- Home

- »

- Next Generation Technologies

- »

-

Security Market Size, Share & Trends Report, 2026-2033GVR Report cover

![Security Market (2026 - 2033)Report]()

Security Market (2026 - 2033)

Size, Share & Trends Analysis Report By Component (System, Service), By End-use (Commercial, Government, Industrial, Transportation, Others), By Region, And Segment Forecasts

Market Size, 2025

$156.2BMarket Estimate, 2026

$169.1BMarket Forecast, 2033

$270.5BCAGR, 2026–2033

6.9%Security Market Summary

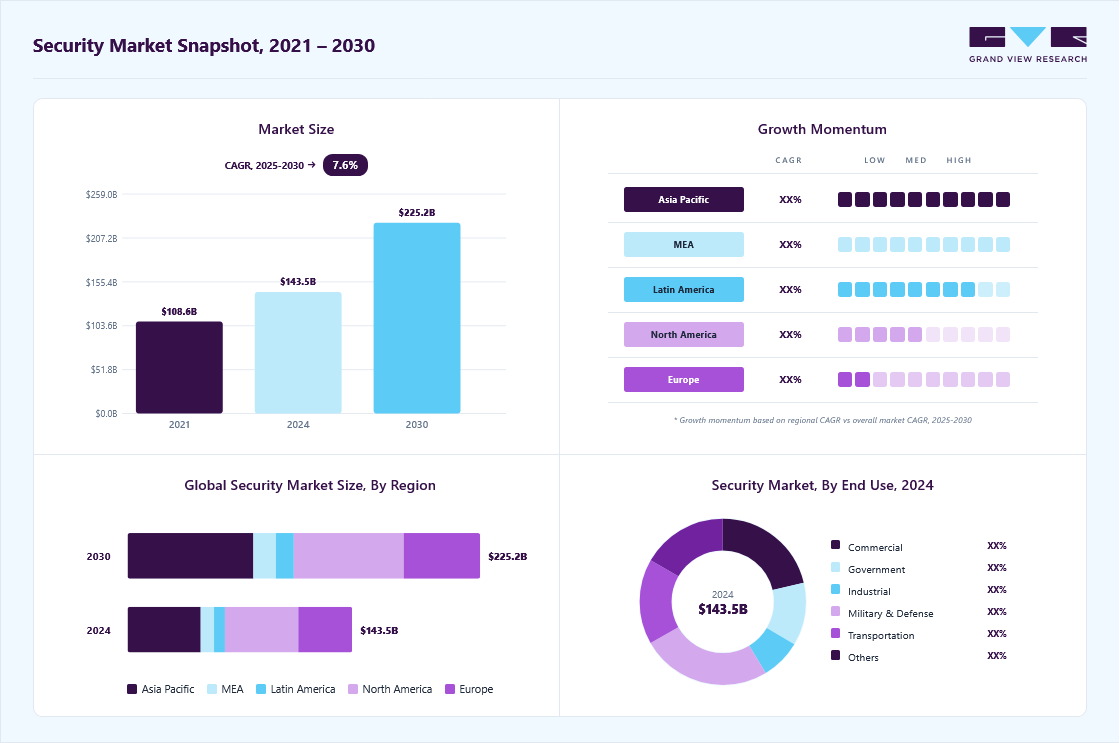

The global security market size was valued at USD 156.2 billion in 2025 and is projected to grow from USD 169.1 billion in 2026 to USD 270.5 billion by 2033, at a CAGR of 6.9% from 2026 to 2033. Asia Pacific dominated the global market with the largest revenue share of 33.1% in 2025. The increasing illegal events, terrorism, and fraudulent activities, across the globe and stringent government norms, has led to a rise in the adoption of security systems.

Key Market Trends & Insights

- By component: System segment led the market with the largest revenue share of 78.0% in 2025.

- By end-use: Military & defense segment led the market with the largest revenue share of 25.4% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (33.1% revenue share, 2025)

- By country: The security market in the China held the largest share in the Asia Pacific region in 2025.

