- Home

- »

- Communication Services

- »

-

Open RAN Market Size, Share & Trends Report, 2026-2033GVR Report cover

![Open RAN Market (2026 - 2033)Report]()

Open RAN Market (2026 - 2033)

Size, Share & Trends Analysis Report By Component (Hardware, Software, Services), By Unit (Radio Unit, Distributed Unit, Centralized Unit), By Deployment, By Network, By Frequency, By Region, And Segment Forecasts

Market Size, 2025

$6.5BMarket Estimate, 2026

$8.6BMarket Forecast, 2033

$45.1BCAGR, 2026–2033

26.8%Open RAN Market Summary

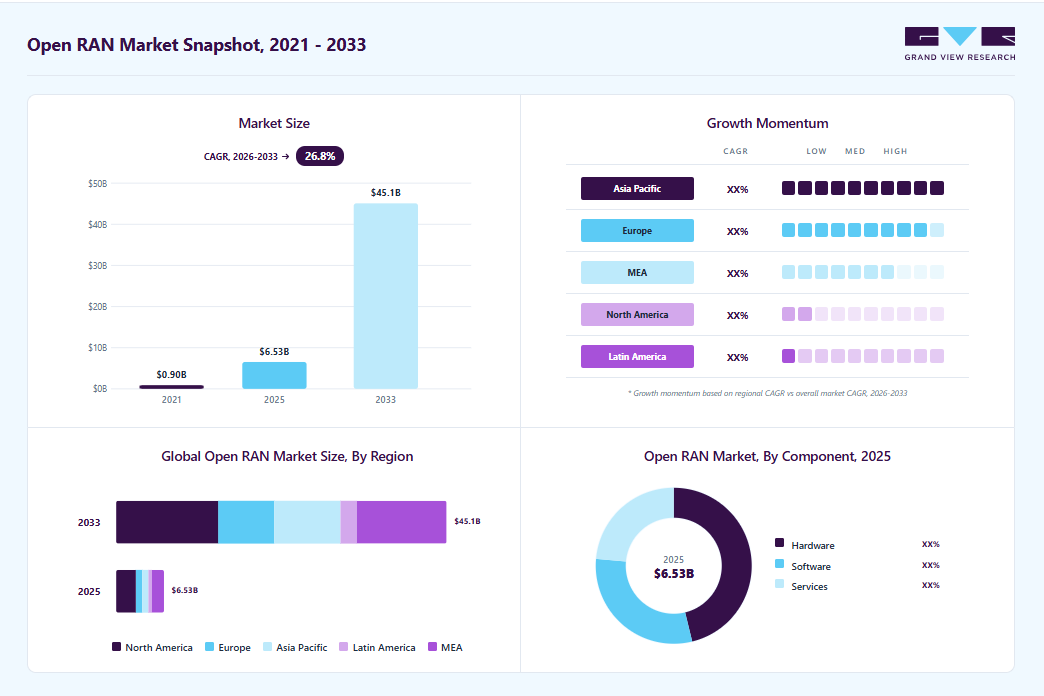

The global open RAN market size was valued at USD 6.5 billion in 2025 and is projected to grow from USD 8.6 billion in 2026 to USD 45.1 billion by 2033, at a CAGR of 26.8% from 2026 to 2033. The market in North America dominated with a revenue share of 41.1% in 2025. An open radio access network, open RAN or O-RAN, is a nonproprietary version of the radio access network (RAN) that allows interoperation between cellular network equipment provided by different vendors.

Key Market Trends & Insights

- By component: Hardware segment held the largest market share of 46.2% in 2025.

- By unit: Distributed unit segment held the largest market share in 2025.

- By deployment: Hybrid cloud segment held the largest market share in 2025.

- By network: 5g segment segment held the largest market share in 2025.

- By frequency: Sub-6 GHz segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: North America (41.1% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 6.5 Billion

- Estimated market size in 2026: USD 8.6 Billion

- Projected market size by 2033: USD 45.1 Billion

- CAGR (2026-2033): 26.8%

Open RAN adoption is accelerating as operators seek cost-efficient alternatives to traditional single-vendor RAN systems. By separating hardware and software, operators gain the flexibility to source lower-cost components from multiple vendors. This reduces both upfront investment and long-term operational expenses. As 5G networks expand and densify, the economic benefits of Open RAN become even more compelling for operators globally.")

