- Home

- »

- Network Security

- »

-

Identity And Access Management Market Size Report, 2033GVR Report cover

![Identity And Access Management Market (2026 - 2033)Report]()

Identity And Access Management Market (2026 - 2033)

Size, Share & Trends Analysis Report By Component (Directory Service, Multifactor Authentication, Provisioning), By Deployment (Cloud, Hybrid), By End Use (Telecom & IT, Education, Healthcare), By Region, And Segment Forecasts

Market Size, 2025

$26.8BMarket Estimate, 2026

$29.7BMarket Forecast, 2033

$62.9BCAGR, 2026–2033

11.3%Identity And Access Management Market Summary

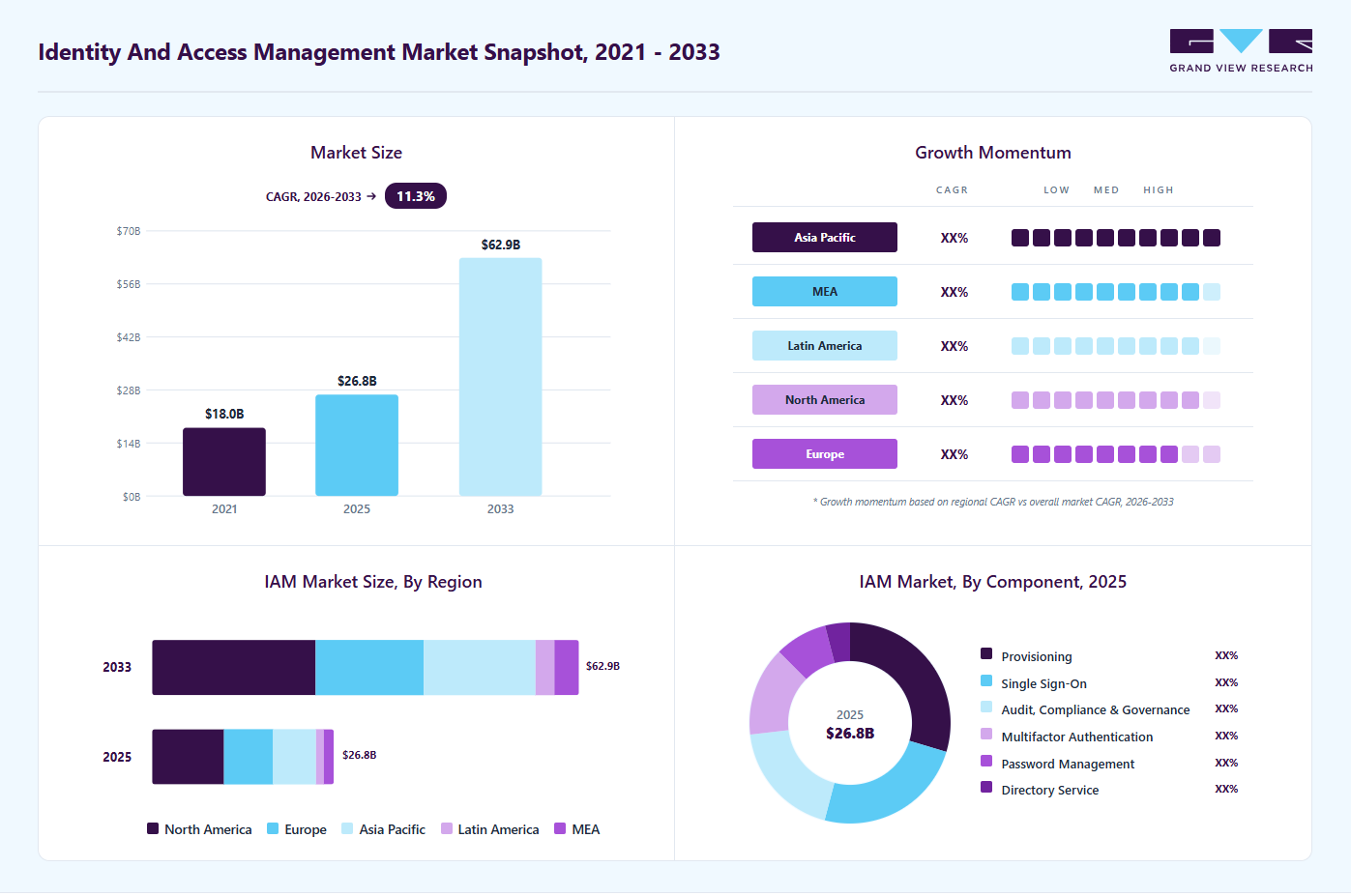

The global identity and access management market size was valued at USD 26.8 billion in 2025 and is projected to grow from USD 29.7 billion in 2026 to USD 62.9 billion by 2033, at a CAGR of 11.3% from 2026 to 2033. North America dominated the market, accounting for 39.4% revenue share in 2025. Several key factors, such as rising cases of cybercrime and the need for secure remote access and third-party integrations, are expected to drive market growth. Identity and access management (IAM) ensures that the appropriate people and job positions (identities) in an organization have access to the tools they need to perform their duties.

Key Market Trends & Insights

- By component: The provisioning segment accounted for the largest revenue share of 29.6% in 2025.

- By deployment: The on-premise segment accounted for the largest share in 2025.

Regional Highlights

- Largest regional market: North America (39.4% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 26.8 Billion

- Estimated market size in 2026: USD 26.2 Billion

- Projected market size by 2033: USD 62.9 Billion

- CAGR (2026-2033): 11.3%

Identity management and access systems allow companies to administer employee apps without having to log in as an administrator to each app. Advances in the internet of things (IoT) and artificial intelligence (AI), rising awareness about regulatory compliance management, increasing reliance on digital platforms & automation, and growing adoption of cloud technologies across industries are estimated to drive the market over the forecast period.The rising cases of fraud and cybercrime are driving organizations to implement IAM systems, driven by the rapid adoption of the cloud and the advancement of new technologies. IAM uses identity analytics