- Home

- »

- Next Generation Technologies

- »

-

IT Professional Services Market Size Report, 2026-2033GVR Report cover

![IT Professional Services Market (2026 - 2033)Report]()

IT Professional Services Market (2026 - 2033)

Size, Share & Trends Analysis Report By Type (Project-oriented Services, ITO Services), By Deployment (On-premise, Cloud), By Enterprise Size, By End-Use, By Region, And Segment Forecasts

Market Size, 2025

$988.7BMarket Estimate, 2026

$1,075.7BMarket Forecast, 2033

$2,152.0BCAGR, 2026–2033

10.4%IT Professional Services Market Summary

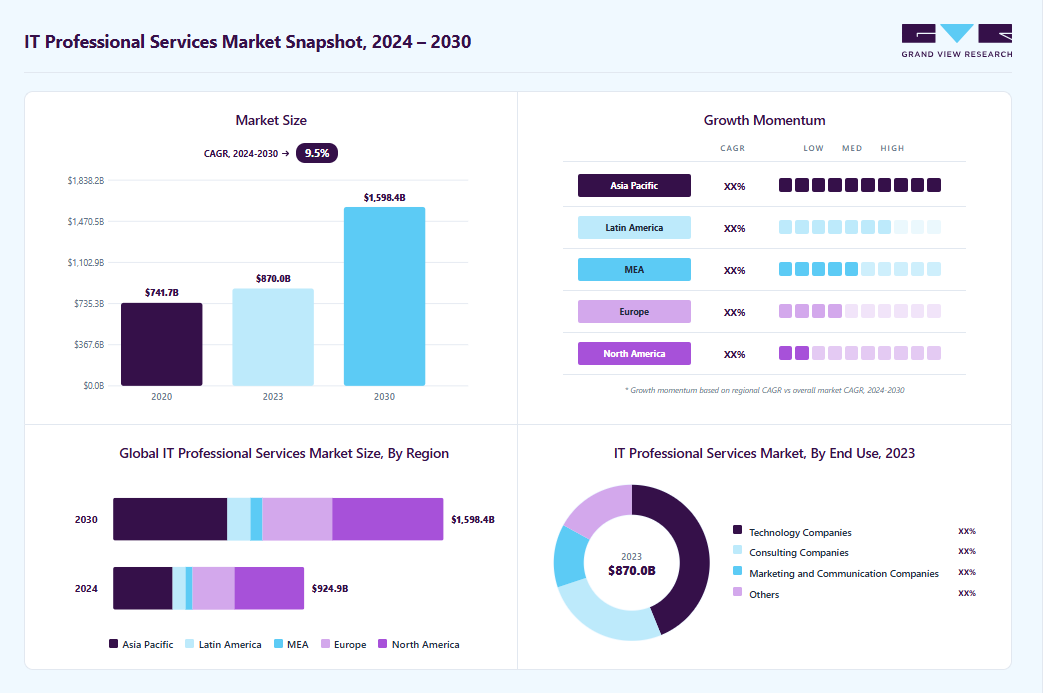

The global IT professional services market size was valued at USD 988.7 billion in 2025 and is projected to grow from USD 1,075.7 billion in 2026 to USD 2,152.0 billion by 2033, at a CAGR of 10.4% from 2026 to 2033. The North America market dominated, with a revenue share of 38.9% in 2025. This growth is driven by the rise in automation for the elimination of everyday tasks, and a shift in customer demand, such as customized pricing options and enhanced customer experience, is propelling enterprises to implement IT services globally and increasing the need for operational efficiency in the professional service firm.

Key Market Trends & Insights

- By type: Project-oriented services segment dominated the market, with a revenue share of 37.4% in 2025.

- By deployment: Cloud segment held the largest market share of 69.3% in 2025.

- By enterprise size: Large enterprises segment held the largest revenue share in 2025.

- By end use: Technology companies segment held the largest revenue share in 2025.

Regional Highlights

- Largest regional market: North America (38.9% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 988.7 Billion

- Estimated market size in 2026: USD 1,075.7 Billion

- Projected market size by 2033: USD 2,152.0 Billion

- CAGR (2026-2033): 10.4%

Furthermore, the COVID-19 pandemic tested the professional services industry by compelling them to implement remote working on a large scale and adjust their business strategies to changing market conditions. COVID-19 augmented several changes across end-use industries; firms countered the epidemic with the help of technology by focusing on talent acquisition and resource management.Professional services software’s fundamental functions are invoice & expense management, resource allocation, project management, and automated billing. The software also plays a dynamic role in instituting robust communication between internal stakeholders of the business, automating several time-consuming tasks, profit margin expansion, and supporting IT professional services market growth.

