- Home

- »

- Next Generation Technologies

- »

-

Integrated Cloud Management Platform Market Report, 2033GVR Report cover

![Integrated Cloud Management Platform Market Size, Share & Trends Report]()

Integrated Cloud Management Platform Market (2025 - 2033) Size, Share & Trends Analysis Report By Component (Solutions, Services), By Deployment Mode, By Organization Size, By End Use, By Region, And Segment Forecasts

Market Size, 2024

$6.6BMarket Estimate, 2026

$7.4BMarket Forecast, 2033

$22.1BCAGR, 2025–2033

14.6%Integrated Cloud Management Platform Market Summary

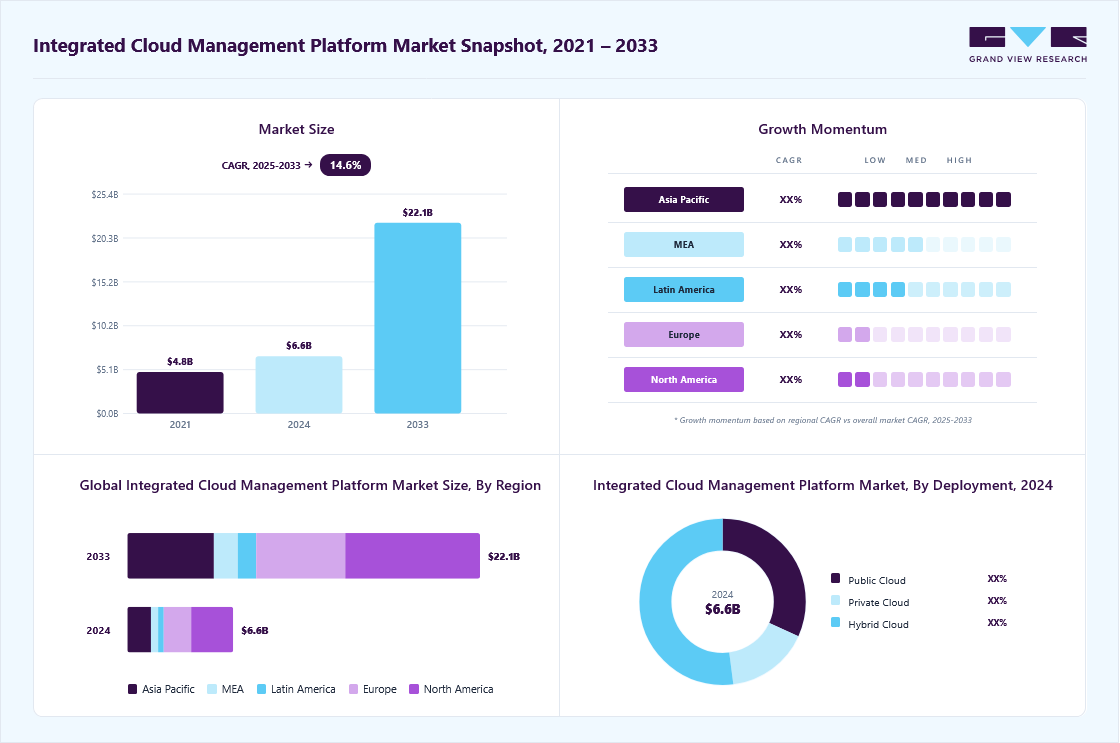

The global integrated cloud management platform market size was estimated at USD 6.62 billion in 2024 and is projected to reach USD 22.10 billion by 2033, growing at a CAGR of 14.6% from 2025 to 2033. Enterprises need unified visibility and control across fragmented cloud environments, leading to demand for platforms that can manage workloads in public, private, and on-premises infrastructure.

Key Market Trends & Insights

- In 2024, North America held a 39.7% revenue share of the global integrated cloud management platform market.

- In the U.S., the market is driven by the rise of remote and hybrid work models which have increased deployment of ICMPs to ensure real-time visibility and secure access across distributed infrastructures.

- By component, the solutions segment held the largest revenue share of 65.2% in 2024.

- By organization size, the large enterprises segment held the largest revenue share in 2024.

