- Home

- »

- Advanced Interior Materials

- »

-

Copper Market Size, Share And Growth Report, 2026-2033GVR Report cover

![Copper Market (2026 - 2033)Report]()

Copper Market (2026 - 2033)

Size, Share & Trends Analysis Report By Type (Primary Copper, Secondary Copper), By Product (Wire, Tube, Foil, Flat Rolled Products), By End Use (Industrial Equipment, Transport, Infrastructure), By Region, And Segment Forecasts

Market Size, 2025

$248.2BMarket Estimate, 2026

$260.2BMarket Forecast, 2033

$388.8BCAGR, 2026–2033

5.9%Copper Market Summary

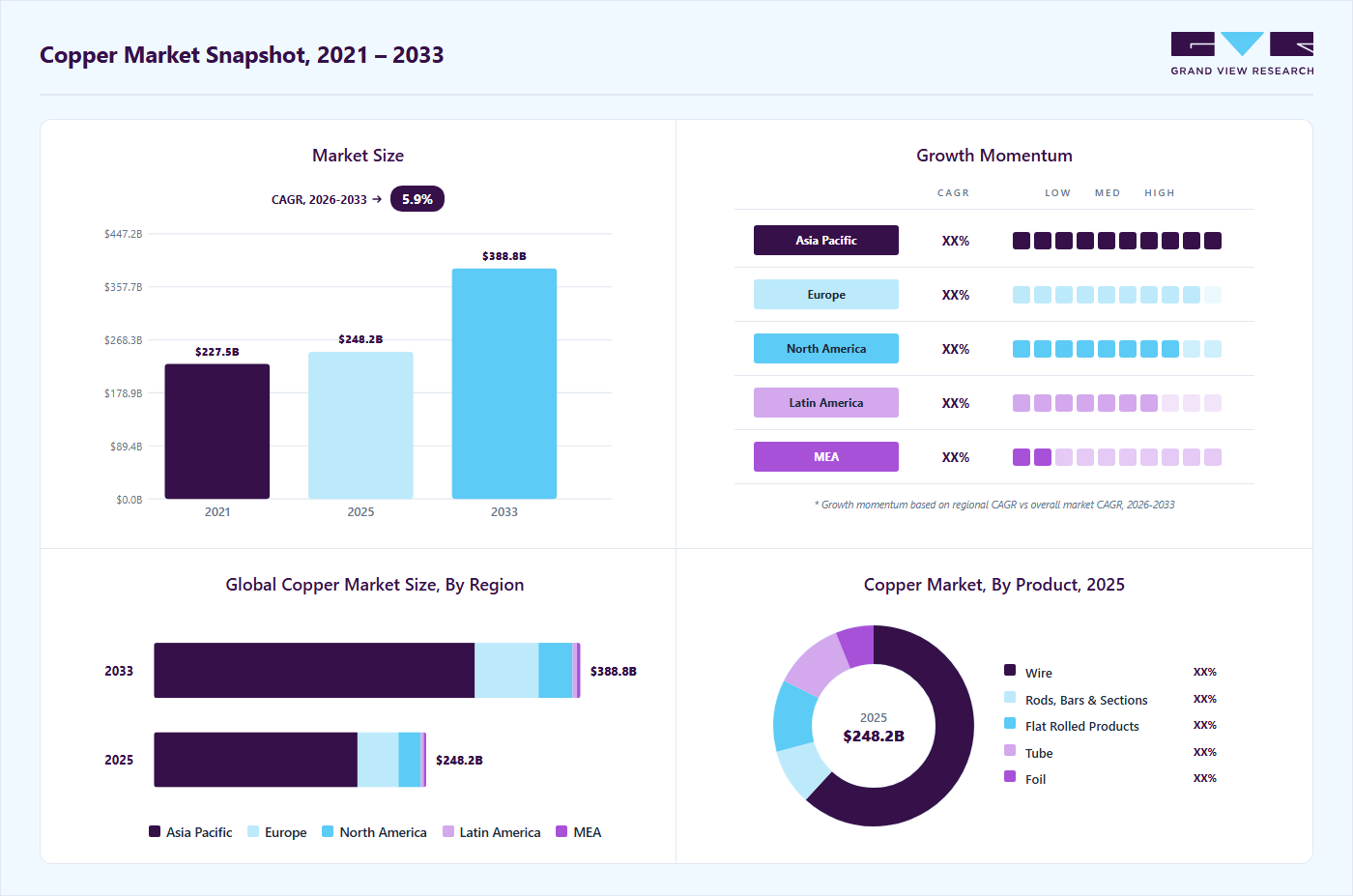

The global copper market size was valued at USD 248.2 billion in 2025 and is projected to grow from USD 260.2 billion in 2026 to USD 388.8 billion by 2033, at a CAGR of 5.9% from 2026 to 2033. The Asia Pacific market held the largest share of 74.0% of the global market in 2025. Copper is critical in solar panels, wind turbines, and associated grid infrastructure.

Key Market Trends & Insights

- By type: The primary copper segment held the revenue share of over 84.0% in 2025.

- By product: The wire segment held the revenue share of over 61.0% in 2025.

- By end use: The building & construction segment held the revenue share of over 26.0% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (74.0% revenue share, 2025)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 248.2 Billion

- Estimated market size in 2026: USD 260.2 Billion

- Projected market size by 2033: USD 388.8 Billion

- CAGR (2026-2033): 5.9%

According to the International Energy Agency (IEA), expanding solar PV and wind capacity globally has sharply increased copper demand, especially for cabling, power conductors, and transformers. With countries like China, the U.S., and those in the EU setting aggressive targets for net-zero emissions, the copper-intensive renewable energy sector is expected to drive consistent market growth through 2030.Copper is a critical material used in building wiring, plumbing, roofing, and other infrastructure components due to its superior conductivity and corrosion resistance. Rapid urbanization, especially in the Asia Pacific and Africa, propels the demand for residential and commercial infrastructure, thereby boosting copper consumption. Large-scale investments in public infrastructure projects such as bridges, highways, and smart cities further stimulate the need for copper-based materials.

")

Due to its electrical efficiency, it plays a central role in solar photovoltaic systems, wind turbines, electric grids, and energy storage systems. The global push for cleaner energy sources to meet climate targets has led to a surge in renewable power installations, all of which require significant amounts of copper. Moreover, as countries upgrade aging power grids and integrate smart grid technologies, the demand for copper-intensive transmission and distribution networks continues to climb.

