- Home

- »

- HVAC & Construction

- »

-

Mining Drilling Services Market Size, Share Report 2026-2033GVR Report cover

![Mining Drilling Services Market (2026 - 2033)Report]()

Mining Drilling Services Market (2026 - 2033)

Size, Share & Trends Analysis Report By Service Type (Surface Drilling, Underground Drilling, Directional Drilling), By Mining Method (Open-Pit Mining, Underground Mining), By Application (Coal Mining, Mineral Mining), By Region, And Segment Forecasts

Market Size, 2025

$3.4BMarket Estimate, 2026

$3.5BMarket Forecast, 2033

$5.3BCAGR, 2026–2033

6.1%Mining Drilling Services Market Summary

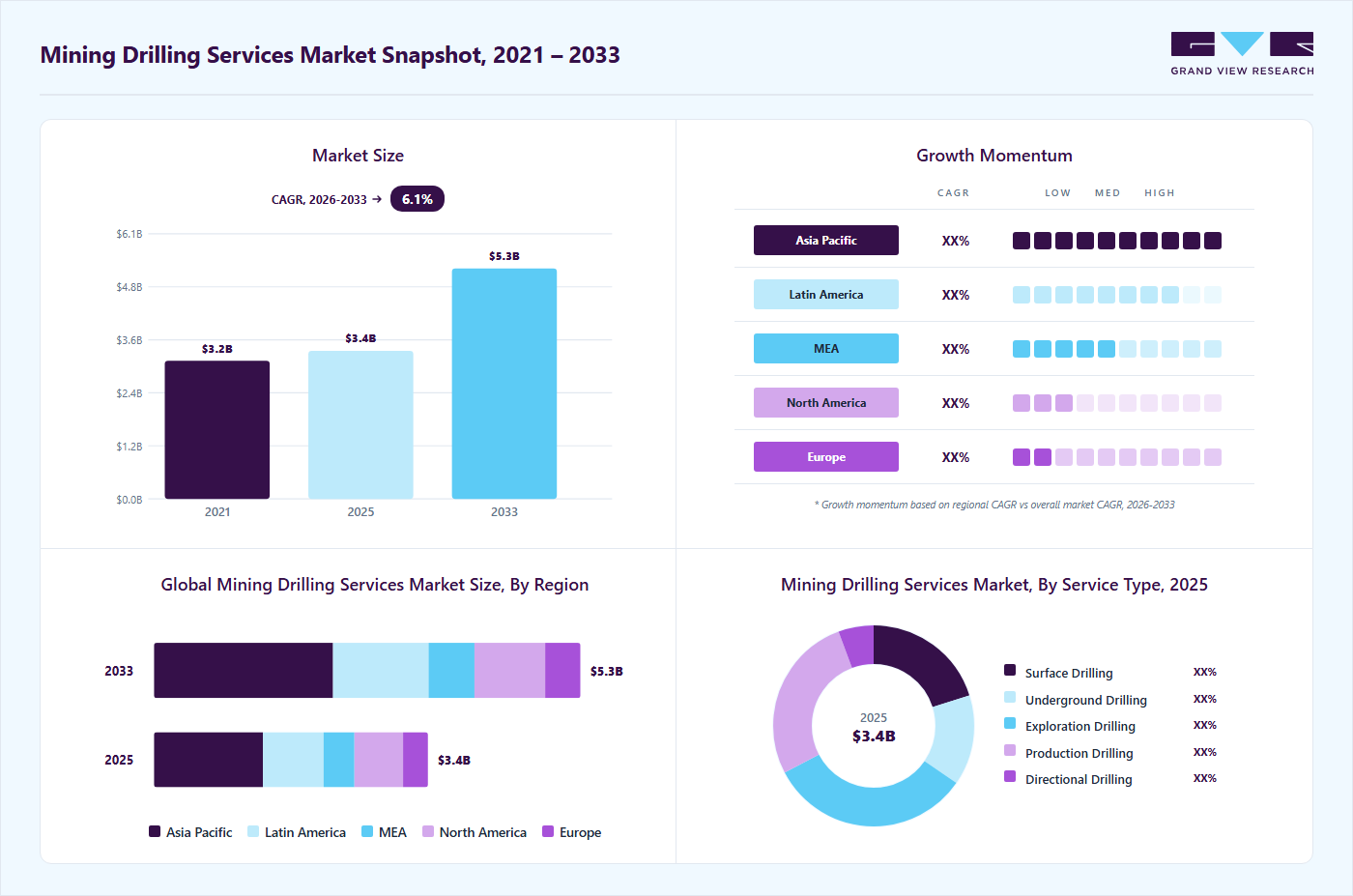

The global mining drilling services market size was estimated at USD 3.4 billion in 2025 and is projected to grow from USD 3.5 billion in 2026 to USD 5.3 billion by 2033, at a CAGR of 6.1% from 2026 to 2033. Asia Pacific held the largest market share of 39.8% in 2025. The major factor expected to drive the industry is the systematic decline in global ore grades, which directly increases drilling intensity per unit of output.

Key Market Trends & Insights

- By service type: Exploration drilling segment held the largest market share of 32.6% in 2025.

- By mining method: Open-pit mining segment held the largest market share in 2025.

- By application: Metal mining segment dominated the market in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (39.8%, share)

- By Country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 3.4 Billion

- Estimated market size in 2026: USD 3.5 Billion

- Projected market size by 2033: USD 5.3 Billion

- CAGR (2026–2033): 6.1%

As high-grade deposits are depleted, mining companies are forced to process larger volumes of material to extract the same quantity of metal, requiring significantly more drilling for both exploration and production. Another major factor expected to drive the market growth is the progressive migration of mining operations toward deeper, geologically complex, and remote deposits. As near-surface resources decline, mining companies are increasingly targeting underground reserves, narrow veins, and structurally complex ore bodies. These environments require significantly more specialized drilling techniques, such as directional drilling, long-hole drilling, and geotechnical drilling. Deep mining introduces challenges such as high temperature, pressure conditions, and rock stress, which increase the technical complexity and frequency of drilling operations. This results in higher demand for contract drilling specialists with advanced equipment and expertise.

