- Home

- »

- Petrochemicals

- »

-

Naphtha Market Size, Share And Trends Report, 2026-2033GVR Report cover

![Naphtha Market (2026-2033)Report]()

Naphtha Market (2026-2033)

Size, Share & Trends Analysis Report By Product Type (Light Naphtha, Heavy Naphtha), By Application (Chemicals, Energy/Fuel), By Region (North America, Europe, APAC), And Segment Forecasts

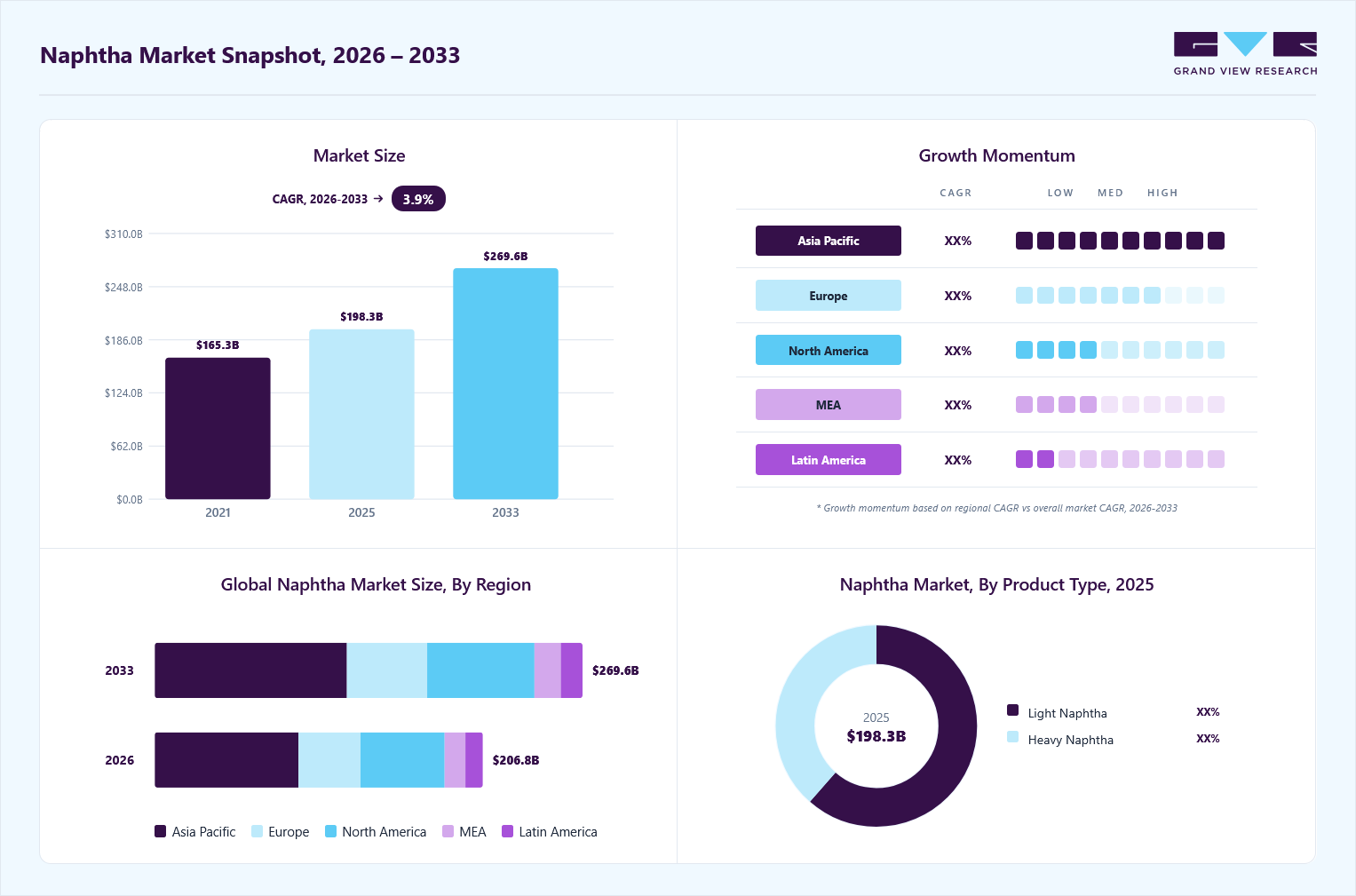

Market Size, 2025

$198.4BMarket Estimate, 2026

$206.8BMarket Forecast, 2033

$269.6BCAGR, 2026–2033

3.9%Naphtha Market Summary

The global naphtha market size was valued at USD 198.4 billion in 2025 and is projected to grow from USD 206.8 billion in 2026 to USD 269.6 billion by 2033, at a CAGR of 3.9% from 2026 to 2033. Asia Pacific dominated the naphtha market with the highest revenue share of 43.7% in 2025. Growing end use industries, development of new manufacturing processes, rise in the petrochemical industry, and expanding transportation sectors are the factors driving the naphtha market growth.

