- Home

- »

- Paints, Coatings & Printing Inks

- »

-

Flexographic Ink Market Size & Share Report, 2025-2033GVR Report cover

![Flexographic Ink Market (2025 - 2033)Report]()

Flexographic Ink Market (2025 - 2033)

Size, Share & Trends Analysis Report Resin Type (Polyurethanes, Acrylics, Polyamides, Nitrocellulose), By Application (Flexible Packaging, Corrugated Cardboard), By Technology (Water-based Inks, UV-curable Inks), By Region, And Segment Forecasts

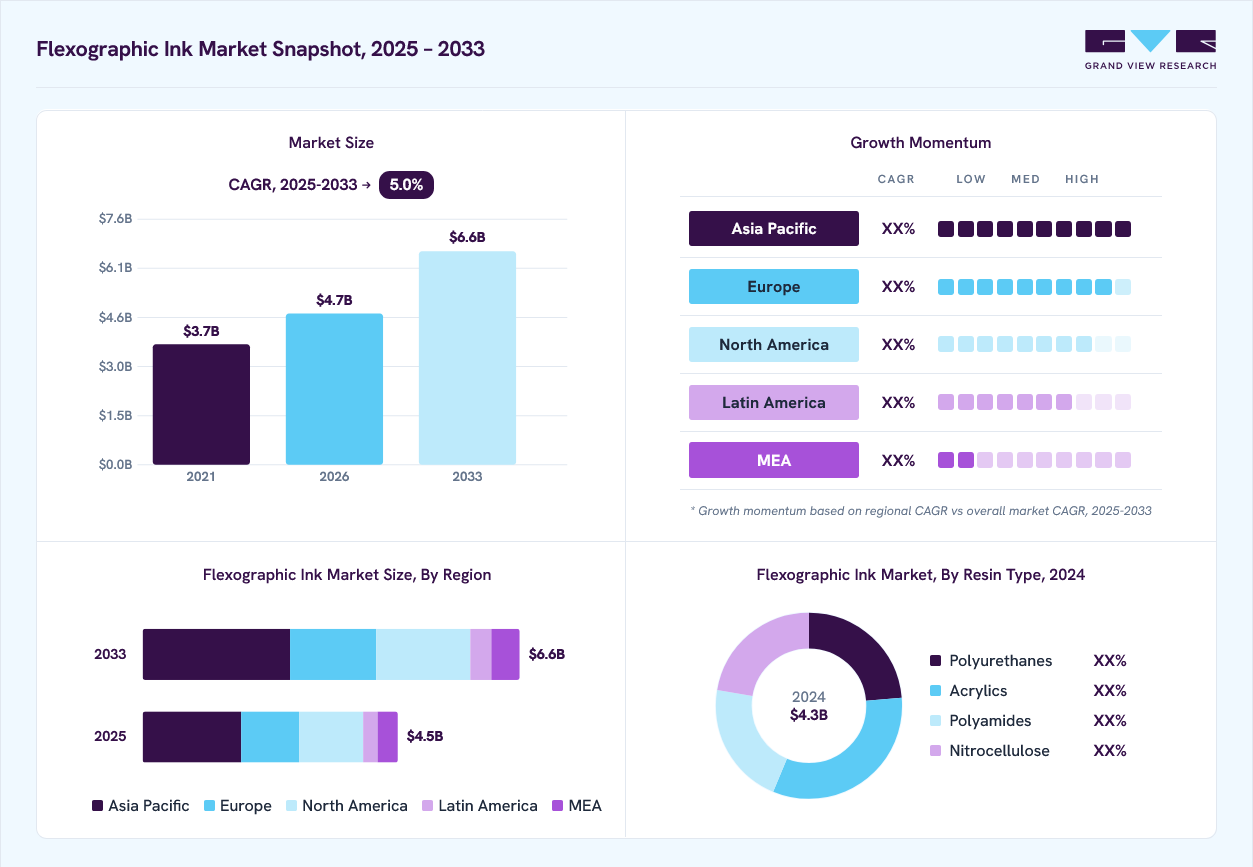

Market Size, 2024

$4.3BMarket Estimate, 2026

$4.7BMarket Forecast, 2033

$6.6BCAGR, 2025–2033

5.0%Flexographic Ink Market Summary

The global flexographic ink market size was valued at USD 4.3 billion in 2024 and is projected to grow from USD 4.7 billion in 2026 to USD 6.6 billion by 2033, at a CAGR of 5.0% from 2025 to 2033. Asia Pacific dominated the market, accounting for a revenue share of 38.7% in 2024. The market is primarily driven by the rapid growth of the packaging industry, fueled by rising e-commerce activities, FMCG expansion, and increasing demand for food and beverage packaging.

