- Home

- »

- Medical Devices

- »

-

Orthopedic Implants Market Size & Share Report, 2026-2033GVR Report cover

![Orthopedic Implants Market (2026 - 2033)Report]()

Orthopedic Implants Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product (Lower Extremity Implants, Spinal Implants, Dental Implants, Upper Extremity Implants), By Material, By Distribution Channel, By End Use, By Region, And Segment Forecasts

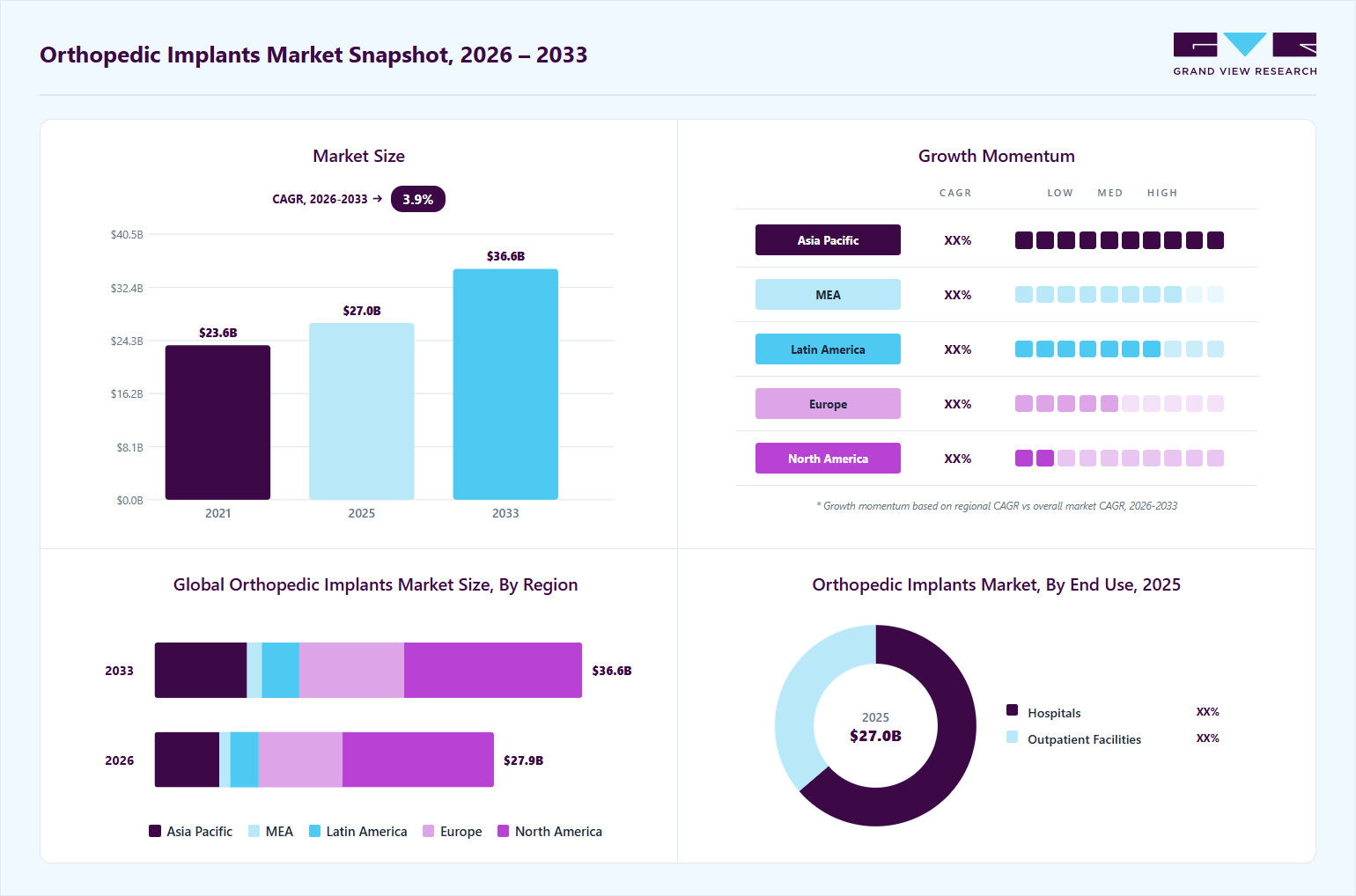

Market Size, 2025

$27.0BMarket Estimate, 2026

$27.9BMarket Forecast, 2033

$36.6BCAGR, 2026–2033

3.9%Orthopedic Implants Market Summary

The global orthopedic implants market size was valued at USD 27.0 billion in 2025 and is projected to grow from USD 27.9 billion in 2026 to USD 36.6 billion by 2033, growing at a CAGR of 3.9% from 2026 to 2033. North America dominated the market with the largest revenue share of 45.1% in 2025. The market is driven by the growing prevalence of reduced bone density, weakened bones, and musculoskeletal disorders.