and intelligence to monitor unusual user account activity. In addition, it allows for the deletion of inactive accounts, the detection of policy violations, and the removal of inappropriate access privileges. Hence, the rising enterprise identity and security concerns drive the growth of the industry. Moreover, lower production costs make application administration effortless; the centralization of time-consuming processes for connectivity and identity modifications increases user reliability, provides easier access to sign-in, signup, and user management processes for application holders, and implements procedures and policies related to user verification and prerogatives.

")

Furthermore, the integration of the IAM solution and mobile device Management (MDM) may utilize IAM more efficiently and enable the organization’s security and control. MDM is a critical component of IAM as it allows one to control apps and users on the device. Because IAM can be used across multiple devices, extending it to mobile devices is essential for any business. MDM is an essential component of IAM as it provides security and the ability to provision apps to devices. MDM collaborates with IAM to help protect each device and, as a result, create security for the user. Both IAM and MDM are critical to each other. MDM enables businesses to easily implement identity and access management while also providing control and security.

Businesses that choose this system will benefit, but they must be aware that, to avoid vulnerabilities, biometric solutions must be compatible with any smartphone. However, failure to store data, such as personal information and authentication credentials, may result in data breaches and digital identity fraud. Enterprise bring-your-own-device (BYOD) policies have complicated IAM systems. Moreover, recent product innovations focused on securing emerging technologies such as AI agents further highlight the evolving scope of IAM solutions. For instance, in October 2025, Aembit introduced IAM for Agentic AI, enabling secure identity control and access management for autonomous AI agents. The solution uses verified identities, dynamic policy enforcement, and auditable access controls to ensure secure interaction with enterprise systems across cloud and hybrid environments. This launch is expected to drive innovation and expand demand in the identity and access management market.

