- Home

- »

- IT Services & Applications

- »

-

Law Enforcement Software Market, Industry Report, 2033GVR Report cover

![Law Enforcement Software Market Size, Share, & Trend Report]()

Law Enforcement Software Market (2026 - 2033) Size, Share, & Trend Analysis By Component (Solutions, Services), By Deployment (On-premises, Cloud), By End Use (Police Departments, Law Enforcement Agencies, Municipalities), By Region, And Segment Forecasts

Market Size, 2025

$18.3BMarket Estimate, 2026

$20.4BMarket Forecast, 2033

$40.8BCAGR, 2026–2033

10.4%Law Enforcement Software Market Summary

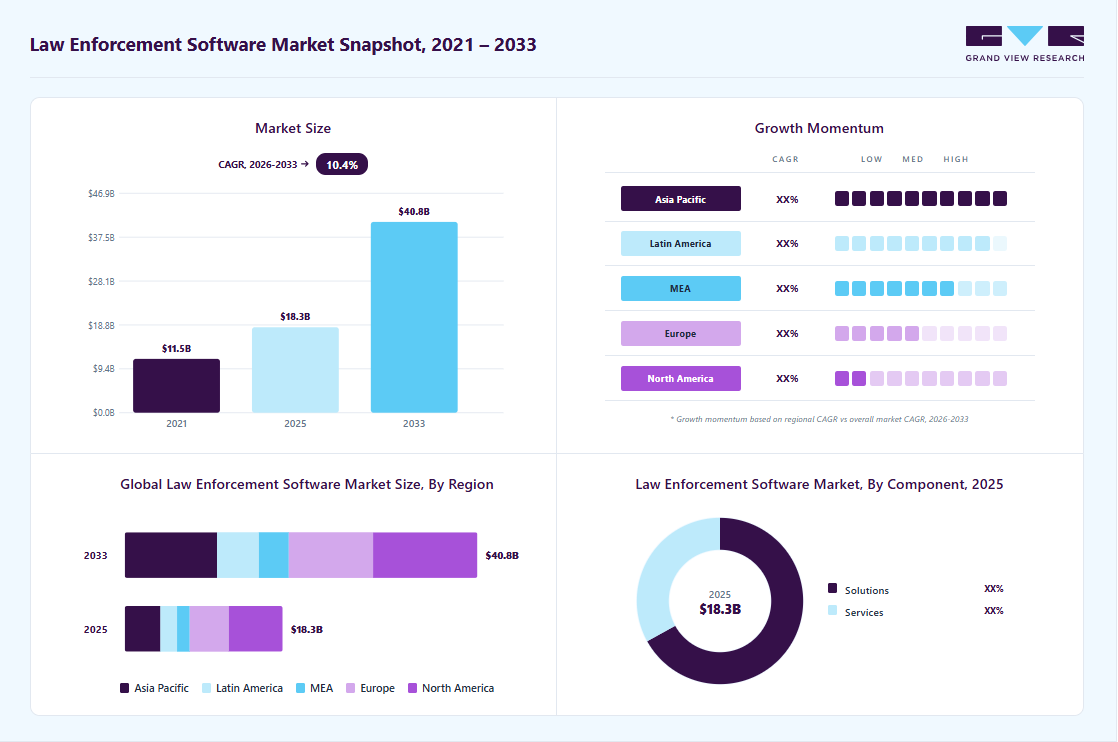

The global law enforcement software market size was valued at USD 18.3 billion in 2025 and is projected to grow from USD 20.4 billion in 2026 to USD 40.8 billion by 2033, at a CAGR of 10.4% from 2026 to 2033. The North America law enforcement software market held the largest share of 34.1% of the global market in 2025. The market growth is driven by the increasing need for advanced digital solutions to enhance public safety, streamline criminal investigations, and improve operational efficiency.

Key Market Trends & Insights

- By component: Solutions segment dominated the market, with a revenue share of 67% in 2025.

- By deployment: Cloud segment held the largest market share in 2025.

- By end use: Police departments segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: North America (34.1% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- The law enforcement software industry in the U.S. is expected to grow significantly at a CAGR of 12.1% from 2026 to 2033.

