- Home

- »

- Advanced Interior Materials

- »

-

Fire Protection System Market Size, Share Report 2026-2033GVR Report cover

![Fire Protection System Market (2026 - 2033)Report]()

Fire Protection System Market (2026 - 2033)

Size, Share & Trends Analysis Report By Component (Product, Service) By Application (Commercial, Industrial, Residential), By Region (North America, Europe, Asia Pacific, Latin America, Middle East & Africa), And Segment Forecasts

Market Size, 2025

$94.9BMarket Estimate, 2026

$101.2BMarket Forecast, 2033

$156.2BCAGR, 2026–2033

6.4%Fire Protection System Market Summary

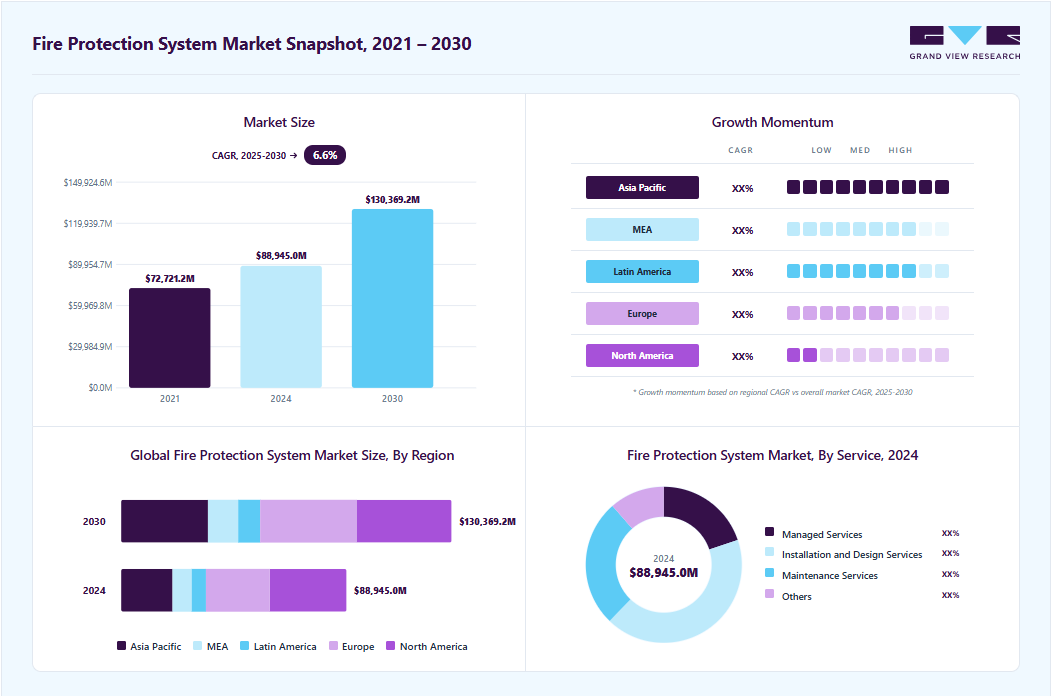

The global fire protection system market size was valued at USD 94.9 billion in 2025 and is projected to grow from USD 101.2 billion in 2026 to USD 156.2 billion by 2033, at a CAGR of 6.4% from 2026 to 2033. North America held the largest global revenue share of 34.9% in 2025. With the introduction of strict fire prevention and control requirements by governments throughout the world, the need for fire detection systems in commercial applications across facilities, including hospitals, educational institutions, and government offices, is growing.

Key Market Trends & Insights

- Based on component: Products held the largest revenue share of 73.0% in 2025.

- Based on application: Commercial held the largest revenue share of 46.4% in 2025.