Also, complex geology increases uncertainty, necessitating continuous exploratory and delineation drilling even during production phases. Unlike traditional deposits, these reserves require dynamic drilling strategies, increasing service intensity over time. Remote locations (e.g., Arctic, deep desert, offshore, or high-altitude regions) further reinforce outsourcing to drilling service providers due to logistical and operational constraints. This reduces the feasibility of in-house drilling capabilities for mining companies. These drivers lead to higher revenue per meter drilled, increased contract durations, and greater reliance on specialized service providers, resulting in increasing market growth.

")

Additionally, drilling demand is inherently volatile across the mine lifecycle (exploration vs. production phases). Outsourcing allows mining companies to scale drilling activity up or down without asset underutilization risks. Service providers, on the other hand, benefit from asset utilization across multiple projects and geographies, creating economies of scale that mining companies cannot achieve individually. This reinforces the structural advantage of third-party drilling services, ultimately the positive impacting in the market growth.

Moreover, rigs and associated equipment operate under continuous, high-load conditions, resulting in rapid wear and frequent maintenance requirements. This directly drives demand for mining drilling equipment and MRO services, as uptime of drilling operations is critical to overall mine productivity. Since drilling is the first operational step in blasting and extraction, any disruption creates a cascading impact across the value chain.

The harsh geological environment, especially in hard rock mining, further accelerates component degradation, reinforcing recurring service demand. As a result, operators prioritize preventive and predictive maintenance within the mining drilling market to avoid costly downtime. This creates a steady, non-cyclical demand stream for MRO services, tightly integrated with drilling activity levels rather than equipment sales cycles.