Market Size & Forecast

- Market size in 2025: USD 18.3 Billion

- Estimated market size in 2026: USD 20.4 Billion

- Projected market size by 2033: USD 40.8 Billion

- CAGR (2026-2033): 10.4%

Rising crime rates, growing adoption of digital evidence management, and the integration of AI, analytics, and cloud technologies in policing are accelerating demand for such software. As crime becomes more sophisticated, law enforcement agencies are rapidly adopting advanced software solutions, including records management systems (RMS), computer-aided dispatch (CAD), and digital evidence management tools, to enhance operational efficiency, data accuracy, and real-time decision-making. For instance, in October 2025, West Midlands Police in the UK advanced its digital transformation by integrating secure AI capabilities through Android Enterprise devices, marking a major step toward smarter, more efficient policing. The initiative aims to enhance officer and staff productivity by replacing traditional, time-consuming procedural workflows with intuitive AI-driven guidance and real-time access to critical police records. This seamless integration of AI and custom Android applications will enable officers to securely retrieve information and procedural support on the go, reducing their administrative workload and allowing them to dedicate more time to community engagement and public safety.")

In addition, governments across the world are also investing heavily in modernizing public safety infrastructure through smart policing initiatives, which is significantly fueling the demand for integrated law enforcement software. For instance, in March 2024, the Port Authority Police Department of New York and New Jersey launched a USD 15 million modernization program to upgrade its law enforcement technology, including a data analytics platform for crime insights, mobile-first reporting tools, and enhanced dispatch systems to boost response efficiency. The increasing use of cloud-based and AI-driven analytics solutions that facilitate predictive policing and improve incident response is also driving growth in the law enforcement software industry. Artificial intelligence, big data analytics, and IoT technologies are increasingly being utilized to analyze large volumes of crime data, identify patterns, and predict potential threats. This trend is particularly strong in North America and Europe, where digital policing reforms are being prioritized. Additionally, the integration of mobile applications and body-worn camera systems with law enforcement software helps ensure transparency, accountability, and effective evidence management, further supporting market expansion.

Moreover, the growing concern for public safety amid increasing urbanization and geopolitical tensions has led to a surge in demand for real-time surveillance and crime analysis tools. The shift toward interoperable and scalable software platforms allow agencies to share intelligence securely across jurisdictions, improving collaboration and crime-solving capabilities. The private sector’s involvement in developing advanced cybersecurity and data protection features also contributes to market growth by ensuring compliance with strict data privacy regulations.

Market Dynamics

Rising crime rates, increasing cyber threats, and the growing complexity of criminal investigations are driving law enforcement agencies to adopt advanced software solutions for real-time surveillance, predictive analytics, digital evidence management, and faster emergency response. Additionally, the increasing need for centralized data sharing, crime tracking, and efficient case management is further accelerating the demand for law enforcement software across police departments and public safety organizations globally.

For instance, in 2024, the FBI Uniform Crime Reporting (UCR) Program highlighted continued concerns regarding violent crimes and law enforcement resource management, with violent crimes in Massachusetts reaching 22,457 reported incidents. Additionally, Massachusetts’ violent crime solve rate remained above the U.S. average and increased to over 50% in 2024, reflecting the growing reliance on advanced analytics, records management systems, and AI-enabled investigative tools to improve crime resolution efficiency and public safety operations. Consequently, the increasing pressure on law enforcement agencies to improve crime prevention, investigation accuracy, operational transparency, and response efficiency is significantly contributing to the growth of the law enforcement software market.

Algorithmic bias and discrimination are emerging as a major restraint on the growth of the law enforcement software market, as AI-powered policing systems rely on historical crime data that may contain racial, socioeconomic, or geographic biases. This leads to inaccurate risk assessments, wrongful identification, over-policing of certain communities, and reduced public trust in automated law enforcement technologies. Additionally, concerns regarding transparency, accountability, civil rights violations, and ethical use of facial recognition and predictive policing tools are further limiting widespread adoption across government agencies and public safety organizations. For instance, in February 2025, Amnesty International reported that predictive policing systems used by UK police forces were “supercharging racism” by relying on historically biased policing data, which disproportionately targeted poor and racialized communities. The report highlighted that AI-driven predictive tools can reinforce discriminatory policing patterns and intensify stop-and-search practices, raising serious concerns regarding fairness, human rights, and regulatory oversight.

