- Home

- »

- Next Generation Technologies

- »

-

Mega Data Center Market Size And Share Report, 2026-2033GVR Report cover

![Mega Data Center Market (2026 - 2033)Report]()

Mega Data Center Market (2026 - 2033)

Size, Share & Trends Analysis Report By Solution (Storage, Networking, Server, Security), By Data Center Type (Hyperscale Self-build, Hyperscale Colocation), By Cooling Technology, By Region, And Segment Forecasts

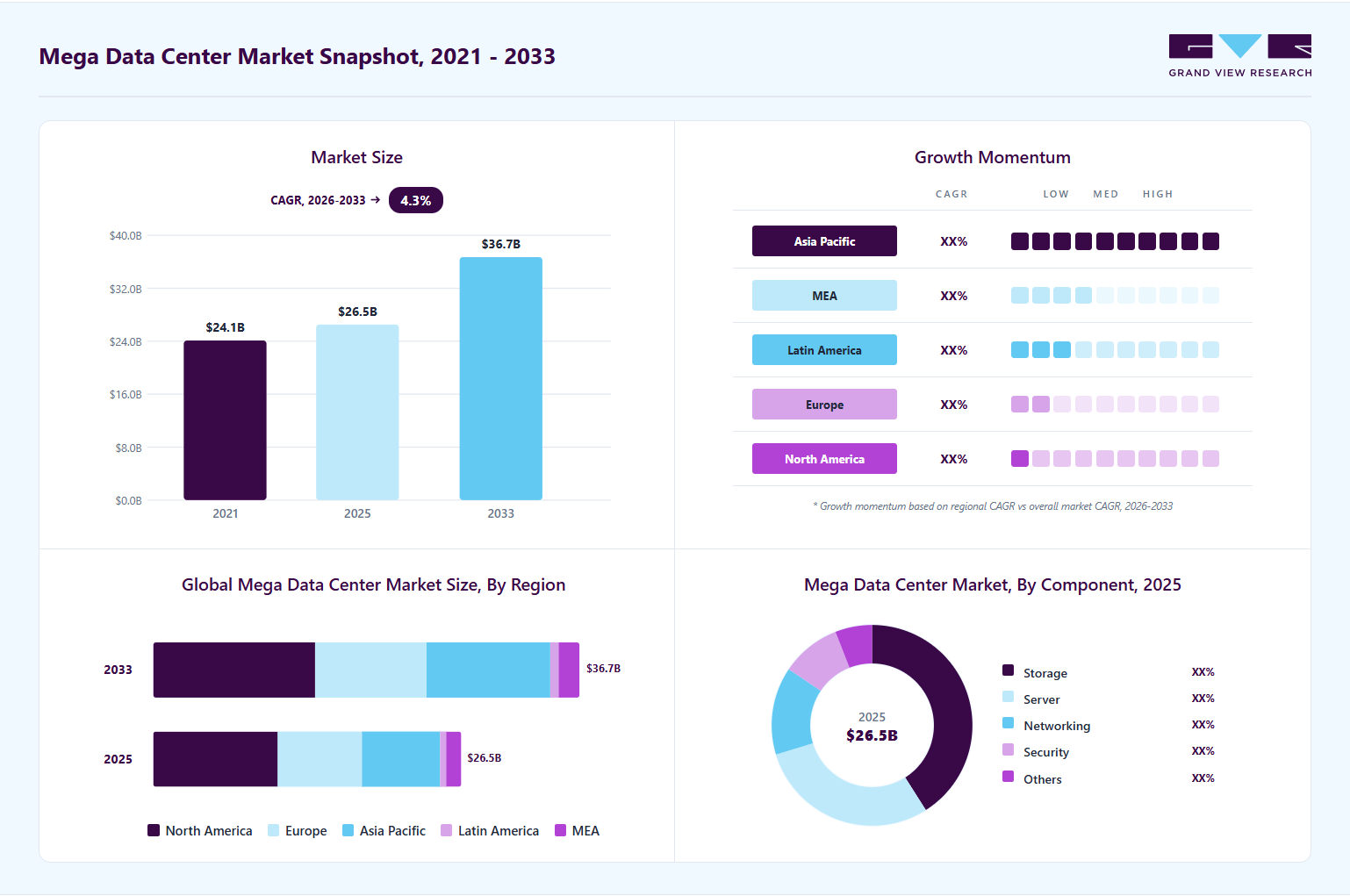

Market Size, 2025

$26.5BMarket Estimate, 2026

$27.3BMarket Forecast, 2033

$36.7BCAGR, 2026–2033

4.3%Mega Data Center Market Summary

The global mega data center market size was valued at USD 26.5 billion in 2025 and is projected to grow from USD 27.3 billion in 2026 to USD 36.7 billion by 2033, at a CAGR of 4.3% from 2026 to 2033. The market in North America dominated with a revenue share of 40.4% in 2025. Enterprises are accelerating migration from on-premise infrastructure to public and hybrid cloud environments, driven by cost optimization, scalability, and the need for high availability.

Key Market Trends & Insights

- By solution: Storage segment held the largest market share of 41.0% in 2025.

- By data center type: Hyperscale self-build segment held the largest market share in 2025.

- By cooling technology: Air-based cooling segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: North America (40.4% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 26.5 Billion

- Estimated market size in 2026: USD 27.3 Billion

- Projected market size by 2033: USD 36.7 Billion

- CAGR (2026-2033): 4.3%

Hyperscalers such as AWS, Microsoft Azure, and Google Cloud continue to expand their global footprint, requiring massive, highly efficient facilities capable of handling Exabyte-scale data workloads.The exponential growth of data generated from AI, machine learning, and high-performance computing (HPC) workloads contributes to the growth of the mega data center industry. Training and deploying large language models, computer vision systems, and real-time analytics platforms demand extremely dense compute environments with advanced cooling and power capabilities. Mega data centers are suited to support these workloads due to their ability to integrate GPU clusters, liquid cooling technologies, and high power densities, making them essential infrastructure for the AI-driven digital economy.

")