Market Dynamics

The increasing shift toward deeper, lower-grade, and geologically complex ore deposits is a key driver of growth in the mining drilling service industry. As easily accessible, high-grade mineral reserves continue to deplete globally, mining companies are increasingly forced to target underground, narrow-vein, and structurally complex ore bodies. This transition significantly increases drilling intensity, as more drilling is required for exploration, resource delineation, and production planning to ensure economic viability of mining operations.

These complex geological conditions require advanced drilling techniques such as directional drilling, geotechnical drilling, and long-hole drilling, which further increases service demand. Deep mining environments also introduce operational challenges such as high pressure, elevated temperatures, and unstable rock formations, necessitating more frequent and specialized drilling interventions. As a result, mining companies increasingly rely on specialized drilling service providers with advanced rigs, technical expertise, and adaptive drilling technologies to maintain operational efficiency and safety.

High operational costs and cyclical volatility in mining investments are restraining the growth of the mining drilling service industry by creating financial uncertainty and limiting long-term drilling commitments. Mining drilling operations require significant capital expenditure on rigs, skilled labor, fuel, logistics, and maintenance, all of which contribute to high service costs. In addition, fluctuating commodity prices directly influence mining exploration and production budgets, leading to periodic slowdowns or delays in drilling activities.

The expansion of deep mining projects, remote resource development, and rising demand for critical minerals is creating significant growth opportunities for the mining drilling service industry. The global transition toward renewable energy, electric vehicles, and advanced manufacturing is driving strong demand for minerals such as lithium, copper, nickel, and cobalt, leading to increased exploration and development activities worldwide.

To meet this demand, mining companies are increasingly investing in new exploration projects in previously untapped or remote regions, including deep underground deposits and geologically challenging terrains. These projects require intensive and continuous drilling services for resource identification, grade control, and mine development planning. As a result, drilling service providers are benefiting from longer project cycles and higher drilling intensity per site.

Market Concentration & Characteristics

The mining drilling service industry is moderately fragmented, with a strong presence of global drilling contractors alongside a large number of regional and niche service providers. The competitive landscape includes multinational mining service companies, specialized drilling contractors, and equipment-linked service providers that collectively cater to exploration, production, surface, and underground drilling requirements across diverse geological environments. While leading players dominate large-scale, long-duration mining projects, particularly in metal-rich and high-volume mining regions, a significant share of the market is still served by small and mid-sized contractors operating at the regional or project-specific level.

Fragmentation is particularly evident in the service-type landscape, where companies specialize in distinct drilling activities such as exploration drilling, production drilling, directional drilling, surface drilling, and underground drilling. This specialization allows service providers to target specific phases of the mining lifecycle and adapt to varying geological conditions, ore types, and operational complexities.

Service Type Insights

The exploration drilling segment accounted for the largest share of 32.61% in 2025. The global surge in demand for critical minerals and metals is fueling the growth of the segment. The clean energy transition fuels an unprecedented need for materials such as lithium, copper, cobalt, nickel, and rare earth elements, which are essential for electric vehicle (EV) batteries, wind turbines, solar panels, and other green technologies. As accessible reserves of these minerals become depleted, mining companies are investing heavily in exploration to discover new deposits.

The directional drilling segment is expected to grow at a significant CAGR of 6.5% from 2026 to 2033. The cost efficiency and operational flexibility drive the growth of the segment. However, initially more capital-intensive, directional drilling can lead to significant long-term cost savings by reducing the need for multiple drill pads, minimizing excavation, and improving ore targeting accuracy. In addition, the ability to drill multiple intersecting holes from a single location offers operational flexibility, enabling better resource estimation and planning. This efficiency is particularly beneficial in exploration and pre-feasibility studies.

Mining Method Insights

The open-pit mining segment held the largest market share in 2025. High productivity and scalability drive the growth of the segment. Open-pit mining enables large-scale extraction of mineral resources, allowing for high-volume output. It facilitates the use of heavy-duty drilling and excavation equipment, which significantly boosts productivity. The method is also highly scalable, making it suitable for both short-term and long-term mining projects. The scalability and ability to handle massive volumes of overburden and ore contribute to sustained demand for surface drilling services such as blast hole drilling and production drilling.