Market Size & Forecast

- Market size in 2025: USD 156.2 Billion

- Estimated market size in 2026: USD 169.1 Billion

- Projected market size by 2033: USD 270.5 Billion

- CAGR (2026-2033): 6.9%

The security systems offer several advantages such as maintaining records for information, monitoring activities in commercial & residential areas and empowering nations against terrorism & external threats at different locations. These systems have significant adoption rates in the military & defense end use industry, owing to the increased threat of terrorism and cross-border intrusions. The security industry is a dynamic and rapidly expanding sector, driven by increasing concerns about physical safety, cybersecurity, and data privacy. As global economies become more interconnected and dependent on Component, the demand for advanced security solutions has surged across various domains, including residential, commercial, industrial, and governmental sectors. The market encompasses a wide range of products and services, such as surveillance systems, access control, cybersecurity tools, biometrics, and integrated solutions powered by artificial intelligence (AI) and Internet of Things (IoT) technologies. These innovations enhance real-time threat detection, streamline responses, and provide predictive analytics to prevent incidents before they occur.")

Rapid technological advancements in the system such as use of security systems linked with internet, has enabled real-time surveillance at remote and critical locations with enhanced accuracy. Furthermore, it has increased the adoption rate of advanced security systems with better product features and improved performance. Also, the reduction of manpower involved in performing critical jobs at perilous locations, and replacing them with surveillance systems, is expected to fuel market growth.

Market Dynamics

The security market is expanding rapidly as organizations face an increasingly complex threat driven by cyberattacks, data breaches, physical security risks, and geopolitical uncertainties. Growing digital transformation, cloud adoption, and the production of connected devices are creating new vulnerabilities that require advanced security solutions, with stricter regulatory requirements and rising awareness of data privacy are compelling enterprises and governments to invest in security infrastructure. The integration of AI, automation, and real-time monitoring technologies is further enhancing threat detection and response capabilities.

The rapid adoption of digital technologies across enterprises is significantly increasing the demand for advanced security solutions. Organizations are transferring critical workloads to cloud environments, digitizing business processes, and enabling remote and hybrid work models, which expand the potential attack surface, making protecting digital assets, networks, applications, and sensitive data a strategic priority for businesses of all sizes.

Furthermore, the growing number of connected devices, including IoT sensors, smart equipment, industrial control systems, and edge computing devices, is creating new security challenges. Each connected endpoint represents a potential entry point for cyber threats if not properly secured. This expanding ecosystem is driving investments in identity management, endpoint protection, network security, and real-time threat monitoring solutions.

As cyber threats become more mature and security infrastructures grow increasingly complex, organizations require highly skilled personnel to monitor, manage, and respond to security incidents effectively. However, the demand for experienced security analysts, threat intelligence experts, and incident response specialists continues to outpace the available talent pool. This skills gap is particularly pronounced in emerging technologies such as cloud security, artificial intelligence-driven security, and zero-trust architectures.

The shortage of expertise often leads to delayed threat detection, slower response times, and underutilization of advanced security solutions, thereby reducing the overall effectiveness of security investments. Many organizations struggle to fully deploy or optimize security platforms due to limited in-house capabilities, while rising competition for skilled professionals increases recruitment and retention costs. Small and medium-sized enterprises are especially vulnerable, as they frequently lack the resources to attract top security talent.

The growing volume and complexity of cyber and physical security threats are creating significant opportunities for AI-powered threat detection solutions. Traditional security systems often struggle to analyze massive amounts of data in real time, whereas artificial intelligence can rapidly identify anomalies, suspicious behavior, and emerging attack patterns. Organizations are increasingly adopting machine learning and behavioral analytics tools to improve threat visibility and reduce response times.

As security operations centers face persistent talent shortages and alert fatigue, autonomous security solutions are becoming increasingly valuable. AI-driven platforms can automate routine monitoring, incident triage, and threat remediation processes, enabling security teams to focus on higher-priority risks. With advancements in generative AI, predictive analytics, and automated response capabilities, vendors have a major opportunity to deliver more proactive, scalable, and cost-effective security solutions across enterprise, government, and critical infrastructure environments.