The rapid expansion of digital services, including streaming, gaming, social media, and e-commerce, is also fueling demand. With increasing global internet penetration and mobile device usage, especially in emerging markets, data traffic volumes are rising sharply. Mega data centers enable content delivery networks (CDNs) and OTT platforms to process, store, and distribute vast amounts of data efficiently, ensuring low latency and seamless user experiences at scale.

In addition, enterprise digital transformation initiatives are contributing significantly to market growth. Organizations across industries such as BFSI, healthcare, manufacturing, and retail are adopting technologies such as IoT, edge computing, and big data analytics. These transformations generate continuous data streams and require robust backend infrastructure, which is increasingly being consolidated into mega data centers for operational efficiency, centralized management, and enhanced security. For instance, in April 2026, Vodafone Business, in collaboration with Google Cloud, announced the launch of new AI and cybersecurity solutions aimed at accelerating digital transformation among small and medium-sized enterprises. As part of an expanded strategic partnership, the companies are introducing advanced tools that integrate agentic AI capabilities with enhanced cybersecurity features, enabling SMBs to strengthen their digital resilience, automate operations, and better manage evolving cyber threats.

Market Dynamics

The rapid expansion of artificial intelligence (AI), cloud computing, and high-performance computing (HPC) workloads is significantly driving market growth. Enterprises, hyperscale cloud providers, and governments are increasingly investing in large-scale data center infrastructure to support generative AI model training, real-time analytics, cloud-native applications, and massive data storage requirements. In addition, rising internet penetration, digital transformation initiatives, increasing enterprise migration toward cloud platforms, and the growing adoption of AI-enabled services are accelerating demand for high-capacity, energy-efficient mega data centers globally.

For instance, in January 2026, Jones Lang LaSalle IP, Inc., a U.S.-based real estate services company, projected that global data center capacity could reach nearly 200 GW by 2030, driven largely by hyperscale cloud expansion and surging AI demand. The report further highlighted that the sector could almost double in size between 2025 and 2030 due to increasing investments in AI infrastructure and cloud computing ecosystems.