The underground mining segment is expected to grow at the fastest CAGR during the forecast period. Access to high-value and deep ore deposits fuels the growth of the market. Underground mining enables access to deep-seated and high-value deposits, including gold, copper, zinc, nickel, and rare earth elements. Many of these deposits are located at depths that are impractical or uneconomical to exploit through open-pit mining. With directional and long-hole drilling techniques, underground operations can extract these resources more efficiently. This growing demand for deeper resource extraction directly fuels the need for advanced underground drilling services.

Application Insights

The metal mining segment dominated the market in 2025. The increasing global consumption of base metals such as copper, zinc, nickel, and aluminum, along with precious metals such as gold and silver, is driving the growth of the market. These metals are critical to infrastructure development, electrical grids, manufacturing, and consumer electronics. In addition, copper and nickel are vital components in electric vehicles (EVs), batteries, and renewable energy systems. As demand surges across industrial and clean energy sectors, mining companies are ramping up drilling efforts to locate and extract new metal reserves, directly boosting the need for drilling services.

The mineral mining segment is projected to grow at a significant CAGR over the forecast period. The growing global demand for agricultural fertilizers, particularly those based on phosphate and potash, fuels the growth of the market. As the global population increases and food security becomes a central concern, countries are investing in enhancing agricultural productivity. This drives the need for large-scale extraction of fertilizer-grade minerals, requiring exploration and production drilling in mineral-rich areas such as Canada, Russia, and Morocco. Drilling services are essential for discovering new reserves and expanding existing operations to meet the rising demand.

Regional Insights

The North America mining drilling service market accounted for 17.75% market share in 2025. The mining drilling service market in North America is driven by robust exploration and production activities, particularly in metal and mineral mining. The region is home to significant reserves of copper, gold, and lithium, which are in high demand for renewable energy technologies and electric vehicles.

U.S. Mining Drilling Service Market Trends

The mining drilling service market in the U.S. held a dominant position in 2025 due to the renewed interest in domestic mining to reduce reliance on imported critical minerals such as rare earth elements, lithium, and copper. Government-backed initiatives aimed at strengthening supply chains for energy transition materials are encouraging greater investment in mineral exploration.

Europe Mining Drilling Service Market Trends

The mining drilling service industry in Europe was identified as a lucrative region in 2025. The growth in the region is driven by increasing demand for strategic minerals needed in green energy and digital technologies. The European Union’s push for raw material security and sustainable mining practices has opened up new opportunities for drilling service providers.

The UK mining drilling service market is expected to grow rapidly in the coming years. In the UK, the focus on critical mineral exploration, such as lithium in Cornwall and rare earths in Scotland, is creating new demand for drilling services. As part of its net-zero goals, the UK is supporting domestic resource development to supply the battery and green technology sectors.

The mining drilling service industry in Germany held a substantial market share in 2025. Germany is intensifying its efforts to secure critical minerals for its high-tech and automotive industries, which is driving investment in domestic and nearby mineral exploration. The country is also looking at repurposing former coal mining regions for rare earth and lithium extraction, creating opportunities for drilling contractors.

Asia Pacific Mining Drilling Services Market Trends

The mining drilling service market in Asia Pacific is anticipated to grow at a CAGR during the forecast period. The market is experiencing growth in the region due to expanding mining activities across both developed and developing nations. The region is a major global hub for coal, base metals, and industrial minerals, with substantial investments being made in exploration and mine development.

The India mining drilling service industry is expected to grow rapidly in the coming years. India’s mining drilling services market is expanding steadily, supported by government initiatives to enhance domestic mineral production. The Make in India and Atmanirbhar Bharat programs are encouraging investment in mining projects for coal, bauxite, and rare earth elements.