")

Professional service firms can provide a variety of services, including consultation, audit and accounting, implementation support, and financial risk protection. They provide analytic capabilities as well as a foundation for managing business information. It is difficult to compete in today's market with data silos and legacy tools, so organizations rely on IT professional services to use advanced tools. These tools facilitate resource sharing, automate delivery processes, and provide accurate insights, all of which will propel the IT professional services market forward.

Most governments focus on digitalizing their economic operations, which is anticipated to create robust market opportunities for professional services automation software. Various governments, such as Canada, India, Germany, and Saudi Arabia, are supporting regional market players to accelerate economic growth. For instance, in March 2022, the Government of Canada’s has established Canada Digital Adoption Program (CDAP) with an investment of USD 4 billion to assist small and medium-sized enterprises (SMEs) in adopting digital technologies. Under this program, the SMEs will receive USD 2,400 microgrant to cover the costs related to their ecommerce business such as social media advertising, website development, and other automated web actions.

The increased competition and digitalization are pushing enterprises to engage with professional service providers. IT professional service providers provide a streamlined and standardized approach to the administrative processes of the organization, assisting in the digital transformation of the organization's operations. For instance, in February 2022, Amazon Web Services, Inc. announced infrastructure deployment global expansion and AWS local zones in 16 cities across the U.S. with around 30 new local zones. These deployments will assist AWS in expanding its computing storage, database, and other services to a large population from multiple industries. These developments would further drive the growth of the IT professional services market during the forecast period.

Market Dynamics

The IT professional services market is undergoing a structural transformation driven by the rapid adoption of AI-native enterprise ecosystems, cloud modernization, and managed services-led delivery models. Enterprises are increasingly shifting from traditional project-based IT engagements to continuous, outcome-driven service models powered by generative AI, automation, and platform engineering. This is accelerating demand for consulting and implementation services around AI governance, FinOps, sovereign cloud strategies, cybersecurity compliance, and cloud-native architecture redesign. At the same time, the rise of AI-enabled managed services and agentic automation is redefining service delivery, enabling providers to scale operations, improve efficiency, and support complex hybrid and multi-cloud environments.

Additionally, market dynamics are being shaped by intensifying competition, shrinking deal sizes, and monetization challenges as AI-driven productivity compresses traditional time-and-materials billing structures. However, strong enterprise spending continues in high-value segments such as cloud migration, cybersecurity, data engineering, and regulatory compliance, supported by increasing regulatory pressure and digital sovereignty requirements. The growing shift toward AI-first managed service platforms and ecosystem-based partnerships is also creating new revenue pools, particularly in MSP-led transformation initiatives and integrated digital operations services.

The IT professional services market is being significantly driven by the rapid integration of AI-native development tools, automation platforms, and generative AI coding assistants across enterprise engineering teams. As organizations increasingly adopt tools such as code-generation models, agentic workflows, and AI-assisted software delivery environments, the demand for professional services to implement, manage, and optimize these ecosystems is rising. A key enabler of this shift is the growing emphasis on cost intelligence and FinOps capabilities. For instance, the launch of cost intelligence solutions such as Opik’s visibility layer for AI coding spend reflects a broader industry need for enterprises to monitor and govern usage of models like Claude Code and Codex, ensuring that AI-driven development remains both efficient and financially controlled.

In parallel, IT service providers are benefiting from the expansion of AI-enabled enterprise modernization initiatives, where organizations require expert consulting for integrating AI into DevOps pipelines, cloud infrastructure, and software engineering lifecycles. This is accelerating demand for specialized IT professional services in areas such as AI governance, cloud cost optimization, and enterprise architecture redesign. As enterprises scale AI adoption beyond experimentation into production-grade systems, professional service providers play a critical role in ensuring scalability, compliance, and measurable ROI from AI investments.

