- Home

- »

- Biotechnology

- »

-

Next Generation Sequencing Market Size Report, 2026-2033GVR Report cover

![Next Generation Sequencing Market (2026 - 2033)Report]()

Next Generation Sequencing Market (2026 - 2033)

Size, Share & Trends Analysis Report By Technology (Targeted Sequencing & Resequencing), By Product (Platform, Consumables), By Application (Oncology, Clinical Investigation), By Workflow, By End Use, By Region And Segment Forecasts

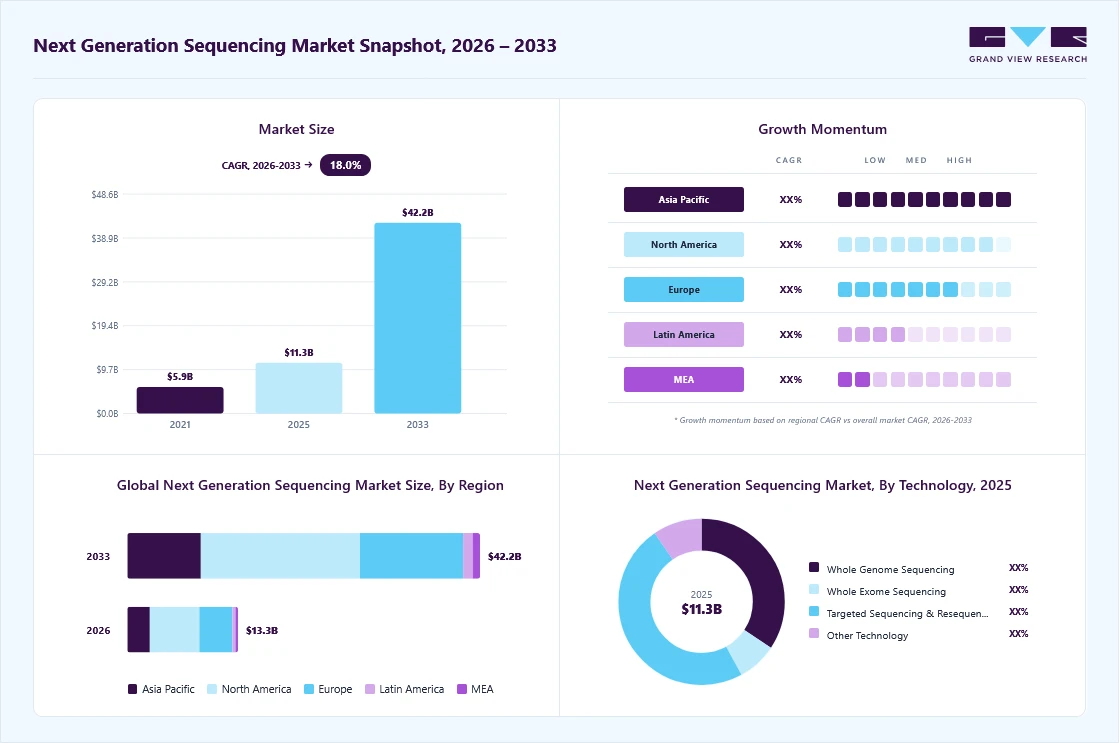

Market Size, 2025

$11.3BMarket Estimate, 2026

$13.3BMarket Forecast, 2033

$42.3BCAGR, 2026–2033

18.0%Next Generation Sequencing Market Summary

The global next generation sequencing market size was valued at USD 11.3 billion in 2025 and is projected to grow from USD 13.3 billion in 2026 to USD 42.3 billion by 2033, at a CAGR of 18.0% from 2026 to 2033. The market in North America dominated with a revenue share of 44.8% in 2025. This growth is driven by the increasing demand for advanced genomic research, rising applications of NGS in clinical diagnostics, and ongoing technological advancements in sequencing platforms.

Key Market Trends & Insights

- By product: Consumables segment held the largest market share in 2025.

- By technology: Targeted sequencing segment held the largest market share of 48.3% in 2025.

- By application: Oncology segment held the largest market share of 32.0% in 2025.

- By workflow: Sequencing segment held the largest market share of 64.3% in 2025.

- By end use: Academic research segment held the largest market share of 36.0% in 2025.

