- Home

- »

- Biotechnology

- »

-

Gene Vector Market Size & Share, Industry Report, 2033GVR Report cover

![Gene Vector Market Size, Share & Trends Report]()

Gene Vector Market (2025 - 2033) Size, Share & Trends Analysis Report By Type (Viral, Non-Viral), By Delivery Method, By Therapeutic Area, By End Use, By Region, And Segment Forecasts

- Report Summary

- Table of Contents

- Segmentation

- Methodology

- Download FREE Sample

-

Download Sample Report

Download Sample Report

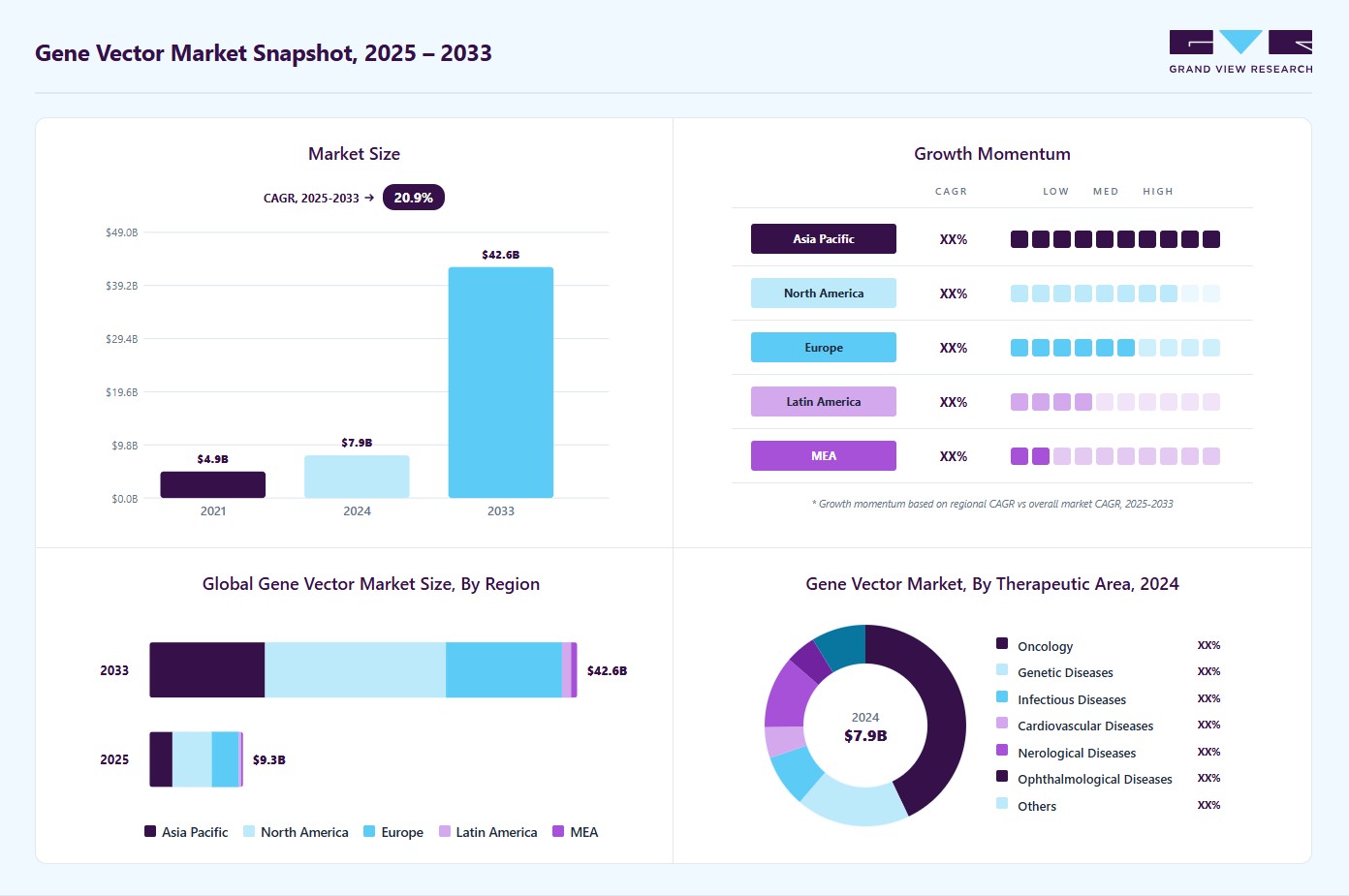

Market Size, 2024

$7.9BMarket Estimate, 2025

$9.3BMarket Forecast, 2033

$42.6BCAGR, 2025–2033

20.9%Gene Vector Market Summary

The global gene vector market size was estimated at USD 7.88 billion in 2024 and is projected to reach USD 42.61 billion by 2033, growing at a CAGR of 20.92% from 2025 to 2033. The main growth drivers are the increasing prevalence of genetic disorders, advancements in gene therapy, and a boom in research and development efforts to create innovative gene delivery systems. The market is expected to grow significantly in several important global regions as the need for targeted therapies and personalized medicine keeps growing.