Key Market Trends & Insights

- By product type: Light naphtha segment held the largest market share of 61.4% in 2025.

- By application: Chemicals application segment held the largest market share of 68.0% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (43.7% revenue share, 2025)

- By country: China held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 198.4 Billion

- Estimated market size in 2026: USD 206.8 Billion

- Projected market size by 2033: USD 269.6 Billion

- CAGR (2026-2033): 3.9%

In addition, growing technological advancement in the refining process increases naphtha utilization. Moreover, the expanding transportation sector increases the need for gasoline, further driving the naphtha market demand. The naphtha market is driven by innovations in refining technologies, which have improved the yield and quantity of naphtha, making it a more competitive feedstock for petrochemical production. The application of advanced technologies, such as steam cracking, has enabled the efficient conversion of naphtha into high-value olefins, such as ethylene, further boosting its competitiveness. The development of these technologies has driven performance, flexibility, and sustainability in naphtha usage, shaping the market’s evolution and growth.")

In addition to its use as a petrochemical feedstock, naphtha serves as a solvent in various industries, including paint and coatings, commercial cleaning, and specialty chemical manufacturing. Its ability to dissolve large quantities of materials at a low cost makes it a preferred choice for many methods. The expanding production, automotive, and manufacturing sectors have led to regular calls for naphtha as a solvent, driving its demand. Ongoing research efforts to enhance its solvent properties are expected to further drive market growth.

The transportation sector is another significant driver of the naphtha market. As the transportation sector expands, there is increased demand for products that include plastics and artificial fibers, which are derived from naphtha. This extended demand for petrochemicals leads to higher consumption of naphtha as a feedstock, thereby boosting the naphtha market. Overall, the naphtha market is driven by the combination of technological advancements, expanding industrial applications, and growing demand from the transportation sector. These factors are expected to continue shaping the market growth and competitiveness in the future.

Market Dynamics

Naphtha is a critical petroleum-derived feedstock used extensively in petrochemical production, fuel blending, and various industrial applications. It serves as a primary raw material for steam crackers producing olefins and aromatics, which are subsequently utilized in plastics, synthetic fibers, solvents, detergents, and numerous downstream chemical products. Growing demand for petrochemicals, expanding industrialization, and increasing consumption of plastics and specialty chemicals continue to support global naphtha demand.

The continuous expansion of petrochemical manufacturing capacity worldwide remains a major driver for the naphtha market. Naphtha serves as a key feedstock for steam cracking operations that produce ethylene, propylene, butadiene, benzene, toluene, and xylene, which are essential building blocks for a broad range of industrial products.

Rapid industrialization, urbanization, and growing demand for plastics, packaging materials, synthetic fibers, and consumer goods are further supporting petrochemical investments globally. Increasing capacity additions across Asia and the Middle East continue to strengthen long-term demand for naphtha as a strategic feedstock.

Competition from alternative petrochemical feedstocks such as ethane, propane, and liquefied petroleum gas (LPG) remains a significant challenge for naphtha demand growth. In regions with abundant natural gas resources, petrochemical producers often favor lighter feedstocks due to their cost advantages and favorable production economics.

The increasing demand for downstream chemicals and specialty materials presents substantial opportunities for the naphtha market. Expanding consumption of plastics, engineering resins, synthetic rubbers, coatings, solvents, and performance materials continues to support demand for naphtha-derived petrochemical intermediates.

Analyst Perspective

The naphtha market remains one of the most important indicators of global petrochemical activity, as its demand is fundamentally tied to the production of olefins, aromatics, and downstream chemical intermediates that underpin modern manufacturing and consumer industries. Unlike many refined petroleum products whose growth is closely linked to transportation fuel demand, naphtha derives the majority of its value from its role as a petrochemical feedstock, with nearly seventy percent of consumption directed toward chemical production. As a result, long-term market growth is increasingly influenced by petrochemical capacity additions, particularly in Asia Pacific and the Middle East, rather than by conventional refining dynamics alone. While competition from ethane, propane, and LPG continues to challenge naphtha economics in regions with abundant natural gas resources, naphtha maintains a strategic advantage due to its ability to generate a broader and more balanced olefin-aromatic product slate. Consequently, competitive positioning within the market is expected to be driven by refinery-petrochemical integration, feedstock flexibility, and the ability to capture value across downstream chemical chains, making naphtha a critical bridge between the refining and petrochemical sectors rather than merely an intermediate refinery stream.

