- Home

- »

- Advanced Interior Materials

- »

-

Nanotechnology In Mining Market Size Report, 2025-2033GVR Report cover

![Nanotechnology In Mining Market (2025 - 2033)Report]()

Nanotechnology In Mining Market (2025 - 2033)

Size, Share & Trends Analysis Report By Nanomaterial Type (Carbon Nanomaterials, Metal Nanomaterials), By End-use (Mining & Metals, Environmental Services), By Region, And Segment Forecasts

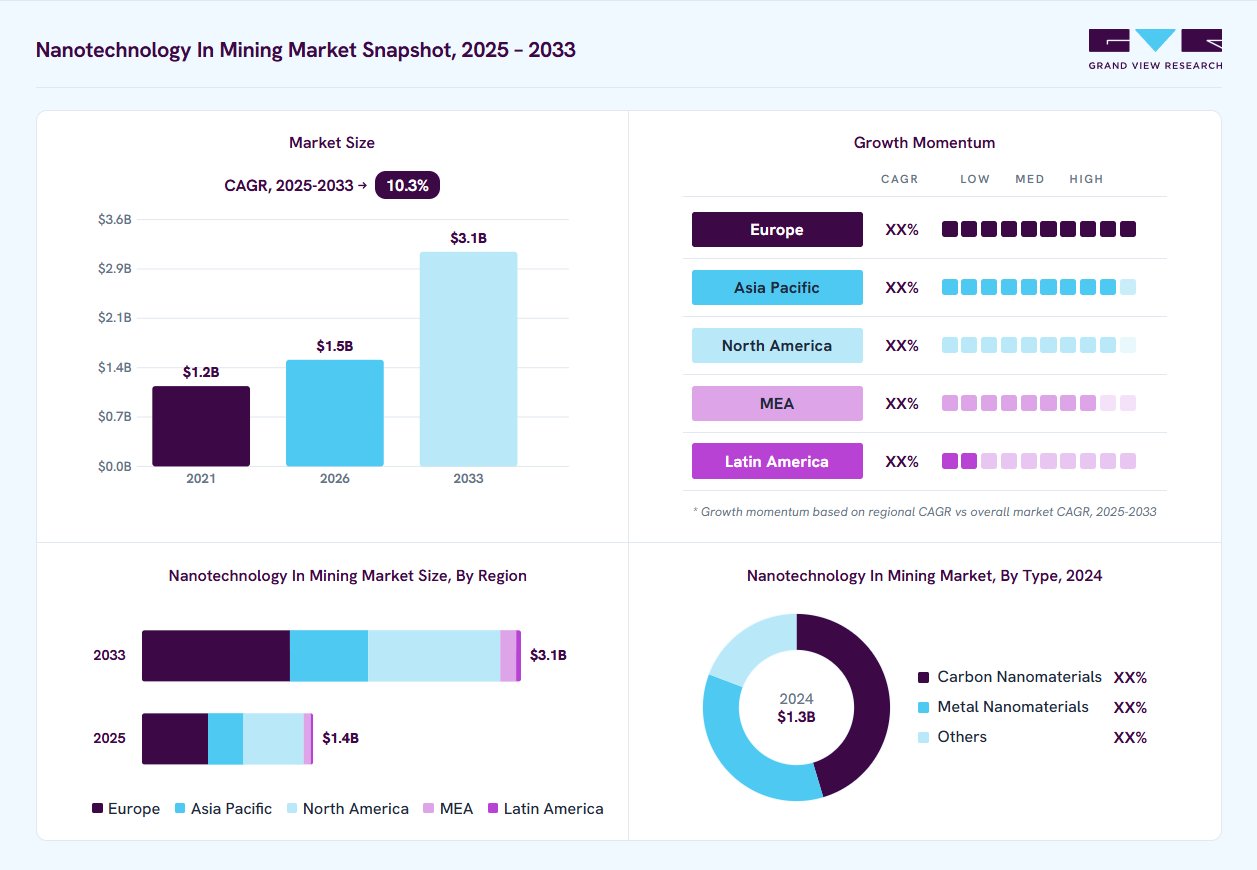

Market Size, 2024

$1.3BMarket Estimate, 2026

$1.5BMarket Forecast, 2033

$3.1BCAGR, 2025–2033

10.3%Nanotechnology in Mining Market Summary

The global nanotechnology in mining market size was valued at USD 1.3 billion in 2024 and is projected to grow from USD 1.5 billion in 2026 to USD 3.1 billion by 2033, at a CAGR of 10.3% from 2025 to 2033. Europe dominated the market, accounting for a revenue share of 38.2% in 2024. The industry is primarily driven by rising supply chain vulnerabilities, geopolitical tensions, and increasing demand for critical minerals used in defense, renewable energy, and advanced manufacturing.