The mining drilling service market in China held a substantial share in 2025 due to its extensive mining industry and strong demand for minerals used in electronics, EVs, and construction. The country is a global leader in the production of rare earths, coal, and base metals, requiring continuous drilling activities for exploration and resource replenishment.

Key Mining Drilling Services Company Insights

Some of the key companies in the mining drilling service market include Boart Longyear, Sandvik AB, Ausdrill, Major Drilling, and others. Organizations are focusing on increasing their customer base to gain a competitive edge in the industry. Therefore, key players are taking several strategic initiatives, such as mergers and acquisitions, and partnerships with other major companies.

-

Boart Longyear is a drilling services company, providing productivity-driven drilling equipment and performance tooling for the mining and drilling industries. With operations in 26 countries, the company serves customers on every continent, spanning commodities such as copper, gold, nickel, zinc, uranium, iron, and more. The company is known for its integrated exploration services, surface and underground coring, pump and rotary services, and advanced drilling technology, such as the revolutionary Q Wireline System. The company combines innovative engineering, decades of field expertise, and a commitment to safety and sustainability to support the world’s most challenging mineral exploration and development projects.

-

Sandvik AB is a global, high-tech engineering company specializing in providing innovative solutions that enhance profitability, productivity, and sustainability across the manufacturing, mining, and construction industries. It has operations in around 150 countries. It develops and manufactures cutting tools, mining equipment, tooling systems, advanced materials, and digital solutions aimed at improving operational efficiency and environmental performance.

Key Mining Drilling Services Companies:

The following key companies have been profiled for this study on the mining drilling services market.

- Boart Longyear

- Sandvik AB

- Ausdrill

- Major Drilling

- Foraco International SA

- Orbit Garant Drilling Inc.

- Action Drill & Blast

- SWICK MINING SERVICES

- Drillcon Group

- Geodrill

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: Boart Longyear; Sandvik AB; Major Drilling; Foraco International SA

- Mature players focus on delivering comprehensive mining drilling services across exploration, production, directional, surface, and underground drilling operations for large-scale mining projects.

- They emphasize investment in advanced drilling technologies, automation-enabled drilling rigs, digital monitoring systems, and safety-focused operational practices to improve drilling efficiency and reduce downtime.

- Strong global operational footprint with extensive experience across diverse mining environments and commodities.

- Advanced drilling equipment fleets and technical expertise supporting deep-hole, complex, and high-precision drilling operations.

- Strong global operational footprint with extensive experience across diverse mining environments and commodities.

- Advanced drilling equipment fleets and technical expertise supporting deep-hole, complex, and high-precision drilling operations.

Emerging Players: Ausdrill; Orbit Garant Drilling Inc.; Action Drill & Blast; SWICK MINING SERVICES; Drillcon Group; Geodrill

- Emerging and challenger players focus on specialized drilling services including underground drilling, blast hole drilling, exploration drilling, and region-specific contract drilling solutions.

- Strategies emphasize operational flexibility, cost-efficient service delivery, rapid deployment capabilities, and adoption of modern drilling technologies for mid-sized mining operators.

- Strong specialization in niche drilling applications and regional mining markets.

- Agile operational models enabling faster project execution and customized drilling solutions.

- Limited global scale and smaller drilling equipment fleets compared to established multinational competitors.

- Lower bargaining power in securing long-term contracts with large mining corporations.

Recent Developments

-

In May 2025, ArcelorMittal Mining Canada partnered with Sandvik Mining to enhance its rotary drilling fleet at its Mont-Wright iron ore mining complex in Québec. The agreement involves the supply of four advanced Sandvik DR412i rotary blasthole drills, with the first two already delivered and the remaining two scheduled by the end of Q3 2025. These intelligent drills, capable of both rotary and down-the-hole drilling, offer improved productivity through drilling depths of up to 75.5 meters and feature real-time operator feedback, advanced safety measures, and a centralized service center to streamline maintenance and reduce environmental impact.