Additionally, growing cases of wrongful arrests linked to facial recognition inaccuracies and increasing scrutiny from regulators and civil rights organizations are compelling governments to impose stricter AI governance and compliance requirements. As a result, concerns over algorithmic fairness, legal liabilities, and reputational risks are hindering the growth of the global law enforcement software market.

The growing adoption of artificial intelligence (AI) and cloud-based policing solutions is expected to create significant future opportunities for the law enforcement software market. Law enforcement agencies implement AI-powered analytics, predictive policing, automated reporting, and real-time surveillance systems to improve operational efficiency, accelerate investigations, and enhance public safety outcomes. At the same time, cloud-based platforms enable secure data storage, remote accessibility, inter-agency collaboration, and faster information sharing, making policing operations more efficient and scalable across regions.

For instance, in June 2025, the Uttar Pradesh government launched an AI-based Smart Policing System (AI-SPS) in Ghazipur, India, aimed at supporting crime mapping, predictive policing, digital investigation tracking, and centralized data management. The initiative reflects the increasing government focus on integrating AI and cloud-enabled technologies to modernize law enforcement infrastructure and strengthen crime prevention capabilities. Moreover, the rising investments in smart city projects, connected surveillance systems, IoT-enabled public safety infrastructure, and digital transformation initiatives are expected to further accelerate the deployment of advanced law enforcement software solutions globally. Therefore, the increasing shift toward AI-driven and cloud-based policing ecosystems is anticipated to create long-term growth opportunities for the law enforcement software market.

Market Concentration & Characteristics

The law enforcement software market is moderately concentrated, with a mix of established global technology providers and specialized public safety software vendors dominating the landscape. Large players hold significant market share due to their strong product portfolios, advanced technological capabilities, and long-standing contracts with government and federal agencies. These companies typically offer integrated platforms covering records management, computer-aided dispatch (CAD), digital evidence management, and analytics, creating high entry barriers for new entrants due to strict compliance requirements, data security standards, and procurement complexities in the public sector.

In terms of market characteristics, the industry is highly technology-driven and innovation-intensive, with strong emphasis on artificial intelligence, cloud computing, cybersecurity, and interoperability across systems. Demand is primarily driven by government modernization programs, smart policing initiatives, and the need for real-time data sharing and predictive analytics. Additionally, the market is characterized by long sales cycles, high regulatory oversight, and strong vendor lock-in due to the critical and sensitive nature of law enforcement operations, making customer switching relatively low once systems are deployed.

Component Insights

The solutions segment dominated the market and accounted for the revenue share of 67.0% in 2025, driven by the growing demand for customized and modular software platforms that cater to the diverse operational needs of different law enforcement agencies. Agencies are increasingly seeking integrated solutions that combine functionalities such as case management, incident tracking, and digital forensics into a single unified interface to streamline workflows and reduce administrative burdens.

The services segment is anticipated to grow at the highest CAGR during the forecast period due to the increasing need for continuous system support, software customization, and training services to ensure effective deployment and utilization of complex law enforcement platforms. As agencies adopt more advanced digital systems, they rely heavily on professional and managed services for implementation, integration, and maintenance to minimize downtime and optimize system performance. The surge in demand for consulting services to align technology adoption with evolving regulatory standards and operational requirements is also propelling market growth.

Deployment Insights

The cloud segment dominated the market and accounted for the largest revenue share in 2025, driven by the growing need for scalable, flexible, and cost-efficient infrastructure that supports remote accessibility and inter-agency collaboration. Cloud-based solutions enable law enforcement agencies to securely store and process vast amounts of data, including video evidence, incident reports, and analytics, without the limitations of on-premise hardware. The increasing adoption of hybrid and multi-cloud environments allows agencies to maintain control over sensitive data while benefiting from the agility and real-time accessibility of cloud platforms.

The on-premises segment is expected to grow at a significant CAGR during the forecast period due to the increasing need for greater control, customization, and data sovereignty among agencies handling highly sensitive information. Many law enforcement bodies, particularly in regions with strict data privacy regulations or limited cloud infrastructure, prefer on-premises systems to ensure that critical intelligence and investigative data remain within secure internal networks. This deployment model also appeals to organizations requiring advanced customization to meet specific operational, jurisdictional, or security requirements.