Restraints: Power availability limitations, rising energy consumption, and sustainability concerns are emerging as major restraints on market growth. Mega data centers require enormous electricity capacity and water resources to support AI-driven workloads and cooling infrastructure, creating significant strain on regional power grids and utility networks. In addition, growing concerns regarding carbon emissions, environmental impact, land usage, and water consumption are increasing regulatory scrutiny and delaying approvals for new hyperscale campus developments in several regions.

For instance, in June 2025, the European Commission announced plans to introduce a new Data Centre Energy Efficiency Package aimed at tightening energy-performance standards for hyperscale data centers due to rapidly increasing electricity demand from AI infrastructure. EU officials highlighted that data centers already account for nearly 3% of the region’s electricity consumption, with demand expected to rise sharply because of generative AI expansion and high-density computing workloads.

Market Concentration & Characteristics

The mega data center industry is highly concentrated, with a small group of hyperscale cloud providers, colocation operators, and global digital infrastructure companies dominating capacity expansion and investment activity. Major players possess significant competitive advantages due to their massive capital resources, global land acquisition capabilities, long-term power procurement agreements, and advanced expertise in high-density computing infrastructure. These companies typically operate integrated ecosystems combining hyperscale cloud services, AI computing infrastructure, networking, energy management, and colocation services, creating substantial entry barriers for new participants because of the enormous capital requirements, power availability constraints, complex regulatory approvals, and growing demand for sustainable infrastructure development.

In terms of market characteristics, the industry is highly technology-intensive and infrastructure-driven, with strong emphasis on artificial intelligence workloads, hyperscale cloud expansion, liquid cooling technologies, renewable energy integration, and high-speed interconnectivity. Demand is primarily driven by the rapid adoption of generative AI, growth in cloud computing services, enterprise digital transformation, and increasing requirements for high-performance computing (HPC) environments. Moreover, the market is characterized by long development and construction cycles, high operational and energy costs, stringent environmental and power-efficiency regulations, and long-term customer contracts, resulting in strong vendor stickiness and relatively low switching rates once enterprises deploy workloads within large-scale data center ecosystems.

Solution Insights

The storage segment dominated the market and accounted for the revenue share of 41.0% in 2025 due to the explosive increase in structured and unstructured data generated from AI workloads, IoT devices, enterprise applications, and digital content platforms. As organizations shift toward data-driven decision-making, there is a rising need for scalable, high-performance storage architectures such as object storage and distributed file systems that can efficiently handle Exabyte-scale data volumes.

The security segment is anticipated to grow at the highest CAGR during the forecast period due to the increasing complexity of cyber threats and the critical need to protect high-value, centralized digital infrastructure. As mega data centers host multi-tenant environments and mission-critical workloads, operators are investing heavily in advanced security frameworks such as zero-trust architectures, AI-driven threat detection, and hardware-level encryption to safeguard data integrity and ensure compliance with stringent global regulations.

Data Center Type Insights

The hyperscale self-build segment dominated the market and accounted for the largest revenue share in 2025 as large technology companies seek greater control over infrastructure design, cost structures, and long-term capacity planning. By developing and operating their own facilities, hyperscalers can customize architecture to align precisely with proprietary hardware, software stacks, and workload requirements, enabling tighter integration and optimized performance.

The hyperscale colocation segment is expected to grow at a significant CAGR during the forecast period, driven by the need for rapid geographic expansion and flexible capacity deployment without the long lead times associated with building new facilities. Hyperscalers are increasingly partnering with large colocation providers such as Equinix, Digital Realty, and CyrusOne to enter new markets and scale operations in response to fluctuating demand. This model enables access to pre-built, carrier-neutral ecosystems with dense interconnection capabilities, allowing cloud providers to establish proximity to enterprise customers and network hubs.

