- Home

- »

- Next Generation Technologies

- »

-

Military Edge Computing Market Size, Growth Report, 2026-2033GVR Report cover

![Military Edge Computing Market (2026 - 2033)Report]()

Military Edge Computing Market (2026 - 2033)

Size, Share & Trends Analysis Report By Component (Hardware, Software, Services), By Platform (Land, Airborne, Naval, Space), By End Use (Intelligence, Surveillance, Reconnaissance (ISR)), By Region, And Segment Forecasts

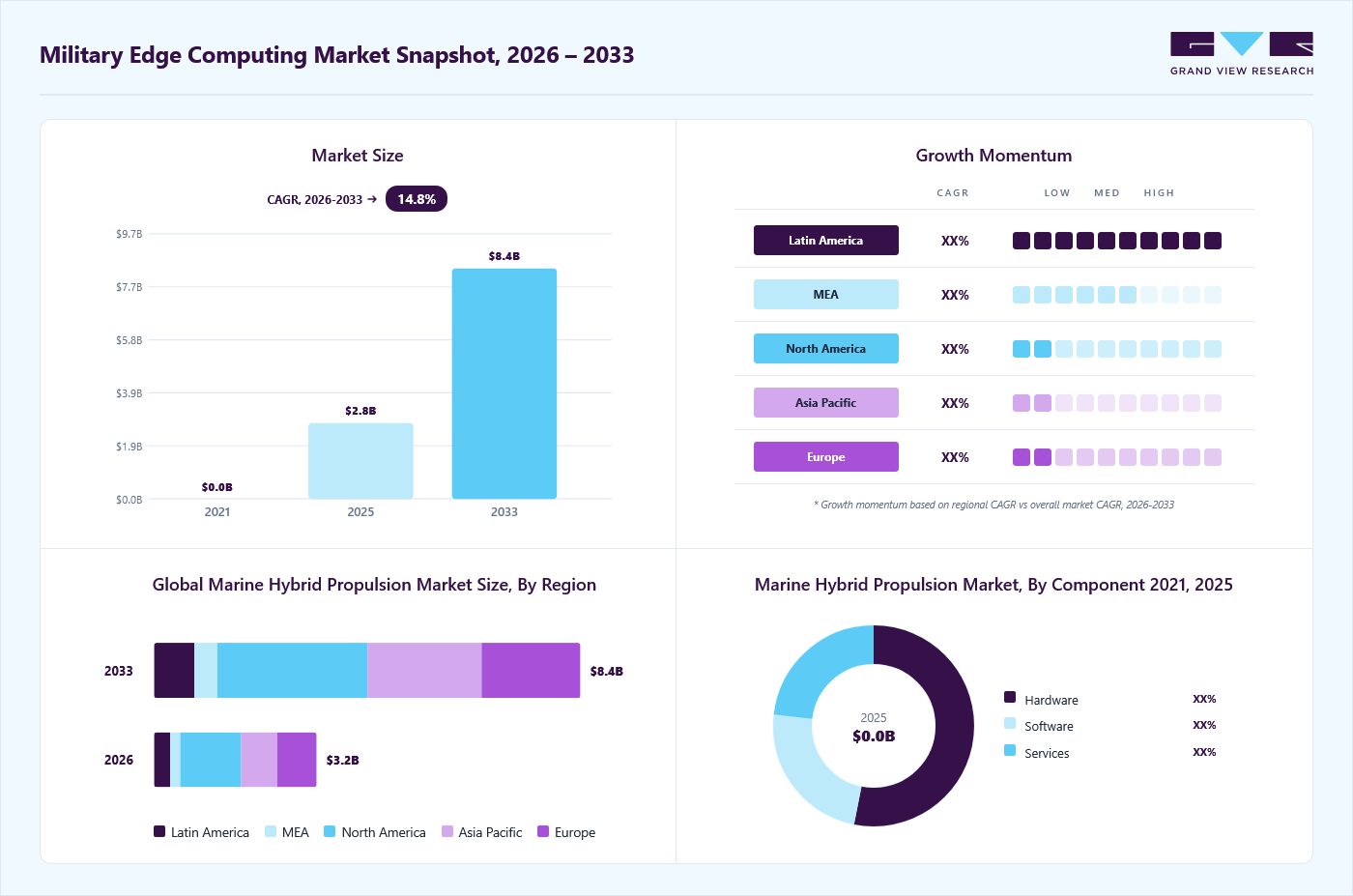

Market Size, 2025

$3.2BMarket Estimate, 2026

$3.7BMarket Forecast, 2033

$9.7BCAGR, 2026–2033

14.9%Military Edge Computing Market Summary

The global military edge computing market size was valued at USD 3.2 billion in 2025 and is projected to grow from USD 3.7 billion in 2026 to USD 9.7 billion by 2033, at a CAGR of 14.9% from 2026 to 2033. North America dominated the global market, accounting for the largest revenue share of 37.4% in 2025. The market is expanding due to increasing demand for real-time data processing in mission-critical defense operations.