Regional Highlights

- Largest regional market: North America (44.8% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 11.3 Billion

- Estimated market size in 2026: USD 42.3 Billion

- Projected market size by 2033: USD 42.3 Billion

- CAGR (2026-2033): 18.0%

Increased Applications in Clinical Diagnostics

The growth of the next-generation sequencing industry is primarily attributed to the increasing implementation of NGS in clinical diagnostics, which is a major factor driving the market. Technology changes the way doctors diagnose and track diseases by providing accurate, fast, and extensive genomic insights. Its use in non-invasive prenatal testing (NIPT) is the most remarkable, allowing early and precise identification of chromosomal defects without harming the fetus. In addition, NGS is widely used in the diagnosis of rare diseases, carrier screening, and oncology testing, where the detection of genetic mutations is crucial for the application of targeted therapy and disease management.

Examples of Targeted Panels Available In Research and Diagnostic Settings

Disease Condition

Available Panel

Type of Inheritance

Specimen Type

Inherited cardiovascular defects

Cardiovascular research panel

Germline

Blood

Arrhythmias and cardiomyopathies

Arrhythmias and cardiomyopathy research panel

Germline

Blood

Sensitivity to pharmacological drugs

Pharmacogenomics research panel (PGex Seq panel)

Germline

Blood

Antimicrobial treatment efficacy testing

Antimicrobial Resistance Research Panel

Microbial gene testing

Bacterial culture

Infertility conditions

Infertility research panel

Germline

Blood

Homologous recombination defect analysis

HRR gene panel

Somatic

Tumor tissue

Myeloid cancers

Myeloid cancer panel

Somatic

Blood

HIV speciation and drug resistance

HIV-Xgene panel

Pathogen detection

HIV-positive plasma

Antimicrobial resistance in MTB

TB research panel

Pathogen detection

MTB-positive specimen

Inborn errors of metabolism

Error of metabolism research panel

Germline

DBS/blood

Hereditary cancers

BRACA and extended breast and ovarian cancer research panel, inherited cancer research panel

Germline

Blood

Source: PMC, Secondary Research. Grand View Research Inc.

Next-Generation Sequencing (NGS) is revolutionizing the field of infectious disease diagnosis, enabling the rapid detection and tracking of infections with unmatched speed and precision. The world's first utility was demonstrated during the COVID-19 pandemic, and it is still being used in the tracking of variants and threats. The shift in the regulatory approvals for NGS-based clinical tests and the slow but steady adoption of these tests in clinical guidelines have really made them more acceptable.

Advancements in Technology

Technology development has been a significant factor driving the growth of the next-generation sequencing industry. Technology has come a long way, and today, whole-genome, whole-exome, and targeted sequencing are the most advanced and, at the same time, the most cost-effective methods of genetic analysis. This has opened the field of genomics to a larger number of laboratories and clinical settings, making it possible to generate a substantial amount of high-quality data quickly and efficiently for the research of genetic disorders, cancer, and even viruses.

The invention of portable, automated, and high-throughput sequencing systems has made NGS the technology of choice. AI-based bioinformatics, cloud-based analytics, and benchtop and nanopore-based platforms have all contributed to making testing, data interpretation, and flexibility decentralized. Moreover, these innovations have increased the use of NGS in research and clinical settings, while also supporting the growth of personalized medicine, epidemiology, and drug development.

Market Concentration & Characteristics

The next-generation sequencing industry benefits from a high degree of innovation, with ongoing advances in sequencing technologies, including single-cell and long-read sequencing, as well as AI-driven data analysis. For instance, in February 2025, Roche launched its SBX sequencing technology in the U.S., introducing Xpandomer chemistry to enhance signal clarity, accuracy, and scalability for clinical and research genomic applications. These innovations enhance accuracy, speed, and clinical utility while reducing costs, driving the adoption of broader research, diagnostics, and personalized medicine.

The next-generation sequencing industry is experiencing a notable surge in mergers and acquisitions (M&A), which has the dual effect of growing and consolidating the market. The major players in the industry are taking over the smaller and more creative companies to not only increase their technological capabilities but also their product ranges and access to different areas. For instance, in June 2025, Illumina agreed to acquire SomaLogic from Standard BioTools for up to $425 million, aiming to enhance its proteomics and multi-omics capabilities. This trend is expected to continue as players seek to capitalize on emerging opportunities in genomics and personalized medicine.

in genomics and personalized medicine.