The proliferation of electric vehicles (EVs) and advancements in automotive technology are powerful forces driving the market’s growth. EVs require substantially more copper than internal combustion engine vehicles, primarily for batteries, wiring harnesses, inverters, and electric motors. As governments worldwide implement stricter emission regulations and offer subsidies for EV purchases, automakers accelerate their transition to electric platforms, fueling a sharp rise in the product’s demand. Moreover, the development of charging infrastructure adds another layer of copper consumption across global markets.

Market Dynamics

The rapid expansion of the electric vehicle (EV) market has emerged as a significant growth driver for the global copper market. Copper is crucial in EV manufacturing due to its excellent electrical conductivity, thermal properties, and durability. EVs typically require 3–4 times as much copper as conventional internal combustion engines. From battery packs and inverters to motors and high-voltage wiring systems, copper supports EV performance, efficiency, and safety. With the global transition towards decarbonization and clean mobility, the surging demand for EVs directly translates to increased copper consumption.

Volatility in copper prices remains a key restraint for the global copper market. For instance, during trading on May 12, 2026, LME copper prices reached USD 14,106.5 per ton. The rise is attributed to tightening global supply and rising demand from electric vehicles, renewable energy systems, and AI-driven data centers.

Geopolitical tensions, trade restrictions, environmental regulations, and mining disruptions in major copper-producing countries, such as Chile, Peru, and Indonesia, continue to affect global copper trade flows. Since a large share of global copper reserves and refining capacity is concentrated in limited regions, supply chain disruptions and changing import-export policies significantly affect material availability and procurement costs across the market.

Type Insights

The primary copper segment held the revenue share of over 84.0% in 2025. Primary copper production offers superior electrical conductivity, making it ideal for applications in power transmission, renewable energy systems, and automotive components. As the global rollout of renewable energy projects and smart grids accelerates, especially in countries like China, the U.S., and Germany, the requirement for high-quality copper extracted from ores is surging. Additionally, new mining investments in regions like Latin America and Africa, combined with large-scale industrialization in the Asia Pacific, are strengthening the supply and utilization of primary copper in various downstream industries.