A key restraint for the IT professional services market is the increasing complexity of service delivery environments combined with persistent shortages of skilled talent in high-demand areas such as AI engineering, cloud-native architecture, cybersecurity, and data engineering. As client environments become more fragmented across multi-cloud, hybrid infrastructure, and AI-integrated stacks, service providers face growing challenges in maintaining consistent delivery quality while controlling costs. This is further intensified by rapidly evolving technology stacks, which require continuous upskilling and increase dependency on niche expertise.

At the same time, automation and AI-driven tools are exerting downward pressure on traditional billable-hour models, leading to pricing commoditization across standard IT services. Clients are increasingly expecting productivity gains from AI tools to translate into lower service costs, which compresses margins for providers. Additionally, intense competition from global IT vendors, boutique consultancies, and emerging AI-first service firms is making differentiation more difficult, particularly in standardized service offerings such as application maintenance, infrastructure management, and basic cloud migration services.

The IT professional services market is witnessing a strong opportunity in the emergence of AI-first managed service platforms and next-generation MSP (Managed Service Provider) ecosystems that combine automation, analytics, and cloud-native delivery models. Recent funding activity in AI-enabled MSP platforms, such as seed investments in companies building intelligent service orchestration and automation layers, highlights growing investor confidence in scalable, software-driven IT service delivery models. These platforms are redefining traditional IT services by embedding AI into monitoring, incident resolution, workload optimization, and customer lifecycle management.

Furthermore, enterprises are increasingly outsourcing complex IT operations to intelligent service providers that can deliver end-to-end visibility, predictive maintenance, and autonomous infrastructure management. This shift is creating new growth avenues for IT professional services firms to evolve into platform-based providers rather than purely manpower-driven consultancies. As organizations prioritize agility, scalability, and cost efficiency, demand for AI-enabled MSP solutions, cloud-native managed services, and outcome-based service models is expected to accelerate, opening significant long-term growth potential across both enterprise and mid-market segments.

Market Concentration & Characteristics

The IT professional services market growth is high, and the pace is accelerating. The rise in the number of cyber breaches across enterprises can be considered as one of the major reasons helping in the IT professional services market. Similarly, the increased adoption of cloud-based services over recent years resulted in an increase in identity theft, and cyber breaches among others. Companies are adopting IT services to analyze the execution of applications and network connections.

The market can be significantly impacted by the regulations implied for ensuring data security, influencing service delivery models and shaping industry standards. Companies have to comply with General Data Protection Regulation (GDPR), NIST Cybersecurity Framework, industry specific regulations among others. Stringent compliance requirements often force companies to opt for IT professional services for regulatory adherence.

The players are actively focusing on new product development to enhance and extend their current products and services, consequently organizations have a potential chance to secure new clients and approve the new technological changes. For instance, In June 2022, HP launched innovations for the HPE GreenLake their edge cloud platform to provide data center operators with cloud services at nominal costs. With these innovations, HPE GreenLake cloud will support applications such as AI, financial services, high-performance computing (HPC) and risk & data analytics in telecom infrastructure. This will help the company attract new clients.

Analyst Perspective

The IT professional services market is entering a structurally redefined growth phase, shifting away from traditional labor-intensive outsourcing toward AI-enabled, platform-driven, and outcome-based service models. From an analyst perspective, the market is increasingly being shaped by enterprise demand for accelerated digital transformation, cloud modernization, and AI integration across core business functions, particularly as organizations move from experimentation to large-scale deployment of generative AI and automation workflows. This transition is expanding the scope of professional services beyond implementation into continuous optimization, governance, and FinOps-led cost management. At the same time, competitive dynamics are intensifying as global IT majors consolidate end-to-end capabilities while emerging MSP and AI-native players introduce agile, software-led service delivery models that challenge legacy pricing structures. However, margin pressures, talent shortages in advanced digital skill sets, and rapid commoditization of standardized services are creating headwinds for traditional players. Overall, the market outlook remains strongly positive, underpinned by sustained enterprise IT spending, rising complexity of hybrid and multi-cloud environments, and growing reliance on external expertise to operationalize AI-first digital ecosystems at scale.

Type Insights

Based on type, the project-oriented services segment led the market with the largest revenue share of 37.4% in 2025. Project-oriented services include timely maintenance, modernization, project installation, and decommissioning. These services are frequently tailored to meet the specific needs of the client, assisting them to maximize operational efficiency and deliver projects on time and within budget. Organizations can benefit from project-oriented services in a variety of ways, such as scope management, revenue management, preparing improved quotations, resource management, and effective project delivery. These are the primary factors driving segment demand.

