- Home

- »

- Network Security

- »

-

IT And Telecom Cyber Security Market Report, 2026-2033GVR Report cover

![IT And Telecom Cyber Security Market (2026 - 2033)Report]()

IT And Telecom Cyber Security Market (2026 - 2033)

Size, Share & Trends Analysis Report By Component (Hardware, Software, Services), By Deployment (On-premise, Cloud), By Enterprise Size, By Security Type, By Technology, By Region, And Segment Forecasts

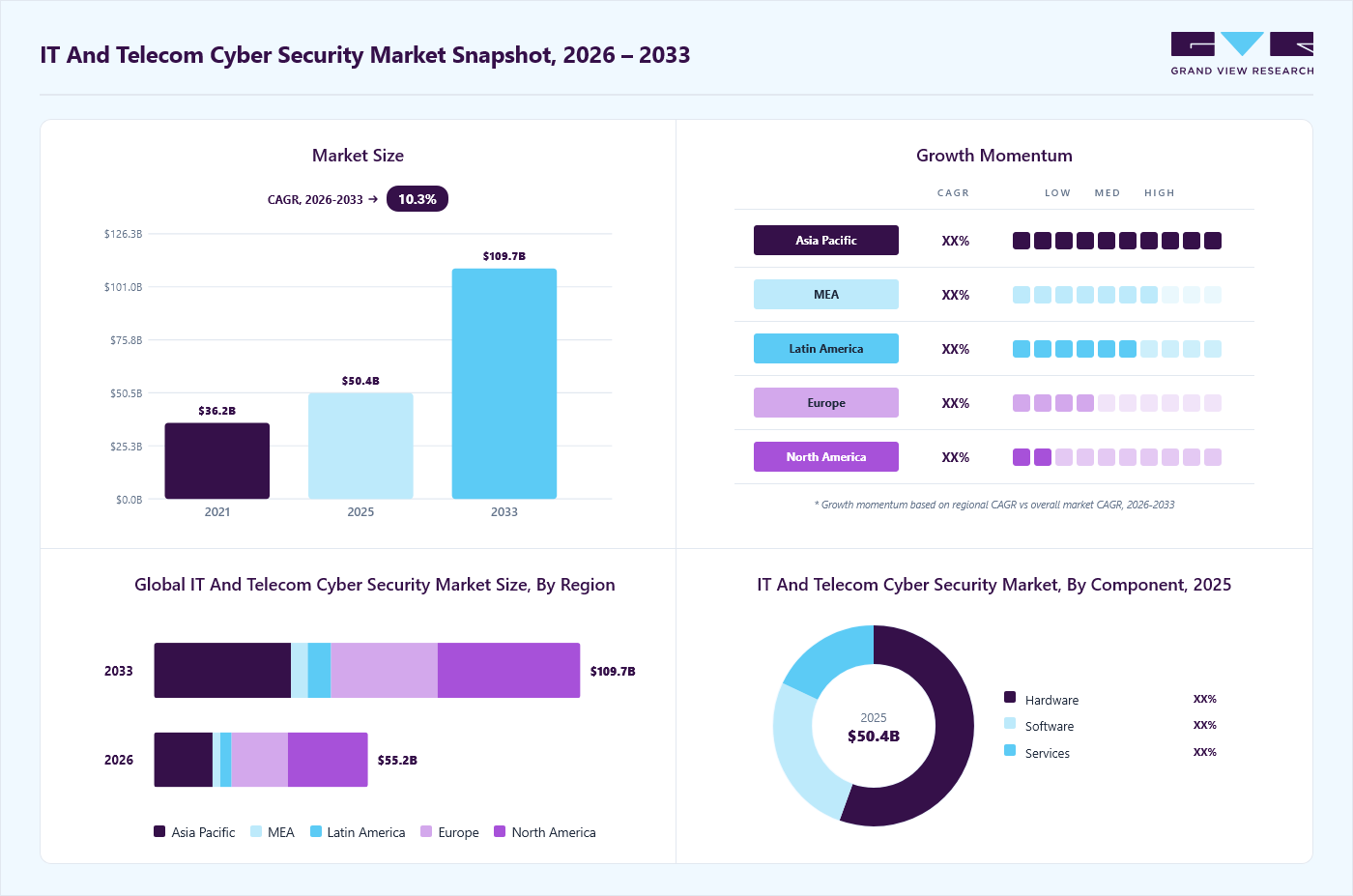

Market Size, 2025

$50.4BMarket Estimate, 2026

$55.2BMarket Forecast, 2033

$109.7BCAGR, 2026–2033

10.3%IT And Telecom Cyber Security Market Summary

The global IT and telecom cyber security market size was valued at USD 50.4 billion in 2025 and is projected to grow from USD 55.2 billion in 2026 to USD 109.7 billion by 2033, at a CAGR of 10.3% from 2026 to 2033. The North America market dominated, with a revenue share of 37.9% in 2025. This growth is driven by the surge in ransomware, DDoS attacks, phishing, and insider threats; businesses are prioritizing robust cybersecurity solutions to safeguard their operations and customer data.

