- Home

- »

- Communication Services

- »

-

Telecom Services Market Size, Share & Growth Report, 2033GVR Report cover

![Telecom Services Market Size, Share & Trends Report]()

Telecom Services Market (2026 - 2033) Size, Share & Trends Analysis Report By Service Type (Mobile Data Service, Fixed Internet Access Service), By Transmission (Wireline, Wireless), By End-use (Consumer/Residential, Business), By Region, And Segment Forecasts

Market Size, 2025

$2,095.7BMarket Estimate, 2026

$2,224.0BMarket Forecast, 2033

$3,584.3BCAGR, 2026–2033

7.1%Telecom Services Market Summary

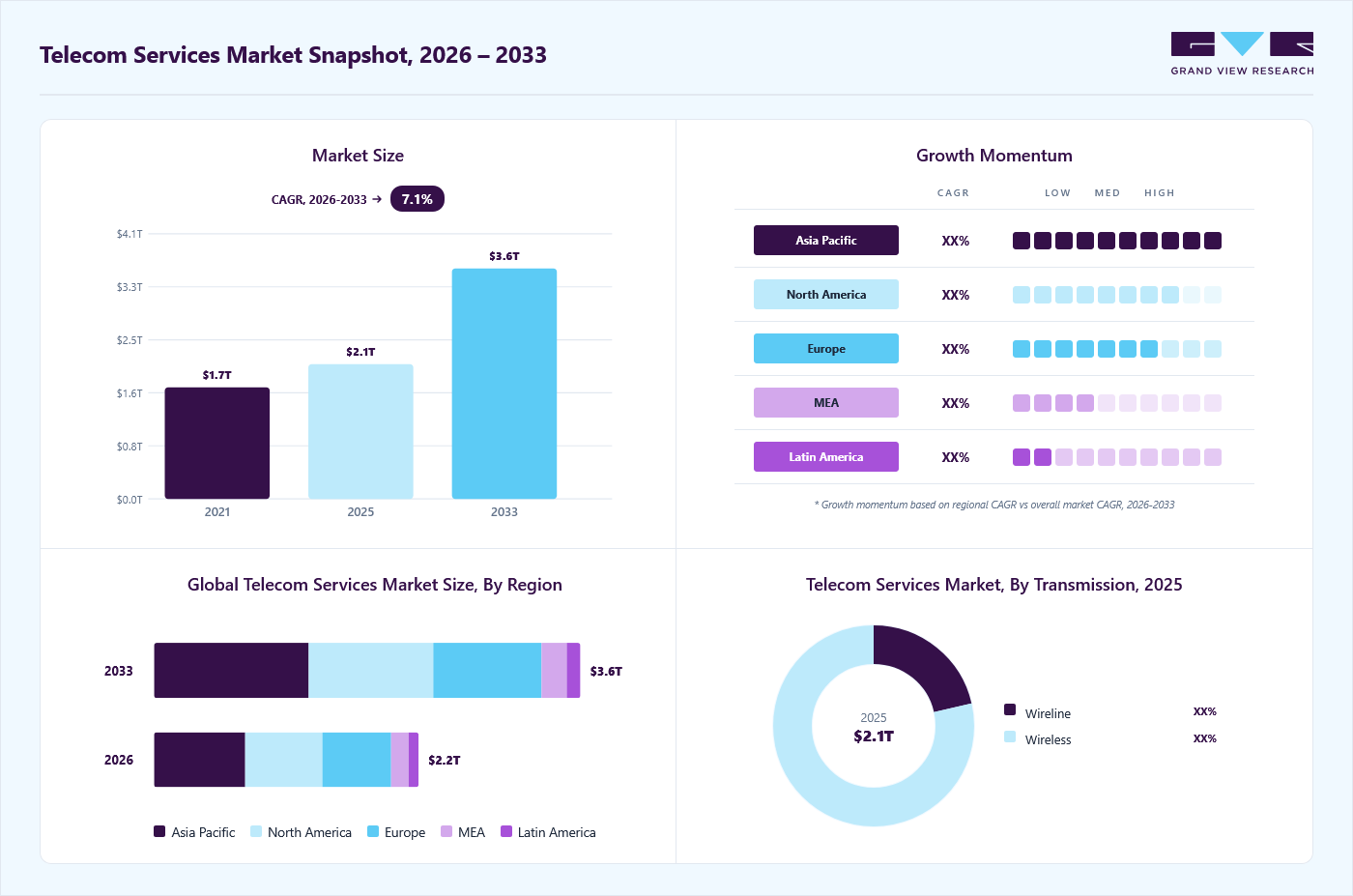

The global telecom services market size was valued at USD 2,095.7 billion in 2025 and is projected to grow from USD 2,224.0 billion in 2026 to USD 3,584.3 billion by 2033, at a CAGR of 7.1% from 2026 to 2033. The market in Asia Pacific dominated with a revenue share of 34.2% in 2025. Rising spending on the deployment of 5G infrastructures due to the shift in customer inclination toward next-generation technologies and smartphone devices is one of the key factors driving this industry.

Key Market Trends & Insights

- By transmission: Wireless segment held the largest market share of 78.6% in 2025.

- By end-use: Consumer/residential segment held the largest market share of 59.1% in 2025.

- By service type: Mobile data services segment held the largest market share of 34.5% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (34.2% revenue share, 2025)

- By country: China held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 2,095.7 Billion

- Estimated market size in 2026: USD 2,224.0 Billion

- Projected market size by 2033: USD 3,584.3 Billion

- CAGR (2026-2033): 7.1%

An increasing number of mobile subscribers, soaring demand for high-speed data connectivity, and the growing demand for value-added managed services are the other potential factors fueling the market growth. The global communication network has undoubtedly been one of the prominent areas for continued technological advancements over the past few decades.")

The industry’s product offering evolved in the late 19th century from only voice and visual signals, such as facsimiles and telegraphs over wired infrastructure, to the current scenario of exchanging audio, video, and text content over numerous wireless infrastructures. The market for telecom services has also witnessed significant improvements in data speeds, from Global System for Mobile communications (GSM) and Code Division Multiple Access (CDMA) to Third Generation (3G), Fourth Generation (4G), and now the commercialization of Fifth Generation (5G) networks. The advent of data connectivity has made it possible the reduction the duration of transferring large chunks of data from days to hours and now to a few seconds.