The next-generation sequencing industry relies heavily on regulatory frameworks as they guarantee the safety and quality of sequencing technologies. The FDA and European regulators have gradually approved more companies, which has been a great support for clinical adoption. At the same time, clear standards are instilling trust among patients and providers. New regulations on data privacy and genetic information, despite being strict, are actively driving innovation, developing the next-generation sequencing industry, and making NGS more acceptable.

Product expansion is a major driver of the next-generation sequencing industry, as companies introduce new sequencing platforms, reagents, and bioinformatics tools to address varied research and clinical needs. Innovations such as portable sequencers, improved library preparation kits, and advanced data analysis software enhance efficiency and broaden applications. Expanding product portfolios enables companies to serve a diverse Range of end users, including academia, pharma, and healthcare, thereby accelerating market growth and adoption.

The next-generation sequencing industry is primarily driven by regional expansion, which is a key factor for companies to strengthen their presence in emerging regions such as the Asia-Pacific, Latin America, and the Middle East. Demand is boosted by improved healthcare infrastructure, supportive government initiatives, and increased awareness of personalized medicine, while local partnerships and expanded distribution make access more accessible.

Product Insights

The consumables segment accounted for the largest market revenue share in 2025 and is expected to grow at the fastest CAGR from 2026 to 2033. This segment's larger share and exponential growth rate are primarily attributed to the recurrent usage and high demand for consumables in NGS's commercial and research applications. These consumables include sample preparation kits and target enrichment kits. The adoption of NGS consumables has increased as most pharmaceutical companies and research institutes are utilizing NGS for several diagnostic applications and cancer research. For instance, in June 2022, PerkinElmer launched three RUO NGS library prep kits: NEXTFLEX Small RNA-Seq Kit v4, NEXTFLEX Rapid XP V2 DNA-Seq Kit, and PG-Seq Rapid Kit v2, designed to streamline workflows and improve accuracy.

The platform segment is anticipated to grow at a significant CAGR during the forecast years, driven by the increasing adoption of next-generation sequencing (NGS) platforms across research, clinical, and pharmaceutical applications. Moreover, constant advancements in sequencing chemistry, automation, and data analysis programs are not only making the platform performance better but also making it scalable and more accessible.

Technology Insights

The targeted sequencing and resequencing segment led the market with the largest revenue share of 48.3% in 2025. This segment is expected to witness growth in demand following the development of whole-genome sequencing, as the availability of a large amount of whole-genome data will necessitate the analytical identification of specific gene locations and isolated genetic expressions. For instance, in June 2025, BJ Medical College and Sassoon Hospital in Pune initiated targeted genome sequencing of 50 TB samples to identify drug resistance mutations, underscoring the practical application and ongoing importance of this approach in clinical research.

The whole exome sequencing segment is projected to grow at the fastest CAGR over the forecast period. The rising adoption of WES in clinical diagnostics, precision medicine, and translational research, coupled with advancements in bioinformatics pipelines for variant interpretation, is fueling its rapid growth.

Application Insights

The oncology segment led the market with the largest revenue share of 32.0% in 2025, driven by the essential role of genomic data analysis in cancer research, diagnostics, and targeted therapies. Genomic profiling enables the identification of cancer-related mutations and biomarkers, supporting precision medicine and personalized treatment. The rising global incidence of cancer, combined with advances in NGS and bioinformatics, continues to drive adoption in oncology.

The consumer genomics segment is anticipated to grow at the fastest CAGR during the forecast period, owing to the increased demand for ancestry analysis, health risk assessment, and personalized wellness. The awareness of genetic testing has increased, direct-to-consumer services have been made available at lower prices, sequencing technologies have been developed, and reporting platforms have been made easier to use, all of which are factors contributing to the widespread adoption of genetic testing across different demographic groups. Regulatory clarity and data protection remain crucial in enhancing customer acceptance.

Workflow Insights

The sequencing segment led the market with the largest revenue share of 64.3% in 2025 and is expected to grow at the fastest CAGR over the forecast period. NGS sequencing is the most important phase of the workflow and consequently accounts for the largest share of the market. These systems can provide an accurate amount of liquid, which is important in NGS. Moreover, functions such as changing tubes and micro-liter plates are also carried out by the system, which helps streamline workflow.