Key Market Trends & Insights

- By component: Hardware led the market with the largest revenue share of 52.3% in 2025.

- By platform: Land held the largest revenue share of 50.3% in 2025.

- By end use: Cybersecurity segment is expected to grow at the fastest CAGR of 17.1% from 2026 to 2033.

Regional Highlights

- Largest regional market: North America (37.4% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. military edge computing industry is a major contributor to the global market.

Market Size & Forecast

- Market size in 2025: USD 3.2 Billion

- Estimated market size in 2026: USD 3.7 Billion

- Projected market size by 2033: USD 9.7 Billion

- CAGR (2026-2033): 14.9%

Rising adoption of AI-enabled systems is accelerating the need for edge-based analytics and decision-making capabilities. The growing deployment of autonomous platforms is further driving demand for localized, high-performance computing. The demand for rugged, AI-enabled edge computing systems in the military edge computing industry is increasing across defense environments. These military edge computing systems support real-time data processing and operate in extreme battlefield conditions. AI-powered edge computing is enhancing decision-making speed and situational awareness in mission-critical operations. The growing use of autonomous defense systems and edge AI infrastructure is driving the adoption of secure, low-latency edge computing solutions. For instance, in April 2025, Advantech Co., Ltd., an industrial technology and embedded computing company, launched the ROCK-301 as a rugged, fanless IP65 edge computer designed for mission-critical and defense applications operating in extreme environments. The system supports AI module expansion, meets MIL-STD certifications, and delivers high-performance edge computing with durability for harsh operational conditions.

")

The market is shifting toward rugged, high-performance edge AI computing platforms designed for mission-critical and harsh environments. These platforms integrate advanced AI accelerators with embedded computing architectures to support autonomous and data-intensive workloads. Adoption is expanding across defense, aerospace, robotics, and industrial automation, driven by demand for low-latency, on-device intelligence and secure edge operations. Companies are increasingly launching AI-enabled edge computing solutions to strengthen real-time performance and operational efficiency. For instance, in March 2026, Forecr.io, A hardware and embedded computing company focused on Edge AI systems, launched five new MIL-grade edge AI platforms powered by NVIDIA Jetson Thor and Jetson AGX Orin for industrial and defense applications. The MILBOX-THR system delivers high AI performance with a rugged design, supporting real-time autonomy, sensor fusion, and advanced edge processing in harsh environments.

Military systems are increasingly adopting AI-enabled decision support at the edge to process large volumes of real-time battlefield data. These systems integrate AI algorithms into vehicles, drones, and sensor platforms. This enables rapid analysis of threats and operational conditions without relying on centralized cloud infrastructure. Edge AI computing reduces latency in critical decision-making processes. It enhances situational awareness for commanders in dynamic environments. Predictive analytics supports better anticipation of enemy movements and system failures. The capability improves mission responsiveness in contested or communication-denied environments. AI-driven insights are being embedded into command and control systems to enable faster coordination. This shift strengthens operational efficiency and battlefield effectiveness.

Component Insights

The hardware segment dominated the military edge computing industry in 2025, accounting for a 52.3% share, due to strong demand for rugged and high-performance computing systems. Defense applications require specialized edge hardware capable of operating in extreme environmental and combat conditions. Increasing deployment of AI-enabled platforms is driving demand for advanced processors, GPUs, and embedded systems. Military modernization programs are accelerating hardware procurement for edge deployments across defense forces. Growing use of autonomous systems and real-time data processing is further strengthening hardware adoption. Continuous advancements in rugged and energy-efficient computing systems are further supporting deployment in harsh environments.

The software segment is growing due to rising demand for AI-driven applications, edge analytics, and secure military data management solutions. Defense organizations are adopting software-defined architectures to enable faster and more flexible mission execution. Integration of artificial intelligence and machine learning is enhancing real-time decision-making at the edge. Increasing focus on cybersecurity software solutions is supporting the protection of sensitive defense data. Cloud-enabled and hybrid deployment models that enable scalable, interoperable military operations. Continuous innovation in modular and interoperable software platforms is further accelerating adoption across defense systems.