Key Market Trends & Insights

- The North America gene vector market held the largest global revenue share of 41.91% in 2024.

- The gene vector industry in the U.S. is expected to grow significantly from 2025 to 2033.

- By therapeutic area, the oncology segment held the highest market share of 42.94% in 2024.

- By delivery method, the in-vivo gene delivery segment held the highest market share in 2024.

- By end use, the pharmaceutical & biotechnology companies segment held the highest market share in 2024.

Market Size & Forecast

- 2024 Market Size: USD 7.88 Billion

- 2033 Projected Market Size: USD 42.61 Billion

- CAGR (2025-2033): 20.92%

- North America: Largest Market in 2024

- Asia Pacific: Fastest Growing Market

")

Advancements in Viral and Non-viral Vectors

The global gene vector industry is seeing significant growth due to advancements in viral and non-viral vector technology. Adeno-associated viruses (AAV), lentiviruses, and retroviruses are viral vectors whose safety profiles, transduction efficiency, and tissue-specific targeting have all been greatly enhanced by ongoing innovation. For example, next-generation AAVs are being developed with improved delivery efficiency and decreased immunogenicity, making them ideal for treating inherited and chronic diseases.

Approved Gene Therapies based on Viral and Non-viral Vectors (April 2025)

Drug name

Company

Condition

Year first approved

Regulatory agency

Zynteglo

bluebird bio

Transfusion-dependent beta thalassaemia

2019/2022

EMA/FDA

Breyanzi

Celgene (Bristol Myers Squibb)

Diffuse large B-cell lymphoma; follicular lymphoma; chronic lymphocytic leukaemia; mantle cell lymphoma

2021

FDA

Abecma

bluebird bio

Multiple myeloma

2021

FDA

Carteyva (Relma-cel)

JW Therapeutics (Shanghai)

Diffuse large B-cell lymphoma; follicular lymphoma; mantle cell lymphoma

2021

NMPA

Skysona

bluebird bio

Early cerebral adrenoleukodystrophy (CALD)

2021

FDA

Carvykti

Legend Biotech

Multiple myeloma

2022

FDA

Lyfgenia

bluebird bio

Sickle cell disease

2023

FDA

Libmeldy/Lenmeldy

Orchard Therapeutics

Metachromatic leukodystrophy

2020/2024

EMA/FDA

Breyanzi

Bristol Myers Squibb

Relapsed/Refractory Chronic Lymphocytic Leukaemia

2024

FDA

Tecelra (Afami-cel)

Adaptimmune

Synovial sarcoma

2024

FDA

Adstiladrin

Merck & Co.

Bladder cancer

2022

FDA

Zolgensma

Norvartis

Spinal muscular atrophy

2019

EMA

Upstaza

PTC Therapeutics

Aromatic l-amino acid decarboxylase (AADC) deficiency

2022

EMA

Hemgenix

uniQure

Hemophilia B

2022

FDA

Elevidys

Sarepta Therapeutics

Duchenne muscular dystrophy

2023

FDA

Roctavian

BioMarin

Hemophilia A

2022

FDA

Beqvez

Pfizer

Hemophilia B

2024

FDA

BBM-H901

Belief BioMed

Hemophilia B

2025

NMPA

Vyjuvek

Krystal Biotech

Dystrophic epidermolysis bullosa

2023

FDA

Delytact

Daiichi Sankyo

Malignant glioma

2021

MHLW

Tecartus (ex vivo)

Kite Pharma (Gilead)

Metachromatic leukodystrophy

2020

FDA

Onpattro

Alnylam&Sanofi

Human transthyretin amyloidosis (hATTR)

2018

FDA

Givlaari

Alnylam

Acute hepatic porphyria (AHP)

2019

FDA

Oxlumo

Alnylam

Primary hyperoxaluria type1 (PH1)