Regional Highlights

- Largest regional market: North America (34.9% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 94.9 Billion

- Estimated market size in 2026: USD 101.2 Billion

- Projected market size by 2033: USD 156.2 Billion

- CAGR (2026-2033): 6.4%

The demand for fire alarm and detection systems in the commercial application is predicted to increase as a result of rising investments made by businesses in protecting infrastructure and minimizing the loss of property and life across various applications. The market is also anticipated to be driven by factors such as the easy availability of technologically advanced equipment and sophisticated networking capabilities that enable effective communication between fire detection solutions and fire suppression systems. However, the coronavirus pandemic and lockdowns have unquestionably affected the market for fire alarms and detection systems.")

The relatively mature market is likely to be driven by the rising number of laws and regulations mandating the installation of fire safety equipment across several industries and sectors over the forecast period. Factors such as the easy availability of technologically advanced equipment and networking capabilities that enable efficient communication between fire detection and fire suppression solutions are also expected to drive the market. The rising use of the Internet of Things (IoT) technology for interconnecting a variety of devices or objects in smart building systems, increasing demand for analyzing fire and security risks associated with a building through research before building structure design, and the continuing need for communicating with building occupants in emergencies are some of the key trends driving industry demand.

Stringent fire safety regulations and standards mandating the installation of fire safety equipment in residential and commercial areas in several countries are also likely to boost market growth. For instance, In-duct smoke detection NFPA Standard 90A and the three model Mechanical Codes developed by the model building code groups BOCA, ICBO, and SBCCI, all require smoke detectors to be installed in certain ducts of building HVAC systems so these systems can automatically shut down during fires. The market is also likely to benefit from advancements in wireless sensor networks and the growing adoption of wireless fire-sensing devices. Growing awareness of fire hazards, along with a substantial rise in infrastructure development, are also expected to be high-impact growth drivers. Organizations across the globe are increasingly spending on the safety and security of infrastructure to reduce human losses. Implementation of fire safety codes for building and renovation activities is further expected to stimulate the demand for fire safety equipment across the globe.

Safeguarding inventory, infrastructure, and human lives from major losses due to fire can be effectively achieved by implementing fire protection systems such as fire alarm & detection systems. However, the cost associated with installing such advanced fire alarm & detection systems is relatively high as they are custom-designed and installed as per specific requirements. For instance, the systems installed in a hospital will vary considerably from the ones installed in a kitchen or a data center. Such varied needs contribute to the high overall cost of fire protection systems. Additionally, with the development of sensor technologies and the consecutive introduction of smart wireless systems, electronic service usage in fire protection devices has significantly increased. These improved devices have heightened sensitivity and respond quickly to emergencies. As they are manufactured with high precision and enhanced materials, the cost of these services and systems is high.

Market Dynamics

The fire protection system market continues to grow due to increasingly stringent fire safety regulations, rapid urbanization, expanding commercial and industrial infrastructure, and heightened awareness of life and asset protection. Fire protection systems—including fire detection, alarm, suppression, sprinkler, and emergency response solutions—help prevent fire-related fatalities, minimize property damage, ensure business continuity, and support regulatory compliance across residential, commercial, and industrial facilities. Rising investments in smart buildings, data centers, manufacturing plants, healthcare facilities, and transportation infrastructure are further driving the adoption of advanced fire protection technologies. Additionally, the rising incidence of fire hazards, the growing emphasis on workplace safety, and the integration of IoT-enabled monitoring and automated fire suppression solutions are accelerating demand for comprehensive fire protection systems worldwide.

The increasing demand for intelligent and integrated fire safety solutions is significantly driving the growth of the fire protection system market by enabling organizations to enhance fire prevention, detection, and emergency response capabilities. Building owners and facility managers are increasingly seeking customized fire protection systems that address specific operational risks, regulatory requirements, and infrastructure characteristics across commercial, industrial, residential, and institutional facilities. In response, manufacturers and solution providers are offering modular fire detection, alarm, suppression, and monitoring systems that can be tailored to diverse end-user needs. The growing adoption of smart buildings, coupled with rising awareness of fire safety risks and the need for real-time monitoring, is further accelerating the deployment of advanced, IoT-enabled fire protection solutions. As businesses prioritize asset protection, occupant safety, and regulatory compliance, demand for flexible and technologically advanced fire protection systems continues to increase across global markets.