In today’s digital age, customers favor Over-The-Top (OTT) channels for a variety of reasons, among which the number of viewing options and the pricing offered are the most prominent ones. The OTT solution providers offer video, audio, and other media content over the internet. Usually, they are not bound by price agreements with limited viewing choices. Common OTT applications include Netflix, Amazon Video, Roku, Jio Hotstar, and HBO. Consumers and marketers alike are getting more acquainted with OTT applications and content. Furthermore, smartphone display and sound quality, open-source platforms, and super-fast Internet Protocol (IP) networks, among other innovative services, act as mobilizing factors to draw more consumers to the OTT providers 'freemium-based business models, thus witnessing an ever-growing adoption rate and boosting the market growth.

As people worldwide struggle with the realities of the COVID-19 pandemic, digital entertainment platforms, as well as the global telecom service providers, have benefited from the current scenario due to their industry type and business model. In the current global lockdown, a shift among the masses to remote work will fuel demand for network connectivity and infrastructure. Similarly, the temporary shutdown of multiplexes and other outdoor entertainment venues due to strict social distancing measures has increased the use of digital platforms, including social media, gaming, and OTT services. The mobile voice traffic has also witnessed an upsurge during this period, with prominent communication operators reporting an enormous escalation in their voice traffic since the outbreak of the pandemic.

However, the escalating consumption of digital media platforms by global customers has resulted in the sudden demand for higher bandwidths with high-speed connectivity. With the upsurge in the consumption of these platforms, the telecom service companies are urging OTT providers to reduce the streaming resolution of their media content. In fact, the Cellular Operators Association of India (COAI) has requested that video streaming providers reduce the quality of their content from High Definition (HD) to Standard Definition (SD). To avoid the congestion in internet traffic, especially when most people are working from home and require high bandwidth, some governments are also helping the market for telecom services to ensure the smooth functioning of their data and voice carriers.