Market Concentration & Characteristics

The security market exhibits a high degree of innovation, driven by the rapid evolution of cyber threats and the need for advanced protection mechanisms. Vendors continuously invest in artificial intelligence, machine learning, behavioral analytics, zero-trust architectures, and cloud-native security platforms to improve threat detection and response capabilities. The emergence of generative AI security tools, autonomous security operations, and predictive threat intelligence is further accelerating innovation across the industry. As attack surfaces expand with cloud computing, IoT, and hybrid work environments, continuous product development remains a critical competitive differentiator for market participants.

Mergers and acquisitions play an important role in the security market as companies seek to strengthen technology portfolios, expand customer bases, and gain access to specialized security capabilities. For instance, in June 2026, ASSA ABLOY acquired Sentinel Dock & Door, a Canada-based commercial dock and door service provider, as part of its strategy to expand complementary offerings within its core access and entrance systems business. Large cybersecurity providers frequently acquire startups focused on niche areas such as identity security, AI-based threat detection, cloud security, and security orchestration. These transactions help accelerate innovation and enable vendors to offer more integrated security platforms.

Analyst Perspective

The security market is at the center of a powerful convergence of digital transformation, rising cyber threats, expanding investments in critical infrastructure, and increasingly stringent regulatory requirements. As organizations operate across cloud environments, connected devices, hybrid workforces, and complex supply chains, security spending is shifting from a compliance-driven function to a core operational priority. The important competitive advantage will belong to providers that unify the threat intelligence within a single integrated platform, hence, transforming fragmented protection measures into continuous risk visibility and creating long-term customer relationships that support sustained recurring revenue growth.

Component Insights

Based on component, the system segment led the market with the largest revenue share of 78.0% in 2025 and is expected to grow at the fastest CAGR over the forecast period. These systems cater to rising security needs in residential, commercial, and industrial sectors, driven by increasing crime rates and regulatory mandates. Innovations such as AI-driven video analytics, biometric authentication, and IoT-enabled security devices have enhanced the effectiveness and efficiency of security solutions, further boosting demand. Additionally, the integration of cloud-based platforms for real-time monitoring and remote management has made these systems more accessible and scalable. The ongoing investment in smart infrastructure and urbanization projects has also significantly contributed to the segment's growth and prominence.

The service segment is expected to experience the fastest CAGR from 2025 to 2030. Organizations increasingly outsource security functions to specialized providers to address complex threats and reduce operational burdens. Services such as cybersecurity consulting, system integration, risk assessment, and 24/7 monitoring have become critical as businesses prioritize safeguarding digital and physical assets. The surge in cyberattacks, coupled with evolving regulatory requirements, has driven demand for incident response and compliance management services. Additionally, the adoption of subscription-based models for continuous support and updates has made security services more flexible and cost-effective.

End Use Insights

Based on end-use, the military & defense segment led the market with the largest revenue share of 25.4% in 2025. Governments worldwide prioritized modernizing defense capabilities, including advanced surveillance, threat detection, and cybersecurity solutions, to address emerging challenges such as cyber warfare, terrorism, and border security. The integration of cutting-edge technologies like AI, unmanned aerial vehicles (UAVs), and space-based defense systems significantly enhanced operational efficiency and strategic decision-making. Additionally, increased spending on military-grade communication networks and missile defense systems bolstered the segment's growth. As nations focus on strengthening both conventional and hybrid warfare capabilities, the demand for robust, next-generation military and defense solutions continues to fuel this sector's prominence.

")

The transportation segment is expected to witness the fastest CAGR during the forecast period. Increasing threats of terrorism, smuggling, and unauthorized access to critical infrastructure spurred the adoption of advanced security technologies, including surveillance systems, biometric access control, and automated threat detection solutions. Governments and private operators invested heavily in upgrading transit hubs with AI-driven monitoring and integrated screening systems to ensure passenger safety and cargo integrity. The rise in global trade and travel further necessitated robust security protocols to prevent disruptions.

Regional Insights

North America security market held with a revenue share of 32.4% in 2025. The U.S., in particular, leads the market with strong demand for both physical and cybersecurity systems across government, military, commercial, and industrial sectors. Increasing cyber threats, high-profile data breaches, and terrorism concerns have prompted businesses and governments to prioritize security. Furthermore, North America's adoption of cutting-edge technologies such as AI, IoT, and cloud-based security systems has driven innovation and the development of more sophisticated solutions.