The high cost associated with the installation, maintenance, and periodic upgrading of fire protection systems is a key factor restraining the growth of the fire protection system market. Advanced fire detection, alarm, suppression, and monitoring systems often require significant upfront investments, particularly in large commercial, industrial, and critical infrastructure facilities. In addition to installation expenses, ongoing costs related to system inspections, testing, maintenance, and regulatory compliance can place a substantial financial burden on end users. Small and medium-sized enterprises (SMEs) and building owners in cost-sensitive markets may delay or limit investments in comprehensive fire protection solutions due to budget constraints. Furthermore, the complexity of integrating modern fire protection systems with existing building infrastructure can increase implementation costs, thereby limiting adoption rates in certain regions and end-use sectors.

The growing adoption of smart buildings and connected infrastructure is creating significant growth opportunities for the fire protection system market. Building owners and facility managers are increasingly investing in IoT-enabled fire detection, monitoring, and suppression solutions that provide real-time data, predictive maintenance capabilities, and faster emergency response. The integration of fire protection systems with building management systems (BMS), artificial intelligence (AI), and cloud-based monitoring platforms enhances operational efficiency while improving occupant safety and regulatory compliance. Additionally, the expansion of data centers, healthcare facilities, transportation hubs, and high-rise commercial developments is driving demand for advanced fire safety technologies capable of protecting complex and mission-critical environments. As organizations continue to prioritize digital transformation and proactive risk management, the adoption of intelligent fire protection systems is expected to generate substantial market growth opportunities over the coming years.

Market Concentration & Characteristics

The fire protection system market is moderately consolidated, with several multinational fire safety solution providers, building technology companies, and specialized fire protection equipment manufacturers accounting for a significant share of the market. Leading players compete based on product reliability, technological innovation, regulatory compliance expertise, service capabilities, distribution reach, and comprehensive fire safety portfolios. Major companies maintain strong market positions through extensive product offerings spanning fire detection, alarm, suppression, sprinkler, and emergency communication systems, supported by established installation and maintenance networks across multiple regions.

Strategic partnerships, acquisitions, technology integrations, and geographic expansion initiatives are commonly observed across the industry as companies seek to strengthen their market presence and enhance end-to-end fire safety capabilities. The market also benefits from long-term service contracts, inspection services, and system upgrades, which contribute to recurring revenue streams and customer retention. While global players dominate large-scale commercial, industrial, and infrastructure projects, regional manufacturers and service providers maintain a strong presence in local markets through cost-effective solutions and compliance with country-specific fire safety regulations.

Analyst Perspective

The fire protection system market continues to benefit from increasingly stringent fire safety regulations, rapid urbanization, expanding commercial and industrial infrastructure, and growing awareness regarding life safety and asset protection. Rising investments in smart buildings, data centers, manufacturing facilities, healthcare infrastructure, and transportation networks are driving demand for advanced fire detection, suppression, sprinkler, and emergency response solutions. However, high installation and maintenance costs, complex regulatory compliance requirements, integration challenges within existing infrastructure, and budget constraints among small and medium-sized enterprises may influence the pace of market adoption. Nevertheless, ongoing advancements in IoT-enabled monitoring, AI-based fire analytics, cloud-connected safety platforms, and predictive maintenance technologies are expected to create significant growth opportunities across both developed and emerging markets.

Component Insights

The product segment led the fire protection system industry, accounting for a revenue share of 73.0% in 2025, driven by increasing implementation of stringent fire safety regulations across residential, commercial, industrial, and institutional facilities. Governments and regulatory authorities worldwide are mandating the installation of fire detection, alarm, suppression, and sprinkler systems to improve occupant safety and reduce property losses. Additionally, rapid urbanization, the growth of smart buildings, the expansion of manufacturing facilities, data centers, and critical infrastructure projects are accelerating demand for advanced fire protection equipment. Continuous technological advancements in sensors, wireless communication, and intelligent fire detection solutions are further supporting growth within the product segment.