In conclusion, the increasing incidence of cyber threats and identity-related risks is driving strong adoption of IAM solutions across organizations. The integration of advanced technologies and mobile device management is enhancing security, access control, and operational efficiency. However, high implementation costs and data security challenges may slightly hinder market growth despite rising demand.

Market Dynamics

The growing frequency of cyberattacks, identity theft, phishing incidents, and unauthorized access attempts is significantly driving the growth of the Identity and Access Management (IAM) market. Organizations are increasingly adopting IAM solutions to strengthen authentication processes, secure sensitive enterprise data, manage user identities, and ensure controlled access to critical applications and systems. The rising adoption of cloud computing, remote and hybrid work environments, bring-your-own-device (BYOD) policies, and digital transformation initiatives is further accelerating the demand for centralized and secure identity management platforms.

For instance, in 2025, Microsoft’s Digital Defense Report highlighted that password-based attacks exceeded 7,000 attacks per second globally, reflecting the growing scale of identity-related cyber threats targeting enterprises and individuals. The report also emphasized the increasing adoption of multi-factor authentication (MFA), passwordless authentication, and zero-trust security architectures as organizations seek to strengthen identity protection and reduce unauthorized access risks. Additionally, increasing regulatory requirements for data privacy, identity governance, and access control compliance are encouraging enterprises to implement advanced IAM solutions across cloud and on-premises environments. Therefore, the rising emphasis on zero-trust security, digital identity protection, and secure workforce access management is significantly contributing to the growth of the identity and access management market.

Managing secure access for remote and hybrid work environments is one of the key challenges restraining the growth of the Identity and Access Management (IAM) market. Organizations are increasingly struggling to maintain consistent identity verification, access control, and authentication policies across geographically dispersed employees, third-party users, personal devices, and cloud-based applications. The growing complexity of managing multiple user identities, endpoints, and access privileges across hybrid IT environments often increases operational burden, implementation complexity, and security risks for enterprises.

For instance, according to a 2024 cybersecurity workforce and identity security survey by the Identity Defined Security Alliance (IDSA), organizations reported that remote work environments significantly increased identity-related risks, particularly due to credential misuse, excessive access privileges, and unmanaged devices. Many enterprises also highlighted difficulties in enforcing consistent multi-factor authentication (MFA), privileged access management, and real-time identity monitoring across remote users and distributed infrastructures. As a result, enterprises often face challenges related to user experience, access governance, integration with legacy systems, and continuous monitoring, which can slow down IAM deployment and adoption within certain organizations and industries.

Market Concentration & Characteristics

The Identity and Access Management (IAM) market is moderately concentrated, with several large global cybersecurity and enterprise software providers dominating the competitive landscape. Major players such as Microsoft, IBM, Okta, Cisco, Oracle, Ping Identity, and CyberArk hold substantial market share due to their broad IAM portfolios, cloud security expertise, strong enterprise relationships, and integrated authentication and governance capabilities. However, the market also includes a growing number of niche and emerging vendors specializing in passwordless authentication, biometric identity verification, privileged access management (PAM), decentralized identity, and AI-driven identity analytics, contributing to competitive diversification.

The IAM market demonstrates a high degree of innovation, driven by rapid advancements in cloud computing, artificial intelligence (AI), machine learning, zero-trust security frameworks, biometric authentication, and passwordless identity solutions. The market is witnessing moderate-to-high merger and acquisition (M&A) activity, as cybersecurity vendors and cloud platform providers acquire specialized identity security firms to strengthen authentication, governance, and privileged access capabilities. Regulatory impact is significant, with data privacy and cybersecurity regulations such as GDPR, HIPAA, CCPA, PCI-DSS, and zero trust mandates accelerating enterprise adoption of IAM solutions. Service substitutes remain relatively limited because IAM platforms are becoming foundational components of enterprise cybersecurity architectures, although standalone authentication and directory management tools still exist in some environments. Additionally, the market exhibits high end-user concentration among large enterprises, BFSI organizations, healthcare providers, government agencies, and IT & telecom companies due to their high identity security requirements, complex user environments, and strict regulatory compliance obligations.