Platform Insights

The land segment dominated the military edge computing market in 2025, due to widespread deployment across ground-based defense systems, armored vehicles, forward operating bases, and battlefield command centers. It supports real-time data processing, secure communication, and rapid decision-making in mission-critical environments. Strong integration of AI-enabled edge devices and rugged computing systems enhances situational awareness and operational efficiency. Continuous modernization of land forces and increasing adoption of network-centric warfare technologies further strengthen its dominant position. The growing deployment of autonomous ground systems and connected battlefield networks is also supporting sustained demand.

The space segment is growing as defense organizations increasingly rely on satellites and space-based platforms for intelligence, surveillance, and reconnaissance. Edge computing enables onboard data processing, reducing latency and dependence on ground stations. Rising investments in space defense infrastructure and secure satellite communication systems are accelerating adoption. The increasing demand for real-time analytics in orbital platforms is also driving the expansion of this segment. Advancements in AI-enabled satellite systems and space-based autonomy are further driving growth.

End Use Insights

The Intelligence, Surveillance, and Reconnaissance (ISR) segment dominated the military edge computing market in 2025, due to its critical role in enabling real-time situational awareness, threat detection, and mission planning across defense operations. It relies heavily on edge computing to process large volumes of sensor, satellite, and battlefield data closer to the source, reducing latency and improving decision accuracy. Continuous modernization of defense systems and increasing deployment of AI-enabled ISR platforms further strengthen its dominant position. Growing emphasis on rapid battlefield intelligence and secure communication also supports sustained demand for ISR capabilities. Increasing integration of autonomous ISR systems and advanced analytics is further enhancing operational efficiency and mission effectiveness.

The cybersecurity segment is growing as defense organizations face increasing risks from advanced cyber threats targeting military networks and connected systems. Edge computing enhances cybersecurity by enabling real-time threat detection, localized data protection, and faster response to attacks. The rising adoption of cloud-edge hybrid defense architectures and the increasing focus on securing distributed battlefield systems are driving demand. The expanding digitalization of military infrastructure and growing reliance on connected devices further support the growth of cybersecurity applications. Continuous advancements in AI-driven threat intelligence and zero-trust security frameworks are further strengthening this segment.

Regional Insights

North America led the military edge computing market, with the largest global share of 37.4% in 2025, driven by strong defense spending and early adoption of advanced military technologies. The region benefits from extensive integration of AI, edge computing, and secure communication systems across defense operations. The presence of major defense contractors and the continuous modernization of military infrastructure further support its dominant position. Increasing deployment of autonomous systems and AI-driven defense platforms is further reinforcing regional demand.

U.S. Military Edge Computing Market Trends

The U.S. military edge computing industry is driven by increasing defense modernization programs and strong investment in advanced digital battlefield technologies. Rising adoption of AI-enabled edge systems supports real-time data processing, faster decision-making, and improved situational awareness across military operations. Growing cybersecurity threats are pushing demand for secure, decentralized computing architectures.

Europe Military Edge Computing Market Trends

The Europe military edge computing industry is growing due to increasing focus on strengthening defense capabilities and enhancing real-time battlefield intelligence. Rising adoption of AI-driven edge systems supports faster data processing and improved operational coordination across military units. Increasing investments in secure communication infrastructure and defense modernization programs are further driving demand.

Asia Pacific Military Edge Computing Market Trends

The Asia Pacific military edge computing industry is expected to grow at the fastest CAGR during the forecast period. This growth is driven by rapid defense modernization and the rising adoption of advanced digital battlefield technologies across the region. Increasing investment in AI-enabled edge systems supports real-time intelligence, surveillance, and faster decision-making in complex operational environments. Growing geopolitical tensions are further accelerating demand for secure and low-latency defense communication networks.

Key Military Edge Computing Company Insights

Some of the key companies in the Military Edge Computing industry include Amazon Web Services, Inc., Intel Corporation, Parry Labs, RTX Corporation (Raytheon Technologies), and Thales Group. Organizations are focusing on increasing their customer base to gain a competitive edge in the industry. Therefore, key players are taking several strategic initiatives, such as mergers and acquisitions, and partnerships with other major companies.

-

Intel Corporation is advancing military edge computing through high-performance processors, AI accelerators, and secure computing platforms designed for real-time battlefield data processing. Its technologies support edge AI workloads in defense systems, enabling faster decision-making, enhanced situational awareness, and efficient handling of sensor and surveillance data. Intel is also focusing on rugged, energy-efficient chipsets that can operate in harsh, contested environments.