The services segment is expected to grow at a significant CAGR from 2026 to 2033. The service segment is experiencing strong growth due to the increasing need for regular inspection, testing, maintenance, and upgrading of fire protection systems to ensure operational reliability and regulatory compliance. Fire safety standards often require periodic system assessments and certification, creating recurring demand for professional services. Furthermore, aging infrastructure and the growing installation base of fire protection systems are driving demand for retrofit and modernization services. The adoption of connected fire protection solutions and remote monitoring technologies is also increasing the need for specialized technical support, predictive maintenance, and lifecycle management services, contributing to sustained growth in the service segment.

Product Insights

The fire detection systems segment led the fire protection system industry, accounting for a revenue share of 58.1% in 2025. The detection system comprises several devices working collectively to detect and warn people through audio and video appliances during incidents involving fire, smoke, carbon monoxide, or other emergencies. Legislative requirements across countries, including the National Fire Protection Association in the USA and the Building Code of Australia, mandate the installation of fire detection devices, thereby bolstering demand for these devices.

Fire suppression systems are used for the reduction of heat release of a fire and the deterrence of its re-growth by means of sufficient and direct application of water or other materials, such as dry chemical powder, among others, through the fire plume to the burning fuel surface. The increasing adoption of environment friendly fire suppression agents is expected to trigger the demand for these equipment. The growing pace of construction of commercial units and industrialization is expected to open lucrative growth opportunities for the fire suppression system market. Moreover, developments and renovations of new infrastructure in recent years require obligatory fire safety codes issued by the government. The players in this region are expected to invest in the market owing to fire safety obligations and regulations.

Service Insights

The installation and design service segment accounted for the largest share of the global fire protection system industry in 2025. Installation and design services refer to the practice of outsourcing the design, development, upgrades, documentation, and installation processes for the fire protection system. Fire protection systems are being installed across buildings of all sizes as inhabitants increasingly understand the benefits they offer in small, mid-size, and large buildings. Furthermore, installation and design services are increasingly preferred due to the subject-matter expertise vendors offer. This is driving the demand for installation and design services in the market.

The maintenance services segment is expected to grow at the fastest CAGR of 6.5% from 2026 to 2033. Fire protection systems play a vital role in detecting and alerting people in the event of smoke or fire; however, any fault in the system may lead to accidents and asset losses. Therefore, regular maintenance is necessary to reduce the risks of failure and extend the life of the system. Maintenance service includes timely audit and service of fire protection equipment to ensure that fire protection systems meet all the essential fire safety standards during an emergency.

Application Insights

The commercial application segment dominated the fire protection system market, accounting for the largest revenue share in 2025. The commercial application segment comprises applications for retail, BFSI, government, healthcare, telecom & IT, and educational institutions. The demand for fire protection systems in commercial applications is increasing due to the formulation of stringent government rules for fire prevention and control across the globe. Furthermore, increasing investments by companies to reduce the loss of property and life and safeguard the infrastructure is expected to fuel the demand for fire protection systems.

The industrial application segment is expected to register the highest CAGR from 2026 to 2033. The industrial application covers major sectors such as oil and gas, mining, energy and power, and manufacturing. The need to safeguard automated systems from fire accidents is expected to fuel the growth of the segment. Furthermore, in the fire-prone sector, the emphasis is on installing complete proof protection and prevention systems in the industries and on stringent government rules. This is expected to further drive the industrial segment.

Regional Insights

North America dominated the fire protection system market with the largest revenue share of 34.9% in 2025. This can be attributed to the rising demand for intelligent houses and smart buildings that deliver optimal safety. Furthermore, North America has a strong presence of fire protection system manufacturers, including Raytheon Technologies Corporation, GENTEX CORPORATION, and Honeywell International Inc. These companies are actively raising awareness through marketing programs about fire protection systems.