Component Insights

The provisioning segment accounted for the largest revenue share of 29.6% in 2025. This segment is witnessing strong growth due to the increasing complexity of IT environments, particularly with the rapid adoption of cloud-based applications, hybrid work models, and multi-platform infrastructures, which require organizations to efficiently manage user lifecycles at scale. A key driver is the growing need to comply with stringent data protection regulations, where automated provisioning helps ensure that access rights are assigned according to predefined policies and revoked promptly to minimize security risks. Additionally, the growing frequency of insider threats and unauthorized access incidents is prompting enterprises to adopt advanced provisioning solutions that integrate with identity governance frameworks to provide real-time visibility and control. As organizations continue to prioritize operational efficiency and risk mitigation, the provisioning segment is expected to remain a fundamental component driving the overall growth of the IAM market.

The multifactor authentication segment is anticipated to grow at the fastest CAGR from 2026 to 2033. MFA enhances security by requiring users to provide multiple forms of authentication, such as passwords, biometrics, or one-time passcodes, thereby significantly reducing the risk of unauthorized access. A key driving factor for this segment is the rapid rise in credential-based attacks, particularly phishing and password breaches in cloud-based environments, which has compelled enterprises to move beyond single-factor authentication. Additionally, the growing adoption of remote and hybrid work models has further accelerated demand for MFA solutions to secure access across distributed networks and devices. As regulatory requirements around data protection and user identity verification continue to tighten across industries, MFA is becoming a standard security layer rather than an optional feature. Consequently, the segment is expected to maintain strong momentum, supported by continuous advancements in biometric technologies and adaptive authentication methods, reinforcing its critical role in modern IAM frameworks.

Deployment Insights

The on-premise segment accounted for the largest revenue share in 2025. A key driver of this segment is the growing need for data sovereignty and regulatory compliance, especially in industries such as banking, healthcare, and the public sector, where organizations must ensure that critical identity data remains within their internal environments to meet stringent national and industry-specific regulations. Additionally, on-premises IAM solutions offer greater customization and integration with legacy systems, which is essential for enterprises operating complex, long-established IT architectures. While cloud-based IAM adoption is rising, concerns around third-party data handling, security breaches, and limited visibility continue to encourage organizations to retain on-premise deployments.

The cloud segment is anticipated to grow at the fastest CAGR during the forecast period. Organizations are adopting cloud IAM solutions to enable centralized identity control, seamless user provisioning, and real-time access monitoring across distributed systems and applications. A key driving factor is the rising need to secure remote access and third-party integrations as businesses rely more on SaaS platforms and multi-cloud environments, which require scalable, flexible identity governance without heavy on-premises infrastructure. As cybersecurity threats continue to evolve and digital transformation accelerates, the cloud segment is expected to remain a critical enabler of secure and agile identity management strategies.

End Use Insights

The public sector & utilities segment accounted for the largest market share in 2025, driven by the need to secure critical infrastructure, sensitive citizen data, and essential service operations. Government bodies and utility providers, including energy, water, and transportation agencies, are increasingly adopting IAM solutions to strengthen access control, ensure regulatory compliance, and protect against rising cyber threats targeting national infrastructure. In conclusion, as public sector entities and utility organizations continue to modernize their systems while facing heightened security risks, the demand for advanced IAM solutions is expected to grow steadily, ensuring secure, efficient, and resilient service delivery.

The BFSI segment is anticipated to grow at the highest CAGR from 2026 to 2033, driven by the sector’s critical need to safeguard sensitive financial data, ensure regulatory compliance, and maintain customer trust. Financial institutions are increasingly adopting IAM solutions to address rising cyber threats, particularly sophisticated fraud, account takeovers, and insider risks, while also complying with stringent regulations such as KYC and data protection mandates. As a result, IAM solutions are becoming essential for enabling secure digital transformation in the BFSI sector, supporting both risk mitigation and enhanced customer experience, thereby driving sustained market growth.