Key Market Trends & Insights

- The flexographic ink market in China accounted for 36.1% of the Asia Pacific market in 2024.

- By resin type, the acrylics segment dominated the market with the largest revenue share of 32.6% in 2024.

- By technology, the water-based inks held the largest revenue share of 51.8% in 2024 in terms of value.

- By application, the flexible packaging segment held the largest revenue share of 41.7% in 2024 in terms of value.

Market Size & Forecast

- 2024 Market Size: USD 4.3 Billion

- 2033 Projected Market Size: USD 6.6 Billion

- CAGR (2025-2033): 5.0%

- Asia Pacific: Largest market in 2024

Stringent environmental regulations also encourage the adoption of eco-friendly water-based and UV-curable inks, while advancements in flexographic printing technologies enable high-quality, cost-effective, and fast-drying ink solutions, further boosting market growth. Significant opportunities exist to develop sustainable and bio-based inks that cater to the growing consumer preference for environmentally responsible packaging. Emerging markets in Asia, particularly India and Southeast Asia, present high growth potential due to expanding industrial and retail sectors. The integration of digital and hybrid printing technologies with flexographic systems offers avenues for enhanced efficiency, customization, and premium packaging solutions.")

The market faces challenges from the environmental and regulatory pressures on solvent-based inks due to VOC emissions, coupled with the high costs associated with UV-curable ink systems and equipment. Variability in raw material prices, compatibility issues with certain substrates, and the need for skilled labor for advanced printing technologies further constrain market expansion, particularly in developing regions.

Market Concentration & Characteristics

The market is fairly consolidated with several global players such as Sun Chemical, Flint Group, Siegwerk, Toyo Ink, INX, and ALTANA, commanding scale through broad product portfolios, global manufacturing footprints and deep customer relationships, while a second tier of specialized regional players such as Qinghe Chemical, Apex International, T&K TOKA and others compete on price, local service and niche formulations. These lead firms differentiate on technology (water-based, UV/EB, low-migration food-grade systems), formulation expertise (pigments, dispersions, additives), and compliance capabilities (food-contact safety, EuPIA/GMP), which lets them supply converters and brand owners across flexible packaging, labels, corrugated, and folding cartons.

Competition is being reshaped by two strategic forces: sustainability and product innovation. Companies such as Siegwerk and Sun Chemical are investing heavily in circular-economy solutions, NC-free toolboxes, and bio-based/low-migration chemistries to meet recyclability and regulatory demands, while Flint Group and others push energy-curable and electron-beam offerings for productivity and VOC reduction - moves that raise technical entry barriers for smaller players. At the same time, consolidation, backward integration by pigment/dispersions suppliers, volatile raw-material costs, and the need for regional supply continuity are driving M&A, localized manufacturing investments, and expanded technical service offerings (pressroom optimization, color management) as key competitive levers. These dynamics favor incumbents with R&D, regulatory, and distribution scale while creating niche opportunities for agile regional specialists.

Resin Type Insights

The acrylics segment dominated the market with the largest revenue share of 32.6% in 2024, due to its superior performance, cost-effectiveness, and versatility across diverse packaging applications. Acrylic-based inks offer excellent adhesion, gloss, and color strength on both porous and non-porous substrates, making them the preferred choice for high-volume packaging formats such as flexible packaging, corrugated cardboard, and folding cartons. Their low VOC emissions and compatibility with water-based systems also align with the industry’s shift toward eco-friendly printing solutions, particularly in regulated markets like North America and Europe. Furthermore, the balance of durability and print quality provided by acrylic resins makes them highly attractive for brand owners seeking premium, sustainable packaging solutions without compromising production efficiency.