U.S. Fire Protection System Market Trends

The U.S. fire protection system industry is anticipated to register significant growth from 2026 to 2033. The market growth is driven by stringent fire safety regulations enforced by authorities such as the National Fire Protection Association (NFPA) and local building codes. Growing investments in commercial buildings, industrial facilities, healthcare infrastructure, and data centers are increasing demand for advanced fire detection and suppression systems. The rising frequency of wildfires and climate-related fire risks is also encouraging property owners to strengthen fire safety measures. Furthermore, the adoption of smart building technologies and IoT-enabled fire protection solutions is accelerating system upgrades across both new and existing facilities.

Europe Fire Protection System Market Trends

The Europe fire protection system industry is poised for significant growth from 2026 to 2033. The market growth is primarily driven by strict fire safety standards, increasing renovation activities, and growing investments in sustainable building infrastructure. Governments across the region are emphasizing occupant safety and compliance with evolving fire protection regulations. The modernization of aging commercial and industrial facilities is creating demand for advanced fire detection and suppression technologies. Additionally, increasing deployment of smart buildings and integrated building management systems is driving adoption of intelligent fire protection solutions.

The UK fire protection system market is expected to grow significantly in the coming years. The market is benefiting from heightened focus on building safety and fire risk management following major regulatory reforms. Stricter requirements for fire detection, alarm systems, and passive fire protection measures are encouraging investments across residential and commercial buildings. The growth of high-rise construction projects and public infrastructure developments is further supporting market expansion. Additionally, property owners are increasingly upgrading legacy fire safety systems to comply with evolving regulations and improve occupant protection.

Asia Pacific Fire Protection System Market Trends

The Asia Pacific fire protection system industry is poised for fastest growth from 2026 to 2033, driven by the fact that manufacturing facilities, automotive plants, logistics centers, and chemical processing sites are investing heavily in advanced fire detection and suppression systems to ensure operational continuity and asset protection. The country's growing adoption of Industry 4.0 technologies is driving demand for integrated, automated fire safety solutions.

The China fire protection system market held a substantial share in 2025. The market is expanding due to rapid urbanization, increasing construction activities, and significant investments in commercial and industrial infrastructure. Government initiatives aimed at strengthening public safety standards are driving the installation of advanced fire protection systems across residential complexes, manufacturing facilities, transportation hubs, and public buildings. The rapid growth of data centers, electronics manufacturing, and smart city projects is creating additional demand for intelligent fire safety solutions.

The fire protection system market in India accounted for a substantial revenue share in 2025. The market is witnessing strong growth driven by rapid urban development, industrial expansion, and increased investments in commercial real estate. Government regulations on fire safety compliance in high-rise buildings, healthcare facilities, educational institutions, and industrial plants are driving the installation of systems.

Key Fire Protection System Company Insights

Major players are adopting strategic initiatives and undertaking measures to gain benefits from the opportunities in the emerging market. The key companies in the market have launched new advanced products to meet the evolving customer needs. For instance, in August 2022,Honeywell announced the launch of the Morley MAx fire detection and alarm system. It enhances occupant and building safety. A highly sophisticated range of capabilities that are simple to install, commission, and maintain is offered to installers and end users by the small, powerful, performance-driven intelligent fire alarm control panel.

-

Johnson Controls has established itself as a leading player in the fire protection system market through its comprehensive portfolio of fire detection, alarm, suppression, and integrated building safety solutions. The company leverages its expertise in smart buildings and connected infrastructure to deliver advanced fire protection systems across commercial, industrial, healthcare, education, and critical infrastructure sectors. Johnson Controls continues to invest in digital fire safety technologies, cloud-based monitoring platforms, and integrated building management systems to enhance real-time threat detection, operational efficiency, and regulatory compliance. The company's strong focus on intelligent building ecosystems, lifecycle service offerings, and sustainable infrastructure solutions has further strengthened its position in the global fire protection market.