The shift toward cloud-native and virtualized architecture is a key growth driver for the Open RAN market. Virtualization allows operators to run RAN functions on standardized hardware using containers and automation tools. This enhances network scalability, agility, and performance while lowering infrastructure costs. More operators are embracing cloud infrastructure and edge computing, which strengthens Open RAN’s technological alignment and increases adoption momentum.

The global rise of 5G deployments, across urban, suburban, and rural areas is increasing demand for flexible RAN solutions. Open RAN supports diverse deployment models that fit varied coverage and capacity needs. Operators are using it for targeted rural coverage, indoor enterprise networks, and selective 5G modernization. The expansion of 5G standalone architecture makes Open RAN a more adaptable and future-ready alternative to traditional RAN systems.

Regulatory support and geopolitical considerations are also driving the Open RAN market forward. Governments, particularly in the U.S. and Europe, are increasingly viewing Open RAN as a strategic approach to enhancing network security and reducing dependency on specific vendors, especially in light of concerns about potential security risks associated with certain foreign suppliers. This endorsement from regulators not only promotes competition but also encourages local and smaller technology vendors to enter the telecom space, fostering innovation and strengthening regional technology ecosystems. As a result, Open RAN is emerging as a crucial component of next-generation telecommunications infrastructure, aligning with broader priorities for security, cost-effectiveness, and flexibility in global markets.

Market growth is being constrained by ongoing concerns related to performance parity, integration complexity, and multi-vendor coordination. Higher technical expertise requirements are being recognized as a barrier, particularly for brownfield operators with complex legacy networks. Limited availability of fully mature, carrier-grade Open RAN solutions is being viewed as a challenge for large-scale nationwide rollouts. Questions around long-term reliability, operational overhead, and ecosystem consistency continue to influence adoption pace.

Market Dynamics

The rapid expansion of 5G infrastructure remains a major driver for the open RAN market, as telecom operators continue modernizing networks to support higher data traffic, low-latency applications, and large-scale IoT connectivity. Open RAN is gaining traction because its architecture is designed to support multi-vendor deployment and interoperability, allowing operators to mix and match components from different suppliers while improving network flexibility and scalability. The O-RAN Alliance states that its specifications are intended to provide the foundation for the industry to supply and innovate in the RAN, while companies of different sizes can use those specifications to build competitive open solutions.

Another important growth factor is the push by governments and industry bodies to diversify telecom supply chains and reduce dependence on single-vendor RAN ecosystems. In the U.S., NTIA (National Telecommunications and Information Administration) launched USD 1.5 billion Wireless Innovation Fund to support more competitive and diverse wireless networks, and later awarded about USD 42.3 million for the ACCoRD open RAN project to advance compatibility and commercialization. NIST (National Institute of Standards and Technology) has also made Open RAN interoperability a research priority, focusing on methods to quantify the way different vendors’ equipment works together and to improve performance in multi-vendor systems. In addition, NIST joined the O-RAN Alliance to help promote stable and diverse supply chains and open standards for next-generation wireless technologies. These initiatives are reinforcing open RAN as a future-ready architecture for 5G network modernization.

Despite growing commercial interest, the Open RAN market continues to face challenges related to integration complexity and operational performance consistency. Unlike conventional RAN systems delivered through tightly integrated single-vendor platforms, Open RAN environments require coordination among multiple hardware, software, semiconductor, and cloud infrastructure providers. This increases the technical complexity associated with deployment, interoperability testing, system validation, and network optimization. Telecom operators require significant engineering expertise and integration resources to ensure stable operation across disaggregated network components.

Performance reliability remains another key concern limiting large-scale open RAN adoption. Operators continue evaluating whether open RAN solutions can consistently deliver carrier-grade network performance comparable to traditional RAN systems, particularly in high-density 5G environments requiring low latency, high throughput, and energy-efficient operations. In addition, compatibility challenges associated with existing legacy telecom infrastructure increase deployment timelines and operational overhead for brownfield operators. Concerns regarding ecosystem maturity, long-term reliability, and standardized interoperability frameworks continue to influence deployment decisions, especially for nationwide network rollouts.