Service Type Insights

The mobile data services segment led the market with the largest revenue share of 34.5% in 2025 and is projected to grow at the fastest CAGR during the forecast period. This is attributed to the significant growth in smartphone use among consumers. Rapidly rising demand for high-speed broadband services for corporate and residential applications is further expected to bolster the segment growth over the forecast period. Moreover, a massive demand for accessing online 4K UHD videos and playing online cloud gaming is estimated to spur the data services market growth.

The machine-to-machine (Mobile IoT) services segment is anticipated to grow at a significant CAGR during the forecast period. The evolution of the Internet of Things (IoT) devices has raised its proliferation across several industry verticals, including healthcare, manufacturing, energy and utilities, and the public sector, among others. The number of IoT-connected devices is expected to exceed 50 billion by 2030. The rapidly growing IoT devices would require high-speed data connectivity to operate and communicate seamlessly. Therefore, the demand for telecom services is expected to grow significantly in the machine-to-machine segment over the forecast period.

Transmission Insights

The wireless segment accounted for the largest market revenue share of 78.6% in 2025 and is projected to grow at the fastest CAGR during the forecast period. The advent of cloud computing, artificial intelligence, and IoT is expected to significantly contribute to the growth of wireless communication channels worldwide. Over the years, systems for Wireless Local Area Networks (WLANs) have enabled internet access on cellular devices in private homes, public spaces, airports, office buildings, cafeterias, and other areas. Such wireless densification to simplify work processes and automate routine testing is expected to be beneficial, thereby driving robust CAGR in the coming years.

The wireline segment is expected to grow at a significant CAGR over the forecast period. Wireline communication involves the transfer of information via twisted pair, coaxial, and optical fiber cables. The wireless method transmits information Over-The-Air (OTA) using transmitters and receivers and Radio Frequency (RF) waves. The moderate growth of the wireline segment is attributed to the rising number of SMEs and MNCs in countries such as the UK, the U.S., and China that utilize extensive networks of the Public Switched Telephone Network (PSTN) and the Integrated Services Digital Network (ISDN).

End-use Insights

The consumer/residential segment led the market with the largest revenue share of 59.1% in 2025. The significant growth is ascribed to the proliferation of smartphones worldwide. The private telecom operators account for a larger subscriber base as compared to government-owned companies. In addition, the growing demand for OTT applications is prompting the users to subscribe to wireless internet offerings, thereby significantly contributing to the deployment of communication networks at a broader level. In addition, the growing trend of using ultra-high-definition videos and online gaming is expected to boost the segment growth over the forecast period.

The business segment is expected to grow at the fastest CAGR over the forecast period. The demand for telecom services is increasing in business applications with the deployment of next-generation high-speed networks. Businesses are installing 5G small cell networks and private LTE and 5G networks to access faster data bandwidth and avoid network latency. The enhanced bandwidth connectivity would help businesses cater to their clients' requirements with minimum waiting time and improve the overall customer experience. Moreover, the key business application areas include VoIP services, fixed and mobile data connectivity, unified communication, and other services. To handle a rapidly increasing volume of customers’ datasets, it would require unified, high-speed network connectivity across businesses globally. This, in turn, is estimated to fuel the segment growth from 2026 to 2033.

Regional Insights

Asia Pacific dominated the global telecom services market with the largest revenue share of 34.2% in 2025. The region is likely to attract more than half of the new mobile subscribers by 2030. The regional market is primarily driven by e-commerce and retailer buy-in platforms, smartphone ubiquity, and investments in 5G networks. China, Japan, and India have emerged as significant contributors to regional market growth. According to industry analysis, in February 2022, China recorded 1.02 billion internet users, more than three times the number of the third-placed United States, which had just over 307 million. India recorded the second-highest number of internet users in February 2022.

The telecom services market in China is expected to grow rapidly over the forecast period. The increasing number of 5G connections across China is a major factor driving the growth of the market. According to the GSMA’s The Mobile Economy China 2023 report, by the end of 2022, the number of 5G base stations in China surpassed 2.3 million, with around 887,000 installed during the year.