2020

FDA

Leqvio

Novartis

Hypercholesterolaemia

2020

FDA

Amvuttra

Alnylam

hATTR

2022

FDA

Rivfloza

Novo Nordisk A/S

Primary hyperoxaluria

2023

FDA

Source: Biomedicines Secondary Research, Grand View Research

The market momentum is being strengthened by the advancements associated with non-viral vectors. Lipid nanoparticles (LNPs), carriers from polymers, and some form of physical delivery, such as electroporation, are increasingly used as alternatives to viral systems because they can be scaled up, have fewer safety concerns, and carry larger genetic payloads. LNPs, specifically, were brought to the forefront of global attention with the COVID-19 pandemic because mRNA vaccines utilized lipid nanoparticles as carriers, further demonstrating their therapeutic potential in the treatment of oncology, rare genetic diseases, and infectious diseases. The dedicated research and development to improve delivery efficiency, reduce cytotoxicity, and improve targeting accuracy of non-viral vectors are still attractive to large-scale commercial manufacturing.

Growing Demand for Personalized Medicine

The rising trend toward personalized medicine is a major growth driver for the gene vector market. Generic, one-size-fits-all treatments often fail to address the underlying cause of complex and rare diseases. This creates a demand for therapy designed for individual patients based on their genetic profile. Gene vectors will be integral to developing these personalized treatments that deliver therapeutic genes directly into targeted cells to help treat the molecular basis of disease, rather than simply addressing symptoms. As advancements in genomic sequencing and biomarker discovery accelerate, healthcare providers are better equipped to design therapies specific to a patient’s genetic makeup, which, in turn, is increasing reliance on viral and non-viral vectors as essential tools in this transformation.

Growing investments in precision medicine initiatives across the globe further underscore this trend. Governments, research institutes, and pharmaceutical companies are focusing on personalized treatment models. They aim to improve patient outcomes, reduce side effects, and make healthcare more cost-effective. Gene and cell therapies, many of which are vector-based, are at the forefront of this movement, with increasing approvals of treatments for cancers, rare genetic disorders, and inherited conditions.

Market Concentration & Characteristics

The gene vector industry shows strong innovation. This is driven by quick progress in both viral and non-viral delivery technologies. Next-generation AAVs, lentiviral, and retroviral vectors are made for better targeting efficiency, reduced immunogenicity, and a broader range of therapeutic uses. At the same time, non-viral platforms like lipid nanoparticles (LNPs) are becoming more popular after their success with mRNA vaccine delivery. Furthermore, using AI-driven design, CRISPR-based editing, and improved vector manufacturing platforms is changing development processes. With strong R&D investments and over 2,000 active clinical trials worldwide, the market’s innovation landscape shapes competition. This speeds up the use of gene therapies in oncology, rare diseases, and regenerative medicine.

The gene vector market is experiencing moderate to high mergers and acquisitions (M&A) activity. This is mainly due to the need for pharmaceutical and biotechnology companies to build their gene therapy pipelines and improve their manufacturing capabilities. Large companies are buying specialized vector manufacturers and technology providers to secure their supply chains, enhance their knowledge in viral and non-viral delivery platforms, and speed up clinical development timelines. For instance, in May 2024, MilliporeSigma (U.S./Canada) announced a USD 600M agreement to acquire Wisconsin-based Mirus Bio, strengthening its viral vector manufacturing portfolio with leading transfection reagents for gene therapy.

Regulations are important in shaping the market for gene vectors. Strict guidelines control the development, manufacturing, and approval of vector-based therapies. Regulatory agencies like the U.S. FDA, EMA, and Japan’s PMDA enforce high standards for vector safety, effectiveness, and quality. This is especially important because of concerns about immunogenicity, long-term expression, and off-target effects. While these frameworks improve patient safety and build trust in new therapies, they pose challenges for developers. These challenges include long approval timelines, high compliance costs, and complicated clinical trial requirements. At the same time, regulators use adaptive pathways like fast-track designations, orphan drug status, and accelerated approvals to support innovation in gene and cell therapies.

Product expansion is a major growth driver for the gene vector industry. Companies constantly diversify their portfolios to meet a wider range of therapeutic areas and patient needs. Manufacturers are working on next-generation viral vectors with better targeting, less immunogenicity, and increased payload capacity. By broadening product offerings and improving delivery capabilities, companies are solidifying their market presence and generating new revenue streams in the fast-changing gene therapy field.