-

Honeywell International is a prominent participant in the fire protection system industry, offering a wide range of fire detection, alarm, emergency communication, and life-safety solutions for residential, commercial, and industrial applications. The company is focused on advancing connected fire safety technologies through the integration of IoT, cloud connectivity, artificial intelligence, and building automation platforms. Honeywell continues to expand its portfolio of intelligent fire protection solutions designed to improve situational awareness, accelerate emergency response, and support compliance with evolving fire safety regulations. Its emphasis on digital transformation, smart building integration, predictive maintenance capabilities, and global service networks has enabled the company to strengthen customer engagement and maintain a competitive position in the rapidly evolving fire protection industry.

Key Fire Protection System Companies:

The following key companies have been profiled for this study of the fire protection system market.

-

Honeywell International, Inc.

-

Johnson Controls

-

Raytheon Technologies Corporation

-

GENTEX CORPORATION

-

Siemens

-

Robert Bosch GmbH

-

Halma plc

-

Eaton

-

Iteris, Inc.

-

Hitachi Ltd.

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: Johnson Controls; Honeywell International, Inc.; Raytheon Technologies Corporation

- Focus on providing end-to-end fire protection solutions, including fire detection, alarm, suppression, emergency communication, and integrated building safety systems.

- Invest heavily in smart building technologies, IoT-enabled monitoring, cloud-based fire management platforms, and predictive maintenance capabilities.

- Strong global presence supported by extensive distribution, installation, and service networks.

- Broad product portfolios and proven compliance with international fire safety standards and regulations.

- Significant R&D capabilities enabling continuous innovation in intelligent fire protection technologies.

- High operational complexity due to large product portfolios and global service operations.

- Dependence on construction, infrastructure, and capital expenditure cycles for new system installations.

- Longer decision-making processes and higher organizational overhead compared to smaller competitors.

Emerging Players: Halma plc; Eaton

- Focus on specialized fire detection, suppression, alarm control, and niche life-safety applications.

- Greater flexibility and faster product development cycles compared to large multinational competitors.

- Strong expertise in niche technologies and application-specific fire protection requirements.

- Limited geographic reach and brand recognition relative to global market leaders.

- Smaller service and distribution networks can restrict large-scale project opportunities

Recent Developments

-

In January 2026, Halma plc acquired Safetec srl, an Italy-based provider of integrated fire and gas safety systems for industrial markets. Safetec srl specializes in customized fire detection and hazard monitoring solutions for high-risk environments, such as oil & gas and manufacturing. The acquisition strengthens Halma’s plc industrial fire protection capabilities and expands its portfolio of integrated safety systems.

-

In July 2025, Honeywell International, Inc. acquired Li-ion Tamer, an early detection technology that identifies lithium-ion battery thermal runaway risks before a fire starts. The solution strengthens the company's fire life-safety portfolio, particularly for data centers, energy storage, and EV infrastructure. The acquisition enhances the company's position in advanced fire detection and battery fire prevention systems

-

In January 2023, Siemens launched Fire Safety Digital Services. Fire safety systems are connected to the cloud by a first-in-market portfolio of digital and managed services, enabling organizations to switch from a reactive, compliance-driven approach to total protection through intelligent safety. Additionally, the prominent players are entering into strategic partnerships in the market to expand their customer base and enhance their product offerings in the market. These factors are expected to boost the growth of the market.

Fire Protection System Market Report Scope

Report Attribute

Details

Market size in 2025

USD 94.9 billion

Estimated market size in 2026

USD 101.2 billion

Projected market size by 2033

USD 156.2 billion

Growth rate

CAGR of 6.4% from 2026 to 2033

Base year for estimation

2025

Actual data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company market share, competitive landscape, growth factors, and trends

Segments covered

Component, application, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; India; Japan; South Korea; Australia; Brazil; Kingdom of Saudi Arabia (KSA); UAE; South Africa

Key companies profiled

Johnson Controls; Honeywell International, Inc.; Raytheon Technologies Corporation; GENTEX CORPORATION; Siemens; Robert Bosch GmbH; Halma plc; Eaton; Iteris, Inc.; Hitachi Ltd.