Key Market Trends & Insights

- The nanotechnology in mining market in the U.S. is expected to grow at a substantial CAGR over the forecast period.

- By nanomaterial type, carbon nanomaterials dominated the market with a revenue share of over 45.0% in 2024.

- By end use, the metals and mining segment held the largest share of over 68.0% in 2024.

Market Size & Forecast

- 2024 Market Size: USD 1.3 Billion

- 2033 Projected Market Size: USD 3.1 Billion

- CAGR (2025-2033): 10.3%

- North America: Largest market in 2024

- Europe: Largest market in 2024

Furthermore, government initiatives to secure strategic reserves and reduce import dependence are expected to propel market growth further. Nanotechnology in mining is increasingly pivotal in improving mineral recovery, enhancing process efficiency, and reducing operational costs. By leveraging nanoscale materials and solutions, mining companies can extract minerals more effectively, optimize processing methods, and reduce energy and chemical usage, making economic and environmental operations efficient.")

The adoption of nanotechnology is particularly significant in sectors such as defense, renewable energy, and advanced manufacturing, where the demand for critical minerals is growing. Nano-enabled solutions help stabilize supply chains, ensure consistent material availability, and support strategic industries, strengthening national security and economic resilience.

Sustainability and circular economy principles are driving further innovation in nanotechnology applications. Governments and industry players increasingly implement traceable, responsible mining practices and nano-enabled recycling or recovery technologies. These approaches reduce reliance on virgin resources, minimize environmental impact, and position nanotechnology as both a strategic advantage and a regulatory-aligned solution for long-term resource security.

Drivers, Opportunities & Restraints

The adoption of nanotechnology in mining is driven by the need to improve mineral recovery, optimize processing efficiency, and minimize environmental impact. Nanoscale materials allow for more precise extraction and advanced filtration, reducing chemical usage and energy consumption. For example, BHP has partnered with Summit Nanotech to apply nanotechnology in direct lithium extraction, improving efficiency while lowering environmental impact. Such innovations help companies meet sustainability goals and operational cost targets. Additionally, rising global demand for critical minerals in renewable energy, electric vehicles, and electronics is pushing mining companies to adopt nano-enabled solutions to secure high-quality output consistently. Integrating nanotechnology also facilitates real-time monitoring and enhanced process control, further boosting operational efficiency.

Nanotechnology offers sustainable mining and resource recovery opportunities, supporting circular economy initiatives. Nano-enabled solutions can extract critical minerals from waste streams or low-grade ores, reducing reliance on virgin materials. A recent example is Anglo American’s use of nanomaterials in FutureSmart Mining to recover metals more efficiently while minimizing environmental footprint. This trend opens avenues for innovation in eco-friendly extraction and recycling of high-value minerals. There is also potential for nanotechnology to improve water treatment, tailing management, and environmental remediation in mining operations. Furthermore, governments and investors are increasingly funding R&D initiatives in nano-enabled mining technologies, creating new commercialization opportunities for innovators.

High initial costs, technical challenges, and regulatory uncertainties restrain the adoption of nanotechnology in mining. Scaling laboratory nanomaterials to industrial mining operations requires significant investment and expertise. For instance, deploying nano-based lithium extraction technologies requires careful design to balance performance, cost, and safety. Additionally, the lack of standardized regulations and safety guidelines for nanomaterials in mining operations can slow widespread adoption. There are also concerns about specific nanomaterials' long-term environmental and health impacts. These challenges can limit market growth despite the technological potential and increasing interest from mining companies.

Nanomaterial Type Insights

The carbon nanomaterials dominated the market with a revenue share of over 45.0% in 2024, accounting for a significant share of revenue and usage in mining applications. This dominance is driven by their extensive applications in advanced filtration, flotation, and mineral recovery processes, which enhance efficiency and reduce energy and chemical consumption. Governments and private mining companies increasingly adopt carbon-based nanomaterials to improve process yields and support sustainable operations.

Metal Nanomaterials represent another key segment, supported by their critical role in catalysis, mineral extraction, and nanocomposite development for high-value metals. Their use is expanding in advanced mining operations targeting lithium, cobalt, nickel, and other battery-related metals, aligning with the growing demand from electric vehicles, energy storage, and renewable energy systems.