Regional expansion plays a major role in the market growth. Companies are increasingly focusing on emerging markets in Asia-Pacific, Latin America, the Middle East, and established markets in North America and Europe. The rising number of genetic disorders, improved healthcare infrastructure, and supportive government programs in these areas promote the setup of local production facilities, research centers, and partnerships. Expanding into new regions helps companies reach untapped patient populations, cut manufacturing and distribution costs, and strengthen their global presence. This regional diversification speeds up market entry and improves resilience against regulatory and economic changes in individual markets.

Type Insights

In 2024, the viral vectors segment held the highest share of the gene vector market. This resulted from their established efficacy for genetic material delivery, characterized by high transduction rates, stable gene expression, and being well-suited for various therapeutics. Their key role in cell and gene therapies, including CAR-T, vaccination, and rare disease therapies, results in strong uptake. New developments in an adeno-associated virus (AAV) and lentiviral platforms and increased investment in scalable manufacturing further enhance the role of viral vectors as the backbone of the market.

The non-viral vectors segment is expected to grow at the fastest CAGR over the forecast period, driven by their favorable safety profile, lower immunogenicity, and cost-effectiveness compared to viral systems. Increasing advancements in lipid nanoparticles, polymer-mediated carriers, and physical delivery methods have led to improved transfection efficiencies and greater ease of scale-up, increasing their appeal for various applications, including mRNA vaccines, gene editing, and regenerative medicine. Furthermore, the ability of non-viral platforms to address the ability to implement repeated doses and overcome limitations of the use of viral vectors will also enhance uptake or utilization across research and therapeutic pipelines.

Delivery Method Insights

The in-vivo gene delivery segment dominated the gene vector industry with a share of 58.17% in 2024, because it directly delivers therapeutic genes into target tissues, ensuring accuracy, localization, and permanence of actions. This strategy simplifies ex vivo manipulation, shortens treatment times, and improves patient compliance. The competitive demand for delivery systems to develop sophisticated gene therapies for rare genetic disorders, oncology, and neurology, along with continuous use of viral and non-viral carriers targeted for systemic and targeted tissue delivery systems, will further enhance the leadership of in-vivo delivery systems.

The ex vivo gene delivery segment is expected to grow at the fastest CAGR during the forecast period, due to its expanding use in personalized cell and gene therapies, especially CAR-T and other immune cell-based treatments. The ex vivo technique provides more precise control over gene integration, improved safety, and enhanced efficacy by modifying the patient's cells outside the body. The increasing investments in infrastructure for cell therapy manufacturing, coupled with advancements in gene editing technologies such as CRISPR and TALEN, further drive the adoption of ex vivo gene delivery.

Therapeutic Area Insights

The oncology segment dominated the gene vector market with a share of 42.94% in 2024, driven by the growing adoption of gene therapies and targeted treatments for various cancers. The demand is driven by a fast-increasing incidence of hematologic malignancies and solid tumors, and the ability of CAR-T therapies and other genetically engineered immune cells to treat these cancers successfully. Further, the segment’s position is complemented by clinical advancements, regulatory approvals, and increased investment in oncology research and development.

The neurological disease segment is expected to grow at the fastest CAGR during the forecast period, due to rising demand for innovative gene therapies for treating disorders including Parkinson's disease, Alzheimer's disease, spinal muscular atrophy, and other inherited neurological diseases. Significant improvements have been made with viral and non-viral delivery systems that can cross the blood-brain barrier, and an overall increase in investment in more neurogenetic research and clinical trials has influenced the adoption of technology. The limited effectiveness of traditional therapies for neurological disorders is also accelerating the transition to gene-based therapies, which will contribute to significant growth in this market.

End Use Insights

The pharmaceutical and biotechnology companies segment dominated the gene vector industry in 2024, with a revenue share of 58.06%. The increase in investment in gene vector therapeutics companies compared to other therapeutic modalities, along with partnerships and collaborations in the market, in the search for new therapeutics for oncology, rare genetic disorders, and neurological disorders, has enhanced the market position of pharmaceutical and biotechnology companies.

The CROs & CMOs segment is projected to grow at the fastest CAGR during the forecast period. This growth is driven by the increasing outsourcing of gene therapy development and manufacturing to specialized service providers. Rising demand for cost-effective, scalable, and flexible production solutions, coupled with the growing complexity of gene vector platforms, encourages pharmaceutical and biotechnology companies to collaborate with CROs and CMOs.

Regional Insights

North America dominated the gene vector market with a share of 41.91% in 2024. This growth is derived from a strong healthcare system, significant research and development investment, and the presence of top biopharmaceutical companies. The region's established supply chains and emphasis on precision medicine have sped up the use of automation technologies in gene vector production.