Market Size & Forecast

- 2024 Market Size: 6.62 Billion

- 2033 Projected Market Size: USD 22.10 Billion

- CAGR (2025-2033): 14.6%

- North America: Largest market in 2024

- Asia Pacific: Fastest-growing market

Automation and AI-powered cloud operations are significantly reshaping the integrated cloud management platform market. Traditional approaches of monitoring, provisioning, and scaling are insufficient, especially as enterprises seek to optimize performance and control costs. By embedding AI and machine learning capabilities into integrated cloud management platforms, businesses leverage predictive analytics and ensure real-time responsiveness. For instance, in February 2024, Dynatrace introduced AI-driven observability within its cloud platform, leveraging its Davis AI engine to enable proactive issue detection and automated remediation across dynamic cloud environments. This innovation helps enterprises reduce mean time to resolution (MTTR), improve uptime, and significantly lower operational overhead, highlighting the growing reliance on AI-powered automation in modern cloud management.")

Key trend fueling market growth is the integration of Integrated Cloud Management Platforms with advanced analytics and marketing automation tools. By capturing user information during login, businesses can build first-party data sets that are valuable in a privacy-first digital environment. This enables personalized marketing, customer segmentation, loyalty program integration, and real-time promotions, which improve customer retention and increase revenue per user. For instance, in April 2025, SplashAccess updated its compatibility with Cisco Meraki, offering businesses branded, secure Wi-Fi login portals that capture user data while meeting privacy regulations. This setup enables personalized experiences, automated marketing, and real-time insights, turning guest Wi-Fi into a powerful tool for customer engagement and business growth.

Additionally, the growing emphasis on cost governance and FinOps integration is a key driver accelerating the adoption of Integrated Cloud Management Platforms, as organizations seek better visibility and control over complex cloud expenditures. In multi-cloud and hybrid environments, enterprises often encounter rising costs, unmanaged shadow IT, and complex billing structures across different cloud providers. Integrated platforms with built-in FinOps capabilities enable centralized tracking, forecasting, and budget enforcement, thereby making cloud spending more accountable.

Component Insights

The solution segment dominated the market and accounted for the largest share of 65.2% in 2024 due to the growing trend of embedding AI capabilities, including autonomous, intelligent agents designed to independently manage cloud environments. These AI agents learn from system metadata, predict operational needs, and execute tasks such as data integration, workload orchestration, and policy enforcement without manual input. As enterprises adopt multi-cloud and hybrid strategies, the need for intelligent management tools is rising, thus making agentic AI a key driver for the integrated cloud management platform market growth. For instance, in May 2025, Informatica launched Agentic AI offerings, including CLAIRE GPT and CLAIRE Agents, as part of its AI-powered Intelligent Data Management Cloud (IDMC) platform. These agents enable no-code orchestration of autonomous data workflows, enforce governance policies across cloud ecosystems, and support intelligent metadata interactions. Therefore, the growing adoption of solutions due to the aforementioned benefits is contributing significantly in driving the growth of the solutions segment.

The service segment is projected to be the fastest-growing segment during the forecast period due to the increasing complexity of hybrid and multi-cloud deployments, which require expertise for successful implementation, customization, and ongoing support. As organizations migrate from traditional infrastructure to the cloud, the demand for professional services such as consulting, integration, and training is increasing. Additionally, managed services are witnessing adoption as enterprises seek to outsource continuous monitoring, maintenance, and optimization of their cloud ecosystems. For instance, in March 2024, IBM Consulting expanded its Cloud Transformation Services portfolio to include advanced support for AI-enabled cloud management tools, enabling clients to accelerate time-to-value while ensuring compliance and operational resilience. Therefore, the rising reliance on specialized service providers for both strategic transformation and everyday operations is a key factor driving the growth of the services segment within the integrated cloud management platforms market.

Deployment Mode Insights

The Hybrid Cloud segment dominated the market in 2024, due to rising demand for operational consistency and intelligent workload mobility across private and public clouds. Organizations seek platforms that offer integrated automation and cross-environment observability, which are the core features enabled by modern hybrid strategies. Additionally, enterprises are also prioritizing consistent infrastructure and policy enforcement across clouds to improve governance and reduce complexity, while lowering operational costs and enhancing time-to-value for cloud-native applications. For instance, in August 2024, Broadcom introduced major enhancements in VMware Cloud Foundation 5.1 and the vSphere+ platform, delivering a unified hybrid cloud infrastructure with built-in automation and AI-ready architecture. These updates empower organizations to standardize infrastructure and services in public clouds, significantly accelerating application deployment and enabling a 30-50% improvement in IT productivity.