Secondary copper production, i.e. refined copper produced after recycling, requires significantly less energy, up to 85% less, than primary methods, making it an environmentally friendly alternative. As governments and industries push toward carbon neutrality, recycling is recognized as a strategic solution to reduce emissions and conserve resources. Additionally, regulatory frameworks in Europe, North America, and parts of Asia are encouraging the development of scrap recovery infrastructure, thereby boosting the volume and efficiency of secondary copper production.

Product Insights

The wire segment held the revenue share of over 61.0% in 2025. Copper wires are essential in residential, commercial, and industrial infrastructure for power distribution, telecommunications, and grounding systems due to their excellent conductivity, flexibility, and corrosion resistance. Solar and wind energy systems, electric vehicle charging stations, battery storage, and grid interconnections rely heavily on copper wiring for efficient energy transmission. Technological upgrades in consumer electronics, data centers, and 5G infrastructure further support the segment’s growth, as these applications require high-performance wiring for speed and reliability. With the global transition toward cleaner energy and digital infrastructure, the wire segment is expected to remain a cornerstone of copper product demand in the coming years.

Flat rolled products is anticipated to register the fastest CAGR over the forecast period. Flat-rolled copper, such as sheets, strips, and plates, is widely used in architectural elements (e.g., roofing and cladding), heat exchangers, printed circuit boards (PCBs), and precision engineering components. The material’s excellent thermal and electrical conductivity, formability, and corrosion resistance make it highly suitable for applications requiring consistent performance and aesthetic appeal, especially in modern building designs and consumer electronics.

End Use Insights

The building & construction segment held the revenue share of over 26.0% in 2025. The building and construction segment represents one of the largest end-use markets for copper, driven by its essential role in electrical wiring, plumbing, roofing, and HVAC systems. Copper’s superior conductivity, durability, and corrosion resistance make it ideal for safe and efficient power distribution in residential, commercial, and industrial structures. Furthermore, the push toward sustainable, energy-efficient buildings increases copper use in green construction initiatives. Copper is a key component in solar panel installations, smart building automation systems, and energy-efficient heating and cooling systems. Renovation and retrofitting of aging infrastructure in developed economies also sustain demand, as outdated systems are replaced with modern copper-based components for improved performance and energy savings.

The infrastructure segment is anticipated to register the fastest CAGR over the forecast period. Copper is fundamental to infrastructure development due to its unmatched electrical and thermal conductivity. This makes it essential for power transmission lines, substations, rail electrification systems, and telecommunications networks. As governments across developed and developing nations continue to allocate substantial budgets for infrastructure modernization and expansion, such as smart grids, metro systems, airports, and highways, the demand for copper has surged.

Regional Insights

Asia Pacific dominated the global copper market and held over 74.0% revenue share in 2025. Countries like China and India led extensive infrastructure development projects, including the construction of residential and commercial buildings, transportation networks, and industrial facilities. Copper's essential role in electrical wiring, plumbing, and roofing materials made it indispensable for these developments. In 2024, countries like China and India accelerated their renewable energy initiatives and EV adoption, necessitating substantial copper inputs. For instance, in June 2024, Freeport Indonesia inaugurated a USD 3.7 billion copper smelter in Gresik to meet the rising demand for copper in renewable energy applications.

North America Copper Market Trends

In 2025, the North American copper industry experienced robust growth, driven by significant investments in renewable energy and EV infrastructure. The U.S. and Canada have been heavily investing in renewable energy projects, such as wind turbines and solar panels, where copper's efficiency in energy transfer significantly reduces wastage, making it a preferred material for sustainable energy technologies. Government initiatives have further bolstered the copper market. The Inflation Reduction Act has spurred investment in solar, wind, and battery storage projects, contributing to the growth of the U.S. green energy market.

U.S. Copper Market Trends

The U.S. Department of Energy reported a 14% increase in renewable energy investments, leading to heightened demand for copper-based components in solar panels, wind turbines, and energy storage systems. Simultaneously, the surge in EV production amplified the need for copper in batteries and charging systems, prompting companies to expand their production capacities to meet this rising demand.