Regional Insights

North America identity and access management market held the major share of over 39.4% in 2025, driven by the region’s highly advanced digital infrastructure, strong presence of major technology providers, and early adoption of cloud and cybersecurity solutions. Organizations across the United States and Canada are rapidly implementing IAM systems as part of large-scale digital transformation and cloud migration initiatives. In addition, stringent regulatory requirements around data privacy and compliance further accelerate IAM adoption across sectors such as BFSI, healthcare, and public services. Supported by continuous innovation and strong cybersecurity spending, North America is expected to maintain its dominance in the IAM market, with sustained growth driven by the need for secure, scalable, and compliant identity management solutions.

U.S. Identity and Access Management Market Trends

The identity and access management market in the U.S. is expected to grow significantly from 2026 to 2033, driven by the country’s highly digitalized economy, widespread cloud adoption, and increasing frequency of sophisticated cyberattacks targeting enterprises and government agencies. Organizations across sectors such as finance, healthcare, and federal services are prioritizing IAM solutions to manage complex user identities, enforce strict access controls, and comply with evolving regulatory frameworks such as zero trust security mandates issued by the federal government.

Asia Pacific Identity and Access Management Market Trends

The identity and access management market in Asia Pacific is growing significantly from 2026 to 2033, driven by rapid digital transformation, expanding cloud adoption, and increasing cybersecurity awareness across both developed and emerging economies. Countries such as China, India, Japan, and Southeast Asian nations are witnessing a surge in mobile-first users, e-commerce platforms, and digital government services, which has significantly increased the volume of digital identities requiring secure management. The overall outlook remains highly positive as enterprises increasingly prioritize IAM solutions to mitigate cyber risks, ensure compliance, and support long-term digital growth strategies.

China identity and access management market held a significant share in 2025, supported by the country’s rapid digital transformation across government, finance, manufacturing, and e-commerce sectors. A key driving factor specific to China is the strong regulatory environment, particularly under frameworks such as the Cybersecurity Law and the Personal Information Protection Law (PIPL), which require organizations to implement strict identity verification, data access control, and user accountability measures.

The identity and access management market in Japan held a significant share in 2025, supported by the country’s strong focus on cybersecurity, digital transformation, and regulatory compliance. A key driving factor is Japan’s accelerated adoption of cloud services and remote work models, particularly among large enterprises and government institutions, which has increased the need for secure and centralized identity control across distributed IT environments.

India identity and access management market is expanding rapidly, driven by the rapid digital transformation across sectors such as banking, government, healthcare, and IT services. The widespread adoption of cloud-based platforms, coupled with initiatives like Digital India and increasing reliance on remote and hybrid work models, has significantly expanded the digital identity landscape, making robust access control a critical requirement.

Europe Identity and Access Management Market Trends

The identity and access management market in Europe is growing significantly from 2026 to 2033. A key region-specific driver is the presence of stringent regulatory frameworks such as GDPR, NIS2, and DORA, which mandate strict access controls, multi-factor authentication, and identity governance, compelling enterprises and public institutions to adopt advanced IAM platforms to ensure compliance and avoid heavy penalties. Additionally, initiatives like the European Digital Identity framework are further accelerating demand by standardizing secure digital identities across member states. As a result, enterprises are increasingly shifting toward zero-trust architectures and centralized identity management systems. In conclusion, the Europe IAM market is set for sustained growth, supported by regulatory pressure, evolving cybersecurity risks, and the region’s strong focus on data privacy and digital sovereignty.

The identity and access management market in the UK is expected to grow rapidly in the coming years, driven by the country’s strong regulatory environment, increasing cyber threats, and rapid digital transformation across both public and private sectors. Organizations are prioritizing IAM solutions to comply with stringent data protection regulations such as the UK GDPR, while also addressing the rising frequency of identity-based cyberattacks, including phishing and credential misuse.