Key Market Trends & Insights

- By Component: The hardware segment dominated the market, with a revenue share of 55.5% in 2025

- By Security Type: The network security segment held the largest market share of 27.6% in 2025

- By Technology: The Security Information and Event Management (SIEM) segment held the largest revenue share in 2025

- By Deployment: The cloud segment held the largest revenue share in 2025

- By Enterprise Size: The large enterprises segment held the largest revenue share in 2025

Regional Highlights

- Largest regional market: North America (37.9% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 50.4 Billion

- Estimated market size in 2026: USD 55.2 Billion

- Projected market size by 2033: USD 109.7 Billion

- CAGR (2026-2033): 10.3%

The IT and tele communications sectors are increasingly vulnerable to cyber-attacks due to the vast amounts of sensitive data and the interconnectedness of systems. With the surge in ransomware, DDoS attacks, phishing, and insider threats, businesses are prioritizing robust cybersecurity solutions to safeguard their operations and customer data. This rising threat landscape fuels demand for cybersecurity technologies and services. The rapid shift to cloud-based services within IT and telecom industries has created new security challenges. As organizations migrate their data, applications, and infrastructure to the cloud, they expose themselves to potential breaches and unauthorized access. This has led to the increased adoption of cloud-specific security tools, such as cloud access security brokers (CASBs), encryption technologies, and identity and access management (IAM) systems, to ensure that cloud environments remain secure.")

Hybrid and multi-cloud deployments have become more popular, requiring tailored security solutions that can protect data across multiple platforms. As more companies embrace cloud technologies to scale their operations and reduce costs, the demand for robust cloud security will continue to rise. This trend is further fueled by the need for organizations to comply with industry regulations regarding data protection and security in the cloud, which accelerates the market growth for cybersecurity solutions in the cloud domain.

The global deployment of 5G networks represents a major milestone for the telecommunications industry but also introduces new cybersecurity risks. 5G technology promises faster connectivity and lower latency, but its decentralized architecture and increased number of connected devices make it more susceptible to attacks. This has heightened the need for security solutions that can manage and mitigate these vulnerabilities, such as secure network slicing, advanced threat detection, and zero-trust architecture for 5G networks. As reported by 5G Americas, a trade association of wireless cellular network operators, global 5G connections reached nearly 2 billion in the first quarter of 2024, with 185 billion new connections added. It is expected to rise to 7.7 billion by 2028. In North America, 5G adoption accounts for 32% of all wireless cellular connections, double the global average. The region saw an 11% growth, adding 22 billion new 5G connections during this period.

Market Dynamics

The IT and telecom cyber security market is experiencing growth as organizations accelerate digital transformation initiatives, expand cloud deployments, and increasingly rely on interconnected networks to support business operations. The proliferation of 5G infrastructure, edge computing, IoT devices, and hybrid work environments has significantly expanded the cyberattack surface, compelling enterprises and telecom operators to strengthen their security postures. At the same time, the growing sophistication of ransomware, phishing, supply chain attacks, and AI-enabled cyber threats is driving demand for advanced security solutions such as Zero Trust architectures, Secure Access Service Edge (SASE), Security Information and Event Management (SIEM), and cloud-native security platforms. As regulatory requirements surrounding data privacy and critical infrastructure protection continue to evolve, organizations are increasing investments in proactive cybersecurity strategies and managed security services.

Furthermore, the convergence of artificial intelligence, automation, and cybersecurity is reshaping how threats are detected, analyzed, and mitigated. Enterprises are increasingly adopting AI-powered security operations, threat intelligence platforms, and automated incident response solutions to address the growing shortage of cybersecurity professionals and improve operational efficiency. Telecom operators are also strengthening network security frameworks to protect next-generation communication infrastructure and support secure digital services. These trends are expected to sustain long-term demand for cybersecurity solutions and professional services across the IT and telecom ecosystem.