The Private Cloud segment is projected to be the fastest-growing segment over the forecast period due to the increasing demand for data sovereignty, regulatory compliance, and enhanced control over infrastructure among enterprises. Private cloud deployments provide organizations with greater transparency and security, allowing them to meet privacy standards without relying on third-party public cloud environments. Additionally, the evolution of AI-ready infrastructure and hyperconverged systems is making private clouds more scalable and cost-effective. For instance, in April 2024, Dell Technologies launched new updates to its Apex Cloud Platform for Microsoft Azure, enabling enterprises to deploy consistent Azure services within their own data centers with full control, enhanced performance, and built-in compliance capabilities. Therefore, the increasing private cloud adoption, particularly among large organizations, is driving the market growth.

Organization Size Insights

The Large Enterprises segment dominated the market in 2024 due to their global-scale IT operations that require centralized governance and automation across multi-cloud and hybrid environments. These enterprises operate in regulated sectors, where consistent policy enforcement, data sovereignty, and performance reliability are essential. As large enterprises adopt digital transformation, they require ICMP solutions that streamline operations and support resilient infrastructure management at scale. For instance, in October 2024, Citi and Google Cloud announced a strategic agreement to modernize Citi’s core platforms using Google Cloud’s AI-driven infrastructure and cloud services. The partnership focuses on enhancing regulatory compliance and intelligent data capabilities across Citi’s global operations, highlighting the growing reliance of large enterprises on sophisticated cloud management platforms to modernize securely and efficiently.

The small and medium enterprises segment is projected to be the fastest-growing segment during the forecast period, driven by increasing SME adoption of cloud-first strategies and cost-optimized SaaS solutions. SMEs are embracing integrated platforms that offer policy enforcement and workload orchestration without requiring large in-house infrastructure. Additionally, the rise of modular, subscription-based ICMP tools with no-code interfaces and embedded analytics makes these platforms both accessible and scalable for small businesses. In conclusion, the above-mentioned factors are contributing notably to spurring the growth of the small and medium enterprises segment in the global integrated cloud management platform market.

End Use Insights

The BFSI segment dominated the market in 2024, driven by the stringent requirements for data security and regulatory compliance. Financial institutions operate across hybrid and multi-cloud infrastructures to ensure uninterrupted services and meet global compliance standards such as PCI DSS, GDPR, and SOX. ICMPs play a crucial role in managing risk, detecting anomalies, and ensuring business continuity in high-stakes financial operations. For instance, in December 2024, JPMorgan Chase announced the expansion of its hybrid cloud strategy in partnership with AWS, leveraging centralized cloud management tools to enhance security controls and meet regulatory expectations across global markets. This reflects the growing reliance of the BFSI sector on integrated platforms to balance innovation and compliance, thereby driving the market share.

The Retail & Consumer Goods segment is projected to be the fastest-growing segment during the forecast period due as retailers are integrating generative AI to transform customer touchpoints, necessitating scalable and intelligent cloud infrastructure. These applications demand robust Integrated Cloud Management Platforms (ICMP) to ensure seamless provisioning and compliance across hybrid and multi-cloud environments. Furthermore, managing seasonal spikes in demand and global logistics in real time relies heavily on ICMP’s capabilities. For instance, in January 2024, Walmart unveiled new generative AI-powered search and replenishment tools leveraging Microsoft’s Azure OpenAI Service to enable conversational, goal-based shopping and “InHome Replenishment”. This deep integration of AI into both customer-facing and operational workflows demonstrates the growing adoption of integrated cloud management platforms in the retail & consumer goods segment.

Regional Insights

North America integrated cloud management platform market accounted for the largest market share of 39.7% in 2024, owing to the rapid adoption of FinOps practices, growing demand for sovereign cloud compliance frameworks and a heightened focus on zero-trust architecture integration within cloud operations. Enterprises across the U.S. and Canada are increasingly prioritizing cross-cloud policy enforcement and AI-powered governance tools due to strict regulatory mandates such as HIPAA, FedRAMP, and CCPA. Additionally, the region’s mature enterprise cloud landscape is accelerating the shift toward platform-centric cloud management strategies, where centralized control, real-time visibility, and automated remediation across AWS, Azure, and GCP environments are critical to maintaining agility and security at scale. Furthermore, the rise of edge-cloud convergence, particularly in manufacturing and telecom, is also prompting demand for ICMP solutions that support distributed infrastructure orchestration and policy continuity across geographically dispersed environments.

