and Premier Soluble Iron Sulphate to improve turf greening and correct iron deficiency in lawns. The launch expands soluble ferrous sulfate offerings, marking a product development within the agricultural and horticultural segment of the market.

-

In May 2025, Russian Vitriol Company opened a new ferrous sulfate monohydrate production plant in Bashkortostan using fully domestic feedstock, aiming to produce up to 3,600 tonnes annually and reduce previous reliance on Chinese imports.

Ferrous Sulfate Market Report Scope

Report Attribute

Details

Market size in 2025

USD 2.4 Billion

Estimated market size in 2026

USD 2.5 Billion

Projected market size by 2033

USD 3.3 Billion

Growth rate

CAGR of 4.0% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2025 - 2033

Quantitative units

Revenue in USD million/billion, volume in kilotons, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product, form, application, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; UK; Italy; Spain; France; China; Japan; South Korea; Brazil; Argentina; Saudi Arabia; South Africa

Key companies profiled

Crown Technology, Inc.; Rech Chemical Co. Ltd.; Venator Materials PLC; Coogee Chemicals Pty Ltd; Chemland Group; Pencco, Inc.; KRONOS Worldwide, Inc.; Kemira Oyj; Guangxi Jintao Titanium Co. Ltd.; Hong Yield Chemical Industrial Co., Ltd.

Customization scope

Free report customization (equivalent to up to 8 analysts’ working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Ferrous Sulfate Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global ferrous sulfate market report based on product, form, application, and region

-

Product Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Anhydrous

-

Monohydrate

-

Heptahydrate

-

-

Form Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Solid

-

Liquid

-

-

Application Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Water & Wastewater Treatment

-

Agriculture

-

Animal Feed Additives

-

Pharmaceuticals & Nutraceuticals

-

Construction Materials

-

Chemical Processing

-

Other Applications

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

Italy

-

Spain

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Regional Segmentation

A detailed regional assessment of the ferrous sulfate market was conducted across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa, with country-level analysis covering production capacity, consumption trends, wastewater treatment investments, agricultural micronutrient demand, and industrial manufacturing activity. The study further evaluated regional regulatory frameworks associated with water treatment chemicals and soil nutrient management.

Enabled identification of high-demand regional markets and emerging consumption centers linked to agriculture and municipal water treatment expansion. Supported regional expansion planning, localization strategies, and prioritization of countries with strong infrastructure and environmental investment activity.

Cross-Segmentation Analysis

A comprehensive cross-segmentation analysis was performed by simultaneously examining product type, form, and application. The assessment evaluated adoption trends for heptahydrate ferrous sulfate in water treatment, monohydrate variants in animal feed additives, and liquid ferrous sulfate in industrial processing applications. Demand patterns across agriculture, pharmaceuticals, construction materials, and chemical processing industries were also assessed.

Assisted in identifying high-growth product-application combinations and niche industrial opportunities across the ferrous sulfate value chain. Facilitated more targeted product positioning, portfolio optimization, and commercialization planning based on end-use demand dynamics.

Opportunity Assessment

An opportunity-focused assessment was conducted to evaluate the potential future demand for ferrous sulfate in wastewater treatment, micronutrient fertilizers, animal nutrition, pharmaceutical formulations, and construction materials applications. The analysis further examined the impact of environmental regulations, soil nutrient management programs, and infrastructure development activities on long-term product adoption.

Helped identify emerging application areas and long-term growth opportunities across environmental and agricultural sectors. Supported strategic investment planning, product diversification initiatives, and expansion into high-potential industrial applications.

Frequently Asked Questions About This Report

The global ferrous sulfate market size was estimated at USD 2.4 billion in 2025 and is expected to reach USD 2.5 billion in 2026.

The global ferrous sulfate market is expected to grow at a compound annual growth rate of 4.0% from 2026 to 2033, reaching USD 3.3 billion by 2033.

Some of the key players operating in the ferrous sulfate market include Crown Technology, Inc., Rech Chemical Co. Ltd., Venator Materials PLC, Coogee Chemicals Pty Ltd, Chemland Group, Pencco, Inc., KRONOS Worldwide, Inc., Kemira Oyj, Guangxi Jintao Titanium Co., Ltd., Hong Yield Chemical Industrial Co., Ltd.

The market is expanding steadily due to rising demand for cost effective water treatment chemicals and micronutrient fertilizers. Its dual role as an environmental treatment agent and agricultural input creates stable, recurring consumption across essential sectors with limited substitution risk and strong regulatory alignment.

Asia Pacific accounted for 42.5% of global revenue in 2025 due to its strong demand from water treatment, agriculture, and industrial chemical processing.

The solid segment dominated the ferrous sulfate market in 2025, representing 84.4% of total revenue, due to its broad suitability across agriculture, feed additives, pharmaceuticals, and industrial processing.

The water and wastewater treatment segment accounted for 33.0% of total revenue in 2025 and pharmaceuticals and nutraceuticals segment is fastest segment to expand at a CAGR of 4.7% from 2026 to 2033

Ferrous sulfate heptahydrate led the market in 2025 with 66.4% while anhydrous ferrous sulfate is projected to grow at a CAGR of 4.6% from 2026 to 2033.

About the Author(s)

Organic Chemicals Research Team

Bulk Chemicals · Organic ChemicalsThis report was authored by the organic chemicals research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the organic chemicals segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.