The Others category, including polymeric, ceramic, and hybrid nanomaterials, is witnessing growing adoption due to their applications in environmental remediation, tailings management, and specialty mineral recovery. Collectively, these segments reflect a global shift toward sustainable, high-efficiency mining practices, resource security, and long-term industrial resilience through nanotechnology.

End-use Insights

In 2024, the metals and mining segment held the largest share, over 68.0% of nanotechnology in mining revenue, reflecting its central role in improving mineral recovery, process efficiency, and resource utilization. Companies increasingly adopt nano-enabled solutions in ore beneficiation, flotation, and extraction processes to enhance yields and reduce environmental impact. Initiatives by major miners such as BHP and Anglo American illustrate the integration of nanotechnology for sustainable, high-efficiency operations.

The Environmental Services segment is gaining prominence as nanomaterials are applied in water treatment, tailings management, and pollution control. Nano-enabled filtration, adsorption, and remediation technologies allow mining operations to meet stringent environmental regulations while minimizing chemical usage and energy consumption. This segment is significant for regions with strict sustainability standards or limited water resources.

Other end uses are steadily expanding, driven by pilot projects, laboratory studies, and innovation in specialty nanomaterials. R&D efforts focus on designing advanced carbon, metal, and hybrid nanomaterials for applications ranging from recycling critical minerals to monitoring and sensor technologies. Emerging economies and industries such as electric mobility and renewable energy increasingly leverage these developments to secure resources, enhance operational efficiency, and support sustainable, long-term growth.

Regional Insights

The North America nanotechnology in mining market is expected to grow at a substantial CAGR over the forecast period. North America increasingly integrates nanotechnology into mining operations to enhance efficiency and sustainability. In 2025, the U.S. government invested USD 36.5 million in Canadian company Trilogy Metals, acquiring a 10% stake, to advance critical mineral projects like the Ambler Road Project in Alaska. This initiative aims to secure domestic supplies of essential materials such as copper, cobalt, gallium, and germanium, aligning with national strategies to reduce reliance on foreign sources. Additionally, Oklahoma is emerging as a critical mineral processing hub, with facilities for lithium refining, battery recycling, and rare earth magnet production, supported by companies like USA Rare Earth and Green Li-ion.

U.S. Nanotechnology In Mining Market Trends

In 2025, the U.S. government intensified its focus on securing critical minerals through strategic investments in nanotechnology applications within the mining sector. A notable example is the Department of Energy's launch of the "Mine of the Future" initiative, allocating USD 95 million to establish demonstration-scale projects across four U.S. mines. Under real-world conditions, these projects aim to test and deploy next-generation mining technologies, including nanomaterial-based solutions for ore processing and resource recovery. This initiative underscores the government's commitment to advancing sustainable and efficient mining practices through integrating nanotechnology.

Asia Pacific Nanotechnology In Mining Market Trends

The nanotechnology in mining market in Asia Pacific continues to lead in adopting nanotechnology in mining, driven by rapid industrialization and a focus on clean energy minerals. India's National Critical Minerals Mission, launched in 2025, accelerates the procurement and stockpiling of lithium and cobalt to support the electric vehicle (EV) and renewable energy sectors. This initiative underscores the region's commitment to securing domestic supplies of essential materials and reducing import dependency, aligning with broader sustainability goals.

Europe Nanotechnology In Mining Market Trends

Europe dominated the nanotechnology in mining market with a revenue share of 38.2% in 2024. The nanotechnology in mining market in Europe is driven by the region’s intensifying efforts to secure critical minerals essential for its green transition and technological sovereignty. In 2025, the European Union announced 47 strategic projects to increase the production of 14 critical materials, including lithium, copper, and rare earth elements, aiming to mine 10%, process 40%, and recycle 25% of these materials by 2030. These projects span 13 EU countries and are part of the EU's Critical Raw Materials Act, which seeks to reduce dependency on external sources, particularly China.

Key Nanotechnology In Mining Companies Insights

Key players operating in the nanotechnology in mining market are undertaking various initiatives to strengthen their presence and increase the reach of their products and services. Strategies such as expansion activities and partnerships are key in propelling the market growth. Some of the key players operating in the market include Alrosa, Anglo American, BHP Group Limited, and Others.

-

Alrosa PJSC, established in 1992 and headquartered in Mirny, Russia, is a leading diamond mining company. It specializes in exploring, mining, processing, and selling rough and polished diamonds. The company operates primarily in Western Yakutia and the Arkhangelsk region. Alrosa invests significantly in community development, environmental stewardship, and sustainable mining practices.