Product Type Insights

Based on product type, the light naphtha segment led the market with the largest revenue share of 61.4% in 2025. Light naphtha is highly sought after in the petrochemical industry due to its high paraffin content, used to produce plastics and chemical compounds. The rising industrialization and urbanization in the economy drive demand for light naphtha as a feedstock and blending agent, fueling growth in the petrochemical and automotive industries.

The heavy naphtha segment is expected to grow at a CAGR of 4.3% over the forecast period. This growth is expected to be driven by technological advancements, increasing market demand, regulatory support, and cost reduction. Furthermore, continuous innovation has improved efficiency and effectiveness, while favorable policies from authorities promote the use of heavy naphtha, further driving market growth in the forecast period.

Application Insights

In 2025, the chemicals application segment accounted for the largest revenue share of 68.0%. Naphtha is primarily used to produce gas, ethylene, and propylene. The demand for chemicals, including paints and coatings, is driving growth in this segment. Moreover, the rising demand for chemicals and cleaning agents used in the automobile and production industries has also boosted the demand for naphtha-based products.

The energy/fuel segment is expected to register significant growth with a CAGR of 4.8% over the forecast period, driven by increasing demand from the automobile and construction industries, rising disposable income, and growing demand from chemical industries. Moreover, the expansion of power plants and fertilizer units contributes to market growth. As emerging economies develop industrially and economically, their energy consumption increases, with a corresponding rise in demand for naphtha-based fuels.

Regional Insights

Asia Pacific dominated the naphtha market with the highest revenue share of 43.7% in 2025. The market dominance can be attributed to factors such as rapid industrialization and urbanization, a rise in the automotive industry, and an increase in disposable income lead market growth. In addition, an increase in the plastic intake in the construction sector drives the naphtha market growth in Asia Pacific.

China Naphtha Market Trends

China accounted for 41.5% of the Asia Pacific naphtha market in 2025. This dominance can be attributed to the economic growth and development in industries leading to high demand for naphtha. In addition, the Chinese government has been implementing policies regarding investments in the petrochemical industries.

Europe Naphtha Market Trends

Europe naphtha market is expected to grow at the fastest CAGR of 4.3% over the forecast period. The growth of this region can be attributed to elements including strong demand for naphtha from the petrochemical industry, disposable income increase driving commercial activities, emphasis on cleaner fuels, deliver chain dynamics, and global market trends shaping the overall naphtha market growth.

The naphtha market in Germany led the European market and held a substantial market share in 2025, owing to the well-developed infrastructure and access to key market players that help in the export opportunities. Moreover, the regulation regarding environmental safety for cleaner fuels has driven the naphtha market in Germany.

North America Naphtha Market Trends

The North America naphtha market is expected to witness substantial growth over the forecast period. The region is experiencing a rise in gasoline intake, fueled by economic increase and enhanced business activity. In addition, North America drives the presence of distinguished marketplace players, fostering innovation, funding, and infrastructure improvement in the petrochemical sector.

The naphtha market in the U.S. dominated the North American market and held the largest revenue share in 2025, due to increasing petrochemical industries, increased demand for naphtha in the construction industry, and increased importance of naphtha in power plants, fertilizer units, and paint industries has driven the market growth.

Key Naphtha Company Insights

Some key companies in the naphtha market include Reliance Industries Limited; Exxon Mobil Corporation; Saudi Arabian Oil Co.; and others. The industry is characterized by intense competition among key players who focus on product innovation, strategic partnerships, and expansion to gain a larger market share.

-

Reliance Industries Limited is an Indian petrochemicals company, operating across various sectors including petrochemicals, with a significant presence in the industry.

-

Saudi Arabian oil Co. (Aramco) is a naphtha producer, supplying a significant portion of the global petrochemical feedstock. The company’s integrating upstream and downstream operations, including the Amiral complex, to capture more value across the hydrocarbon chain and strengthen its position in the petrochemical industry.

Key Naphtha Companies:

The following key companies have been profiled for this study on the naphtha market.

-

Reliance Industries Limited

-

Exxon Mobil Corporation

-

Saudi Arabian Oil Co.