The IT and Telecom Cyber Security Market is primarily driven by the increasing frequency, sophistication, and financial impact of cyberattacks targeting enterprises, telecom networks, cloud environments, and critical infrastructure. Organizations are facing growing risks from ransomware attacks, advanced persistent threats (APTs), supply chain compromises, and identity-based attacks, which can disrupt operations and expose sensitive data. As digital transformation initiatives continue to expand, enterprises are prioritizing investments in cybersecurity technologies to safeguard digital assets, ensure business continuity, and maintain customer trust.

Additionally, the rapid deployment of cloud services, 5G networks, IoT ecosystems, and remote work environments has significantly increased network complexity and security requirements. Telecom operators and enterprises are implementing Zero Trust Network Access (ZTNA), SASE, SIEM, and advanced threat detection solutions to secure distributed environments and protect critical communications infrastructure. The increasing regulatory focus on cybersecurity resilience and data protection further reinforces demand for comprehensive security solutions and services.

One of the major restraints affecting the IT and Telecom Cyber Security Market is the persistent shortage of skilled cybersecurity professionals capable of managing increasingly complex security environments. Organizations often struggle to recruit and retain qualified personnel with expertise in threat hunting, cloud security, incident response, identity management, and security architecture. This talent gap can delay security implementations, increase operational risks, and limit the effectiveness of cybersecurity investments.

In addition, the growing number of security tools and fragmented technology environments creates operational complexity for enterprises and telecom operators. Managing multiple security platforms across on-premise, cloud, edge, and hybrid environments can lead to integration challenges, visibility gaps, and increased operational costs. Small and medium-sized organizations are particularly affected, as limited budgets and resources can restrict their ability to deploy and manage advanced cybersecurity solutions effectively.

The increasing adoption of AI-powered cybersecurity solutions presents a significant growth opportunity for the IT and Telecom Cyber Security Market. Organizations are leveraging artificial intelligence and machine learning to enhance threat detection, automate security operations, identify anomalies, and accelerate incident response. AI-driven security platforms enable enterprises to improve cyber resilience while reducing reliance on scarce cybersecurity talent, making them increasingly attractive across industries.

Moreover, growing adoption of Zero Trust security frameworks, SASE architectures, and managed security services is creating substantial opportunities for cybersecurity vendors and service providers. As enterprises transition toward cloud-first and hybrid work models, demand for identity-centric security, secure remote access, and continuous threat monitoring continues to rise. Telecom operators are also investing heavily in securing 5G and edge computing environments, creating new revenue opportunities for providers offering network security, threat intelligence, managed detection and response (MDR), and cloud-native security solutions. These trends are expected to drive sustained market expansion throughout the forecast period.

Analyst Perspective

The IT and telecom cybersecurity market is at a pivotal inflection point, transitioning from traditional perimeter-based security frameworks to AI-driven, cloud-native, and identity-centric security architectures. From an analyst's standpoint, this shift is primarily being driven by the convergence of rapid cloud adoption, 5G rollout, edge computing expansion, and exponential growth in connected devices, all of which are significantly enlarging the attack surface across enterprise and telecom ecosystems. As cyber threats become more sophisticated, leveraging automation, AI, and supply-chain vulnerabilities, organizations are increasingly prioritizing proactive, intelligence-led security approaches such as Zero Trust, SASE, and extended detection and response (XDR) models.

At the same time, the market is witnessing a clear structural shift toward platform consolidation and managed security services, as enterprises struggle with tool sprawl, talent shortages, and rising operational complexity. Large vendors are strengthening their end-to-end cybersecurity ecosystems through acquisitions and integration of AI-powered analytics, while emerging players are disrupting the market with cloud-native, subscription-based, and simplified security offerings. However, margin pressures, regulatory fragmentation across regions, and high implementation complexity continue to challenge scalability. Overall, the market outlook remains strongly positive, supported by rising cyber risk exposure, increasing regulatory enforcement, and enterprise demand for unified, automated, and continuously adaptive cybersecurity solutions.

Component Insights

Based on component, the hardware segment led the market with the largest revenue share of 55.5% in 2025. The integration of AI and machine learning (ML) into cybersecurity software is transforming how threats are detected and mitigated. AI-powered cybersecurity software can analyze vast amounts of data in real time, identifying patterns and anomalies that might signal potential attacks. This predictive capability enables companies to detect threats earlier and respond more effectively, minimizing damage. The adoption of AI-based security solutions is growing rapidly, as IT and telecom companies look to enhance their security posture in the face of increasingly complex threats

The services segment is expected to grow at the fastest CAGR of 14.2% over the forecast period. The increasing regulatory pressures faced by IT and telecom companies. Compliance with data protection regulations such as GDPR, CCPA, and sector-specific standards such as PCI-DSS (for telecoms handling payment data) requires continuous monitoring, auditing, and reporting. Cybersecurity service providers offer compliance management and auditing services to help companies meet these legal requirements and avoid fines. As governments and industry bodies tighten regulations around data privacy and security, the demand for cybersecurity services that ensure compliance is expected to grow significantly.