The NGS data analysis segment is anticipated to grow at a significant CAGR throughout the forecast period. A key factor contributing to the industry's growth is the increasing acceptance of sequencing platforms for clinical diagnosis, driven by a significant reduction in installation costs. Moreover, the easy availability of genomic and proteomic information is anticipated to create significant growth opportunities in this industry during the forecast period. For instance, Illumina's BaseSpace Suite facilitates the rapid analysis of sequencing data and the generation of findings. The company has also purchased DRAGEN Bio-IT Platform (DRAGEN) and Edico Genome to expand its data analytics capabilities.

End Use Insights

The academic research segment led the market with the largest revenue share of 36.0% in 2025. The application of NGS solutions in research projects conducted at universities and research centers accounts for the largest share of this segment in the market. Moreover, scholarships offered for PhD projects in NGS are anticipated to drive demand for NGS products and services, resulting in lucrative growth over the forecast period. The provision of on-site bioinformatics courses, which include workshops on the practical implementation of NGS sequencing and data analysis, is also expected to boost revenue generated by the academic research segment during the forecast period.

The clinical research segment is anticipated to grow at the fastest CAGR during the forecast period, driven by the increasing use of NGS in cancer research, particularly in the discovery of new cancer-related genes, the study of tumor heterogeneity, and the identification of alterations contributing to tumorigenesis. For instance, in February 2025, BioSpectrum Asia reported on Asia’s growing use of NGS in precision oncology, highlighting national efforts to expand genomic profiling, clinical trials, and personalized cancer care across the region. Moreover, the availability of clinical research solutions through market entities such as Illumina, Thermo Fisher Scientific Corporation, and Agilent Technologies for target enrichment & detection is anticipated to provide this segment with high growth opportunities over the forecast period.

Regional Insights

North America dominated the global next-generation sequencing market with the largest revenue share of 44.8% in 2025. The regional market is driven by multiple clinical laboratories employing NGS to provide genetic testing services. Moreover, due to the presence of high R&D investment and the availability of a technologically advanced healthcare research framework, the development of NGS in the region is also expected to serve as a critical factor for the growth of the North American NGS market throughout the forecast period.

U.S Next-Generation Sequencing Market Trends

The next-generation sequencing market in the U.S. accounted for the largest market revenue share in North America in 2025, primarily due to its advanced healthcare system, robust research funding, and the dominance of key players such as Illumina, Thermo Fisher, and Pacific Biosciences. The country is a global leader in genomic medicine, with large-scale initiatives such as the All of U.S. Research Program propelling widespread adoption of NGS in both research and clinical settings. For instance, in October 2022, PathoQuest formally opened a 7,000 sq ft NGS testing facility in Wayne, Pennsylvania, USA, backed by a USD 10 million investment to accelerate biopharma biosafety and viral safety services.

Europe Next-Generation Sequencing Market Trends

The next-generation sequencing market in Europe represents a significant share of the global market, driven by strong government support for genomic research, the expanding applications of NGS in clinical diagnostics, and a well-established healthcare infrastructure. For instance, in May 2025, France-based SeqOne raised funding to expand its AI-driven NGS platform for oncology and rare disease diagnostics.

The UK next-generation sequencing market is expected to grow at a significant CAGR during the forecast period, owing to an increase in the development of companion diagnostics and the subsequent establishment of molecular diagnostic development facilities by key market players. Moreover, ongoing strategic alliances between players in European and Eastern markets are expected to drive the growth of the next-generation sequencing market during the forecast period in the region.

The next-generation sequencing market in Germany is a leading force in Europe’s NGS landscape, primarily due to its strong biotechnology industry, extensive academic research, and state-supported precision medicine programs. The nation is channeling its resources into digitized healthcare, merging NGS with cancer genomics, diagnostics for rare diseases, and monitoring of infectious diseases. Besides, the public-private partnerships are furthering the development of new technologies and their applications in sequencing.