-

LG Chem

-

Formosa Petrochemical Corporation

-

Shell plc

-

Indian Oil Corporation Ltd

-

Asahi Kasei Corporation

-

Petróleos Mexicanos

-

JFE Chemical Corporation

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (Reliance Industries Limited, Exxon Mobil Corporation, Saudi Arabian Oil Co., LG Chem, Formosa Petrochemical Corporation, Shell plc, and Indian Oil Corporation Ltd)

- Expanding integrated refining and petrochemical operations to maximize feedstock utilization and value creation.

- Investing in capacity enhancements and downstream petrochemical production to strengthen market competitiveness globally.

- Large-scale refining infrastructure ensures reliable naphtha production and supply across international markets.

- Strong vertical integration supports operational efficiency and improves profitability throughout the petrochemical value chain.

- Significant exposure to crude oil price volatility can impact operating margins and business performance.

- High capital requirements for refinery modernization and expansion projects may affect investment flexibility.

Emerging Players (Asahi Kasei Corporation, Petróleos Mexicanos, and JFE Chemical Corporation)

- Strengthening regional refining and petrochemical operations to improve supply security and customer reach.

- Expanding participation in downstream chemical markets through targeted investments and operational optimization initiatives.

- Strong regional presence enables efficient servicing of domestic petrochemical and industrial demand requirements.

- Diversified industrial operations provide flexibility to capitalize on evolving market and feedstock opportunities.

- Comparatively smaller influence on global naphtha trade flows may limit international market expansion.

- Lower production scale than industry leaders can reduce economies of scale and cost competitiveness.

Recent Developments

-

In February 2024, Saudi Aramco solidified its domestic supply chain ecosystem by securing 40 procurement agreements worth USD 6 billion with Saudi-based suppliers, supporting localization initiatives and aligning with the iktva program, which fosters economic growth and diversification in Saudi Arabia.

-

In December 2023, Coolbrook cracked naphtha in its large-scale pilot plant, validating its RotoDynamic Reactor Technology for electric steam cracking and reducing CO2 emissions by 300 million tons annually, solidifying its leadership in electric steam cracking and decarbonization.

-

In March 2023, ExxonMobil Corporation completed its USD 2 billion Beaumont refinery expansion, adding 250,000 barrels per day capacity to a Gulf Coast complex, equivalent to a medium-sized refinery, boosting energy product output and meeting growing demand.

Naphtha Market Report Scope

Report Attribute

Details

Market size in 2025

USD 198.4 billion

Estimated Market size in 2026

USD 206.8 billion

Projected Market size by 2033

USD 269.6 billion

Growth rate

CAGR of 3.9% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, Volume in Kilotons and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product Type, application, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; China; Japan; India; South Korea; Brazil; Argentina; South Africa; Saudi Arabia; UAE

Key companies profiled

Reliance Industries Limited; Exxon Mobil Corporation; Saudi Arabian Oil Co.; LG Chem; Formosa Petrochemical Corporation; Shell plc; Indian Oil Corporation Ltd; Asahi Kasei Corporation; Petróleos Mexicanos; JFE Chemical Corporation

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Naphtha Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and analyzes the latest industry trends in each sub-segment from 2021 to 2033. For this study, Grand View Research has segmented the global naphtha market report based on product type, application, and region:

-

Product Type Outlook (Volume, Million Metric Tons; Revenue, USD Billion, 2021 - 2033)

-

Light Naphtha

-

Heavy Naphtha

-

-

Application Outlook (Volume, Million Metric Tons; Revenue, USD Billion, 2021 - 2033)

-

Chemicals

-

Energy/Fuel

-

Others

-

-

Regional Outlook (Volume, Million Metric Tons; Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East and Africa

-

South Africa

-

Saudi Arabia

-

UAE

-

-

Research Methodology

The naphtha market figures in this report are based on a proven research process that combines executive interviews with secondary research from proprietary databases, company filings, and recognized regulatory and institutional sources. Market size is built through value-chain sizing - reconciling supply-side and demand-side estimates - and triangulated with bottom-up and top-down approaches. Every estimate passes multiple levels of expert validation before publication, with each naphtha segment quantified using the revenue-capture definitions in the table below.

Segment Definition

Segment - Product Type

Revenue capture definition

Light Naphtha

As the dominant product segment, revenue is primarily generated through sales to petrochemical producers utilizing naphtha as a feedstock for steam cracking and olefin production. Large consumption volumes, continuous plant operations, and expanding petrochemical capacity support substantial market value.

Heavy Naphtha

Revenue capture is driven by utilization in catalytic reforming units for aromatic production and gasoline blending applications. Demand is influenced by refinery operating rates, transportation fuel consumption, and downstream requirements for benzene, toluene, and xylene production.