Security Insights

Network security accounted for the largest market share in the IT and telecom cybersecurity market primarily due to the sector’s heavy reliance on highly interconnected and continuously exposed network infrastructures. Telecom operators and IT service providers manage vast volumes of data traffic across cloud environments, 5G networks, IoT ecosystems, and distributed data centers, making the network layer the most frequent entry point for cyberattacks such as DDoS attacks, ransomware propagation, man-in-the-middle attacks, and unauthorized access attempts. As digital transformation accelerates, organizations are increasingly prioritizing perimeter defense, intrusion detection and prevention systems, firewalls, and secure network gateways to safeguard critical communication channels and ensure service continuity. Additionally, the rapid expansion of 5G and edge computing has significantly increased the attack surface, further strengthening demand for advanced network security solutions. Regulatory compliance requirements and the growing adoption of zero-trust architectures have also reinforced investments in network-centric security controls, solidifying its dominance in overall cybersecurity spending within the IT and telecom sector.

Cloud security is projected to witness the fastest growth by security type in the IT and telecom cybersecurity market due to the rapid and large-scale migration of workloads, applications, and data from on-premises infrastructure to cloud environments. IT and telecom organizations are increasingly adopting multi-cloud and hybrid cloud architectures to improve scalability, reduce operational costs, and support digital services such as 5G, IoT platforms, and edge computing, which significantly expands the attack surface. This shift has heightened the need for advanced cloud-native security solutions such as cloud workload protection platforms (CWPP), cloud security posture management (CSPM), identity and access management (IAM), and encryption services to protect distributed assets and workloads. Additionally, rising concerns over data breaches, misconfigurations, and compliance risks in shared cloud environments are pushing enterprises to invest heavily in proactive and automated cloud security tools. The growing adoption of DevSecOps practices and zero-trust frameworks in cloud environments is further accelerating demand, making cloud security the fastest-growing segment in this market.

Technology Insights

Security Information and Event Management (SIEM) accounted for the largest market share due to its critical role in providing centralized visibility, real-time threat detection, and efficient incident response across highly complex and distributed IT environments. IT and telecom organizations generate enormous volumes of security logs and network events from data centers, cloud platforms, 5G infrastructure, endpoints, and IoT devices, making centralized monitoring essential for identifying sophisticated cyber threats. SIEM solutions aggregate and correlate data from multiple security tools, enabling security operations centers (SOCs) to detect anomalies, prioritize alerts, and accelerate incident investigations while reducing response times. The increasing frequency of advanced persistent threats (APTs), ransomware attacks, and insider threats, combined with stringent regulatory compliance requirements for audit trails and continuous monitoring, has further strengthened enterprise adoption of SIEM platforms. Additionally, the integration of artificial intelligence, machine learning, and threat intelligence feeds into modern SIEM solutions has enhanced detection accuracy and operational efficiency, reinforcing its position as the dominant cybersecurity technology in the IT and telecom market.

Secure Access Service Edge (SASE) is projected to witness the fastest growth due to the rapid shift toward cloud-first, remote, and highly distributed work environments that require unified and scalable security solutions. Traditional perimeter-based security models are no longer sufficient as IT and telecom organizations increasingly rely on cloud applications, mobile workforces, and edge computing, which demand secure, location-independent access. SASE addresses this need by converging networking and security functions such as secure web gateways, cloud access security brokers (CASB), zero trust network access (ZTNA), and firewall-as-a-service into a single cloud-native platform. This integrated approach simplifies security architecture, reduces operational complexity, and improves performance for users accessing applications from anywhere. Additionally, the rise of 5G networks, IoT expansion, and hybrid cloud adoption is further accelerating demand for agile, low-latency, and identity-driven security frameworks. Growing enterprise focus on zero trust security models and cost-efficient consolidation of multiple security tools is also driving rapid SASE adoption, making it the fastest-growing technology segment in the market.Deployment Insights

Based on deployment, the cloud segment led the market with the largest revenue share of 61.9% in 2025, driven by the requirements of the integration with legacy systems. Many IT and telecom companies rely on legacy infrastructure that may not be easily compatible with cloud-based security solutions. On-premise deployment allows for better compatibility with existing systems, providing a smoother transition when upgrading security infrastructure. This is especially important for large telecom companies with vast, complex networks that require highly customized security solutions tailored to their specific needs. On-premise deployment ensures that companies can implement these custom solutions more effectively, without the need to completely overhaul their systems, making it an appealing choice for organizations seeking to balance innovation with stability.