Information Technology Outsourcing (ITO) service segment is anticipated to witness a significant CAGR of 10.3% during the forecast period owing to its ability to help organizations across various industries respond to changing business needs, allowing organizations to focus on innovation instead of IT infrastructure. Organizations utilize ITO services to gain access to deep technical expertise, deliver automation, and bring down costs by choosing an appropriate delivery model. Additionally, ITO services offer a deep pool of resources to create effective Return on Investment (ROI), and it bridges the gap between legacy IT systems and innovation. These benefits provided by ITO services are expected to boost the growth of the segment.

Deployment Insights

Based on deployment, the cloud segment led the market with the largest revenue share of 69.3% in 2025. Cloud computing is gaining traction owing to various benefits offered such as increased accessibility, reduction in technology infrastructure costs and reduced overall implementation costs. Furthermore, the improving infrastructure for internet services is augmenting the adoption of cloud-based services. Rise in competition across various end-use industries is forcing companies to cut down on expenditure, hence creating a need for affordable services. These capabilities and features would further supplement the growth of the segment during the forecast period.

The on-premise segment is expected to witness a considerable growth of a CAGR of 8.2% over the forecast period. On-premise solutions offer increased privacy, robust data security and are less vulnerable to digital threats, driving the segment growth. Furthermore, these solutions can perform their work and provide safe access to the data even if the internet connection is interrupted due to its local data storage system.

Enterprise-size Insights

Based on enterprise size, the large enterprises segment led the market with the largest revenue share of 63.2% in 2025. Due to improved customer experience, low operating costs, improved team collaboration, and low workforce costs, these organizations are major users of IT professional service solutions. These enterprises sign long-term agreements with IT professional services software providers in order to reduce software costs and enable their employees to become familiar with-IT professional service types quickly. For instance, in March 2022, Nividous Software Solutions announced that they had collaborated with Damco Types for streamlining non-core and core business processes across various industries using intelligent automation processes.

The Small & Medium Enterprise (SMEs) segment is expected to witness a significant growth of a CAGR of 11.6% over the forecast period. The SMEs sector is an untapped market and has become an area of focus for industry players. According to the World Bank, the SMB sector accounts for 95% of the existing business. The availability of cloud-based IT professional services tools at affordable prices is anticipated to drive their demand in the SMEs sector. On average, a small enterprise spends over 6% of its revenue on IT, whereas a mid-sized firm spends over 4% and a large enterprise spends around 3%. As the number of SMEs is increasing, competition is also increasing, which has resulted in a price drop of the solution and profit erosion.

End-Use Insights

Based on end use, the technology companies segment led the market with the largest revenue share of 43.0% in 2025. Technology companies rely on the intelligent use of data analytics that can be attained with the help of IT professional services. Moreover, technology continues to evolve; thus, several technology companies, particularly those focusing on the development of Technology as a Service (TaaS), opt for IT professional services as part of their efforts to support their business operations. Additionally, the COVID-19 pandemic also triggered the need for digital transformation, with many technological shifts in work culture, such as working remotely and maintaining the organization’s IT infrastructure; all of these factors are contributing to the growth of this segment.

The marketing and communication companies’ segment is anticipated to grow at a CAGR of 10.9% over the forecast period. These companies depend on extensive market research, website analysis, budget allocation, and reputation management which can be executed with the help of IT professional services. Additionally, the rise of digital media and enhanced customer experience will push the segment to grow further.

Regional Insights

North America dominated the global IT professional services market with the largest revenue share of 38.9% in 2025, owing to the high adoption of cloud services and Enterprise Resource Planning (ERP) for data management. Furthermore, the integration of advanced technologies such as ITO Services (AI) & Machine Learning (ML) and new type of introduction by market players are creating positive traction for IT professional services in the region. Moreover, the majority of foreign-owned U.S. affiliate firms in the U.S. are investing heavily in IT professional services research and development, which will support the growth of IT professional services in this region during the forecast period.

U.S. IT Professional Services Market Trends

The IT professional services market in the U.S. held the largest share in the North America region in 2025. The country is one of the largest economies in the world, creating lucrative opportunities for IT services like outsourcing, data processing, etc. Similarly, the increasing adoption of cloud-based services will help in market growth.