The India telecom services market is experiencing rapid growth. Rapid advancements in 5G network deployment are at the forefront, enabling faster connectivity and fostering innovations in sectors such as IoT, smart cities, and industrial automation.

North America Telecom Services Market Trends

The telecom services market in North America is expected to grow at a significant CAGR during the forecast period, driven by the presence of prominent players, such as AT&T Inc., Verizon Communications Inc., and T-Mobile US, Inc., as well as the growing adoption of mobile services in the region. For instance, according to the Mobile Economy North America 2022 report by GSMA, nearly 329 million people, or 84% of the population in North America, subscribed to mobile services in 2021.

The telecom services market in the U.S. accounted for the largest market revenue share in North America in 2025. In the U.S., the launch of 5G services has opened access to high-speed internet for people. The growing adoption of 5G technology in the manufacturing industry is particularly anticipated to contribute to the market growth over the forecast period.

Europe Telecom Services Market Trends

The telecom services market in Europe was identified as a lucrative region in 2025. The telecommunications industry is one of Europe’s growing, technology-based industries. The infrastructures the incumbents of the industry are rolling out are laying the foundation for green and digital transformation by accelerating the adoption of edge computing, 5G, cloud computing, and mobile IoT, among other latest technologies. The increasing adoption of these advanced technologies by businesses and consumers is driving the demand for telecom services in the region.

The UK telecom services market is characterized by technology-driven changes, delivering new, innovative services to both consumers and businesses. According to the Office of Communications (Ofcom), as of Q2/2023, there were 28.2 million fixed broadband lines in the UK, an increase of 139,000, or 0.5%, over the year

The telecom services market in Germany held a substantial market share in Europe in 2025. The rapid growth in the number of internet users is a major factor driving the growth of the telecom services industry in Germany. For instance, according to the data published by the World Bank, in 2022, 92% of the total population in Germany used the internet, up from 82% in 2010.

The Italy telecom services market held a substantial market share in Europe in 2025. The A strong ongoing trend driving the Italy telecom services industry is the accelerated deployment of high-speed connectivity, notably 5G and fiber-optic networks, which is expanding ultra-broadband access, enabling IoT and digital services, and reshaping consumer and enterprise demand.

Key Telecom Services Company Insights

Some of the key companies in the telecom services industry include Verizon Communications Inc., Deutsche Telekom AG, China Mobile Limited, and others. All these market players are investing aggressively to introduce innovative and application-specific services as part of their efforts to strengthen their foothold in the market.

-

Verizon Communications Inc. has been at the forefront of the telecom services industry, delivering cutting-edge solutions across wireless, wireline, and enterprise segments. By leveraging its 5G Ultra Wideband network, Verizon continues to enhance connectivity, supporting innovations such as private networks, edge computing, and IoT solutions.

-

Deutsche Telekom AG offers mobile and fixed network solutions to its business customers and individual consumers worldwide. Deutsche Telekom AG is one of the prominent players in the telecom services industry, providing a comprehensive portfolio that includes high-speed internet, cloud services, and IoT integration. With a robust presence in Europe and expanding global operations, the company emphasizes digital transformation and innovation across its services.

Key Telecom Services Companies:

The following key companies have been profiled for this study on the Telecom Services market.

- AT&T Inc.

- China Mobile Limited

- China Telecom Corporation Limited

- Deutsche Telekom AG

- Nippon Telegraph and Telephone Corporation

- SoftBank Corp.

- Orange S.A.

- Telefonica S.A.

- Verizon Communications Inc.

- Vodafone Group Plc

- KDDI Corporation

Recent Developments

-

In February 2026, Ericsson launched Agentic rApp as a Service (rApp aaS), a cloud-based, AI-driven network optimization solution designed to help telecom operators move toward autonomous networks. Built on Amazon Web Services, the platform uses agentic AI and generative AI to automate network optimization workflows and enables engineers to interact with networks through a natural-language interface. Delivered via AWS Marketplace, the as-a-service model reduces infrastructure complexity and capital expenditure while allowing scalable, on-demand deployment.