The cloud segment is expected to grow at a significant CAGR over the forecast period, owing to the increased demand for hybrid and multi-cloud environments. As more IT and telecom companies adopt multi-cloud strategies to diversify their operations and avoid vendor lock-in, the complexity of securing data across multiple cloud platforms grows. This complexity has driven the demand for advanced security solutions that can offer seamless protection and management across various cloud providers. Tools that ensure unified security management, threat visibility, and compliance across hybrid and multi-cloud environments are becoming crucial for enterprises, further contributing to market expansion.

Enterprise Size Insights

Based on enterprise size, the large enterprises segment led the market with the largest revenue share of 74.3% in 2025. The digital transformation journey of SMEs has accelerated significantly in recent years, driving the need for enhanced cybersecurity measures. As these businesses adopt cloud computing, e-commerce platforms, and digital communication tools, they become more vulnerable to cyber threats. This transformation has led SMEs to recognize the importance of investing in cybersecurity to protect their digital assets and customer data.

The large enterprise segment is expected to grow at a significant CAGR over the forecast period. The adoption of advanced technologies, such as the Internet of Things (IoT), artificial intelligence (AI), and blockchain, is reshaping the IT and telecom landscape for large enterprises. While these technologies offer significant benefits, they also introduce new vulnerabilities that necessitate enhanced security measures. Large organizations are increasingly seeking cybersecurity solutions that can integrate with these emerging technologies, enabling them to secure their evolving digital environments effectively.

Regional Insights

North America dominated the global IT and telecom cyber security market with the largest revenue share of 37.9% in 2025. North American enterprises are significantly ramping up their investments in cybersecurity solutions in response to the escalating frequency and sophistication of cyber threats. With high-profile breaches making headlines, organizations recognize the urgent need to bolster their security postures. As a result, companies are allocating larger portions of their IT budgets to cybersecurity technologies, including advanced threat detection, incident response, and endpoint security solutions. This trend is expected to continue as organizations prioritize cybersecurity as a critical component of their overall risk management strategies.

U.S. IT And Telecom Cyber Security Market Trends

The IT and telecom cyber security market in the U.S. held the largest share in the North America region in 2025. Regulatory compliance is a significant trend impacting the U.S. IT and telecom cybersecurity landscape. With the introduction of stringent data protection regulations, such as the California Consumer Privacy Act (CCPA) and various sector-specific guidelines, organizations must ensure compliance to avoid penalties and reputational harm. This regulatory pressure is driving investment in cybersecurity solutions that facilitate compliance, including data encryption, identity management, and comprehensive auditing capabilities.

Europe IT And Telecom Cyber Security Market Trends

The IT & telecom cyber security market in Europe is anticipated to grow at a significant CAGR from 2025 to 2030, owing to the growing adoption of advanced cybersecurity technologies, including artificial intelligence (AI), machine learning, and automation. European companies are increasingly leveraging these technologies to enhance threat detection, response capabilities, and overall security posture.

The UK IT & telecom cyber security market is expected to grow at a rapid CAGR during the forecast period, due to growing cyber incidents highlighting vulnerabilities within supply chains, prompting organizations to focus more on securing their supply chain networks. As businesses increasingly rely on third-party vendors and partners, the risk of cyber threats infiltrating through these connections has become a significant concern. Organizations are adopting strategies to assess the cybersecurity posture of their suppliers, implement stringent security requirements, and conduct regular audits to mitigate risks.

The IT & telecom cyber security market in Germany held a substantial market share in Europe in 2024. The increasing awareness of the cyber skills gap is driving initiatives aimed at developing a skilled cybersecurity workforce in Germany. The country is investing in education and training programs to address the shortage of qualified professionals in the cybersecurity field. Organizations are collaborating with academic institutions and industry partners to create training initiatives, internships, and certification programs that foster the development of new cybersecurity talent.

Asia Pacific IT And Telecom Cyber Security Market Trends

The IT & telecom cyber security market in Asia Pacific is anticipated to grow at a significant CAGR of 16.3% from 2025 to 2030, driven by the growing adoption of cloud services. As businesses migrate their operations to the cloud, they face new challenges in securing their data and applications. Consequently, there is a surge in demand for cloud security solutions that offer features such as encryption, identity and access management, and threat detection. Organizations are increasingly seeking to implement shared responsibility models to ensure that both cloud providers and users are accountable for security.