The increasing deployment of private 5G networks across industrial and enterprise environments presents a significant growth opportunity for the open RAN market. Enterprises operating in manufacturing, logistics, mining, transportation, healthcare, and smart-city development are increasingly investing in dedicated wireless infrastructure to support industrial automation, autonomous operations, real-time monitoring, and mission-critical connectivity applications. Open RAN architectures provide enterprises with modular, customizable, and software-driven network solutions capable of supporting diverse operational requirements at lower infrastructure costs compared to conventional proprietary systems.

The growing adoption of edge computing and AI-enabled industrial operations is further strengthening enterprise demand for flexible wireless networking platforms. Open RAN solutions allow organizations to deploy scalable private network environments using virtualized and cloud-based infrastructure optimized for localized data processing and low-latency communication. In addition, governments and industry organizations are increasingly supporting private wireless spectrum allocation and Industry 4.0 initiatives, encouraging broader enterprise adoption of advanced connectivity technologies. As digital transformation initiatives continue expanding across industrial sectors, Open RAN vendors are expected to benefit from rising demand for secure, adaptable, and enterprise-focused wireless network deployments.

Market Concentration & Characteristics

The Open RAN industry is moderately fragmented, with participation from established telecom equipment manufacturers, cloud infrastructure providers, semiconductor companies, and emerging software-focused network vendors. Major industry participants maintain significant market presence through large-scale telecom partnerships, while newer open RAN-focused vendors continue gaining traction through specialized software and virtualization capabilities. The growing involvement of cloud service providers and semiconductor companies is further intensifying market competition and innovation activity.

The market is characterized by rapid technological evolution, increasing adoption of cloud-native architectures, and strong emphasis on interoperability and network virtualization. Vendors are focusing on AI-driven network automation, energy-efficient radio systems, and software-defined network management solutions to improve operational efficiency and performance. Strategic collaborations among telecom operators, chipset manufacturers, system integrators, and software providers are also becoming increasingly common to accelerate Open RAN commercialization and standardization efforts. In addition, governments and telecom regulators are actively supporting domestic telecom ecosystem development, further stimulating investments in open RAN infrastructure and innovation.

Component Insights

The hardware segment dominated the market in 2025 and accounted for the largest share of 46.2%. Open RAN hardware specifically refers to the physical equipment and infrastructure of the radio access network in an open RAN architecture. Some of the common hardware components include baseband units (BBUs), remote radio units (RRUs), and virtualized RAN (vRAN) servers, among others. The O-RAN hardware allows operators to replace legacy 4G/3G/2G systems with fully virtualized Open RAN technology. Moreover, the hardware enables multiple technologies to run simultaneously on the same RRH to provide flexible and superior voice and data services to the end-users, driving the segment’s adoption and growth.

The services segment is expected to register a notable CAGR over the forecast period. The services segment is further bifurcated into consulting, deployment & implementation, and support & maintenance. Since O-RAN is comparatively new technology, network operators need adequate support to ensure the efficiency and operability of the network. In addition, operators and vendors need to be trained in how to use the O-RAN to their maximum advantage. The growing demand for consulting, deployment & implementation, and support & maintenance services is anticipated to propel the segment’s growth over the forecast period.

Unit Insights

The distributed unit segment dominated the market in 2025.The distribution unit converts a signal from one form to another and aggregates all data to be transmitted over a communication channel. The distribution unit takes the digitized radio signal from the radio unit and sends it into the network. The DU is used at the base station for computation, and it plays an important role in transmitting the radio signal, which is anticipated to drive the segment’s growth over the forecast period.

The radio unit segment is expected to grow at a moderate CAGR over the forecast period. The radio unit is an important component of the open RAN architecture. It transmits, receives, amplifies, and digitizes the radio frequency signals. The radio unit is near or integrated into the antenna. The radio unit has significance in the O-RAN market as it enables wireless communication between the user device and the core network. The growing use of radio units to enhance network performance is driving the open RAN radio unit market growth.

Deployment Insights

The hybrid cloud segment dominated the market in 2025. Open RAN's hybrid cloud deployment combines on-premises and cloud infrastructure, optimizing network performance while leveraging scalability and cost efficiency. Hybrid cloud deployment offers the public cloud's flexibility while providing the private cloud's security. Thus, the amalgamation of the two provided by hybrid cloud deployment is contributing to the segment's growth.

The private cloud segment is expected to grow at a notable CAGR over the forecast period.Open RAN's private cloud deployment involves utilizing dedicated cloud infrastructure for enhanced network control and security. The private cloud deployment segment's growth can be attributed to the growing need for tailored solutions, data privacy compliance, and optimal resource utilization. Private cloud deployment offers efficient network management while addressing specific operational requirements of the organization, which is anticipated to drive the adoption of the private cloud segment over the forecast period.