-

In May 2023, Verizon Communications Inc. announced plans to deploy 5G Ultra Wideband in multiple markets across the U.S. states of Wisconsin, Illinois, Ohio, Arizona, Pennsylvania, and West Virginia by utilizing up to 100 MHz of the C-Band spectrum it acquired recently. Plans called for the company to add more bandwidth once the licensed spectrum is available in its entirety. The additional bandwidth would be available by the end of 2023 and would help provide exceptional capacity and speed.

-

In February 2023, AT&T Inc. and ServiceNow, a software company, announced a telecom product that can assist Communication Service Providers (CSPs) in managing their inventory of 5G and fiber networks. The ServiceNow Telecom Network Inventory has been developed with AT&T Inc.'s valuable input on strategic design and technical aspects. The product has been built on the ServiceNow Platform and is accessible to telecom companies worldwide.

Telecom Services Market Report Scope

Report Attribute

Details

Market size in 2025

USD 2,095.7 billion

Estimated market size in 2026

USD 2,224.0 billion

Projected market size by 2033

USD 3,584.3 billion

Growth rate

CAGR of 7.1% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company market share, competitive landscape, growth factors, and trends

Segments covered

Service type, transmission, end-use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; China; Japan; India; South Korea; Australia; Brazil; Columbia; Peru; Chile; KSA; UAE; South Africa

Key companies profiled

AT&T Inc.; China Mobile Limited; China Telecom Corporation Limited; Deutsche Telekom AG; Nippon Telegraph and Telephone Corporation; SoftBank Corp.; Orange S.A.; Telefonica S.A.; Verizon Communications Inc.; Vodafone Group Plc; KDDI Corporation.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Telecom Services Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global telecom services market report based on service type, transmission, end-use, and region:

-

Service Type Outlook (Revenue, USD Billion, 2021 - 2033)

-

Fixed Voice Services

-

Fixed Internet Access Services

-

Mobile Voice Services

-

Mobile Data Services

-

Pay TV Services

-

Machine-to-Machine (Mobile IoT) Services

-

-

Transmission Outlook (Revenue, USD Billion, 2021 - 2033)

-

Wireline

-

Wireless

-

-

End-use Outlook (Revenue, USD Billion, 2021 - 2033)

-

Consumer/Residential

-

Business

-

IT & Telecom

-

Manufacturing

-

Healthcare

-

Retail

-

Media & Entertainment

-

Government & Defense

-

Education

-

BFSI

-

Energy and utilities

-

Transportation & Logistics

-

Travel & Hospitality

-

O&G and Mining

-

Others

-

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

-

Asia Pacific

-

China

-

India

-

Japan

-

Australia

-

South Korea

-

-

Latin America

-

Brazil

-

Columbia

-

Peru

-

Chile

-

-

Middle East & Africa

-

Kingdom of Saudi Arabia (KSA)

-

UAE

-

South Africa

-

-

Frequently Asked Questions About This Report

The global telecom services market size was valued at USD 2,095.7 billion in 2025 and is estimated at USD 2,224.0 billion for 2026.

The mobile data services held the largest share (over 34.0%) in 2025 and is the fastest-growing type.

Consumer/residential held the largest revenue share of 59.1% in 2025, while business is the fastest-growing segment.

The global telecom services market is expected to grow at a CAGR of 7.1% from 2026 to 2033, reaching USD 3,584.3 billion.

Asia Pacific dominated with a 34.2% revenue share in 2025.

Key factors include rising spending on the deployment of 5G infrastructures, increasing number of mobile subscribers, soaring demand for high-speed data connectivity, and the growing demand for value-added managed services.

Key players include AT&T Inc.; China Mobile Limited; China Telecom Corporation Limited; Deutsche Telekom AG; Nippon Telegraph and Telephone Corporation; SoftBank Corp.; Orange S.A.; Telefonica S.A.; Verizon Communications Inc.; Vodafone Group Plc; KDDI Corporation.

Wireless led with a 78.6% revenue share in 2025 and is the fastest-growing segment.

About the Author(s)

Communication Services Research Team

Technology · Communication ServicesThis report was authored by the communication services research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the communication services segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.