Europe Copper Market Trends

The European Union's Green Deal, aiming for climate neutrality by 2050, has accelerated investments in wind and solar energy projects, requiring substantial amounts of copper for turbines, wiring, and grid infrastructure. Additionally, the surge in EV production across Europe has heightened the demand for copper, as each electric vehicle uses significantly more copper than a traditional combustion engine vehicle. This trend is particularly evident in countries like Germany and France, where automotive manufacturers are expanding their EV offerings to meet environmental targets.

Latin America Copper Market Trends

In 2025, Latin America's copper industry experienced notable growth, driven by its substantial mining capacity and increasing global demand for copper-intensive technologies. The region accounted for approximately 46% of the world's raw copper production, with Chile and Peru leading as top producers. Major mining operations, such as the Escondida mine in Chile, the world's largest copper mine with an annual capacity of approximately 1.4 million metric tons, played a pivotal role in meeting global copper demand. Countries like Mexico and Argentina have also been expanding their mining activities to capitalize on the growing demand.

Middle East & Africa Copper Market Trends

In the Middle East, countries like Saudi Arabia, the UAE, and Oman are investing in copper-intensive projects to diversify their economies beyond oil. Saudi Arabia's Vision 2030 emphasizes mining, including copper, as a key sector. The UAE and Oman are developing metal trading hubs to capitalize on the growing copper and other critical minerals demand.

Key Copper Company Insights

Some of the key players operating in the market include AngloAmerican, Codelco, and others

-

AngloAmerican is a global mining company headquartered in London, United Kingdom, with operations spanning Africa, Australia, and North and South America. The company has positioned itself as a sustainability-focused miner, aligning its business strategy with global decarbonization and clean energy goals.

-

Codelco (Corporación Nacional del Cobre de Chile) is the world's largest copper producer, wholly owned by the Chilean government. Established in 1976 following the nationalization of Chile's copper industry, Codelco is headquartered in Santiago and operates seven major mining divisions. The company also manages the Ventanas Smelter and Refinery.

Key Copper Companies:

The following key companies have been profiled for this study on the copper market.

- AngloAmerican

- Antofagasta plc.

- Aurubis AG

- BHP

- Codelco

- Freeport-McMoRan

- Glencore

- GRUPO MÉXICO

- Jiangxi Copper Corporation

- KGHM

- Rio Tinto

- Teck Resources Limited

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: BHP; Codelco; Freeport-McMoRan; Rio Tinto; Glencore; Anglo American

- Strengthen vertically integrated operations across mining, smelting, refining, and distribution.

- Invest heavily in automation, digital mining technologies, low-carbon operations, and long-term supply agreements with EV, construction, and infrastructure sectors.

- Extensive global mining operations with vertically integrated copper extraction, smelting, and refining capabilities.

- Strong reserve base, large-scale production capacities, and long-term supply agreements across industrial sectors.

- High exposure to copper price fluctuations and cyclical industrial demand.

- Increasing environmental regulations, ESG compliance costs, and geopolitical risks in mining regions.

Emerging Players: Antofagasta plc.; Aurubis AG; Jiangxi Copper Corporation; KGHM; Grupo México; Teck Resources Limited

- Focus on regional expansion, refining capacity additions, and operational efficiency improvements.

- Pursue strategic partnerships, modernization of mining assets, and targeted international expansion strategies.

- Competitive production costs supported by strategic asset locations and infrastructure access.

- Increasing adoption of advanced refining technologies and sustainability-focused operations.

- Comparatively lower production scale and global diversification versus mining majors.

- Operational risks related to labor issues, energy costs, and infrastructure limitations in key regions.

Recent Development

-

In June 2025, Adani Enterprises Ltd commissioned the world’s largest copper smelter as part of the initial phase of its project, with further capacity expansion already cleared by environmental regulators. This milestone strengthens the company’s position in the global metals industry while significantly boosting India’s copper production and processing capabilities.

-

In April 2024, Prysmian, a global leader in energy and telecom cable systems, signed a long-term contract with Aurubis, the largest copper recycler and a leading European manufacturer of copper wire rods, to supply significant and progressively increasing volumes of copper wire rods. This agreement primarily supports Prysmian's European plants, ensuring supply continuity for current operations and future growth.