Cooling Technology Insights

The air-based cooling segment dominated the market and accounted for the largest revenue share in 2025 due to its proven reliability, lower implementation complexity, and compatibility with existing facility designs. Many operators continue to prefer advanced air-cooling techniques such as hot aisle/cold aisle containment and economization because they offer a cost-effective way to manage thermal loads without requiring significant redesign of infrastructure. Improvements in airflow management, intelligent control systems, and the integration of outside air cooling have enhanced the efficiency of air-based systems, making them viable even as rack densities increase moderately.

The liquid-based cooling segment is expected to grow at a significant CAGR over the forecast period, driven by the rapid rise of ultra-high-density computing environments that exceed the thermal limits of conventional systems. As rack power densities climb beyond traditional thresholds, particularly in GPU-intensive clusters and accelerated computing setups, operators are increasingly adopting direct-to-chip and immersion cooling technologies to efficiently dissipate heat at the source. Liquid cooling enables significantly higher heat transfer efficiency, supports compact rack configurations, and reduces reliance on large air-handling infrastructure, thereby freeing up physical space for compute expansion.

Regional Insights

North America dominated the global market with the largest revenue share of 40.4% in 2025, driven by the presence of a highly mature digital ecosystem and early adoption of advanced technologies such as edge-cloud integration and 5G-enabled services. The region benefits from dense fiber-optic infrastructure, strong capital availability from REITs and institutional investors, and a well-established ecosystem of cloud, content, and enterprise customers.

U.S. Mega Data Center Market Trends

The mega data center market in the U.S. is expected to grow significantly at a CAGR of 3.5% from 2026 to 2033, due to the concentration of global hyperscale operators and the expansion of secondary data center markets beyond traditional hubs like Northern Virginia and Silicon Valley. Increasing demand for low-latency services is pushing development into Tier 2 and Tier 3 cities, supported by favorable state-level tax incentives and access to diverse energy grids.

Europe Mega Data Center Market Trends

The mega data center market in Europe is anticipated to register considerable growth from 2026 to 2033 due to stringent data privacy regulations such as GDPR, which are compelling organizations to localize data storage and processing within regional boundaries. This has led to increased investment in sovereign data infrastructure and regional cloud ecosystems.

The UK mega data center market is expected to grow rapidly in the coming years, owing to its role as a major financial and digital services hub, particularly centered around London. The increasing adoption of fintech, digital banking, and electronic trading platforms is generating substantial demand for secure, high-capacity data processing environments.

The mega data center market in Germany held a substantial market share in 2025 due to its strong industrial base and the rapid adoption of Industry 4.0 practices. Manufacturing enterprises are increasingly integrating automation, robotics, and industrial IoT, generating large volumes of operational data that require centralized processing and storage.

Asia Pacific Mega Data Center Market Trends

The mega data center market in the Asia Pacific held a significant share in the global market in 2025, due to rapid urbanization, expanding digital economies, and large-scale internet user bases across emerging markets. Governments and private sector players are heavily investing in digital infrastructure to support smart cities, digital payments, and e-governance initiatives.

Japan mega data center market is expected to grow rapidly in the coming years, driven by the need for disaster-resilient infrastructure due to the country’s exposure to natural risks such as earthquakes and typhoons. This has led to the development of highly robust, fault-tolerant mega data centers with advanced redundancy systems.

The mega data center market in China held a substantial market share in 2025, due to strong government-backed digital initiatives such as “Eastern Data, Western Computing,” which aims to optimize data processing by distributing workloads across regions. Massive domestic demand from e-commerce, digital platforms, and state-owned enterprises is also accelerating infrastructure development.

Key Mega Data Center Company Insights

Key players operating in the mega data center industry are Amazon Web Services (AWS), Microsoft Azure, Google Cloud Platform (GCP), Oracle Cloud, CyrusOne, Schneider Electric, and Vantage Data Centers. The companies are focusing on various strategic initiatives, including new product development, partnerships & collaborations, and agreements to gain a competitive advantage over their rivals. The following are some instances of such initiatives.

-

In January 2026, Vantage Data Centers entered into a strategic partnership with Liberty Energy Inc. to develop utility-scale, high-efficiency power solutions across Vantage’s growing data center portfolio in North America. As part of the agreement, the partners aim to deliver up to 1 gigawatt (GW) of power capacity over the next five years, including a reserved 400 megawatts (MW) scheduled for 2027, with additional expansion potential beyond 1GW to meet rising demand for scalable digital infrastructure.