Alongside acrylics, other resin types play important roles in shaping the market. Polyurethane resins are gaining traction due to their superior chemical resistance, flexibility, and suitability for high-performance packaging, particularly in applications requiring scratch resistance and durability, such as labels and industrial packaging. Polyamides are widely used in solvent-based flexographic inks, offering fast-drying properties, strong adhesion, and resistance to grease and chemicals, which makes them popular in food packaging applications. Nitrocellulose resins, long established in the industry, remain favored for their quick-drying nature and balanced performance; however, their market share is gradually declining as sustainability pressures drive innovation in water-based and polyurethane systems. The evolving resin landscape reflects a broader market transition toward environmentally responsible, high-performance solutions tailored to the changing demands of the global packaging sector.

Application Insights

The flexible packaging segment dominated the market with the largest revenue share of 41.7% in 2024, driven by surging demand from the food, beverage, personal care, and pharmaceutical industries. Flexible packaging offers lightweight, cost-efficient, and versatile solutions that align with evolving consumer preferences for convenience, portability, and extended shelf life. Flexographic inks, particularly water-based and UV-curable formulations, are well-suited for printing on plastic films, pouches, and laminates due to their strong adhesion, vibrant color quality, and compliance with food safety regulations. The rapid expansion of e-commerce further reinforced demand, as brands increasingly adopted flexible packaging formats to optimize shipping efficiency and enhance product presentation. In addition, sustainability initiatives, such as the push for recyclable and mono-material packaging, continue to support the dominance of this segment by encouraging the adoption of inks compatible with eco-friendly substrates.

Beyond flexible packaging, other application segments contribute significantly to market growth. Corrugated cardboard is experiencing strong momentum, driven by the rise of online retail and logistics, where sturdy and print-enhanced cartons are essential for both product protection and branding. Labels & tags represent a high-value niche segment, supported by rising demand in consumer goods, healthcare, and cosmetics, where product differentiation and regulatory compliance require high-quality, durable printing inks. Folding cartons, while more traditional, remain critical in premium packaging for confectionery, personal care, and pharmaceuticals, where aesthetic appeal and durability are vital. Together, these applications illustrate the pivotal role of flexographic inks in enabling high-quality, cost-efficient, and sustainable packaging solutions across diverse end-use industries, with flexible packaging setting the growth trajectory for the sector.

Technology Insights

The water-based inks segment captured the largest revenue share of 51.8% in 2024 due to rising regulatory pressures, sustainability goals, and growing consumer demand for environmentally friendly packaging solutions. Water-based flexographic inks emit significantly lower volatile organic compounds (VOCs) levels than solvent-based alternatives, making them highly attractive for converters and brand owners seeking compliance with stringent environmental standards in North America and Europe. Their compatibility with a wide range of substrates used in food, beverage, and personal care packaging also positions them as the preferred choice in applications where safety and low migration are critical. In addition, advancements in formulation technologies have improved their drying times, printability, and adhesion, helping water-based inks close the performance gap with solvent-based systems and further solidify their market dominance.

While water-based inks lead the market, solvent-based and UV-curable inks continue to serve important roles. Solvent-based inks remain relevant in applications demanding superior adhesion and durability on non-porous substrates such as films, foils, and laminates, particularly in emerging markets where regulatory restrictions are less stringent. However, their growth is constrained by VOC-related challenges and rising compliance costs. On the other hand, UV-curable inks are gaining momentum as a high-performance alternative, offering instant curing, energy efficiency, and superior resistance properties. Their faster delivery of vibrant, high-quality prints makes them increasingly attractive for premium labels and flexible packaging. Together, these technology segments highlight the industry’s dual focus on balancing sustainability with performance, with water-based inks driving mainstream adoption while UV-curable technologies gain traction as the future growth engine.

Regional Insights

Asia Pacific dominated the flexographic ink market with the largest revenue share of 38.7% in 2024, underpinned by the rapid expansion of packaging, retail, and e-commerce industries across China, India, Japan, and Southeast Asia. Strong growth in flexible packaging for food, beverages, and pharmaceuticals, combined with increasing investments in modern printing technologies, positions APAC as the leading hub for demand. Moreover, favorable demographics, rising disposable incomes, and the shift toward sustainable packaging solutions are expected to accelerate further the region's adoption of water-based and UV-curable inks.