Asia Pacific Next-Generation Sequencing Market Trends

The next-generation sequencing market in Asia-Pacific is anticipated to grow at the fastest CAGR of 18.43% during the forecast period, driven by rising healthcare spending, expanding genomic research, and increasing adoption of precision medicine. Strong investments by countries such as China, Japan, India, and South Korea in genomic infrastructure and public-private partnerships, along with the rapid emergence of local biotech firms, are accelerating innovation and regional competition. Initiatives such as India’s LuNGS Alliance further underscore the region’s commitment to expanding access to NGS-based personalized oncology care.

The China next-generation sequencing market is growing rapidly, driven by strong government funding, a robust domestic biotech ecosystem, and expanding clinical adoption. Partnerships, such as the June 2025 collaboration between Gene Solutions and Shenzhen USKBio, to establish an NGS laboratory in southern China, underscore efforts to integrate advanced ctDNA and PCR-based diagnostics, improving cancer detection and treatment access.

The next-generation sequencing market in Japan is well established, supported by an aging population, strong government backing for genomic medicine, and advanced healthcare infrastructure. Initiatives led by the Japan Agency for Medical Research and Development (AMED) are accelerating the adoption of NGS in cancer diagnostics and drug discovery. At the same time, domestic companies and research institutions continue to develop sequencing technologies tailored to regional needs.

Middle East & Africa Next-Generation Sequencing Market Trends

The next-generation sequencing market in the Middle East & Africa is developing and shows strong potential due to the increasing government focus on healthcare modernization and precision medicine. Countries such as Kuwait, Saudi Arabia, and the UAE are investing in genomics research and personalized healthcare as part of their national health strategies, which further supports the expansion of the NGS industry.

The Kuwait next-generation sequencing market is an emerging market for NGS, driven by increased investment in healthcare infrastructure and the adoption of personalized medicine. Despite being in an early stage, the municipality-backed genomic research projects and foreign partnerships are laying the groundwork for growth, with the anticipated increase in NGS diagnostics for cancer and rare diseases during the projection period.

Key Next-Generation Sequencing Company Insights

Industry leaders such as Illumina, F. Hoffman-La Roche Ltd., QIAGEN, and Thermo Fisher Scientific, Inc. hold significant market share owing to their advanced sequencing platforms, comprehensive service offerings, and extensive global distribution networks.

Companies like Bio-Rad Laboratories, Inc., Oxford Nanopore Technologies, PierianDx, and Genomatix GmbH are rapidly expanding their footprint by introducing innovative sequencing solutions, bioinformatics tools, and customized services that address the evolving needs of research institutions, clinical laboratories, and pharmaceutical companies.

Organizations such as DNASTAR, Inc., Perkin Elmer, Inc., Eurofins GATC Biotech GmbH, and BGI further enrich the competitive landscape, which continues to drive innovation through cutting-edge technologies and strategic growth initiatives.

The companies that incorporate the latest technological advancements along with the extensive service ecosystems effectively will not only be the ones to provide long-term value but also the ones who will be the driving forces in the future of genomics research, clinical diagnostics, and precision healthcare.

Key Next-Generation Sequencing Companies:

The following are the leading companies in the next-generation sequencing market. These companies collectively hold the largest market share and dictate industry trends.

- Illumina

- F. Hoffman-La Roche Ltd.

- QIAGEN

- Thermo Fisher Scientific, Inc.

- Bio-Rad Laboratories, Inc.

- PacBio

- Oxford Nanopore Technologies

- Revvity, Inc.

- Merck KGaA

- BGI

Recent Developments

-

In July 2025, QIAGEN expanded its NGS portfolio in India by launching QIAseq xHYB Long-Read Panels, enhancing target enrichment capabilities for clinical and translational research in oncology and genetic diseases.

-

In July 2025, Thermo Fisher Scientific enabled precision oncology advancements in the U.S. by launching the Oncomine Comprehensive Assay Plus on the Genexus System, accelerating next-day comprehensive genomic profiling for researchers.

-

In May 2025, Illumina supported a high‑speed, high‑tech NGS laboratory in Australia’s Northern Territory by enabling Territory Pathology to deploy MiSeq and NextSeq systems with cloud‑based analytics, accelerating local pathogen and oncology genomic services.