U.S. Gene Vector Market Trends

The U.S. remains the global leader in the gene vectors industry, backed by robust investments in biopharmaceutical R&D, regenerative medicine, and advanced biologics pipelines. Rapid adoption of process control systems, AI-driven monitoring, and robotics is streamlining large-scale gene therapy production. For instance, in June 2025, the U.S. FDA designated platform technology to the rAAVrh74 viral vector in Sarepta Therapeutics’ SRP-9003 gene therapy. This therapy is based in Cambridge, Massachusetts, and is designed to treat limb-girdle muscular dystrophy.

Europe Gene Vector Market Trends

Europe is witnessing steady growth in the gene vectors industry, backed by government funding and EU research programs like Horizon Europe. Leading companies like Sartorius, Merck KGaA, and Cytiva are expanding their portfolios with improved automation solutions. There is also a growing focus on biobanking, cell-based therapies, and collaborations across borders, which drives regional innovation. For instance, in July 2025, the European Commission approved Autolus Therapeutics' CAR-T therapy AUCATZYL in the EU. The lentiviral vectors for this therapy are produced at AGC Biologics' site in Milan, marking the company's 10th major regulatory approval.

The gene vector market in the UK is growing quickly, fueled by the country’s strong biomedical research system and top academic institutions. Collaborations between universities and businesses speed up the process of moving innovative gene therapies from the lab to clinical development. This mix of research strength, strategic partnerships, and manufacturing skills makes the UK an important center in the global market.

Germany’s gene vector market is growing steadily. This growth comes from its strong biotechnology ecosystem, established pharmaceutical industry, and robust research infrastructure. The country benefits from strong collaborations between universities, specialized biotech startups, and contract development and manufacturing organizations (CDMOs).

Asia Pacific Gene Vector Market Trends

The Asia Pacific gene vector industry is expected to grow at the fastest CAGR of 22.47% over the forecast period, as the region invests significantly in biotechnology research and therapy development. China, Japan, and South Korea are at the forefront of this growth. Governments are backing clinical trial approvals and infrastructure improvements. For instance, in August 2025, Vector BioMed India launched low-cost CAR-T therapy at Kailash Cancer Hospital in rural India. Their LENTIVERSE platform made cell and gene therapies available to underserved communities. New biotech startups, along with established pharmaceutical companies, are emphasizing local production and new delivery technologies. This trend is making the Asia Pacific a more competitive center for gene vector development.

The China gene vector market is becoming an important player in the region. This growth is backed by significant investments in biotechnology and research on therapies. The country is improving its capacity to produce viral vectors, particularly adeno-associated viruses (AAVs). Greater awareness and demand for treatments for genetic disorders and cancers are fueling market growth. These factors make China a vital location for gene vector development in the Asia Pacific.

The gene vector market in Japan is projected to grow over the forecast period. Japan is becoming a major center for gene vector development. This growth is supported by a strong biotech industry and effective government initiatives that promote new therapies. The country focuses on efficient manufacturing of viral and non-viral vectors, thorough research, and clinical expertise, which support the market expansion.

MEA Gene Vector Market Trends

The gene vector industry in the Middle East and Africa is gradually expanding. Countries such as the UAE, Saudi Arabia, and South Africa are investing in research centers and partnerships with global biotech firms to develop gene therapy capabilities. Collaborative programs between academic institutions and industry players foster innovation and enable the translation of gene therapies from research to clinical trials, fueling the demand for the gene vector.

The Kuwait gene vector market is gradually stepping up, leveraging initiatives to modernize its healthcare and biotechnology sectors. There are ongoing efforts to develop clinical expertise and infrastructure for gene therapy trials, especially for rare genetic diseases. Although still evolving, Kuwait’s strategic investments and policy support set the stage for the nation to become an important player in the regional market.

Key Gene Vector Company Insights

The gene vector industry has several strong competitors that leverage superior technological footholds, large-scale manufacturing capabilities, and long-term investments in innovation to uphold their market leadership positions. Market leaders, including Charles River Laboratories, VGXI, Inc., Danaher (Aldevron), Kaneka Corporation, and Lonza, maintain strong positions in the market with their background in viral and non-viral vectors, proven regulatory history, and ability to provide global support for cell and gene therapy development.

Firms such as Cell and Gene Therapy Catapult, Eurofins Genomics, Luminous BioSciences, LLC, and Akron Biotech are consistently broadening their reach through specialized vector design, analytical services, and flexible manufacturing services for the various needs of biopharmaceutical developers, research organizations, and clinical-stage companies.