Europe IT Professional Services Market Trends

The Europe IT professional services market will witness a high growth rate during the forecast period. The region has a strong emphasis on the implementation of data security and privacy due to the strict GDPR regulations helping drive the demand for various compliance and IT services.

The IT professional services market in the UK will experience lucrative growth opportunities during the forecast period. Companies across the UK are investing heavily in implementing digital transformation initiatives to enhance efficiency and drive innovation across various end-use sectors.

Germany IT professional services market is expected to grow at a CAGR of 8.2% during the forecast timeline. The proliferation of Industry 4.0 and the rising adoption of cloud-based services to improve overall flexibility, cost-efficiency, and scalability will help in market growth. These services provide assistance in cloud management, migration and optimization.

The IT professional services market in France will witness a high growth rate during the forecast period. The proliferation of Industry 4.0 has increased the adoption of various technologies such as AI, ML, IoT, automation for enhancing manufacturing processes. The adoption of such technologies will help in the IT professional services market growth.

Asia Pacific IT Professional Services Market Trends

The Asia Pacific IT professional services market is anticipated to witness a fastest growth of a CAGR of 11.5% over the forecast period. The demand for knowledge-based services is expected to rise exponentially in the legal & advisory, and accounting service industries of this region which will boost the growth over the forecast period. Besides, growing economies such as China and India are focusing on IT development which will unfold numerous opportunities for IT professional services in the region. Additionally, the Asia Pacific region comprises numerous SMEs that largely rely on professional services for the smooth execution of daily operations.

The IT professional services market in China will grow at a CAGR of 11.6% during the forecast period. Various government initiatives such as “Made in China 2025” and “Internet Plus” to promote digital transformation and technological innovation across various end-use industries is driving the market for IT professional services.

India IT professional services market is expected to hold a market share of 13.9% in the Asia Pacific region. The increasing adoption of technologies such as big data analytics, cloud computing, artificial intelligence, and Internet of Things (IoT) is on the rise among companies in India helping the market growth.

The IT professional services market in Japan will hold a market share of 8.9% in the Asia Pacific region. The country has been an early adopter of advanced technologies across end-use industries helping provide lucrative growth opportunities in the forecast period. Furthermore, the integration of automation, cloud-based services, and AI in operations and supply chain activities will help market growth.

MEA IT Professional Services Market Trends

The Middle East & Africa (MEA) IT professional services market will grow at a CAGR of 9.5% during the forecast period. Initiatives undertaken by governments and corporations to promote advanced technologies, such as machine learning, business analytics, and Al, coupled with continuous adoption of cloud-based technologies, are anticipated to fuel the demand for IT Professional Services across business processes in Middle East countries.

The IT professional services market in Saudi Arabia will witness a high growth rate during the forecast period. Various initiatives such as the “Vision 2030” launched by the government to promote digital transformation across various sectors and reduce the dependency on oil will drive the need for IT Professional Services across various sectors in the region.

Key IT Professional Services Company Insights

The key industry participants include Accenture; Datto, Inc.; Capgemini; Microsoft Corporation, and International Business Machines Corporation.

-

Accenture plc has a diverse portfolio of IT professional services and helps their clients define their IT strategies, align technology investments with business objectives. They have expertise in IT service management, enterprise architecture helping them stand out from its competitors.

-

Microsoft Corporation has a comprehensive portfolio of products and services designed to work seamlessly, facilitating integration and interoperability across IT landscape. This integration capability simplifies deployment, maintenance and management for organizations.

Atera Networks Ltd., Datto, Inc., HELIXSTORM, Veritis Group Inc, etc. are the emerging players operating in the IT professional services market.

-

Atera Networks Ltd. Offers an all-in-one platform that combines professional services automation (PSA), remote monitoring and management (RMM) and remote access into a single solution. This integrated platform streamlines IT management processes and improves operational efficiency.

-

Datto, Inc. focuses on providing innovative and comprehensive solutions specifically designed for service providers and medium-sized businesses. It offers backup and disaster recovery solutions providing robust data protection and business continuity capabilities.

Key IT Professional Services Market Companies:

The following key companies have been profiled for this study on the IT professional services market.

-

Accenture

-

Amazon Web Services

-

Atera Networks Ltd.