The Japan IT & telecom cyber security market is expected to grow at a rapid CAGR during the forecast period. The Japanese government has implemented various initiatives to enhance national cybersecurity, particularly in response to the increasing frequency of cyber-attacks. The establishment of the Cybersecurity Strategy Council and the National Center of Incident Readiness and Strategy for Cybersecurity (NISC) signifies a concerted effort to boost defenses. These initiatives include setting stricter regulations for data protection and cybersecurity, particularly for critical infrastructure sectors such as finance, healthcare, and telecommunications.

The IT & telecom cyber security market in China held a substantial market share in Asia Pacific in 2024, owing to the growing adoption of advanced technologies such as artificial intelligence (AI) and big data analytics in cybersecurity practices. Chinese companies are leveraging these technologies to enhance their threat detection and response capabilities. AI-driven security solutions can analyze vast amounts of data in real-time, identify anomalies, and predict potential threats, allowing organizations to proactively mitigate risks.

Key IT And Telecom Cyber Security Company Insights

Key players operating in the global market includePalo Alto Networks, Inc.,Cisco Systems, Inc.,Broadcom, CrowdStrike, and IBM Corporation. The companies are focusing on various strategic initiatives, including new product development, partnerships & collaborations, and agreements to gain a competitive advantage over their rivals. The following are some instances of such initiatives.

Key IT And Telecom Cyber Security Companies:

The following are the leading companies in the IT and telecom cyber security market.

-

AO Kaspersky Lab

-

Broadcom

-

Check Point Software Technology Ltd.

-

Cisco Systems, Inc.

-

CrowdStrike

-

IBM Corporation

-

McAfee, Inc.

-

Microsoft

-

Palo Alto Networks, Inc.

-

Sophos

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Mature Players (AO Kaspersky Lab; Broadcom; Check Point Software Technologies; Cisco Systems; IBM Corporation; McAfee; Microsoft; Palo Alto Networks)

- Focus on delivering comprehensive cybersecurity platforms that integrate endpoint, network, cloud, identity, and threat intelligence capabilities under unified security architectures.

- Expand through strategic acquisitions, partnerships, and AI-driven innovation to strengthen managed security services, Zero Trust offerings, and cloud security portfolios.

- Strong global brand recognition, extensive enterprise customer bases, and established channel partner networks that support large-scale deployments.

- Broad product portfolios with advanced threat intelligence capabilities, enabling end-to-end security coverage across complex enterprise and telecom environments.

- Large and complex product ecosystems can increase deployment, integration, and management complexity for customers.

- Premium pricing structures may limit adoption among cost-sensitive SMEs and emerging-market customers.

Emerging Players (CrowdStrike and Sophos)

- Focus on cloud-native, AI-powered cybersecurity solutions with emphasis on endpoint protection, threat intelligence, managed detection and response (MDR), and simplified security operations.

- Leverage subscription-based SaaS models and platform consolidation strategies to rapidly expand customer adoption and recurring revenue streams.

- High agility and innovation speed, enabling rapid response to emerging threats and faster deployment of new security capabilities.

- Strong cloud-native architectures provide scalability, centralized management, and lower infrastructure requirements compared to many legacy security platforms.

- Relatively narrower product portfolios compared to diversified cybersecurity giants, often requiring partnerships for complete security coverage.

- Greater dependence on specific security domains such as endpoint security and MDR services can increase exposure to competitive pressures within those segments.

Recent Developments

-

In September 2024, Broadcom, Comcast, and Charter Communications announced a collaborative effort to develop Unified DOCSIS chipsets for smart amplifiers, network nodes, and cable modems, facilitating both FDX and ESD versions of the DOCSIS 4.0. The partnership aims to significantly enhance DOCSIS networks by integrating advanced Artificial Intelligence and Machine Learning, leveraging Broadcom’s embedded Neural Processing Unit (NPU) in network nodes, smart amplifiers, and modems. These advancements aim to enable operators to boost operational efficiency and enhance network security and reliability with features like advanced cybersecurity, intrusion detection, and phishing protection to combat AI-driven threats.

-

In March 2024, Cisco completed the acquisition of Splunk, an American software company paving the way for enhanced visibility and insights across an organization’s digital landscape. This move allows Cisco to offer distinctive solutions tailored for networking, security, and operations leaders. Coupled with its investments in channels and AI, this acquisition enables customers to unlock business value than before.