The gene vector market is developing quickly through mergers and acquisitions, strategic partnerships, and advances in vector engineering and manufacturing productivity. Companies that achieve the integration of innovation and patient-focused, scalable solutions are well-positioned for the realization of long-term value in this paradigm-changing and increasingly competitive market.

Key Gene Vector Companies:

The following are the leading companies in the gene vector market. These companies collectively hold the largest market share and dictate industry trends.

- Charles River Laboratories

- VGXI, Inc.

- Danaher (Aldevron)

- Kaneka Corp.

- Catalent Inc.

- Cell and Gene Therapy Catapult

- Eurofins Genomics

- Lonza

- Luminous BioSciences, LLC

- Akron Biotech

Recent Developments

-

In September 2025, RION partnered with Lonza in the US to scale cGMP manufacturing of its platelet-derived exosome therapeutic PEP, supporting late-phase clinical supply and future commercialization.

-

In July 2025, UK-based Cellular Origins, CGT Catapult, and Resolution Therapeutics formed a consortium to develop a fully automated robotic CGT manufacturing platform, supported by a UK Smart Grant.

Gene Vector Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 9.32 billion

Revenue forecast in 2033

USD 42.61 billion

Growth rate

CAGR of 20.92% from 2025 to 2033

Base year for estimation

2024

Historical data

2021 - 2023

Forecast period

2025 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2025 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Type, delivery method, therapeutic area, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; Italy; Spain; Denmark; Sweden; Norway; India; China; Japan; Australia; South Korea; Thailand; Brazil; Argentina; Saudi Arabia; UAE; South Africa; Kuwait

Key companies profiled

Charles River Laboratories; VGXI, Inc.; Danaher (Aldevron); Kaneka Corp.; Cell and Gene Therapy Catapult; Eurofins Genomics (Eurofins Scientific); Lonza; Luminous BioSciences, LLC; Akron Biotech; Catalent, Inc.

Customization scope

Free report customization (equivalent up to 8 analyst’s working days) with purchase. Addition or alteration to country, regional & segment scope.

Global Gene Vector Market Report Segmentation

This report forecasts revenue growth and provides an analysis on the latest trends in each of the sub-segments from 2021 to 2033. For this report, Grand View Research has segmented the global gene vector market on the basis of type, delivery method, therapeutic area, end use, and region:

-

Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Viral Vectors

-

Adenoviral Vectors

-

Adeno-Associated Viral (AAV) Vectors

-

Lentiviral Vectors

-

Retroviral Vectors

-

Herpes Simplex Virus (HSV) Vectors

-

Others

-

-

Non-Viral Vectors

-

Plasmid DNA

-

Lipid Nanoparticles

-

Polymer-based Vectors

-

Others

-

-

-

Delivery Method Outlook (Revenue, USD Million, 2021 - 2033)

-

In-vivo Gene Delivery

-

Ex-vivo Gene Delivery

-

Others

-

-

Therapeutic Area Outlook (Revenue, USD Million, 2021 - 2033)

-

Oncology

-

Genetic Diseases

-

Infectious Diseases

-

Cardiovascular Diseases

-

Neurological Diseases

-

Ophthalmological Diseases

-

Others

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Pharmaceutical & Biotechnology Companies

-

Academic & Research Institutes

-

CROs & CMOs

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

Thailand

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East and Africa (MEA)

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Frequently Asked Questions About This Report

The global gene vector market size was estimated at USD 7.88 billion in 2024 and is expected to reach USD 9.32 billion in 2025.

The global gene vector market is expected to grow at a compound annual growth rate of 20.92% from 2025 to 2033 to reach USD 42.61 billion by 2033.

North America dominated the gene vector market with a share of 41.91% in 2024. This is attributable to strong healthcare infrastructure, significant R&D investments, advanced biotech companies, supportive regulatory frameworks, and high demand for personalized treatments.

Some key players operating in the gene vector market include Charles River Laboratories, VGXI, Inc., Danaher (Aldevron), Kaneka Corp., Nature Technology Cell and Gene Therapy Catapult, Eurofins Genomics, Lonza, Luminous BioSciences, LLC, Akron Biotech

The gene vector market is expanding, driven by advances in gene therapy, rising prevalence of genetic disorders, increasing research funding, and demand for targeted treatment solutions.

About the Author(s)

Biotechnology Research Team

Healthcare · BiotechnologyThis report was authored by the biotechnology research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the biotechnology segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Share this report with your colleague or friend.

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.