-

Capgemini

-

Datto, Inc.

-

DXC Technology Company

-

FUJITSU

-

HELIXSTORM

-

Hewlett Packard Enterprise Development LP

-

International Business Machines Corporation

-

Microsoft Corporation

-

Oracle Corporation

-

ScienceSoft USA Corporation

-

Veritis Group Inc.

-

VMware, Inc.

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Mature Players (Accenture; Amazon Web Services; Capgemini; IBM (International Business Machines Corporation); DXC Technology; Fujitsu; Hewlett Packard Enterprise (HPE); Microsoft; Oracle; VMware)

- Focus on large-scale enterprise digital transformation programs combining consulting, cloud migration, AI integration, and managed services under long-term contracts.

- Strong emphasis on ecosystem-led delivery models, leveraging proprietary platforms (cloud, AI, ERP, and automation tools) to lock in enterprise clients and expand recurring revenue streams.

- Deep global enterprise client base with multi-decade relationships and strong brand trust in mission-critical IT infrastructure and transformation programs.

- Comprehensive service portfolios spanning consulting, infrastructure, cloud, cybersecurity, and enterprise software, enabling end-to-end solution delivery.

- High cost structure limits competitiveness in price-sensitive SME and mid-market segments.

- Slower decision-making and legacy organizational structures reduce agility in rapidly evolving AI-native and niche service areas.

Emerging Players (Atera Networks Ltd.; Datto, Inc.; HELIXSTORM; ScienceSoft USA Corporation; Veritis Group Inc.)

- Focus on niche IT services such as managed IT platforms, SMB-centric outsourcing, cybersecurity services, and cloud-first delivery models with high automation.

- Heavy reliance on SaaS-based, subscription, and platform-driven models that reduce dependency on traditional manpower-based consulting.

- High agility and faster innovation cycles, enabling quick adoption of AI-driven automation, MSP platforms, and cloud-native service delivery.

- Strong positioning in SME and mid-market segments through cost-effective, scalable, and standardized service offerings.

- Limited global scale and weaker presence in large enterprise transformation deals compared to Tier-1 IT service providers.

- Dependency on narrow service portfolios or regional markets, limiting diversification and resilience against market fluctuations.

Recent Developments

-

In February 2024, Skyhigh Security announced the addition of managed & professional IT services to its Altitude Partner Program. With these professional services offered, companies can complete their product development and resell SkyHigh Security solutions.

-

In August 2023, Rackspace Technology announced a professional services collaboration with Google Cloud to help accelerate VM migrations. This collaboration will migrate virtual machines to Google Cloud, helping provide an efficient and innovative solutions to businesses.

-

In August 2023, HCLTech signed an agreement with TIBCO Solutions: a cloud software group. Under this agreement, HCLTech will help implement, modernize, upgrade and provide services for TIBCO products globally, helping strengthen HCL’s professional services portfolio.

IT Professional Services Market Report Scope

Report Attribute

Details

Market size in 2025

USD 988.7 billion

Estimated market size in 2026

USD 1,075.7 billion

Projected market size by 2033

USD 2,152.0 billion

Growth rate

CAGR of 10.4% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecasts period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecasts, company market share analysis, competitive landscape, growth factors, and trends

Segments covered

Type, deployment, enterprise size, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; China; Japan; India; South Korea; Australia; Brazil; Saudi Arabia; South Africa; UAE

Key companies profiled

Accenture; Amazon Web Services; Atera Networks Ltd.; Datto, Inc.; Capgemini; International Business Machines Corporation; DXC Technology Company; FUJITSU; HELIXSTORM; Hewlett Packard Enterprise Development LP; Microsoft; Oracle; ScienceSoft USA Corporation; Veritis Group Inc.; VMware, Inc.