Copper Market Report Scope

Report Attribute

Details

Market Definition

Copper market size represents refined copper usage/demand in various applications.

Market size in 2025

USD 248.2 billion

Estimated market size in 2026

USD 260.2 billion

Projected market size by 2033

USD 388.8 billion

Growth rate

CAGR of 5.9% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative Units

Volume in Kilotons, Revenue in USD million, and CAGR from 2026 to 2033

Report coverage

Volume forecast, revenue forecast, competitive landscape, growth factors, and trends

Segments covered

Type, product, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; France; Italy; Russia; China; India; Japan; South Korea; Brazil; Saudi Arabia; UAE

Key companies profiled

Jiangxi Copper Corporation; Aurubis AG; Codelco; Glencore; BHP; AngloAmerican; Teck Resources Limited; Antofagasta plc.; KGHM; Rio Tinto; Freeport-McMoRan; GRUPO MÉXICO

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Copper Market Report Segmentation

This report forecasts revenue and volume growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For the purpose of this study, Grand View Research has segmented the global copper market report on the basis of type, product, end use, and region.

-

Type Outlook (Revenue, USD Million; Volume, Kilotons; 2021 - 2033)

-

Primary Copper

-

Secondary Copper

-

-

Product Outlook (Revenue, USD Million; Volume, Kilotons; 2021 - 2033)

-

Wire

-

Rods, Bars & Sections

-

Flat Rolled Products

-

Tube

-

Foil

-

-

End Use Outlook (Revenue, USD Million; Volume, Kilotons; 2021 - 2033)

-

Industrial Equipment

-

Transport

-

Infrastructure

-

Building & Construction

-

Consumer & General Products

-

Others

-

-

Regional Outlook (Revenue, USD Million; Volume, Kilotons; 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

Italy

-

France

-

Russia

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Copper Alloys in Connector Applications Assessment

Delivered a focused study on copper alloy consumption in connector applications, with segmentation by alloy type and end-use industries such as telecommunications, aerospace & defense, industrial automation, medical equipment, and consumer electronics. Also developed detailed company profiles and competitive assessments for selected players as required by the client.

Helped the client identify high-growth application areas, alloy demand trends, and competitive positioning opportunities within the connector market. Supported strategic planning through targeted insights on key manufacturers and end-use demand patterns.

Copper Scrap & Recycling Market Assessment

Included analysis of emerging recycled copper sources, market sizing by end-use sectors such as power generation, construction, appliances & electronics, and transport, along with competitor profiling of major recycled copper users. The study also covered recycling focus areas, partnerships, key strengths, and recent technology developments.

Prioritize high-potential recycled copper sources, evaluate competitive positioning across the recycling value chain, and understand end-use demand dynamics to support strategic expansion and sourcing decisions.

Copper Price Monitoring & Weekly Newsletter

Weekly newsletter tracking monthly copper price movements and market trends. The newsletter included weekly price assessments, supply-demand updates, end-use industry analysis, and key market developments influencing copper pricing.

Enabled the client to monitor copper price volatility, support procurement planning, and make informed purchasing decisions through timely market intelligence and regular pricing updates.

Frequently Asked Questions About This Report

Asia Pacific dominated with a 74.0% revenue share in 2025.

The building & construction segment accounted for the largest revenue share of over 26.0% in 2025, while infrastructure is the fastest-growing segment.

Wire segment held the largest share (over 61.0%) in 2025, while flat rolled products is the fastest-growing product.

The key factor that is driving the growth of the global copper market is driven by the increasing demand from renewable energy systems, electric vehicles, and infrastructure development, all of which require significant amounts of copper for electrical conductivity, thermal efficiency, and durability.

The global copper market size was valued at USD 248.2 billion in 2025 and is estimated at USD 260.2 billion for 2026.

The global copper market is expected to grow at a CAGR of 5.9% from 2026 to 2033, reaching USD 388.8 billion by 2033.

The primary copper segment dominated the market with a revenue share of over 84.0% in 2025.

Key players include Jiangxi Copper Corporation; Aurubis AG; Codelco; Glencore; BHP; AngloAmerican; Teck Resources Limited; Antofagasta plc.; KGHM; Rio Tinto; Freeport-McMoRan; GRUPO MÉXICO.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.