China Flexographic Ink Market Trends

The flexographic ink market in China accounted for 36.1% of the Asia Pacific market in 2024, supported by its vast packaging ecosystem and strong manufacturing base. The country’s leadership in e-commerce and FMCG sectors and rapidly growing pharmaceutical and personal care industries have created a robust demand for high-quality and sustainable flexographic printing inks. Government initiatives promoting green packaging and the large-scale transition from solvent-based to water-based systems also drive growth, solidifying China’s role as the single largest market within APAC.

North America Flexographic Ink Market Trends

The flexographic ink market in North America captured 25.1% of the global market in 2024, led by strong demand for premium packaging solutions across the food & beverage, pharmaceutical, and e-commerce sectors. The region’s well-established printing infrastructure and regulatory pressures to reduce VOC emissions have accelerated the shift toward water-based and energy-curable ink systems. Furthermore, technological innovations and the integration of hybrid printing solutions support consistent growth, particularly in the U.S. market, which remains the largest contributor.

The U.S. flexographic ink market commanded 78.2% of the North American market in 2024, reflecting its mature packaging sector, strong consumer goods demand, and leadership in sustainable printing adoption. The rise of e-commerce logistics and food packaging applications has reinforced the dominance of water-based inks. UV-curable technologies are gaining traction in premium labels and flexible packaging. In addition, the country’s stringent environmental regulations and innovation-driven ink manufacturers are fostering continued market growth and technological leadership.

Europe Flexographic Ink Market Trends

The flexographic ink market in Europe held 22.7% of the global market in 2024, supported by stringent environmental policies and the region’s emphasis on sustainable packaging solutions. Countries such as Germany, Italy, and the UK are at the forefront of adopting water-based and low-migration inks, especially in food and pharmaceutical packaging. The region’s advanced printing infrastructure and high consumer demand for recyclable and premium packaging formats position Europe as a critical market for eco-friendly flexographic ink innovation.

Germany flexographic ink market remains one of the most influential markets in Europe, underpinned by its highly advanced packaging and printing sectors. The country’s leadership in engineering, innovation, and sustainable manufacturing practices has fostered significant water-based and UV-curable inks adoption. Strong demand from food, beverage, and industrial packaging applications, along with regulatory pressure to reduce carbon footprints, continues to make Germany a strategic hub for ink manufacturers expanding their eco-friendly product portfolios in the European market.

Middle East & Africa Flexographic Ink Market Trends

The flexographic ink market in the Middle East & Africa is developing but presents strong growth potential, fueled by urbanization, expanding retail networks, and the rising demand for packaged food and beverages. Countries such as the UAE, Saudi Arabia, and South Africa are seeing increased investments in modern packaging technologies, while sustainability initiatives are slowly influencing a shift toward water-based ink systems. Despite its smaller market share, MEA is emerging as a strategic growth frontier for global ink manufacturers seeking to tap into underpenetrated markets.

Latin America Flexographic Ink Market Trends

The flexographic ink market in Latin America is steadily expanding, supported by the growth of consumer goods, beverages, and agricultural packaging industries, particularly in Brazil and Mexico. The region is gradually transitioning from solvent-based inks to water-based systems, driven by regulatory changes and increasing sustainability awareness. However, cost sensitivity and economic volatility continue to shape buying behavior, making affordability and adaptability critical for ink suppliers. Despite these challenges, rising investments in packaging infrastructure and growing exports are expected to fuel long-term growth.

Key Flexographic Ink Company Insights

Key players, such as DIC CORPORATION, Qinghe Chemical, Apex International, Flint Group, Sun Chemical, and Siegwerk Druckfarben AG & Co. KGaA, dominate the market.