Customization scope

Free report customization (equivalent to up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Fire Protection System Market Report Segmentation

The report forecasts revenue growth at the global, regional & country levels and provides an analysis of the latest trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the fire protection system market report based on component, application, and region:

-

Component Outlook (Revenue, USD Million/Billion, 2021 - 2033)

-

Product

-

Fire Detection

-

Fire Suppression

-

Fire Response

-

Fire Analysis

-

Fire Sprinkler System

-

-

Services

-

Managed Service

-

Installation and Design Service

-

Maintenance Service

-

Others

-

-

-

Application Outlook (Revenue, USD Million/Billion, 2021 - 2033)

-

Commercial

-

Industrial

-

Residential

-

-

Regional Outlook (Revenue, USD Million/Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

Australia

-

South Korea

-

-

Latin America

-

Brazil

-

-

Middle East & Africa (MEA)

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Research Methodology

Segment Definition

Segment- Component

Revenue Capture Definition

Products

This segment includes revenue generated from the sale of physical fire protection equipment and systems designed to detect, suppress, monitor, and respond to fire incidents. It encompasses hardware components, including fire alarms, smoke detectors, fire suppression systems, sprinkler systems, control panels, emergency communication devices, and fire monitoring solutions, deployed across residential, commercial, and industrial facilities.

Services

This segment includes revenue generated from professional and managed services associated with fire protection systems, including system design, engineering, installation, testing, inspection, monitoring, maintenance, repair, upgrades, and compliance-related support services throughout the system lifecycle.

Segment- Product

Revenue Capture Definition

Fire Detection

This segment includes fire detection solutions designed to identify the presence of smoke, heat, flames, or combustible gases and provide early warning of fire incidents. Revenue is generated from products such as smoke detectors, heat detectors, flame detectors, fire alarm panels, sensors, and associated monitoring devices.

Fire Suppression

This segment includes systems and equipment designed to control, contain, or extinguish fires automatically or manually. Revenue is generated from fire extinguishers, gaseous suppression systems, foam suppression systems, water mist systems, chemical suppression systems, and related control equipment.

Fire Response

This segment includes products that facilitate emergency response and occupant safety during fire incidents. Revenue is generated from emergency communication systems, voice evacuation systems, public address systems, firefighter communication equipment, emergency lighting, and incident management solutions.

Fire Analysis

This segment includes technologies used for fire monitoring, analytics, risk assessment, and incident intelligence. Revenue is generated from fire monitoring software, analytics platforms, cloud-based fire management systems, predictive maintenance solutions, AI-enabled fire risk assessment tools, and integrated fire safety management applications.

Fire Sprinkler System

This segment includes automatic sprinkler systems designed to detect and suppress fires through water discharge mechanisms. Revenue is generated from sprinkler heads, piping networks, valves, pumps, control assemblies, pre-action systems, deluge systems, and associated sprinkler infrastructure components.

Segment- Service

Revenue Capture Definition

Managed Services

This segment includes outsourced fire protection system management services such as remote monitoring, centralized alarm management, compliance reporting, system performance monitoring, predictive maintenance, and cloud-based fire safety management services provided under recurring service contracts.

Installation and Design Services

This segment includes consulting, engineering, system design, integration, deployment, commissioning, and project implementation services associated with the installation of fire protection systems in new and existing facilities.

Maintenance Services

This segment includes periodic inspection, testing, certification, preventive maintenance, repair, replacement, calibration, and upgrade services required to maintain system functionality, regulatory compliance, and operational readiness.

Others

This segment includes additional professional services such as fire risk assessments, fire safety audits, employee training, emergency preparedness consulting, code compliance advisory services, and retrofit project support.

Estimation Model

Layer Name

Key Question

Description

Building & Infrastructure Base Layer

What creates demand for fire protection systems?

Global installed base and annual construction of commercial buildings, industrial facilities, manufacturing plants, data centers, healthcare facilities, educational institutions, residential buildings, transportation infrastructure, energy facilities, warehouses, and other structures requiring fire safety compliance and protection.