-

In September 2025, Schneider Electric introduced a comprehensive liquid cooling portfolio developed in collaboration with Motivair, targeting high-performance computing (HPC) and AI-driven data center environments. The newly launched end-to-end solutions are designed for hyperscale, colocation, and high-density facilities, addressing the growing thermal management demands of next-generation workloads. By integrating advanced cooling technologies with dedicated services, the portfolio aims to improve energy efficiency, optimize performance, and support the development of future-ready “AI factories,” reinforcing the shift toward more sustainable and scalable digital infrastructure.

-

In July 2025, CyrusOne entered into a strategic 190-megawatt (MW) agreement with Calpine Corporation to power a new state-of-the-art data center in Bosque County, Texas. The upcoming facility, being developed near the Thad Hill Energy Center, will leverage secured power supply, grid connectivity, and land to support its operations. Currently under construction, the data center is expected to be operational by the fourth quarter of 2026, marking a significant step in CyrusOne’s expansion strategy to meet rising demand for scalable and energy-efficient digital infrastructure.

Key Mega Data Center Companies:

The following key companies have been profiled for this study on the mega data center market.

- Alibaba Cloud

- Amazon Web Services

- Baidu AI Cloud

- CyrusOne

- Digital Realty

- Equinix

- Google Cloud

- IBM Cloud

- Microsoft Azure

- NTT Ltd.

- Oracle Cloud Infrastructure

- QTS Realty Trust

- Schneider Electric

- Tencent Cloud

- Vantage Data Centers

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weakness

Mature Players: Amazon Web Services (AWS), Microsoft Azure, Google Cloud Platform (GCP), Oracle Cloud, CyrusOne, Schneider Electric, and Vantage Data Centers

- Building multi-gigawatt hyperscale campuses optimized for AI training, inference, and cloud scalability.

- Investing heavily in liquid cooling, direct-to-chip cooling, and renewable-powered infrastructure to support high-density AI racks.

- Expanding through long-term utility partnerships, land banking strategies, and vertically integrated infrastructure ecosystems, including networking, energy management, and edge connectivity.

- Massive capital reserves and established hyperscale customer bases enable the rapid deployment of large-scale campuses globally.

- Strong relationships with governments, utilities, telecom providers, and enterprise customers create high entry barriers for new competitors.

- Proven ability to operate mission-critical infrastructure with high uptime, advanced cybersecurity, global interconnection ecosystems, and scalable cloud platforms.

- Mega campus development requires extremely high capital expenditure and long construction cycles, limiting operational agility.

- Dependence on regional power availability and grid approvals can delay expansion projects and increase operational risk.

- Large organizational structures may slow the adoption of emerging technologies or innovative deployment models compared to smaller, agile competitors.

Emerging Players: CyrusOne, Baidu AI Cloud, Alibaba Cloud, QTS Realty Trust

- Developing AI-focused facilities with modular and scalable architectures that reduce deployment timelines.

- Targeting niche opportunities such as sovereign AI infrastructure, edge-integrated mega facilities, and sustainable carbon-neutral campuses.

- Leveraging flexible partnerships with renewable energy providers, GPU vendors, and regional telecom operators to accelerate market entry.

- Faster deployment capabilities and flexible design approaches enable rapid response to AI infrastructure demand spikes.

- Strong specialization in energy-efficient operations, modular construction, or regional hyperscale expansion creates differentiation from incumbents.

- Modern infrastructure designs optimized for GPU-intensive workloads provide advantages in supporting next-generation AI and HPC applications.

- Limited global footprint and smaller balance sheets reduce the ability to compete for massive hyperscale contracts.

- Heavy reliance on external financing and power procurement agreements can increase long-term operational vulnerability.

- Smaller interconnection ecosystems and fewer enterprise relationships may limit scalability compared to established hyperscale operators.