Customization scope

Free report customization (equivalent to up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global IT Professional Services Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global IT professional services market based on type, deployment, enterprise size, end-use, and region:

-

Type Outlook (Revenue, USD Billion, 2021 - 2033)

-

Project-oriented Services

-

ITO Services

-

IT Support & Training Services

-

Enterprise Cloud Computing Services

-

-

Deployment Outlook (Revenue, USD Billion, 2021 - 2033)

-

On-premise

-

Cloud

-

-

Enterprise-size Outlook (Revenue, USD Billion, 2021 - 2033)

-

Small & Medium-sized Enterprises (SMEs)

-

Large Enterprises

-

-

End-Use Outlook (Revenue, USD Billion, 2021 - 2033)

-

Technology Companies

-

Consulting Companies

-

Marketing & Communication Companies

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

Australia

-

South Korea

-

-

Latin America

-

Brazil

-

Mexico

-

-

MEA

-

UAE

-

South Africa

-

Saudi Arabia

-

-

Research Methodology

The IT professional services market figures in this report are based on a proven research process that combines executive interviews with secondary research from proprietary databases, company filings, and recognized regulatory and institutional sources. Market size is built through value-chain sizing - reconciling supply-side and demand-side estimates - and triangulated with bottom-up and top-down approaches. Every estimate passes multiple levels of expert validation before publication, with each IT professional services segment quantified using the revenue-capture definitions in the table below.

Segment Definition

Segment - Type

Revenue Capture Definition

Project-oriented Services

Revenue is generated through short- to medium-term IT consulting and implementation projects such as system integration, application development, digital transformation, cloud migration, and enterprise modernization. These services are typically contract-based, with revenue driven by project scope, complexity, timelines, and resource allocation. Higher-value engagements such as AI integration, cloud-native transformation, and cybersecurity implementation command premium billing rates.

ITO Services (IT Outsourcing Services)

Revenue is earned through long-term outsourcing contracts where IT operations such as infrastructure management, application maintenance, helpdesk support, and network management are delivered regularly. Revenue is typically structured as annuity-based contracts (managed services agreements), often involving SLA-driven pricing models, ensuring predictable and stable cash flows for service providers.

IT Support and Training Services

Revenue is generated through technical support services, end-user assistance, system troubleshooting, and professional training programs. This includes onboarding support for enterprise software, upskilling programs for digital tools, and ongoing IT helpdesk services.

Enterprise Cloud Computing Services

Revenue is captured through consulting, migration, optimization, and managed services for public, private, and hybrid cloud environments. This includes cloud architecture design, workload migration, cloud cost optimization (FinOps), and ongoing cloud operations management.

Segment - Deployment

Revenue Capture Definition

On-premise

Revenue is generated from IT professional services supporting traditional in-house IT infrastructure, server management, legacy system maintenance, security upgrades, and integration of enterprise applications.

Cloud

Revenue is earned through cloud-native and cloud-enabled IT services, including migration, application modernization, SaaS integration, DevOps implementation, and managed cloud operations.

Segment - Enterprise Size

Revenue Capture Definition

Large Enterprises

Revenue is captured through complex, multi-year enterprise contracts involving digital transformation, global IT outsourcing, cloud migration at scale, cybersecurity architecture, data engineering, and AI integration services.

Small & Medium Enterprises (SMEs)

Revenue is generated through standardized, scalable, and cost-effective IT services tailored to SMEs, including cloud onboarding, cybersecurity setup, managed IT support, and subscription-based SaaS implementation.

Segment - End Use

Revenue Capture Definition

Technology Companies

Revenue is earned by providing advanced IT engineering services, cloud infrastructure support, platform development, DevOps automation, and AI/ML integration to software firms, SaaS providers, and digital-native companies. Demand is driven by rapid innovation cycles and scalable product engineering needs.

Consulting Companies

Revenue is generated through partnerships and subcontracting arrangements where IT professional service firms support strategy execution, system implementation, digital transformation, and enterprise technology advisory services.

Marketing and Communication Companies

Revenue is captured through IT services supporting digital marketing platforms, customer experience (CX) systems, CRM implementation, data analytics, mar tech integration, and automation tools.

Others

Revenue is generated from sectors such as healthcare, BFSI, retail, manufacturing, government, and education, where IT professional services support core operations, regulatory compliance, data management, and digital transformation initiatives.

Estimation Model

Layer

Question

Analysis

Digital Transformation & Enterprise Base Layer (Total Addressable Market)

Who can potentially use IT professional services?

Estimate the total addressable base of organizations and digital users that can potentially consume IT professional services. This includes global enterprises, SMEs, government bodies, and technology startups across all industries that rely on IT infrastructure, software systems, and digital platforms. The layer also accounts for workforce digitization trends, increasing enterprise software dependency, and growing cloud adoption. In addition, virtually all digitally active organizations are included due to the rising need for cybersecurity, data management, cloud migration, and AI integration services.