Key Market Trends & Insights

- By product: Lower extremity implants segment held the largest market share of 52.1% in 2025.

- By material: Metallic material segment held the largest market share of 46.4% in 2025.

- By distribution channel: Offline segment held the largest market share of 83.9% in 2025.

- By end-use: Hospitals segment held the largest market share of 63.7% in 2025.

Regional Highlights

- Largest regional market: North America (45.1% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 27.0 Billion

- Estimated market size in 2026: USD 27.9 Billion

- Projected market size by 2033: USD 36.6 Billion

- CAGR (2026-2033): 3.9%

")

The surging risk of degenerative bone disorders is another factor driving market growth over the forecast period. In addition, the availability of advanced orthopedic implants and the rapid development of healthcare infrastructure globally are expected to positively impact market growth.Market Dynamics

The market is driven by the growing prevalence of reduced bone density, weakened bones, and musculoskeletal disorders. The surging risk of degenerative bone disorders is another factor driving market growth over the forecast period. In addition, the availability of advanced orthopedic implants and the rapid development of healthcare infrastructure globally are expected to positively impact market growth.

The growing penetration of robots in orthopedic procedures is further supplementing the growth of the orthopedic implants market. For instance, in March 2025, Stryker Corporation reported that Mako SmartRobotics system has been used in over 1.5 million procedures globally, reflecting significant expansion in robotic-assisted hip and knee surgeries worldwide. Companies investing in robotics are Stryker Corporation, Zimmer Biomet, Mazor Robotics, Smith & Nephew, Medtronic plc, Think Surgical, OMNlife Science Inc., Intuitive Surgical, and Verb Surgical. In addition, companies are increasingly receiving approvals for surgical robots, further driving the market’s growth. For instance, in July 2024, Think Surgical has received multiple FDA 510(k) clearances for its TMINI Miniature Robotic System, including expanded compatibility with additional knee implant systems. The TMINI platform features a wireless robotic handpiece designed to improve precision during total knee arthroplasty.

Orthopedic Implants Market: Product Pipeline Analysis

Product

Company

Pipeline Phase

Smart Implants

Uteshiya Medicare

N/A

REMEOS Trauma Screw

Bioretec

FDA 510(k) Clearance / Classification

Smaller Diameter

SI-BONE Inc

FDA 510(k) Clearance

Aging Population is Driving the Orthopedic Implants Demand

The global demand for orthopedic solutions is rising due to an aging population and age-related conditions such as bone loss, reduced bone density, arthritis, and weakened ligaments. According to WHO article published in February 2025, the number of people aged 60 years or older worldwide is projected to grow from approximately 1.1 billion in 2023 to about 1.4 billion by 2030, meaning one in six people globally will be aged 60 or above by 2030. This older population is expected to double to around 2.1 billion by 2050, reflecting a sustained increase in longevity and a significant rise in age associated health conditions. This shift contributes to the growing prevalence of orthopedic ailments and drives increased demand for surgical interventions and implants.

")

Growing use of Smart Implants in the Market

Advancements in orthopedic implants, healthcare infrastructure, and minimally invasive surgical techniques are driving market growth. Smart implants, which monitor real-time data such as pressure and strain, enable better clinical decisions and are increasingly used in procedures such as spine fusion and fracture fixation. For instance, in July 2023, Parkview Regional Medical Center and Orthopedics Northeast, in collaboration with Integrum, launched Indiana’s first osseointegration program using the OPRA Implant System-highlighting progress in bone-anchored prosthetics.

Some of the technologies used by companies for smart implants- Verasense: A sensor-based device for Total Knee Arthroplasty (TKA), providing real-time data to help surgeons optimize knee balance and stability during surgery without disrupting workflow.

- Sensor for the Spine: Intellirod Spine's LOADPRO and ACCUVISTA offer intraoperative and postoperative monitoring of spinal cord strain, helping achieve balance during fusion surgeries and tracking strain asymmetry afterward.

Technological Advancements in Orthopedic Implants Market

Digital tools are transforming orthopedic care by enabling real-time patient monitoring, enhancing rehabilitation outcomes, and supporting data-driven clinical decisions. These technologies promote personalized treatment, boost patient engagement, and streamline communication between patients and providers. The growing demand for orthopedic apps and software solutions is further fueling market growth, as they offer benefits such as improved practice management and better clinical outcomes. Popular platforms supporting this shift include Exer Health, iOrtho+, PeekMed Orthogeriatrics, AO Surgery Ref., myrecovery, OrthoClass, Ortho Traumapedia, and DrawMD Ortho.

List of orthopedic apps that can help enhance patient care and educational resources in practice through advanced technology.