Germany identity and access management market held a significant market share in 2025, driven by a stringent data protection framework, including GDPR compliance and national regulations such as the IT Security Act 2.0, which require organizations, especially in banking, manufacturing, and critical infrastructure, to implement robust identity governance and access controls. In addition, the country’s strong industrial base and growing use of IIoT and hybrid IT environments are accelerating demand for IAM solutions to secure both human and machine identities.

Key Identity and Access Management Company Insights

Some of the key companies operating in the market, include Amazon Web Services, Inc., Broadcom, One Identity LLC., ForgeRock, HID Global Corp., IBM Corporation, McAfee, LLC, among others are some of the leading participants in the identity and access management market.

-

In March 2026, SailPoint partnered with Amazon Web Services to develop a unified identity governance layer for managing human and AI-driven identities. The solution enables secure access control, lifecycle management, and policy enforcement across cloud environments, supporting scalable and secure deployment of agentic AI systems. This collaboration is expected to accelerate adoption of identity-first security approaches and drive growth in the identity and access management market.

-

In June 2025, LoginRadius launched Partner IAM, a purpose-built identity solution for managing external users such as partners and customers in B2B ecosystems. The platform offers granular access control, secure authentication, and scalable identity management, addressing limitations of traditional workforce IAM systems and improving security and operational efficiency. This launch is expected to drive demand for specialized IAM solutions and accelerate growth in the identity and access management market.

-

In March 2025, Axonius launched Axonius Identities, a unified platform that integrates identity governance, security posture management, threat detection, and lifecycle management. The solution enhances visibility, automation, and compliance across enterprise environments, enabling proactive identity security and reducing risks associated with fragmented IAM systems. This launch is expected to accelerate the adoption of integrated identity security platforms and drive growth in the identity and access management market.

Key Identity And Access Management Companies:

The following key companies have been profiled for this study on the identity and access management market.

- Amazon Web Services, Inc.

- Broadcom

- One Identity LLC.

- ForgeRock

- HID Global Corp.

- IBM Corporation

- McAfee, LLC

- Microsoft

- Okta

- OneLogin

- Oracle

- Ping Identity

- SecureAuth

- Evidian

- Intel Corp.

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weakness

Mature Players: Microsoft (Entra ID); AWS; IBM Corporation; Oracle; Broadcom (Symantec); Okta; Ping Identity (inc. ForgeRock); One Identity (inc. OneLogin); HID Global Corp.

- Prioritizing the unification of acquired brands into a single "Identity Fabric" that covers IGA, PAM, and Access Management.

- Deeply embedding identity services into broader cloud platforms to make them the "default" choice for enterprise workloads.

- Moving away from standalone tools toward unified platforms that manage both standard employee access and high-risk privileged accounts in one dashboard.

- Holding the "Source of Truth" for millions of identities, creating extreme stickiness and making it nearly impossible for large enterprises to fully displace.

- Proven ability to handle massive, complex regulatory requirements across diverse jurisdictions (GDPR, HIPAA, SOC2) with automated auditing.

- The capital to integrate advanced Generative AI to automate identity lifecycle tasks and detect sophisticated "deepfake" login attempts.

- Post-merger transitions can lead to temporary roadmap confusion and support delays as product teams attempt to merge disparate codebases.

- Older on-premise suites from giants like Oracle or IBM can be cumbersome to manage and slower to update compared to nimble, cloud-first competitors.

Emerging Players: SecureAuth; Evidian; Intel Corp.; Saviynt; CyberArk; Strata Identity; BeyondTrust

- Leading the push toward a "passwordless" future using biometrics and FIDO2 standards to eliminate the primary vector for credential theft.

- Focusing on the "Identity Gap" using software to bridge and manage multiple inconsistent identity providers across hybrid-cloud environments.

- Tailoring identity solutions for specific high-security hardware needs or European-specific sovereign cloud requirements.

- Ability to deploy bleeding-edge features such as "Continuous Adaptive Authentication" months or years before the larger, slower-moving incumbents.