Network Insights

The 5G segment dominated the market in 2025. The majority of network operators and telecom equipment providers are focusing on creating a robust 5G ecosystem. Many countries have already released 5G networks. The shift from 4G to 5G networks is driving open RAN network operators and providers to opt for 5G networks, which is driving the segment’s growth.

The 4G segment is expected to grow at a moderate CAGR over the forecast period.The market has witnessed 4G network deployments primarily due to their established infrastructure and widespread adoption across the globe. The dominant share of the 4G network can be attributed to the compatibility of open RAN solutions with the existing 4G setups. Moreover, the mature technology of 4G has led to significant deployments of Open RAN on the 4G network. Key players are focusing on enhancing and modernizing these networks while maintaining operational efficiency, thus boosting the segment’s growth.

Frequency Insights

The sub-6 GHz segment held the largest market in 2025. The sub-6 GHz frequency enables expansive coverage and better penetration through dense urban areas and rural areas where network connectivity is otherwise slow/poor. Hence, the sub-6 GHz frequency is better suited for urban as well as rural applications. It provides efficient data transmission to improve user experience and fulfills open RAN’s aim to enhance connectivity and accessibility. These benefits are anticipated to drive the market’s growth over the forecast period.

The mmwave segment is expected to grow at the fastest CAGR during the forecast period. The growth of the mmWave segment can be attributed to its ability to bring ultra-fast speeds and high data capacity. Even though mmWave offers network connectivity over a shorter range, the ultra-fast speeds provided by the frequency are driving its adoption in the O-RAN market. Moreover, as 5G expands, mmWave's role within O-RAN becomes more crucial for delivering the high-speed, high-capacity performance users expect in various environments, thus propelling the segment’s growth.

Regional Insights

North America open RAN industry dominated and accounted for a share of 41.1% in 2025. The regional growth can be attributed to several factors, including the presence of prominent key players, such as AT&T, Inc., and the region's technological inclination toward early adoption of advanced solutions. Moreover, the region is witnessing significant investment in telecommunication infrastructure, creating significant growth opportunities for adopting O-RAN. The convergence of these factors has propelled North America to the forefront of Open RAN expansion, fostering the regional market’s growth and development in the market.

U.S. Open RAN Market Trends

The U.S. open RAN market held a dominant position in the region in 2025. The market is witnessing a significant growth, driven by the demand for more flexible and cost-effective network solutions. Major telecom players are actively adopting Open RAN technologies to diversify their network infrastructure and enhance operational efficiency.

Europe Open RAN Market Trends

Europe open RAN market is expected to register a notable CAGR from 2026 to 2033. In Europe, the Open RAN market is experiencing rapid expansion fueled by the continent's push towards the adoption of 5G and the desire for more flexible network architectures. Governments across Europe are investing in improving their networking infrastructure.

The Germany Open RAN market is expected to grow at the fastest CAGR from 2026 to 2033. In Germany major players such as Deutsche Telekom and Vodafone Germany are actively exploring Open RAN solutions to drive network agility and efficiency. For instance, Deutsche Telekom has initiated various pilot projects and collaborations to test Open RAN technology, aiming to leverage its potential for cost reduction and vendor diversification.

The open RAN market in the UK held a substantial market share in 2025. The market is burgeoning as telecom operators embrace this technology to drive network innovation and efficiency. Leading players such as BT Group (including EE) and Vodafone UK are at the forefront of Open RAN trials and deployments across the country. For example, BT Group has launched several initiatives to pilot Open RAN solutions, aiming to enhance network flexibility and reduce vendor lock-in.

Asia Pacific Open RAN Market Trends

The Asia Pacific open RAN market is expected to grow at the fastest CAGR during the forecast period. The region's growth can be attributed to the increasing demand for advanced telecommunication infrastructure, a growing mobile subscriber base, and favorable government regulations. Countries, such as Japan, South Korea, and India, are at the forefront of regional growth due to their technological prowess and growing emphasis on fostering a robust digital ecosystem. All these factors are contributing to the growth of the regional market.