-

In February 2024, Ausdrill, a drilling services provider, established a strategic alliance with SITECH WA, a technology solutions specialist for mining processes in Western Australia. This collaboration sees SITECH WA's Trimble Groundworks machine guidance technology integrated into Ausdrill's Rock Commander fleet, representing a substantial leap in mining safety, precision, and operational efficiency. Together, the two companies aim to redefine industry standards in these areas, propelling the mining sector forward with advanced technological innovations.

Mining Drilling Services Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 3.4 billion

Estimated Market size in 2026

USD 3.5 billion

Projected Market size by 2033

USD 5.3 billion

Growth rate

CAGR of 6.1% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report mining method

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Service type, mining method, application, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; Japan; India; South Korea; Australia; Brazil; KSA; UAE; South Africa

Key companies profiled

Boart Longyear; Sandvik AB; Ausdrill; Major Drilling; Foraco International SA; Orbit Garant Drilling inc.; Action Drill & Blast; SWICK MINING SERVICES; Drillcon Group; Geodrill

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Mining Drilling Services Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global mining drilling services market report based on service type, mining method, application, and region

-

Service Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Surface Drilling

-

Underground Drilling

-

Exploration Drilling

-

Production Drilling

-

Directional Drilling

-

-

Mining Method Outlook (Revenue, USD Million, 2021 - 2033)

-

Open-Pit Mining

-

Underground Mining

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Coal Mining

-

Metal Mining

-

Mineral Mining

-

Quarrying and Aggregates

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East and Africa (MEA)

-

KSA

-

UAE

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Mining Drilling Services Market Opportunity Assessment

- Country/region-wise autonomous network market sizing and growth forecasts across North America, Europe, Asia Pacific, Latin America, and Middle East & Africa

- Assessment of regulatory frameworks impacting autonomous networks (data privacy laws, AI governance policies, telecom automation standards.

- Identified region-specific growth opportunities in expanding mineral exploration and large-scale mining projects

- Supported mining contractors and drilling service providers in targeting high-growth commodity and infrastructure development markets

Mining Drilling Technology & Operational Behavior Study

- Analysis of mining company adoption patterns for advanced drilling technologies and outsourced drilling services across coal, metal, and mineral mining sectors

- Evaluation of operational preferences including automated drilling systems, directional drilling technologies, and sustainable drilling practices.

- Improved segmentation of drilling service demand by mining method, commodity type, and operational scale

- Supported service providers in positioning technologically advanced and cost-efficient drilling solutions

Competitive Benchmarking and Strategic Positioning in the Mining Drilling Services Market

- Benchmarking of key market players across drilling fleet capabilities, exploration expertise, safety standards, automation integration, and geographic presence

- Comparative assessment of partnerships with mining companies, equipment manufacturers, and resource exploration firms

- Identified competitive white spaces in specialized drilling services, deep exploration projects, and technologically advanced drilling solutions

- Supported strategic expansion planning, partnership development, and regional market entry strategies

Frequently Asked Questions About This Report

Some key players operating in the mining drilling service market include Boart Longyear; Sandvik AB; Ausdrill; Major Drilling; Foraco International SA; Orbit Garant Drilling inc.; Action Drill & Blast; SWICK MINING SERVICES; Drillcon Group; Geodrill.

The mining drilling services market is witnessing steady growth, driven primarily by the rising global demand for minerals, metals, and rare earth elements essential to industries such as construction, electronics, automotive, and renewable energy.

The global mining drilling service market size was estimated at USD 3.39 billion in 2025 and is expected to reach USD 3.48 billion in 2026.

The global mining drilling service market is expected to grow at a compound annual growth rate of 6.1% from 2026 to 2033 to reach USD 5.27 billion by 2033.

Asia Pacific dominated the mining drilling service market with a share of 39.77% in 2025. The market is experiencing growth in the region due to expanding mining activities across both developed and developing nations.

About the Author(s)

HVAC & Construction Research Team

Technology · HVAC & ConstructionThis report was authored by the hvac & construction research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the hvac & construction segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.