-

Parry Labs is developing modular edge computing and digital engineering solutions for defense applications, with a strong focus on autonomous systems and mission-ready platforms. It provides software-defined infrastructure that integrates AI, command and control, and edge processing for rapid deployment in military environments. The company emphasizes interoperability and scalability to support connected battlefield operations and real-time mission execution.

Key Military Edge Computing Companies:

The following key companies have been profiled for this study on the military edge computing market.

- Amazon Web Services, Inc.

- BAE Systems

- Cisco Systems, Inc.

- General Dynamics

- Intel Corporation

- Lockheed Martin

- Northrop Grumman

- Parry Labs

- RTX Corporation (Raytheon Technologies)

- Thales Group

Recent Developments

-

In March 2026, Cincoze, a Taiwan-based industrial computing company, launched the DX-1300 high-performance compact industrial computer as an edge computing platform designed for space-constrained environments. It supports AI inference, real-time image processing, and data integration with Intel Core Ultra processors, delivering high compute performance in a compact, rugged design suitable for industrial and edge AI applications.

-

In November 2025, General Dynamics Information Technology, an IT service management company, expanded its collaboration with Google Public Sector to develop secure AI, cloud, and cyber solutions for defense and government agencies. This collaboration focuses on delivering mission-edge AI capabilities using Google Distributed Cloud to support real-time decision-making in disconnected and tactical environments.

-

In October 2025, Shield AI, an Aerospace and defense company, and Parry Labs announced a partnership to integrate Shield AI’s Hivemind autonomy software with Parry Labs’ STRATIA edge computing and mission systems to enhance autonomous operations in contested environments. The partnership aims to deliver interoperable, AI-enabled edge solutions that enhance speed, resilience, and decision-making for military platforms operating in GPS- and communication-denied conditions.

Military Edge Computing Market Report Scope

Report Attribute

Details

Market size in 2025

USD 3.2 billion

Estimated Market size in 2026

USD 3.7 billion

Projected Market size by 2033

USD 9.7 billion

Growth rate

CAGR of 14.9% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive sector, growth factors, and trends

Segment scope

Component, platform, end use, and region

Region scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; Japan; India; Australia; South Korea; Brazil; KSA; UAE; South Africa

Key companies profiled

Amazon Web Services, Inc.; BAE Systems; Cisco Systems, Inc.; General Dynamics; Intel Corporation; Lockheed Martin; Northrop Grumman; Parry Labs; RTX Corporation (Raytheon Technologies); Thales Group

Customization scope

Free report customization (equivalent up to 8 analysts’ working days) with purchase. Addition or alteration to country, regional & segment scope

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Military Edge Computing Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends and opportunities in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global military edge computing market report based on component, platform, end use, and region:

-

Component Outlook (Revenue, USD Billion, 2021 - 2033)

-

Hardware

-

Software

-

Services

-

-

Platform Outlook (Revenue, USD Billion, 2021 - 2033)

-

Land

-

Airborne

-

Naval

-

Space

-

-

End Use Outlook (Revenue, USD Billion, 2021 - 2033)

-

Intelligence, Surveillance, and Reconnaissance (ISR)

-

Command and Control (C2)

-

Cybersecurity

-

Autonomous Systems (UGVs/UAVs)

-

Weapon Systems

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

Australia

-

South Korea

-

-

Latin America

-

Brazil

-

-

Middle East & Africa (MEA)

-

KSA

-

UAE

-

South Africa

-

-

Frequently Asked Questions About This Report

Asia Pacific is the fastest-growing region over the forecast period.

The hardware segment led with a 52.3% revenue share in 2025.

Land segment dominated the market and accounted for the largest revenue share 50.3% in 2025.

The intelligence, surveillance, and reconnaissance (ISR) segment held the largest revenue share in 2025.

The global military edge computing market size was valued at USD 3.2 billion in 2025 and is estimated at USD 3.7 billion for 2026.

The global military edge computing market is expected to grow at a CAGR of 14.9% from 2026 to 2033, reaching USD 9.7 billion by 2033.

North America dominated the military edge computing market with a share of 37.4% in 2025. This is attributable to high defense spending, advanced technological infrastructure, and early adoption of edge computing solutions in military operations.

Key players include Amazon Web Services, Inc.; BAE Systems; Cisco Systems, Inc.; General Dynamics; Intel Corporation; Lockheed Martin; Northrop Grumman; Parry Labs; RTX Corporation (Raytheon Technologies); Thales Group.

Key factors that are driving the market growth include increasing adoption of advanced technologies, rising demand for real-time data processing, expansion of connected devices, and growing investment in digital infrastructure.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.