IT And Telecom Cyber Security Report Scope

Report Attribute

Details

Market size in 2025

USD 50.4 billion

Estimated market size in 2026

USD 55.2 billion

Projected market size by 2033

USD 109.7 billion

Growth rate

CAGR of 10.3% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecasts period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecasts, company market share analysis, competitive landscape, growth factors, and trends

Segments covered

Component, Security, Technology, Deployment, Enterprise Size, and Region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; China; Japan; India; South Korea; Australia; Brazil; Saudi Arabia; South Africa; UAE

Key companies profiled

AO Kaspersky Lab; Broadcom; Check Point Software Technology Ltd.; Cisco Systems, Inc.; CrowdStrike; IBM Corporation; McAfee, Inc.; Microsoft; Palo Alto Networks, Inc.; Sophos

Customization scope

Free report customization (equivalent to up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global IT And Telecom Cyber Security Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global IT & telecom cyber security market report based on component, deployment, deployment, enterprise size, and region.

-

Component Outlook (Revenue, USD Billion, 2021 - 2033)

-

Hardware

-

Software

-

Services

-

-

Security Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Endpoint Security

-

Cloud Security

-

Network Security

-

Application Security

-

Infrastructure Protection

-

Data Security

-

Others

-

-

Technology Outlook (Revenue, USD Million, 2021 - 2033)

-

Software-Defined Wide Area Network (SD-WAN)

-

Secure Access Service Edge (SASE)

-

Zero Trust Network Access (ZTNA)

-

Security Information and Event Management (SIEM)

-

Virtual Private Network (VPN)

-

Others

-

-

Deployment Outlook (Revenue, USD Billion, 2021 - 2033)

-

On-premise

-

Cloud

-

-

Enterprise Size Outlook (Revenue, USD Billion, 2021 - 2033)

-

Large Enterprises

-

Small and Medium-sized Enterprises (SMEs)

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Research Methodology

The IT & telecom cyber security market figures in this report are based on a proven research process that combines executive interviews with secondary research from proprietary databases, company filings, and recognized regulatory and institutional sources. Market size is built through value-chain sizing - reconciling supply-side and demand-side estimates - and triangulated with bottom-up and top-down approaches. Every estimate passes multiple levels of expert validation before publication, with each IT & telecom cyber security segment quantified using the revenue-capture definitions in the table below.

Segment Definition

Segment - Component

Revenue Capture Definition

Hardware

Revenue is generated through the sale and deployment of cybersecurity hardware solutions such as firewalls, secure gateways, intrusion detection and prevention systems (IDS/IPS), network appliances, secure routers, and telecom security equipment. Additional revenue is captured through hardware upgrades, maintenance contracts, and lifecycle replacement requirements driven by evolving threat landscapes.

Software

Revenue is earned through licensing, subscriptions, and recurring SaaS fees for cybersecurity software solutions including endpoint protection, SIEM platforms, identity and access management (IAM), threat intelligence, encryption, vulnerability management, and security analytics tools.

Services

Revenue is captured through consulting, implementation, managed security services (MSS), incident response, threat hunting, penetration testing, compliance audits, security assessments, and cybersecurity training. Recurring managed detection and response (MDR) and security operations center (SOC) services contribute significantly to long-term revenue generation.

Segment - Security

Revenue Capture Definition

Endpoint Security

Revenue is generated through endpoint protection platforms, antivirus solutions, endpoint detection and response (EDR), mobile device security, and endpoint management services.

Cloud Security

Revenue is earned through cloud workload protection, cloud security posture management (CSPM), cloud access security brokers (CASB), container security, and cloud-native application protection solutions. Growing cloud adoption and multi-cloud environments continue to drive recurring subscription revenue.

Network Security (including NaaS)

Revenue is captured through firewalls, intrusion prevention systems, secure network access solutions, network monitoring platforms, and Network-as-a-Service security offerings.

Application Security

Revenue is generated through application testing, DevSecOps solutions, web application firewalls (WAF), API security, code scanning, and runtime application protection.

Infrastructure Protection

Revenue is earned through securing servers, data centers, telecom infrastructure, operational technology (OT) environments, and critical digital assets.

Data Security

Revenue is captured through encryption solutions, data loss prevention (DLP), tokenization, data governance, backup security, and privacy compliance solutions.

Others

This segment includes identity and access management (IAM), email security, threat intelligence, fraud detection, security orchestration, and emerging cybersecurity technologies. Revenue is generated through specialized security requirements and evolving enterprise risk management needs.

Segment - Technology

Revenue Capture Definition

Software-Defined Wide Area Network (SD-WAN)

Revenue is generated through SD-WAN software subscriptions, implementation services, network optimization solutions, and managed SD-WAN offerings.

Secure Access Service Edge (SASE)

Revenue is earned through cloud-delivered security and networking services combining SD-WAN, Zero Trust security, CASB, secure web gateways, and firewall-as-a-service capabilities. Subscription-based pricing and managed SASE deployments contribute significantly to recurring revenue.