App Name

Description

Pros

Cons

Use Cases

Pricing

Exer Health

An AI-driven app measuring patient mobility and participation in Home Exercise Protocols (HEPs) postorthopedic surgery

- Run higher-quality in-person sessions with less effort

- Collect more nuanced and reliable data

- Requires in-depth knowledge of orthopedic practices

- Perfect for orthopedic surgeons & residents and physical therapists.

- Subscription-based model

Rising Sports Participation and Related Injuries

The rising number of people participating in sports and physical activities is directly linked to an increase in sports-related injuries that require medical attention, which is expected to further supplement the market's development. According to the Safe Kids Lincoln-Lancaster County article published in January 2026 , about 30 million children and adolescents participate in organized sports each year, with more than 3.5 million young people (ages 14 and under) sustaining injuries annually while playing sports or engaging in recreational activities. Moreover, as per the Stanford Medicine Children’s Health article published in January 2026, of these, an estimated over 775,000 children in this age group are treated in emergency rooms for sports-related injuries annually. The most common injury types include sprains, strains, bone or growth plate injuries, and overuse injuries resulting from both formal organized sports and informal recreational activity.

Investment Trends in Orthopedics

Investment activity in the orthopedic sector and related musculoskeletal care technologies has shifted in recent years, with a stronger focus on later stage funding and strategic transactions rather than broad early stage venture rounds. For instance, in June 2025, Sword Health secured USD 40 million in new funding at a USD 4 billion valuation, led by General Catalyst and maintained by multiple healthcare investors, strengthening confidence in AI-enabled care models that integrate digital therapy and musculoskeletal solutions.

In addition to funding rounds, consolidation remains a key trend as companies seek scale and expanded service offerings. In January 2026, Sword Health acquired Kaia Health for USD 285 million, a move aimed at enhancing its digital musculoskeletal and AI-powered care platform and expanding its market reach in the U.S. and Europe. This acquisition emphasizes investor preference for strategic deals and technology driven businesses that deliver scalable, profitable growth in orthopedic care and related digital health services.

The FDA heavily regulate the orthopedic implants market to ensure patient safety and product efficacy. However, these regulations create significant barriers for manufacturers, leading to a lengthy and costly approval process for new orthopedic implants. Regulatory compliance involves ongoing quality assurance and adherence to Good Manufacturing Practices (GMP) standards, adding further complexity and costs to the manufacturing process. This can lead to delays, fines, or even product recalls, jeopardizing manufacturers' reputations and market viability. Small- and medium-sized manufacturers may need help navigating these regulations and affording associated costs, limiting their ability to innovate & compete.

The stringent regulatory framework also hampers innovation and competition within the orthopedic implants market. This can limit patients' access to new and advanced orthopedic implant options. Moreover, the variability in regulatory requirements across different regions complicates market entry and expansion, especially for companies with limited resources or those operating on a smaller scale. This can further hinder innovation and competition within the market.

Market Concentration & Characteristics

The treatment of orthopedic conditions and injuries has been significantly transformed by recent advancements in the field of orthopedic implants. Advanced techniques such as 3D printing in orthopedic care provide new opportunities for patient-specific implants, which eliminate the need for off-the-shelf implants. Furthermore, market players are investing in innovative technologies and procedures to keep up with the demand. For instance, in February 2023, Medline announced the launch of its UNITE Ankle Fusion Plating System, offering innovative features to aid foot and ankle surgeons in treating patients with ankle-related conditions.

The orthopedic implants market is characterized by a high level of merger and acquisition (M&A) activity by the leading players, owing to several factors, including the desire to expand the business to cater to the growing demand for orthopedic implants and to maintain a competitive edge. In February 2024, SATO Europe GmbH collaborated with Medacta, a Swiss-based pioneer in orthopedic implants, to optimize the logistics of orthopedic implantation using PJM RFID technology.

Orthopedic implants must meet strict regulatory requirements to ensure high quality, safety, and effective standards before are introduced to the market. In the U.S., the U.S. FDA regulates orthopedic medical devices. The FDA and EMA agencies heavily regulate the orthopedic implants market to ensure patient safety and product efficacy. However, these regulations create significant barriers for manufacturers, leading to a lengthy and costly approval process for new orthopedic implants. Furthermore, the stringent regulatory framework also hampers innovation and competition within the orthopedic implants market. This limit patients' access to new and advanced orthopedic implant options.

Substitutes of orthopedic implants are non-surgical treatment options, such as physiotherapy, drug therapy, and allied product options. Moreover, technologically advanced products are likely to be considered as a substitute. The threat of substitutes is expected to be moderate in the industry because, even though substitutes are available for orthopedic implants, some key products still hold a strong place and are growing in demand because of established clinical evidence.