End Use Insights

The police departments segment dominated the market and accounted for the largest revenue share in 2025, driven by the increasing focus on improving field-level coordination, operational transparency, and rapid incident response. Police forces are adopting advanced digital tools to enhance patrol management, automate reporting, and support evidence-based decision-making, thereby improving overall efficiency. The rise in urban crime, traffic violations, and emergencies is prompting departments to rely on integrated platforms that connect dispatch systems, mobile devices, and command centers in real time.

The municipalities segment is expected to grow at a significant CAGR over the forecast period, owing to the rising emphasis on smart city initiatives and integrated public safety management. Local governments are increasingly investing in digital platforms that enable seamless coordination among emergency services, law enforcement units, and civic departments, thereby enhancing situational awareness and incident response. The need to manage urban challenges such as traffic control, community safety, and disaster response through data-driven systems is further accelerating adoption.

Regional Insights

North America dominated the global market, accounting for the largest revenue share of 34.1% in 2025, due to the region’s early adoption of advanced technologies, including artificial intelligence, predictive analytics, and biometrics, in policing. Strong government funding toward modernizing public safety infrastructure and enhancing interoperability between federal, state, and local law enforcement agencies is a major catalyst. The growing focus on reducing manual reporting, combined with the rise of cybercrime and the increasing need for digital evidence management, has further accelerated software adoption.

U.S. Law Enforcement Software Market Trends

The law enforcement software industry in the U.S. is expected to grow significantly at a CAGR of 12.1% from 2026 to 2033, due to the growing emphasis on community policing, accountability, and transparency amid rising public scrutiny of law enforcement practices. Agencies are increasingly investing in integrated platforms for body-worn camera management, real-time crime mapping, and digital forensics to improve operational visibility and evidence integrity.

Europe Law Enforcement Software Market Trends

The law enforcement software industry in Europe is anticipated to register considerable growth from 2026 to 2033, as governments across the region prioritize data standardization, interoperability, and cross-border intelligence sharing in line with EU security directives. The growing need for collaborative digital systems to combat organized crime, terrorism, and human trafficking is fueling the adoption of integrated law enforcement solutions.

The UK law enforcement software market is expected to grow rapidly in the coming years, driven by the rapid digitalization of policing under initiatives such as the Home Office’s Digital Policing Strategy 2030, which emphasizes data-driven decision-making, cloud migration, and national data interoperability. Police forces are increasingly investing in advanced analytics, automated reporting, and digital case management systems to streamline investigations and reduce administrative workloads.

The law enforcement software market in Germany held a substantial market share in 2025 due to the country’s strong focus on cybersecurity, data protection, and advanced forensic technologies. The government’s investment in digital policing infrastructure, especially for counterterrorism and cybercrime prevention, has significantly boosted demand for secure, on-premises, and hybrid law enforcement systems.

Asia Pacific Law Enforcement Software Industry Trends

Asia Pacific law enforcement software held a significant share in the global market in 2025, due to the increasing urbanization, population density, and the corresponding need for efficient public safety management systems. Governments in the region are investing heavily in digital transformation and smart city projects that integrate law enforcement software for real-time surveillance, crime tracking, and emergency response. The increasing adoption of mobile policing solutions and cloud-based platforms in emerging economies, such as India and Southeast Asian countries, is also driving market growth.

The Japan law enforcement software market is expected to grow rapidly in the coming years due to the country’s strong commitment to public safety, precision technology, and data analytics integration in law enforcement operations. The government’s initiatives to enhance disaster response, cybercrime prevention, and urban surveillance systems have significantly increased demand for reliable and secure law enforcement software.

The law enforcement software market in Japan held a substantial market share in 2025, due to the government’s large-scale investments in public safety digitization and national security infrastructure. The integration of big data analytics, facial recognition, and AI-powered surveillance systems has significantly enhanced policing efficiency in major cities. China’s emphasis on building centralized databases for real-time intelligence and citizen monitoring supports a strong demand for domestic law enforcement software solutions.