-

Anglo American plc, founded in 1917 and headquartered in London, UK, is a major global mining company. It operates across diverse commodities, including copper, diamonds, iron ore, coal, nickel, and platinum. The company emphasizes sustainable mining practices, technological innovation, and digital solutions for operational efficiency. Anglo American also focuses on improving its projects' safety, environmental management, and community engagement.

-

BHP Group Limited, established in 1885 and headquartered in Melbourne, Australia, is one of the world’s largest mining companies. It produces iron ore, copper, coal, and potash, and engages in exploration, development, and processing of mineral resources. The company pursues strategic growth initiatives, mergers, and acquisitions to expand its operations. BHP also emphasizes sustainability, risk management, and reducing environmental impact across its global operations.

Key Nanotechnology In Mining Companies:

The following are the leading companies in the nanotechnology in mining market. These companies collectively hold the largest market share and dictate industry trends.

- Alrosa

- Anglo American

- BHP Group

- Energy Exploration Technologies Inc.

- Litus

- NanoStruck Technologies

- Novalith

- Rio Tinto

- Summit Nanotech

- Vale S.A.

Recent Developments

-

Alrosa has introduced NanoMark, a non-invasive laser marking technology that imprints a unique identifier within diamonds' atomic structure. This subatomic marking ensures complete traceability from mine to market without compromising the diamond’s integrity. The technology provides a digital passport containing information about the diamond’s origin, characteristics, and history. It enhances the diamond industry's transparency, consumer confidence, and ethical sourcing.

-

Anglo American’s FutureSmart Mining initiative integrates advanced technologies, including nanotechnology, to transform mining operations. The approach focuses on improving operational efficiency, reducing environmental impact, and enhancing safety through automation and digital solutions. Nanotechnology is applied to develop sustainable methods for mineral extraction and processing. The initiative also emphasizes community engagement and environmental stewardship.

-

BHP has partnered with Summit Nanotech to advance sustainable lithium extraction using nanotechnology. The collaboration aims to develop efficient direct lithium extraction (DLE) methods that minimize environmental impact. The project supports BHP’s commitment to sustainable mining and the production of battery-grade lithium. Nanotechnology enables higher recovery rates, reduced chemical usage, and improved water management in lithium operations.

Nanotechnology In Mining Market Report Scope

Report Attribute

Details

Market size in 2024

USD 1.3 billion

Estimated market size in 2026

USD 1.5 billion

Projected market size by 2033

USD 3.1 billion

Growth rate

CAGR of 10.3% from 2025 to 2033

Base year for estimation

2024

Historical data

2021 - 2023

Forecast period

2025 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2025 to 2033

Report coverage

Revenue forecast, competitive landscape, growth factors, and trends

Segments covered

Nanomaterial type, end-use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; France; UK.; Italy; China; India; Japan; South Korea; Brazil; South Africa

Key companies profiled

Alrosa; Anglo American; BHP; EnergyX (Energy Exploration Technologies Inc.); Litus; NanoStruck Technologies; Novalith; Rio Tinto; Summit Nanotech; Vale S.A.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Nanotechnology In Mining Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and analyzes the latest trends in each sub-segment from 2021 to 2033. For this study, Grand View Research has segmented the global nanotechnology in mining market report by nanomaterial type, end-use, and region.

-

Nanomaterial Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Carbon Nanomaterials

-

Metal Nanomaterials

-

Others

-

-

End-use Outlook (Revenue, USD Million, 2021 - 2033)

-

Mining and Metals

-

Environmental Services

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

France

-

UK

-

Italy

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

South Africa

-

-

Frequently Asked Questions About This Report

The global nanotechnology in mining market size was valued at USD 1.3 billion in 2024 and is estimated at USD 1.5 billion for 2026.

The global nanotechnology in mining market is expected to grow at a CAGR of 10.3% from 2025 to 2033, reaching USD 3.1 billion by 2033.

By type, carbon nanomaterials dominated the market with a revenue share of over 45.0% in 2024.

Some of the key vendors in the global nanotechnology in mining market are Alrosa, Anglo American, BHP, EnergyX (Energy Exploration Technologies Inc.), Litus, NanoStruck Technologies, Novalith, Rio Tinto, Summit Nanotech, and Vale S.A.

The global nanotechnology in mining market is mainly driven by the need for enhanced mineral recovery and process efficiency through nanoscale innovations. It is also fueled by environmental regulations and sustainable mining practices, which encourage the adoption of nanotechnology for waste treatment and pollution control.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.