U.S. Integrated Cloud Management Platform Market Trends

The integrated cloud management platform industry in the U.S. is expected to grow significantly as organizations are emphasizing centralized cloud governance and automation tools to manage digital estates. Also, the rise of remote and hybrid work models has led to increased deployment of ICMPs to ensure real-time visibility, policy enforcement, and secure access across distributed infrastructures. Additionally, U.S. companies are accelerating investments in AI-powered cloud management tools to streamline operations and enhance business agility, especially as they adopt edge computing and sector-specific cloud strategies.

Europe Integrated Cloud Management Platform Market Trends

The integrated cloud management platform industry in Europe is anticipated to register considerable growth from 2025 to 2033, owing to the rise of European cloud alliances like GAIA-X. Enterprises are deploying ICMPs to ensure transparent cross-border data governance, especially in industries like banking, insurance, and public services, where compliance with both local and EU-wide regulations is critical. Also, there is a shift toward cloud-neutral tools that provide interoperability across hyperscalers and local providers, driven by the EU’s push for reduced dependence on non-European cloud infrastructures. Additionally, the market is witnessing strong adoption of open-source and modular cloud management platforms, aligning with Europe’s emphasis on vendor neutrality and greater autonomy over data infrastructure.

The U.K. integrated cloud management platform industry is experiencing notable growth as the government’s classification of data centers as Critical National Infrastructure (CNI) has heightened focus on data sovereignty, compelling enterprises to adopt ICMP solutions offering control over data location and governance. Additionally, U.K. organizations are integrating AI-enhanced cloud security and Zero Trust frameworks into ICMP platforms to reinforce resilience against ransomware and other cyber threats.

The integrated cloud management platform market in Germany is driven by increasing investments by key players. These sovereign cloud investments necessitate advanced ICMP solutions to manage hybrid and multi-cloud environments effectively, ensure consistent policy enforcement, and automate compliance workflows. Moreover, the rapid growth of cloud professionals further supports adoption, as enterprises seek tailored orchestration, cost optimization, and governance capabilities across increasingly complex infrastructures. For instance, in May 2024, AWS announced it to invest €7.8 billion to launch a European Sovereign Cloud in Germany, enabling organizations to migrate critical workloads to the cloud while maintaining full control over data locality and access.

Asia Pacific Integrated Cloud Management Platform Market Trends

The integrated cloud management platform market in Asia Pacific is expected to witness the fastest growth, registering a CAGR of 15.8% from 2025 to 2033, due to the proliferation of IoT and smart city initiatives. As cities across India, China, Singapore, and South Korea deploy networks of connected devices for traffic systems, surveillance, utilities, and public services the volume of data generated across edge locations has surged, demanding real-time processing, orchestration, and monitoring. ICMP solutions enable governments and enterprises to manage these distributed, multi-cloud environments efficiently by automating workload deployment and optimizing performance across both central and edge infrastructures.

Japan integrated cloud management platform industry is experiencing substantial growth, driven by growing focus on hybrid cloud adoption, regulatory compliance, and IT modernization. Enterprises in sectors like manufacturing, finance, and public services are increasingly deploying hybrid environments to retain control over sensitive data while accessing the scalability of the public cloud. Furthermore, Japan’s emphasis on security, operational transparency, and vendor diversity is encouraging the adoption of ICMP solutions that support granular policy control, cost optimization, and seamless integration across multi-cloud and edge infrastructures.

Key Integrated Cloud Management Platform Companies Insights

Key players operating in the integrated cloud management platform market are undertaking various initiatives to strengthen their presence and increase the reach of their products and services. Strategies such as expansion activities and partnerships are key in propelling the market growth.

Key Integrated Cloud Management Platform Companies:

The following are the leading companies in the integrated cloud management platform market. These companies collectively hold the largest market share and dictate industry trends.

- BMC Software, Inc.