Key Law Enforcement Software Company Insights

Key players operating in the law enforcement software industry are Tyler Technologies, Axon Enterprise, Hexagon, Wolters Kluwer N.V., Datamaran, and OneTrust, LLC. The companies are focusing on various strategic initiatives, including new product development, partnerships & collaborations, and agreements to gain a competitive advantage over their rivals. The following are some instances of such initiatives.

-

In October 2025, Axon Enterprise, Inc. upgraded its public safety ecosystem with new AI and real-time features, integrating 911 intelligence, community collaboration, and officer connectivity. Key additions include Axon Assistant, Axon Air Drone as First Responder via Axon Body 4, and the Community Shield and Community Link programs to enhance cooperation between agencies, residents, and businesses.

-

In September 2025, TRULEO expanded its AI Analyst tool to support police chiefs and administrative teams. Building on its proven use among investigators, the enhanced tool now streamlines key administrative functions by automating report generation, compliance documentation, and records management. It also enables agency leaders to track performance trends, analyze crime patterns, and prepare accreditation and budget materials through intuitive data visualizations, strengthening operational efficiency and transparency across departments.

-

In February 2025, Flock Safety introduced two new AI-powered tools, Flock Nova and FreeForm, to help law enforcement agencies accelerate investigations and improve data-driven decision-making. Flock Nova serves as a unified data platform that consolidates information from Flock devices, CAD, Record Management Systems (RMS), and open-source intelligence into a single interface, enabling faster analysis and case resolution. It also supports secure, opt-in data sharing across jurisdictions to enhance collaboration in multi-agency investigations.

Key Law Enforcement Software Companies:

The following are the leading companies in the law enforcement software market. These companies collectively hold the largest Market share and dictate industry trends.

- Axon Enterprise, Inc.

- Datamaran

- EcoVadis

- FactSet

- Hexagon

- LSEG

- NAVEX Global, Inc.

- NEC Corporation

- TRULEO

- OneTrust, LLC.

- SAS Institute Inc.

- Sustainalytics

- Tyler Technologies, Inc.

- Verisk Analytics, Inc.

- Wolters Kluwer N.V.

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weakness

Mature Players: Axon Enterprise; Hexagon; NEC Corp; Tyler Tech; Motorola Solutions; SAS Institute; Verisk; Wolters Kluwer

- Moving from siloed software to integrated cloud ecosystems (e.g., Axon’s "Public Safety OS") that link body-cam hardware directly to AI report-writing and evidence management.

- Acquiring niche tech such as counter-drone systems or specialized forensics to offer a "single-pane-of-glass" solution for government agencies.

- Leveraging massive capital to localize products for international markets, adapting to various regional legal frameworks and language requirements.

- Decades-long relationships with federal and municipal agencies create high switching costs and a "trusted advisor" status.

- Proven ability to handle massive, mission-critical data loads (petabytes of video and records) and CJIS-compliant security.

- Dominance in "Computer-Aided Dispatch" (CAD) and "Records Management Systems" (RMS) that serve as the backbone for all other departmental functions.

- Older product lines can be cumbersome to migrate to the cloud, leading to "clunky" user interfaces compared to modern SaaS startups.

- Rigid, long-term contract structures and high storage fees often alienate smaller departments with limited budgets.

- The sheer size of these organizations can result in bureaucratic delays when attempting to pivot toward disruptive technologies like generative AI.

Emerging Players: TRULEO; OneTrust, LLC.; Datamaran; EcoVadis; NAVEX Global, Inc.; Sustainalytics

- Using advanced machine learning to analyze data that mature players capture but ignore (e.g., TRULEO’s analysis of 100% of body-cam audio for de-escalation insights).

- Designing lightweight, API-first software that plugs directly into existing legacy systems rather than trying to replace them.

- Focus specifically on the "transparency" side of policing, automating FOIA requests and public records redaction.

- Faster deployment of high-impact features, such as automated audio transcription or real-time performance analytics, which solve immediate pain points.

- Deep focus on specific regulatory or ethical niches (e.g., ESG metrics, privacy compliance, or officer wellness) that large generalists overlook.

- Modern, intuitive interfaces that require minimal training, leading to higher adoption rates among officers in the field.