Japan open RAN market is expected to grow at the moderate growth rate during the forecast period. Favorable government initiatives and strategic initiatives by the major providers to boost 5G connectivity are benefiting the growth of the Open RAN market in Japan. Japanese telecom operators are taking initiatives to develop and deploy 5G RAN solutions nationwide, which in turn propelling the growth of the market.

Open RAN market in India is expected to grow at the fastest CAGR from 2026 to 2033. Major players such as Bharti Airtel, Reliance Jio, and Vodafone Idea are actively investing in Open RAN technologies to drive network efficiency and innovation. For instance, Reliance Jio has been at the forefront of Open RAN adoption, deploying it in its nationwide 4G network and preparing for 5G rollout to enhance scalability and cost-effectiveness.

Key Open RAN Company Insights

Some of the key companies in the open RAN industry include Samsung Electronics Co., Ltd., NEC Corporation, Fujitsu Limited, and others. Telefonaktiebolaget LM Ericsson and Nokia Corporation, among others. These companies provide advanced standalone 5G solutions and benefit from government-backed support in 5G infrastructure development. These companies focus on product innovation, R&D, and strategic initiatives such as new product launches, business expansions, partnerships, collaborations, and mergers and acquisitions.

-

Samsung Electronics Co., Ltd. specializes in providing telecommunications equipment. The company has been actively involved in the development and implementation of open RAN solutions, leveraging its expertise in telecommunications and network infrastructure. Besides, Samsung Electronics has a vast global footprint, with subsidiaries, manufacturing facilities, and sales offices in numerous countries. The company distributes its products worldwide with a significant presence in key markets such as the U.S., Europe, China, and emerging markets in Asia, Africa, and Latin America. Samsung Electronics Co., Ltd. invests heavily in research and development to maintain its position as a technology leader.

-

NEC Corporation is a global technology company, renowned for its contributions to various sectors, including IT, telecommunications, and electronics. Established in 1899, NEC Corporation has grown into a multinational corporation with a diverse portfolio of products and services. As for Open RAN, the company has been actively involved in this space. It has been developing open RAN solutions to enable mobile network operators to deploy more flexible and cost-effective radio access networks.

Key Open RAN Companies:

The following are the leading companies in the open RAN market. These companies collectively hold the largest market share and dictate industry trends.

- Mavenir

- NEC Corporation

- Fujitsu Limited

- Nokia Corporation

- Samsung Electronics Co., Ltd.

- Radisys Corporation (Reliance Industries)

- Parallel Wireless

- ZTE Corporation

- AT&T Inc.

- Casa Systems, Inc.

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: NEC Corporation; Fujitsu Limited; Nokia Corporation; Samsung Electronics Co., Ltd.; ZTE Corporation

- These companies are focusing on large-scale Open RAN commercialization through 5G infrastructure expansion, cloud-native RAN development, and strategic telecom operator partnerships.

- The players are actively investing in AI-driven network automation, energy-efficient radio solutions, and virtualized RAN platforms to strengthen their market presence.

- Mature players in the Open RAN market benefit from strong telecom infrastructure expertise, established global customer relationships, and extensive R&D capabilities.

- Their ability to provide end-to-end telecom solutions, including radio units, software platforms, core networks, and system integration services, gives them a competitive advantage in large-scale 5G deployments.

- Despite strong technological capabilities and market recognition, mature Open RAN vendors face intense competition from agile software-centric players and low-cost regional providers.

- Large organizations also encounter slower innovation cycles and operational complexity during the integration of multi-vendor Open RAN ecosystems.

Emerging Players: Radisys Corporation (Reliance Industries); Parallel Wireless; AT&T Inc.; Casa Systems, Inc.

- These players are focusing on innovation-driven growth strategies centered on software-defined networking, virtualized RAN architecture, and Open RAN interoperability solutions.

- The companies are actively engaging in partnerships, pilot deployments, and ecosystem collaborations to strengthen their market positioning.

- Emerging players benefit from higher operational flexibility and faster innovation cycles compared to traditional telecom infrastructure vendors.

- Their cloud-native and software-focused business models enable rapid customization and integration of Open RAN solutions based on operator-specific requirements.

- Emerging Open RAN companies face limitations related to financial scale, global distribution reach, and large-scale deployment experience compared to established telecom equipment providers.

- Many players continue to depend heavily on strategic partnerships and telecom operator collaborations to expand commercially.