U.S. Security Market Trends

The security industry in the U.S. dominated the regional industry in 2024. Rising concerns over cyberattacks, terrorism, and national security threats have driven significant investments in advanced security technologies, including AI-powered surveillance, biometric access control, and cybersecurity systems. The U.S. is also home to numerous leading security solution providers and has a strong focus on research and development, fostering innovation.

Europe Security Market Trends

The growing demand for security in Europe is attributed to regional businesses' strong focus on innovation, robust government support, and strategic initiatives to enhance technological infrastructure. With rising threats of cyberattacks, terrorism, and geopolitical instability, European nations have prioritized the adoption of advanced security technologies in both public and private sectors. The demand for surveillance systems, access control, and cybersecurity solutions is growing across industries such as banking, critical infrastructure, and transportation. Additionally, the European Union’s stringent data protection regulations, such as the GDPR, have further spurred investments in secure systems.

Asia Pacific Security Market Trends

Asia Pacific dominated the security market with the largest revenue share of 33.1% in 2025. As countries like China, India, and Japan invest heavily in infrastructure development, the demand for advanced security systems, including surveillance, access control, and cybersecurity solutions, has surged. The rise in digital transformation across businesses and government sectors in the region has further fueled the need for robust cybersecurity measures. Additionally, rising concerns about terrorism, political instability, and border security have led to greater adoption of both physical and digital security technologies. The rapid growth of smart cities and IoT integration also contributes to the region's substantial market share in security solutions.

China Security Market Trends

The security market in the China held the largest share in the Asia Pacific region in 2025. The China security market is witnessing steady expansion supported by rapid urbanization and large-scale infrastructure development. Government-led smart city programs are accelerating the deployment of advanced surveillance and monitoring systems across major cities. AI-powered video analytics and facial recognition technologies are increasingly integrated into security solutions for real-time threat detection. Demand is growing across commercial, residential, and industrial sectors for integrated security platforms combining physical and digital protection. Cybersecurity integration with physical security systems is gaining importance due to rising concerns over data protection and network vulnerabilities.

Key Security Company Insights

Some key companies in the security industry include ASSA ABLOY; Apex Fabrication & Design, Inc.; and Apex Perimeter Protection.

-

ASSA ABLOY is a global leader in the security industry, specializing in access solutions, including locks, doors, and entrance systems. The company operates in more than 70 countries and is renowned for its innovative products in both physical and electronic security. ASSA ABLOY offers a wide range of solutions, from traditional mechanical locks to smart locks, access control systems, and key management solutions. The company serves various sectors, including residential, commercial, industrial, and institutional markets. With a strong emphasis on innovation and technology, ASSA ABLOY integrates IoT, cloud-based systems, and biometrics to provide secure, efficient, and scalable solutions.

-

Apex Perimeter Protection is a company specializing in advanced security solutions designed to protect the perimeters of critical infrastructure, properties, and high-security sites. The company focuses on providing robust physical security systems such as fencing, gates, barriers, and surveillance technologies to prevent unauthorized access and safeguard assets. Apex Perimeter Protection integrates cutting-edge technologies, including motion detection, video surveillance, and access control systems, to deliver comprehensive security solutions that can be tailored to various industries, including government, military, commercial, and residential sectors. Their services often include custom installations and ongoing maintenance, ensuring that perimeter security remains effective and adaptable to evolving threats. Apex's expertise in perimeter security solutions has established it as a key player in the global security industry.

Key Security Companies:

The following are the leading companies in the security market. These companies collectively hold the largest market share and dictate industry trends.

-

ASSA ABLOY

-

Apex Fabrication & Design, Inc.

-

Apex Perimeter Protection

-

Anixter Inc.

-

Perimeter Protection Germany GmbH

-

Johnson Controls

-

Honeywell International, Inc.

-

ZABAG Security Engineering GmbH

-

Teledyne FLIR LLC

-

Axis Communications AB

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (ASSA ABLOY, Johnson Controls, Honeywell International, Inc., Teledyne FLIR LLC, Axis Communications AB)

Focus on integrated security portfolios combining physical security and cybersecurity capabilities.Expand through acquisitions, global distribution networks, and long-term enterprise contracts.