- Cisco Systems, Inc.

- Cognizant

- Dynatrace, Inc.

- IBM Corporation

- Lumen Technologies, Inc.

- Micro Focus International plc

- Microsoft Corporation

- Oracle Corporation

- Snow Software AB

- Splunk Inc.

- VMware, Inc.

Recent Developments:

-

In May 2025, IBM introduced webMethods Hybrid Integration5, a next-generation hybrid cloud integration solution featuring intelligent, agent-driven automation to replace rigid workflows. This solution supports seamless integration across apps, APIs, B2B partners, and hybrid cloud environments, driving significant ROI and operational efficiencies. IBM also enhanced its AI capabilities with watsonx.data for better utilization of unstructured data and integrated automation tools with HashiCorp and Red Hat technologies to accelerate AI and hybrid cloud management.

-

In February 2025, IBM completed its USD 6.4 billion acquisition of HashiCorp, integrating key automation tools like Terraform and Vault into its Red Hat, watsonx, and broader hybrid cloud portfolio. This move enhances IBM's platform by enabling automated infrastructure provisioning, robust secrets management, and unified governance across complex hybrid and multi-cloud environments.

-

In August 2024, Lumen Technologies partnered with Informatica to modernize its data management by migrating on-premises workloads to Informatica’s AI-powered Intelligent Data Management Cloud (IDMC) platform. This modernization reduced manual data reconciliation efforts by over a thousand hours and improved data reliability, enabling faster cloud expansion and better integration of network assets and security solutions.

Integrated Cloud Management Platform Market Report Scope

Report Attribute

Details

Market size in 2025

USD 7.42 billion

Revenue forecast in 2033

USD 22.10 billion

Growth rate

CAGR of 14.6% from 2025 to 2033

Actual data

2021 - 2024

Forecast period

2025 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2025 to 2033

Report coverage

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Component, deployment mode, organization size, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; Kingdom of Saudi Arabia; South Africa

Key companies profiled

Microsoft Corporation; IBM Corporation; VMware; Inc.; Dynatrace, Inc.; Micro Focus International plc; Snow Software AB; Cognizant; BMC Software, Inc.; Lumen Technologies, Inc.; Splunk Inc.; Oracle Corporation; Cisco Systems, Inc.

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Integrated Cloud Management Platform Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global integrated cloud management platform market report based on component, deployment mode, organization size, end use, and region.

-

Component Outlook (Revenue, USD Billion, 2021 - 2033)

-

Solutions

-

Services

-

Professional Services

-

Managed Services

-

-

-

Deployment Mode Outlook (Revenue, USD Billion, 2021 - 2033)

-

Public Cloud

-

Private Cloud

-

Hybrid Cloud

-

-

Organization Size Outlook (Revenue, USD Billion, 2021 - 2033)

-

Large Enterprises

-

Small and Medium Enterprises

-

-

End Use Outlook (Revenue, USD Billion, 2021 - 2033)

-

Healthcare

-

BFSI

-

Retail & Consumer Goods

-

Education

-

IT & Telecom

-

Manufacturing

-

Government & Public Sector

-

Energy & Utilities

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Frequently Asked Questions About This Report

The global integrated cloud management platform market size was valued at USD 6.61 billion in 2024 and is expected to reach USD 7.42 billion in 2025.

The global integrated cloud management platform market is expected to witness a compound annual growth rate of 14.6% from 2025 to 2033 to reach USD 22.10 billion by 2033.

Solution segment dominated the market and accounted for the largest share of 65.2% in 2024 due to the growing trend of embedding AI capabilities including autonomous, intelligent agents designed to independently manage cloud environments. These AI agents learn from system metadata, predict operational needs, and execute tasks such as data integration, workload orchestration, and policy enforcement without manual input.

Some of the companies operating in the integrated cloud management platform market include Microsoft Corporation, IBM Corporation, VMware, Inc., Dynatrace, Inc., Micro Focus International plc, Snow Software AB, Cognizant, BMC Software, Inc., Lumen Technologies, Inc., Splunk Inc., Oracle Corporation, Cisco Systems, Inc., and Others.

Enterprises need unified visibility and control across fragmented cloud environments, leading to demand for platforms that can manage workloads in public, private, and on-premises infrastructure.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.