Technology Readiness & Infrastructure Layer (Serviceable Market)

Who can technically adopt IT professional services?

Refine the addressable base by evaluating organizations with sufficient digital maturity, cloud readiness, and IT infrastructure compatibility. This includes enterprises using cloud platforms (AWS, Azure, Google Cloud), hybrid IT environments, and AI-enabled tools, as well as organizations with established cybersecurity frameworks and digital workflows. Market accessibility is further shaped by regulatory readiness, data governance standards, and availability of skilled IT ecosystems across regions. Only digitally enabled and transformation-ready enterprises are considered in this layer.

Adoption & Engagement Layer (Active Services Market)

Who actively uses IT professional services?

Convert the serviceable base into active consumers of IT professional services based on real-world adoption of digital transformation initiatives, cloud migration projects, AI integration programs, managed services contracts, and cybersecurity engagements. Demand is driven by enterprise priorities such as automation, cost optimization (FinOps), remote/hybrid work enablement, and modernization of legacy systems. Recurring engagement through managed IT services, multi-year outsourcing contracts, and continuous DevOps support further defines active usage intensity.

Monetization Layer (Revenue Realization Model)

How much revenue is generated?

Estimate revenue generation through multiple IT professional services streams, including project-based consulting (digital transformation, system integration, cloud migration), recurring managed services (ITO, cloud operations, application maintenance), and high-value emerging services such as AI implementation, data engineering, and cybersecurity architecture. Additional monetization comes from subscription-based managed service platforms, outcome-based pricing models, and value-added services such as training, FinOps optimization, and enterprise AI governance. Revenue realization is increasingly shifting toward hybrid models combining fixed contracts with usage-based and performance-linked pricing structures.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Enterprise AI, Cloud & Digital Transformation Adoption Trends

Conducted a detailed assessment of enterprise adoption trends across cloud migration, generative AI, cybersecurity, application modernization, managed services, data analytics, and IT outsourcing, including deployment priorities, investment patterns, and technology maturity levels.

Helps stakeholders identify high-growth service areas, understand enterprise technology spending priorities, and align service offerings with evolving digital transformation requirements.

Industry-Specific IT Services Demand Assessment

Analyzed IT professional services adoption and spending patterns across key end-use industries including BFSI, healthcare, manufacturing, retail, government, telecommunications, and technology sectors, highlighting key use cases, outsourcing trends, and digital transformation initiatives.

Supports targeted market entry and sales strategies by identifying the most attractive industry verticals, high-value service opportunities, and sector-specific technology requirements.

Regional Opportunity Analysis (Southeast Asia)

Delivered a dedicated Southeast Asia assessment covering country-level IT spending trends, cloud adoption, AI implementation initiatives, digital infrastructure investments, regulatory developments, outsourcing demand, and competitive dynamics across major regional markets.

Enables informed expansion and investment decisions by identifying high-growth countries, emerging technology adoption hotspots, market entry barriers, and long-term revenue opportunities within Southeast Asia.

Frequently Asked Questions About This Report

The global IT professional services market size was estimated at USD 988.7 billion in 2025 and is expected to reach USD 1,075.7 billion in 2026.

The global IT professional services market is expected to grow at a compound annual growth rate of 10.4% from 2026 to 2033 to reach USD 2,152.0 billion by 2033.

Key players include Accenture; Amazon Web Services; Atera Networks Ltd.; Datto, Inc.; Capgemini; International Business Machines Corporation; DXC Technology Company; FUJITSU; HELIXSTORM; Hewlett Packard Enterprise Development LP; Microsoft; Oracle; ScienceSoft USA Corporation; Veritis Group Inc.; VMware, Inc.

The project-oriented services segment led with a 37.4% revenue share in 2025, while ITO services segment is the fastest-growing segment.

The rise in automation for the elimination of everyday tasks and shift in customer demand, such as customized pricing options and enhanced customer experience, are propelling enterprises to implement IT services globally and increasing the need for operational efficiency in the professional service firm.

North America dominated with 38.9% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

The large enterprises segment held the largest share (over 63.2%) in 2025, while small & medium enterprises segment is the fastest-growing segment.

The cloud segment held the largest share over 69.3% in 2025 and on-premise segment is the fastest-growing segment.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.