Mega Data Center Market Report Scope

Report Attribute

Details

Market size in 2025

USD 26.5 billion

Estimated market size in 2026

USD 27.3 billion

Projected market size by 2033

USD 36.7 billion

Growth rate

CAGR of 4.3% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Solution, data center type, cooling technology, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; Saudi Arabia; South Africa

Key companies profiled

Alibaba Cloud; Amazon Web Services; Baidu AI Cloud; CyrusOne; Digital Realty; Equinix; Google Cloud; IBM Cloud; Microsoft Azure; NTT Ltd.; Oracle Cloud Infrastructure; QTS Realty Trust; Schneider Electric; Tencent Cloud; Vantage Data Centers

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Mega Data Center Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global mega data center market report based on solution, data center type, cooling technology, and region:

-

Solution Outlook (Revenue, USD Billion, 2021 - 2033)

-

Storage

-

Networking

-

Server

-

Security

-

Others

-

-

Data Center Type Outlook (Revenue, USD Billion, 2021 - 2033)

-

Hyperscale Self-build

-

Hyperscale Colocation

-

-

Cooling Technology Outlook (Revenue, USD Billion, 2021 - 2033)

-

Air-Based Cooling

-

Liquid-Based Cooling

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Mega data center opportunity assessment for a hyperscale infrastructure provider

Assessment of mega data center demand across key regions and hyperscale clusters

Analysis of adoption trends for AI-ready infrastructure, high-density racks, liquid cooling, renewable-powered campuses, and modular deployments

Benchmarking of major operators, colocation providers, and infrastructure vendors based on capacity expansion, power efficiency, and technology integration

Identified high-growth mega data center investment hotspots

Supported infrastructure positioning and expansion strategy

Highlighted key growth drivers, power and land constraints, sustainability trends, and regulatory considerations

Customized cross-segmentation analysis for mega data centers by infrastructure type and end user

Conducted cross-segmentation analysis of mega data center infrastructure and end-user industries

Evaluated categories such as hyperscale cloud facilities, AI/HPC data centers, colocation mega campuses, edge-integrated mega facilities, and green data centers

Assessed demand across cloud providers, BFSI, government, telecom, healthcare, and AI enterprises

Identified high-adoption infrastructure models driving next-generation data center expansion

Highlighted end-user industries with the strongest hyperscale and AI compute demand

Supported strategic understanding of deployment differences across industries and regions

Mega data center, digital infrastructure, and market entry assessment for a technology and infrastructure vendor

Analysis of regional data center investments, power procurement trends, and land development strategies

Evaluation of operator requirements for AI compute scalability, energy efficiency, liquid cooling integration, and high-speed interconnectivity

Assessment of partnership ecosystems, including utilities, cloud providers, chipmakers, and construction firms

Identified attractive regional expansion opportunities for mega data center development

Supported GTM, partnership, and capacity expansion strategy

Enabled strategic entry into hyperscale cloud, AI infrastructure, and high-performance computing ecosystems

Frequently Asked Questions About This Report

The global mega data center market size was estimated at USD 26.52 billion in 2025 and is expected to reach USD 27.32 billion in 2026.

The global mega data center market is expected to grow at a compound annual growth rate of 4.3% from 2026 to 2033 to reach USD 36.70 billion in 2033.

The hyperscale self-build segment dominated the market and accounted for the largest revenue share in 2025 as large technology companies seek greater control over infrastructure design, cost structures, and long-term capacity planning. By developing and operating their own facilities, hyperscalers can customize architecture to align precisely with proprietary hardware, software stacks, and workload requirements, enabling tighter integration and optimized performance.

Key players operating in the mega data center industry are Amazon Web Services (AWS), Microsoft Azure, Google Cloud Platform (GCP), and Oracle Cloud, CyrusOne, Schneider Electric, and Vantage Data Centers.

The exponential growth of data generated from AI, machine learning, and high-performance computing (HPC) workloads contributes to the growth of the mega data center industry. Training and deploying large language models, computer vision systems, and real-time analytics platforms demand extremely dense compute environments with advanced cooling and power capabilities.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.