- Small firms often provide only a "piece of the puzzle," forcing agencies to manage multiple vendor relationships and integration points.

- Limited sales and field-support teams make it difficult to compete for massive, multi-year state or national government contracts.

- High reliance on venture capital or niche market trends can lead to concerns about long-term stability and platform longevity for government buyers.

Law Enforcement Software Report Scope

Report Attribute

Details

Market size in 2026

USD 20.41 billion

Revenue forecast in 2033

USD 40.76 billion

Growth rate

CAGR of 10.4% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion and CAGR from 2026 to 2033

Report enterprise size

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Component, deployment, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; Saudi Arabia; South Africa

Key companies profiled

Axon Enterprise, Inc.; Datamaran; EcoVadis; FactSet; Hexagon; LSEG; NAVEX Global, Inc.; NEC Corporation; TRULEO; OneTrust, LLC.; SAS Institute Inc.; Sustainalytics; Tyler Technologies, Inc.; Verisk Analytics, Inc.; Wolters Kluwer N.V.

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Law Enforcement Software Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the law enforcement software market report based on component, deployment, end use, and region:

-

Component Outlook (Revenue, USD Billion, 2021 - 2033)

-

Solutions

-

Computer-Aided Dispatch

-

Record Management

-

Case Management

-

Jail Management

-

Incident Response

-

Digital Policing

-

Others

-

-

Services

-

Implementation

-

Training and Support

-

Consulting

-

-

-

Deployment Outlook (Revenue, USD Billion, 2021 - 2033)

-

On-premises

-

Cloud

-

-

End Use Outlook (Revenue, USD Billion, 2021 - 2033)

-

Police Departments

-

Law Enforcement Agencies

-

Federal and State Agencies

-

Municipalities

-

Correctional Facilities

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Law enforcement software opportunity assessment for a public safety technology provider

Assessment of software demand across different regions

Analysis of adoption trends for RMS, CAD, digital evidence management, and AI-based policing solutions

Benchmarking of key vendors, product capabilities, and deployment models

Identified high-growth public safety software segments

Supported product positioning and expansion strategy

Highlighted key adoption drivers, restraints, and regulatory trends

Customized cross-segmentation analysis for law enforcement software by type and end user

Conducted a cross-segmentation analysis of the law enforcement software type and end user

Evaluated key categories such as Records Management Systems (RMS), Computer-Aided Dispatch (CAD), Digital Evidence Management, Crime Analytics, and Body-Worn Camera Management Platforms

Identified high-adoption software types driving digital transformation

Highlighted end-user segments with the strongest demand

Supported strategic understanding of technology penetration differences across agencies and jurisdictions

Law enforcement digital transformation and market entry assessment for a software vendor

Analysis of regional public safety IT spending and procurement trends

Evaluation of agency requirements for cloud deployment, mobile policing, and real-time data sharing

Identified attractive regional market opportunities

Supported GTM and partnership strategy

Enabled strategic expansion into public safety and security sectors

Frequently Asked Questions About This Report

Asia Pacific is the fastest-growing region over the forecast period.

The solutions segment led with a 67% revenue share in 2025, while services is the fastest-growing segment.

Police departments held the largest share in 2025 and is the fastest-growing model.

Key factors include increasing need for efficient and effective crime prevention and investigation tools as law enforcement agencies strive to enhance public safety amid rising crime rates.

The global law enforcement software market size was estimated at USD 18.3 billion in 2025 and is expected to reach USD 20.4 billion in 2026.

The global law enforcement software market is expected to grow at a compound annual growth rate of 10.4% from 2026 to 2033 to reach USD 40.8 billion by 2033.

North America dominated with a 34.1% revenue share in 2025.

Some key players operating in the law enforcement software market include CSRware, Inc., Datamaran, EcoVadis, OneTrust, LLC., Refinitiv, SAS Institute Inc., Sustainalytics, TruValue Labs, Verisk Analytics, Inc., and Wolters Kluwer N.V.

Cloud held the largest revenue share in 2025, while on-premises is the fastest-growing area.

About the Author(s)

IT Services & Applications Research Team

Technology · IT Services & ApplicationsThis report was authored by the it services & applications research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the it services & applications segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.