Zero Trust Network Access (ZTNA)

Revenue is captured through identity-centric access control platforms, authentication services, policy management, and continuous verification solutions.

Security Information and Event Management (SIEM)

Revenue is generated through SIEM software licensing, cloud-based subscriptions, log management, threat analytics, compliance monitoring, and managed SOC services.

Virtual Private Network (VPN)

Revenue is earned through VPN software licenses, subscription services, secure remote access platforms, and enterprise connectivity solutions. Continued hybrid work adoption and secure remote access requirements support recurring revenue generation.

Others

This segment includes Extended Detection and Response (XDR), Security Orchestration Automation and Response (SOAR), threat intelligence platforms, deception technologies, and emerging AI-powered security solutions. Revenue is generated through advanced threat protection and specialized security applications.

Segment - Deployment

Revenue Capture Definition

Cloud

Revenue is generated through subscription-based cloud security solutions, SaaS cybersecurity platforms, cloud-native protection services, and managed cloud security offerings. Recurring revenue models, scalability, and growing cloud adoption are key contributors to market growth.

On-Premise

Revenue is earned through software licenses, hardware appliances, implementation services, maintenance contracts, and security infrastructure upgrades deployed within customer-owned environments.

Segment - Enterprise Size

Revenue Capture Definition

Large Enterprises

Revenue is captured through large-scale cybersecurity deployments, enterprise-wide security platforms, SOC operations, managed security services, regulatory compliance programs, and multi-year contracts.

SMEs

Revenue is generated through affordable, cloud-based cybersecurity solutions, managed security services, endpoint protection, and subscription-based security platforms tailored to smaller organizations.

Estimation Model

Layer

Question

Analysis

Digital Infrastructure Layer (Total Addressable Market)

Who can potentially use cybersecurity solutions?

Estimate the total addressable base of enterprises, telecom operators, government agencies, SMEs, cloud users, and connected devices that require protection against cyber threats. This layer defines the maximum potential market for IT and telecom cybersecurity solutions.

Technology Readiness Layer (Serviceable Market)

Who can technically adopt cybersecurity solutions?

Refine the addressable base by assessing cloud adoption, network infrastructure maturity, digital transformation levels, regulatory requirements, and cybersecurity awareness. Organizations with sufficient IT infrastructure and security budgets form the serviceable market.

Security Adoption Layer (Active Market)

Who actively invests in cybersecurity?

Convert the serviceable base into active users based on deployment of security solutions such as endpoint security, cloud security, SASE, ZTNA, SIEM, VPNs, and managed security services. Threat exposure, compliance requirements, and cyber risk management priorities influence adoption.

Monetization Layer (Revenue Realization Model)

How is revenue generated?

Estimate revenue from cybersecurity software subscriptions, hardware appliances, managed security services, consulting, threat intelligence, compliance solutions, and recurring cloud-based security platforms. Premium security technologies and long-term service contracts drive revenue realization.

Delivered Customizations

This report has been delivered with the following In-depth customizations

CLIENT REQUEST

CUSTOMIZATION DELIVERED

VALUE ADDS

Industry-Specific Cybersecurity Demand Assessment

Analyzed cybersecurity adoption patterns across key industries including BFSI, telecom, healthcare, manufacturing, retail, government, and IT services, highlighting sector-specific threat exposure, compliance requirements, and security investment priorities.

Supports targeted go-to-market strategies by identifying high-risk industries, regulatory-driven demand areas, and sector-specific cybersecurity solution opportunities.

Regional Cybersecurity Opportunity Analysis (Global + Emerging Markets Focus)

Delivered a detailed regional breakdown covering North America, Europe, Asia Pacific, Latin America, and Middle East & Africa, with emphasis on regulatory frameworks, cyber threat intensity, digital infrastructure maturity, and enterprise security spending trends.

Enables informed expansion strategies by identifying high-growth geographies, regulatory hotspots, investment priorities, and region-specific cybersecurity adoption barriers and opportunities.

Managed Security & AI-Driven Security Transformation Analysis

Evaluated the shift toward managed security services (MSSP, MDR, SOC-as-a-Service) and AI-enabled cybersecurity operations, including automation of threat detection, response orchestration, and predictive security analytics.

Help stakeholders understand the transition toward service-led cybersecurity models, recurring revenue opportunities, and the impact of AI on security operations efficiency and cost optimization.

About the Author(s)

Network Security Research Team

Technology · Network SecurityThis report was authored by the network security research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the network security segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.