Next-Generation Sequencing Market Report Scope

Report Attribute

Details

Market size in 2025

USD 11.3 billion

Estimated market size in 2026

USD 13.3 billion

Projected market size by 2033

USD 42.3 billion

Growth rate

CAGR of 18.0% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Technology, product, application, workflow, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; UK; Germany; France; Italy; Spain; Denmark; Sweden; Norway; India; China; Japan; Australia; South Korea; Thailand; Brazil; Argentina; Saudi Arabia; UAE; South Africa; Kuwait

Key companies profiled

Illumina; F. Hoffman-La Roche Ltd; QIAGEN; Thermo Fisher Scientific, Inc.; Bio-Rad Laboratories, Inc.; PacBio; Oxford Nanopore Technologies; Revvity, Inc.; Merck KGaA; BGI

Customization scope

Free report customization (equivalent up to 8 analyst’s working days) with purchase. Addition or alteration to country, regional & segment scope.

Global Next Generation Sequencing Market Report Segmentation

This report forecasts revenue growth and provides an analysis on the latest trends in each of the sub-segments from 2021 to 2033. For this report, Grand View Research has segmented the global next-generation sequencing market report based on the technology, product, workflow, end use, and region:

-

Technology Outlook (Revenue, USD Million, 2021 - 2033)

-

WGS

-

Whole Exome Sequencing

-

Targeted Sequencing & Resequencing

-

DNA-based

-

RNA-based

-

-

Others

-

-

Product Outlook (Revenue, USD Million, 2021 - 2033)

-

Platform

-

Sequencing

-

Data Analysis

-

-

Consumables

-

Sample Preparation

-

Target Enrichment

-

Others

-

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Oncology

-

Diagnostics and Screening

-

Oncology Screening

-

Sporadic Cancer

-

Inherited Cancer

-

-

Companion Diagnostics

-

Other Diagnostics

-

-

Research Studies

-

-

Clinical Investigation

-

Infectious Diseases

-

Inherited Diseases

-

Idiopathic Diseases

-

Non-Communicable/Other Diseases

-

-

Reproductive Health

-

NIPT

-

Aneuploidy

-

Microdeletions

-

-

PGT

-

Newborn Genetic Screening

-

Single Gene Analysis

-

-

HLA Typing/Immune System Monitoring

-

Metagenomics, Epidemiology & Drug Development

-

Agrigenomics & Forensics

-

Consumer Genomics

-

-

Workflow Outlook (Revenue, USD Million, 2021 - 2033)

-

Pre-Sequencing

-

Nucleic Acid Extraction

-

Library Preparation

-

-

Sequencing

-

NGS Data Analysis

-

NGS Primary Data Analysis

-

NGS Secondary Data Analysis

-

NGS Tertiary Data Analysis

-

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Academic Research

-

Clinical Research

-

Hospitals & Clinics

-

Pharma & Biotech Entities

-

Other Users

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

Japan

-

China

-

India

-

South Korea

-

Australia

-

Thailand

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Frequently Asked Questions About This Report

The global next generation sequencing market size was valued at USD 11.3 billion in 2025 and is estimated at USD 42.3 billion for 2026.

The global next generation sequencing market is expected to grow at a CAGR of 18.0% from 2026 to 2033, reaching USD 42.3 billion.

North America dominated with a 44.8% revenue share in 2025.

Key players include Illumina, QIAGEN; Thermo Fisher Scientific Inc.; F Hoffman-La Roche Ltd.; Oxford Nanopore Technologies; Genomatix GmbH; PierianDx; DNASTAR, Inc.; Eurofins GATC Biotech GmbH; Perkin Elmer, Inc.; BGI; and Bio-Rad Laboratories, Inc.

Key factors that are driving the NGS market growth include exponentially decreasing costs for genetic sequencing, development of companion diagnostics and personalized medicine, rise in competition amongst prominent market entities, a rising clinical opportunity for NGS technology, technological advancements in cloud computing and data integration, growing healthcare expenditure, and increasing prevalence of cancer.

Targeted sequencing segment led with a 48.3% revenue share in 2025, while whole exome sequencing is the fastest-growing segment.

Oncology held the largest revenue share 32.0% in 2025, while consumer genomics is the fastest-growing area.

Sequencing segment led with a 64.3% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

About the Author(s)

Biotechnology Research Team

Healthcare · BiotechnologyThis report was authored by the biotechnology research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the biotechnology segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.