Fire Safety Equipment Layer

How many fire protection systems can be deployed?

Assessment of fire protection equipment requirements across buildings and facilities, including fire detection systems, fire suppression systems, sprinkler systems, fire alarms, extinguishers, hydrants, emergency communication systems, and specialized fire protection solutions. Evaluation based on building size, occupancy levels, fire risk classification, asset value, and regulatory requirements.

Fire Safety Compliance & Adoption Intensity Layer

How rapidly are fire protection systems being adopted?

Adoption is driven by stringent fire safety regulations, building codes, insurance requirements, industrial safety standards, urbanization, infrastructure development, increasing awareness of fire risks, asset protection needs, and modernization of existing fire safety systems. Includes retrofitting activities and investments in smart fire protection technologies.

Revenue Layer

How is revenue captured?

Revenue is generated from the sale, installation, integration, inspection, testing, monitoring, and maintenance of fire protection systems across product types, technologies, applications, and end-user industries. Includes revenues from fire detection equipment, fire suppression systems, sprinkler networks, fire alarm systems, software platforms, monitoring services, maintenance contracts, and recurring inspection and compliance services.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Fire Protection System Market Opportunity Assessment

Country/region-wise fire protection system market sizing and growth forecasts across North America, Europe, Asia Pacific, and the Rest of the World.

Assessment of fire safety regulations, building codes, industrial safety standards, and compliance requirements influencing fire protection system deployment across key markets.

Identified region-specific growth opportunities driven by infrastructure development, industrial expansion, urbanization, and increasing fire safety compliance requirements.

Supported market expansion strategies, product portfolio planning, and investment prioritization.

Competitive Benchmarking and Strategic Positioning in the Fire Protection System Market

Benchmarking of leading vendors across pricing strategies, product portfolios, managed services, installation capabilities, maintenance offerings, and digital fire safety technologies.

Comparative assessment of market share, operational capabilities, and growth strategies.

Identified market gaps across integrated building safety systems, predictive maintenance solutions, wireless fire protection technologies, and lifecycle service offerings.

Supported strategic expansion, mergers & acquisitions planning, and ecosystem partnership development.

Application-Level Growth Opportunity Assessment

Detailed assessment of fire protection system adoption across commercial, industrial, and residential applications.

Analysis of demand trends across data centers, healthcare facilities, manufacturing plants, warehouses, transportation infrastructure, and smart buildings.

Identified high-growth application segments and emerging investment opportunities.

Supported customer targeting strategies, vertical expansion planning, and resource allocation decisions.

Frequently Asked Questions About This Report

The global fire protection system market size was estimated at USD 94.9 billion in 2025 and is expected to reach USD 101.2 billion in 2026.

The global fire protection system market is expected to grow at a compound annual growth rate of 6.4% from 2026 to 2033 to reach USD 156.2 billion by 2033.

Some key players operating in the fire protection system market include Johnson Controls; Honeywell International, Inc.; GENTEX CORPORATION; Siemens; Robert Bosch GmbH; Halmaplc; Eaton; and Raytheon Technologies Corporation.

Key factors that are driving the fire protection system market growth include growth in the adoption of wireless technology in fire detection systems and the development of the construction industry across the world.

North America dominated the fire protection system market with a share of over 34.9% in 2025. This is attributable to the implementation of stringent fire safety regulations and norms and rapid infrastructural developments.

Fire detection systems segment dominated the fire protection system market with a share of over 58.1% in 2025.

Commercial segment dominated the fire protection system market with a share of over 46.4% in 2025.

The Asia Pacific region witnessed for high CAGR in the global fire protection system market. This is due to Rapid urbanization, strict government safety mandates, and massive commercial construction expansions across developing nations.

The UK witnessed for high CAGR in the Europe fire protection system market. This is due to strict regulatory mandates, a surge in high-density urban developments, and localized infrastructure investments across major commercial and healthcare hubs.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.