Strong brand recognition, extensive installed customer base, and broad geographic presence.Significant R&D resources enabling continuous product innovation and platform integration.

Large organizational structures can slow product development and deployment cycles.Higher solution costs may limit penetration among small and mid-sized customers.

Emerging Players (Apex Fabrication & Design, Inc., Apex Perimeter Protection, Perimeter Protection Germany GmbH, ZABAG Security Engineering GmbH)

Concentrate on specialized security, including perimeter protection, fencing systems, and site-specific solutions.Focus on customized deployments and project-based engagements for targeted customers.

Greater flexibility in addressing unique customer requirements and industry-specific applications.Strong expertise in niche security domains with focused product offerings.

Limited global reach and smaller networks than those of established competitors.Lower financial resources may constrain expansion and technology development initiatives.

Recent Developments

-

In August 2024, Robert Bosch GmbH, a leading provider of innovative security and safety solutions, launched its India assembly line for video systems, featuring the FLEXIDOME IP Starlight 5000i cameras. This strategic initiative underscores Bosch India's commitment to localization and strengthens its position across various product verticals.

-

In May 2024, Hanwha VisionCo., Ltd. launched the AIB-800, an AI Box designed to transform any standard ONVIF-compatible video surveillance camera into an AI-powered analytics camera. The AI Box offers a cost-effective solution for businesses to upgrade their existing camera systems, allowing them to harness the advantages of AI without the need for system modifications or the complexities of full equipment replacement, according to the company.

-

In January 2024, Johnson Controls, the U.S.-based global leader in smart security solutions, launched its latest range of advanced security cameras, the Ilustra Standard Gen3. Designed and manufactured in India with over 75 percent localization, this new product line aligns with the company’s goal to fully produce its security solutions within the country in the coming years, supporting the government’s Make-in-India initiative.

Security Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 156.2 billion

Estimated market size in 2026

USD 169.1 billion

Projected market size by 2033

USD 270.5 billion

Growth rate

CAGR of 6.9% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Component, end-use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; Japan; India; South Korea; Australia; Brazil; Saudi Arabia; South Africa; UAE

Key companies profiled

ASSA ABLOY; Apex Fabrication & Design, Inc.; Apex Perimeter Protection; Anixter International, Inc.; Perimeter Protection Germany GmbH; Johnson Controls., Honeywell International, Inc.; ZABAG Security Engineering GmbH; Teledyne FLIR LLC; Axis Communications AB.

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Security Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest trends in each of the sub-segments from 2017 to 2030. For this report, Grand View Research has segmented the global security market report based on component, end use, and region:

-

Component Outlook (Revenue, USD Million, 2021 - 2033)

-

System

-

Access Control Systems

-

Alarm & Notification Systems

-

Intrusion Detection Systems

-

Video Surveillance Systems

-

Barrier Systems

-

Others

-

-

Service

-

System Integration & Consulting

-

Risk Assessment & Analysis

-

Managed Security Services

-

Maintenance & Support

-

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Commercial

-

Government

-

Industrial

-

Military & Defense

-

Transportation

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

Australia

-

South Korea

-

-

Latin America

-

Brazil

-

-

Middle East and Africa

-

UAE

-

KSA

-

South Africa

-

-

Research Methodology

Segment Definition

Segment - Component

Revenue capture definition

System

Revenue generated from systems includes sales of hardware and software platforms designed to prevent, detect, monitor, and respond to security threats across physical and digital environments. This segment captures revenue by enterprises and government organizations.

Service

Revenue generated from services includes consulting, integration, deployment, monitoring, maintenance, managed security, and incident response activities provided by security vendors and third-party service providers. This segment captures recurring and project-based revenue that support the effective utilization of security technologies.

Segment - End-use

Revenue capture definition

Commercial

Revenue from the commercial segment includes security solutions deployed across offices, retail stores, data centers, hospitality facilities, educational institutions, and corporate campuses. It covers spending on cybersecurity software, and managed security services used to protect business operations and assets.

Government

This segment captures spending by federal, state, and local government agencies on cybersecurity infrastructure, public safety systems, identity management solutions, and critical infrastructure protection. Revenue is driven by national security priorities, data protection mandates, and modernization of government IT environments.