Recent Developments

-

In March 2025, o2 Telefónica rolled out its first Cloud RAN network using Ericsson’s technology. This architecture enables telecom operators to run virtualized elements within the radio access network. Customers in Offenbach can access 5G mobile data services through o2 Telefónica. The company, in collaboration with Ericsson, aims to advance the growth of open and interoperable mobile network solutions.

-

In November 2024, Viettel launched a commercial Open RAN 5G network, incorporating core equipment developed in-house. This deployment represents the world’s first O-RAN-based 5G network built on Qualcomm Technologies’ 5G RAN platforms.

Open RAN Market Report Scope

Report Attribute

Details

Market size in 2025

USD 6.5 billion

Estimated market size in 2026

USD 8.6 billion

Projected market size by 2033

USD 45.1 billion

Growth rate

CAGR of 26.8% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Component, unit, deployment, network, frequency and region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; India; Japan; South Korea; Australia; Malaysia; Brazil; KSA; UAE; South Africa

Key companies profiled

Mavenir; NEC Corporation; Fujitsu Limited; Nokia Corporation; Samsung Electronics Co., Ltd.; Radisys Corporation (Reliance Industries); Parallel Wireless; ZTE Corporation; AT&T Inc.; and Casa Systems, Inc.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Open RAN Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global open RAN market report based on component, unit, deployment, network, frequency, and region.

-

Component Outlook (Revenue, USD Million, 2021 - 2033)

-

Hardware

-

Software

-

Services

-

Consulting

-

Deployment and Implementation

-

Support and Maintenance

-

-

-

Unit Outlook (Revenue, USD Million, 2021 - 2033)

-

Radio Unit

-

Distributed Unit

-

Centralized Unit

-

-

Deployment Outlook (Revenue, USD Million, 2021 - 2033)

-

Private

-

Hybrid Cloud

-

Public Cloud

-

-

Network Outlook (Revenue, USD Million, 2021 - 2033)

-

2G/3G

-

4G

-

5G

-

-

Frequency Outlook (Revenue, USD Million, 2021 - 2033)

-

Sub-6 GHz

-

mmWave

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

-

Asia Pacific

-

India

-

Japan

-

Australia

-

South Korea

-

Malaysia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

Kingdom of Saudi Arabia (KSA)

-

UAE

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Open RAN Deployment Strategy Assessment

- Regional 5G infrastructure adoption analysis

- Telecom operator Open RAN readiness evaluation

- Vendor interoperability assessment

- Identified high-growth deployment regions

- Supported telecom infrastructure investment planning

Private 5G and Enterprise Network Analysis

- Industry-wise private network demand analysis

- Enterprise connectivity use-case assessment

- Edge computing and AI integration evaluation

- Supported enterprise network expansion strategy

- Identified emerging industrial opportunities

Competitive Landscape Assessment

- Benchmarking of Open RAN solution providers

- Product and software capability comparison

- Partnership and ecosystem analysis

- Supported competitive intelligence initiatives

- Identified strategic collaboration opportunities

Frequently Asked Questions About This Report

Asia Pacific is the fastest-growing region over the forecast period.

The hardware segment led with a 46.2% revenue share in 2025, while the services segment is the fastest-growing.

The distributed unit segment held the largest revenue share in 2025, while the radio unit segment is the fastest-growing.

The hybrid cloud segment held the largest revenue share in 2025, while the private cloud segment is the fastest-growing.

5g segment segment held the largest share in 2025, while the 4g segment segment is the fastest-growing.

The global open RAN market is expected to grow at a CAGR of 26.8% from 2026 to 2033, reaching USD 45.1 billion by 2033.

North America dominated with a 41.1% revenue share in 2025.

The global open RAN market size was valued at USD 6.5 billion in 2025 and is estimated at USD 8.6 billion for 2026.

Some key players operating in the open RAN market include Mavenir, NEC Corporation, Fujitsu Limited, Nokia Corporation, Samsung Electronics Co., Ltd., Radisys Corporation (Reliance Industries), Parallel Wireless, ZTE Corporation, AT&T Inc., and Casa Systems, Inc.

Open RAN enables operators to choose hardware and software solutions from various vendors, which can lead to reduced equipment and operational costs. The vendor diversity, cost reduction, and flexibility offered by open RAN are anticipated to drive the market's growth over the forecast period.

About the Author(s)

Communication Services Research Team

Technology · Communication ServicesThis report was authored by the communication services research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the communication services segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.