Segment - Application

Revenue capture definition

Chemicals

As the largest application segment, revenue is supported by naphtha consumption in steam crackers and petrochemical facilities producing olefins, aromatics, and chemical intermediates. Global demand for plastics, synthetic fibers, resins, and specialty chemicals remains the primary growth driver.

Energy/Fuel

Revenue is generated through the use of naphtha in gasoline blending, fuel production, and energy-related applications. Refinery throughput levels, transportation fuel demand, and regional fuel specifications significantly influence commercial consumption within this segment.

Other Application

Market value is derived from industrial solvents, specialty chemical manufacturing, extraction processes, and niche industrial uses. Demand is supported by diverse downstream industries requiring hydrocarbon feedstocks with specific processing and formulation characteristics.

Estimation Model

Layer Name

Key Question

Description

Refinery Production Layer

What forms the supply base?

Identify global refinery output and crude oil processing volumes that generate light and heavy naphtha streams. This establishes the foundational supply base available for petrochemical, fuel, and industrial applications.

Application Adoption Layer

Where is naphtha consumed?

Estimate the proportion of naphtha directed toward chemicals, energy and fuel applications, and other industrial uses based on regional refining configurations and downstream demand requirements.

Consumption Intensity Layer

How much naphtha is utilized?

Analyze feedstock requirements of steam crackers, reformers, fuel blending operations, and industrial processes to determine annual naphtha consumption across major end-use sectors.

Revenue Layer

How is market revenue generated?

Market revenue is quantified through the sale of light and heavy naphtha supplied to petrochemical manufacturers, refiners, fuel blenders, and industrial consumers operating across global downstream value chains.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Regional Segmentation

The study delivers detailed country-level analysis across major naphtha-producing and consuming markets including China, India, Japan, South Korea, Saudi Arabia, the U.S., and other key petrochemical hubs, covering production, consumption, trade, and demand outlooks.

Enables stakeholders to identify regional demand centers, evaluate supply-demand dynamics, and prioritize investments in markets exhibiting strong petrochemical and refining sector growth potential.

Trade Assessment

The report delivers comprehensive historical trade analysis covering naphtha imports, exports, major trading nations, supply routes, trade balances, and evolving global market dynamics influencing regional availability and competitiveness.

Provides valuable insights into supply chain dependencies, import-oriented markets, and international trade flows, supporting strategic sourcing decisions and market risk evaluation..

Opportunity Assessment

The study delivers detailed assessment of growth opportunities across expanding petrochemical capacities, integrated refinery-petrochemical complexes, emerging Asian markets, and regions experiencing increasing demand for petrochemical feedstocks and derivative products.

Helps companies identify attractive investment locations, evaluate long-term demand potential, and align expansion strategies with emerging petrochemical industry developments and consumption trends globally.

Frequently Asked Questions About This Report

The global naphtha market is expected to grow at a compound annual growth rate of 3.9% from 2026 to 2033 to reach USD 269.6 billion by 2033.

Key factors that are driving the market growth include increasing demand for transportation fuel globally and rising product demand in hydrocarbon cracking process.

The global naphtha market size was estimated at USD 198.4 billion in 2025 and is expected to reach USD 206.8 billion in 2026.

Asia Pacific dominated the naphtha market with a share of 43.7% in 2025. This is attributable to increasing population coupled with increasing electrical and transport equipment consumption.

The chemicals segment led the naphtha market in 2025, accounting for 68.0% of market revenue, owing to the extensive use of naphtha as a feedstock in the production of olefins, aromatics, and other petrochemical derivatives.

Some key players operating in the naphtha market include Reliance Industries Limited, Exxon Mobil Corporation, Saudi Arabian Oil Co., LG Chem, Formosa Petrochemical Corporation, Shell plc, Indian Oil Corporation Ltd, Asahi Kasei Corporation, Petróleos Mexicanos, JFE Chemical Corporation.

Asia Pacific is projected to be the fastest-growing regional market during the forecast period, registering a CAGR of 4.2% from 2026 to 2033, driven by expanding petrochemical production, industrialization, and rising energy demand across emerging economies.

The energy/fuel segment is projected to witness the fastest growth during the forecast period, registering a CAGR of 4.3% from 2026 to 2033

The light naphtha segment dominated the naphtha market in 2025, capturing 61.4% of market revenue, due to its widespread utilization as a petrochemical feedstock and blending component in fuel production processes.

About the Author(s)

Petrochemicals Research Team

Bulk Chemicals · PetrochemicalsThis report was authored by the petrochemicals research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the petrochemicals segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.