Industrial

Industrial revenue includes security solutions deployed across manufacturing facilities, energy plants, utilities, mining operations, and industrial automation environments. Adoption is influenced by the need to secure operational technology (OT) networks, industrial control systems, and connected production assets from cyber and physical threats.

Military & Defense

The military and defense segment comprises expenditures on advanced cybersecurity systems, intelligence security platforms, secure communications, surveillance technologies, and defense-grade protection solutions. Market revenue reflects ongoing investments in safeguarding defense networks, classified information, and mission-critical infrastructure.

Transportation

Revenue within the transportation segment is derived from security deployments across airports, railways, seaports, logistics hubs, and public transit networks. Organizations invest in surveillance, access management, threat monitoring, and cybersecurity solutions to maintain operational continuity and passenger safety.

Others

The others segment includes security spending across healthcare institutions, educational facilities, residential complexes, entertainment venues, and non-profit organizations. Revenue generation is supported by increasing awareness of cyber risks, physical security requirements, and protection of sensitive operational data.

Estimation Model

Each layer progressively narrows the population pool and applies a conversion rate to arrive at addressable revenue.

Audience Layer

Deployment Layer

Protection Layer

Monetisation Layer

Who Needs Security Solutions?

Who deploy Security Solutions?

How Much Security Is Utilized?

How Much Revenue Is Generated?

Identify consumers open to security risks. Calculate the installed base of assets and environments that require protection.

Apply security adoption rates and evaluate deployment, identity management platforms, and managed security services among target users.

Measure the breadth and intensity of security implementation through protected endpoints and service utilization levels.

Apply average spending per customer and aggregate revenues across software and hardware deployments to estimate total market revenue.

Delivered Customizations

This report has been delivered with the following In-depth customizations

CLIENT REQUEST

CUSTOMIZATION DELIVERED

VALUE ADDS

Market Entry & Expansion Assessment

• Regional demand sizing and forecasting

• Customer segmentation and buying behavior analysis

• Competitive landscape benchmarking

• Regulatory and distribution channel assessment

• Identified high-growth market opportunities

• Supported go-to-market strategy development

• Highlighted investment priorities and risks

• Enabled data-driven expansion planning

Technology & Innovation Assessment

• Emerging technology trend analysis

• Innovation pipeline

• Technology adoption readiness assessment

• Ecosystem and partnership mapping

• Identified future growth areas

• Supported innovation roadmap planning

• Evaluated commercialization potential

• Strengthened strategic partnership decisions

Product Positioning & Competitive Intelligence

• Product benchmarking and feature comparison

• Pricing and value proposition analysis

• Brand perception and customer preference study

• Competitor strategy evaluation

• Improved product differentiation strategy

• Supported pricing optimization

• Identified unmet customer needs

• Enhanced competitive positioning

Frequently Asked Questions About This Report

Key factors driving the growth of the security market include the increasing incidence of criminal activities, terrorism, and fraud worldwide, stringent government regulations and public safety mandates, the rapid development of smart city projects requiring advanced surveillance and monitoring solutions, and growing investments in critical infrastructure protection and cybersecurity systems.

The global security market size was estimated at USD 156.2 billion in 2025 and is expected to reach USD 169.1 billion in 2026.

The global security market is expected to grow at a compound annual growth rate of 6.9% from 2026 to 2033 to reach USD 270.5 billion by 2033.

Prominent players dominating the security market include ASSA ABLOY; Apex Fabrication & Design, Inc.; Apex Perimeter Protection; Anixter International, Inc.; Perimeter Protection Germany GmbH; Johnson Controls., Honeywell International, Inc.; ZABAG Security Engineering GmbH; Teledyne FLIR LLC; Axis Communications AB.

The System segment led with a 78.0% revenue share in 2025, while Service is the fastest growing segment.

Military & defense segment led the market with the largest revenue share of 25.4% in 2025.

Asia Pacific dominated the security market with a share of 33.1% in 2025. The rise in digital transformation across businesses and government sectors in the region has further fueled the need for robust cybersecurity measures.

The video surveillance systems segment led the market with a 47.0% revenue share in 2025, while the intrusion detection systems segment is witnessing significant growth during the forecast period.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.