- Focusing exclusively on a specific identity problem, resulting in a more polished and efficient user experience.

- Providing "neutral" platforms that allow enterprises to switch cloud providers without having to rebuild their entire identity architecture.

- High-performing specialists are frequent targets for acquisition by Mature Players, which can lead to concerns about long-term platform independence.

- Lacking the massive global field teams and 24/7 support infrastructure required to win and maintain "all-of-government" or global tier-1 banking contracts.

Identity And Access Management Market Report Scope

Report Attribute

Details

Market size in 2025

USD 26.8 billion

Market size value in 2026

USD 29.7 billion

Revenue forecast in 2033

USD 62.9 billion

Growth rate

CAGR of 11.3% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Component, deployment, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Thailand; Brazil; UAE; Saudi Arabia; South Africa

Key companies profiled

Amazon Web Services, Inc.; Broadcom; One Identity LLC.; ForgeRock; HID Global Corp.; IBM Corporation; McAfee, LLC; Microsoft; Okta; OneLogin; Oracle; Ping Identity; SecureAuth; Evidian, Intel Corp.

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Identity and Access Management Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global identity and access management market report based on component, deployment, end use, and region.

-

Component Outlook (Revenue, USD Billion, 2021 - 2033)

-

Audit, Compliance & Governance

-

Directory Service

-

Multifactor Authentication

-

Provisioning

-

Password Management

-

Single Sign-On

-

-

Deployment Outlook (Revenue, USD Billion, 2021 - 2033)

-

On-premises

-

Cloud

-

Hybrid

-

-

End Use Outlook (Revenue, USD Billion, 2021 - 2033)

-

BFSI

-

Energy, Oil & Gas

-

Telecom & IT

-

Education

-

Healthcare

-

Public Sector & Utilities

-

Manufacturing

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

Thailand

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Zero trust and passwordless authentication adoption assessment for an enterprise security provider

- Analysis of enterprise adoption trends for zero trust architecture, MFA, and passwordless authentication across industries

- Evaluation of regulatory and compliance impact on IAM deployment strategies

- Identified high-growth authentication segments and enterprise demand trends

- Supported product positioning and security roadmap development

Identity governance and privileged access management benchmarking for a cybersecurity vendor

- Comparative assessment of leading IAM and PAM vendors based on scalability, AI capabilities, and cloud integration

- Analysis of customer preferences for identity lifecycle management and privileged access controls

- Highlighted competitive differentiation opportunities

- Supported go-to-market and feature enhancement strategies

Regional IAM investment and cloud identity security opportunity analysis for a cloud technology company

- Assessment of IAM spending patterns and cloud identity security adoption across North America, Europe, and the Asia Pacific

- Evaluation of demand for workforce identity, customer identity, and hybrid cloud access management solutions

- Identified attractive regional expansion opportunities

- Supported strategic investment and partnership planning

Frequently Asked Questions About This Report

Key factors that are driving the market growth include increasing implementation of IAM solution for business facilitation, improving operational efficiency, and increasing security concerns among organizations.

Key players include Oracle Corporation, IBM Corporation, CA Technologies, NetIQ Corporation (Micro Focus), HID Global Corporation.

The provisioning segment led with a 29.6% revenue share in 2025, while multifactor authentication is the fastest-growing segment.

The on-premise held the largest revenue share in 2025, while cloud is the fastest-growing area.

The public sector & utilities held the largest share in 2025 and BFSI is the fastest-growing.

Asia Pacific is the fastest-growing region over the forecast period.

The global identity and access management market size was estimated at USD 26.8 billion in 2025 and is expected to reach USD 29.7 billion in 2026.

The global identity and access management market is expected to grow at a compound annual growth rate of 11.3% from 2026 to 2033 to reach USD 62.9 billion by 2030.

North America dominated the identity and access management market with a share of 39.4% in 2025.

About the Author(s)

Network Security Research Team

Technology · Network SecurityThis report was authored by the network security research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the network security segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.