-

DIC Corporation, headquartered in Tokyo, Japan, is a global leader in printing inks, including flexographic inks, with a strong footprint across Asia Pacific, North America, and Europe. The company has established itself as a key innovator in sustainable ink formulations, particularly in water-based and UV-curable technologies, aligning with growing demand for eco-friendly packaging solutions. Leveraging its extensive R&D capabilities and diversified product portfolio, DIC serves a wide range of end-use industries such as flexible packaging, labels, and corrugated applications. Its strategic focus on acquisitions, partnerships, and regional expansions has strengthened its position in the global market, while its commitment to low-VOC and bio-based ink systems continues to enhance its competitive edge in an increasingly sustainability-driven industry.

Key Flexographic Ink Companies:

The following are the leading companies in the flexographic ink market. These companies collectively hold the largest market share and dictate industry trends.

- DIC CORPORATION

- Qinghe Chemical

- Apex International

- Flint Group

- Sun Chemical

- Siegwerk Druckfarben AG & Co. KGaA

- INX International Ink Co.

- Toyo Ink

- T&K TOKA Corporation

- ALTANA

Global Flexographic Ink Market Report Scope

Report Attribute

Details

Market size in 2024

USD 4.3 billion

Estimated market size in 2026

USD 4.7 billion

Projected market size by 2033

USD 6.6 billion

Growth rate

CAGR of 5.0% from 2025 to 2033

Base year for estimation

2024

Historical data

2018 - 2023

Forecast period

2025 - 2033

Quantitative units

Volume in kilotons, revenue in USD million/billion, and CAGR from 2025 to 2033

Report coverage

Volume & revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Resin type, application, region

Regional scope

North America; Europe; Asia Pacific; Middle East & Africa; Latin America

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; China; India; Japan; South Korea; Brazil; Argentina; South Africa; Saudi Arabia

Key companies profiled

DIC CORPORATION; Qinghe Chemical; Apex International; Flint Group; Sun Chemical; Siegwerk Druckfarben AG & Co. KGaA; INX International Ink Co.; Toyo Ink; T&K TOKA Corporation; ALTANA

Customization scope

Free report customization (equivalent up to 8 analysts’ working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Flexographic Ink Market Report Segmentation

This report forecasts volume & revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2018 to 2033. For this study, Grand View Research has segmented the global flexographic ink market report based on material, application, and region:

-

Resin Type Outlook (Volume, Kilotons, Revenue, USD Million, 2018 - 2033)

-

Polyurethanes

-

Acrylics

-

Polyamides

-

Nitrocellulose

-

-

Technology Outlook (Volume, Kilotons, Revenue, USD Million, 2018 - 2033)

-

Water-based inks

-

Solvent-based inks

-

UV-curable inks

-

-

Application Outlook (Volume, Kilotons, Revenue, USD Million, 2018 - 2033)

-

Flexible Packaging

-

Corrugated Cardboard

-

Labels & Tags

-

Folding Cartons

-

-

Regional Outlook (Volume, Kilotons, Revenue, USD Million, 2018 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

South Africa

-

-

Frequently Asked Questions About This Report

The global flexographic ink market size was valued at USD 4.3 billion in 2024 and is estimated at USD 4.7 billion for 2026.

The global flexographic ink market is expected to grow at a CAGR of 5.0% from 2025 to 2030, reaching USD 6.6 billion by 2030.

The water-based inks segment dominated the flexographic inks market with a 51.8% share in 2024 primarily due to its eco-friendly profile, regulatory compliance, and strong adoption across food and beverage packaging. Growing restrictions on volatile organic compounds (VOCs) and rising consumer demand for sustainable packaging solutions have accelerated the shift from solvent-based to water-based systems.

Some of the key players operating in the flexographic ink market include DIC CORPORATION, Qinghe Chemical, Apex International, Flint Group, Sun Chemical, Siegwerk Druckfarben AG & Co. KGaA, INX International Ink Co., Toyo Ink, T&K TOKA Corporation, and ALTANA

The flexographic inks market is driven by rising demand for sustainable and low-VOC printing solutions, coupled with the rapid growth of flexible packaging in food, beverage, and consumer goods sectors. The advancements in ink technologies and increasing regulatory pressure to adopt eco-friendly alternatives are fueling market expansion.

About the Author(s)

Paints, Coatings & Printing Inks Research Team

Bulk Chemicals · Paints, Coatings & Printing InksThis report was authored by the paints, coatings & printing inks research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the paints, coatings & printing inks segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.