Several market players are expanding their business by entering new geographical regions to strengthen their market position and expand their product portfolio. In September 2025, Zimmer Biomet announced plans to establish a new manufacturing plant in Grecia, Costa Rica, marking its first greenfield investment in nearly two decades. The highly automated facility is expected to produce components for knee and hip implants, reflecting the company’s strategic commitment to global operational expansion and supply chain diversification.

Analyst Perspective

The global orthopedic implants market continues to benefit from rising musculoskeletal disorders, increasing prevalence of osteoarthritis, growing demand for joint replacement procedures, and an expanding geriatric population. Advancements in implant materials, minimally invasive surgical techniques, and robotic-assisted orthopedic procedures are improving implant longevity, surgical precision, and patient outcomes. Additionally, increasing participation in sports and physical activities is driving demand for trauma, extremity, and sports medicine implants across both developed and emerging healthcare markets.

The market's competitive dynamics are increasingly shaped by technological innovation and procedural efficiency. Robotic-assisted surgery, computer-assisted navigation, 3D-printed implants, patient-specific instrumentation, and smart implant technologies are becoming key differentiators among leading manufacturers. Healthcare providers are also prioritizing solutions that reduce revision rates, shorten hospital stays, and support value-based care initiatives. As orthopedic procedures continue shifting toward ambulatory surgical centers and outpatient settings, manufacturers that combine comprehensive implant portfolios, strong surgeon relationships, advanced surgical technologies, and global commercialization capabilities will be best positioned to capture long-term growth opportunities in the evolving orthopedic implants market.

Product Insights

By product, the lower extremity implants segment held the largest market share of 52.1% in 2025. However, the dental implants segment is anticipated to witness the fastest growth with a CAGR over the forecast period. The growth is attributed to the aging population, increasing prevalence of orthopedic conditions, advancements in implant materials & designs, and the growing demand for improved quality of life through surgical interventions. In addition, the number of R&D initiatives by manufacturers is increasing to enhance these implants’ longevity, functionality, & biocompatibility through innovative materials and minimally invasive surgical techniques. For instance, in October 2023, DePuy Synthes, a company within the Johnson & Johnson Medical Devices Companies, received FDA clearance for the TRILEAP Lower Extremity Anatomic Plating System. This system is designed to aid in the treatment of various lower extremity conditions, providing orthopedic surgeons with advanced tools to address patient needs effectively.

The dental implants product type segment in orthopedic implants market is anticipated to witness the fastest growth with a CAGR over the forecast period. The rising incidence of dental injuries due to car accidents and sports injuries is one of the key factors boosting the need for dental implants. According to a report by the American Academy for Implant Dentistry in November 2023, about 3 million people in the U.S. currently have dental implants, with approximately 500,000 additional implants placed each year, reflecting strong and growing clinical adoption of implant-based restorative solutions. These procedures help preserve jawbone structure and provide a stable foundation for crowns, bridges, and full arch restorations, making dental implants a preferred long term treatment for tooth loss.

Material Insights

By material, metallic material segment held the largest market share of 46.42% in 2025. However, the polymeric biomaterials segment is expected to register fastest growth over the forecast period, owing to the high preference for hospitals in case of any injury. The metallic material segment is further classified into stainless steel, titanium, titanium alloy, cobalt alloy, and others. Stainless steel is favored in orthopedic applications due to its excellent strength, corrosion resistance, and biocompatibility, making it suitable for various implants such as plates, screws, and rods used in fracture fixation and joint replacement surgeries. For instance, the mechanical strength of stainless steel allows it to withstand the stress encountered in load-bearing applications within the human body, which is crucial for ensuring the longevity and effectiveness of implants.

The polymeric biomaterials segment is expected to register fastest growth over the forecast period. The advanced polymers such as ultra-high molecular weight polyethylene (UHMWPE) continue gaining traction in hip, knee, and spine applications due to their low density, good biocompatibility, and reduced stress shielding compared with metal alloys. UHMWPE has a long clinical history in orthopedic bearings and continues to evolve with antioxidant stabilized formulations to improve wear resistance and long-term performance. While research expands into bioabsorbable polymers and composite materials, polymeric biomaterials are increasingly explored for applications beyond traditional load bearing roles.

Distribution Channel Insights

By distribution channel, the offline segment held the largest market share of 83.9% in 2025. The online segment is expected to register fastest growth over the forecast period. The physical infrastructure where these procedures occur, namely hospitals and surgical centers, is expanding, especially in emerging economies. The increasing number of hospitals, coupled with government initiatives aimed at improving the quality of healthcare and the development of private enterprises offering modern healthcare facilities, directly drives the need for effective physical distribution channels to supply these institutions with the necessary implants.

The online segment is expected to register fastest growth over the forecast period due to the increasing demand for convenient and efficient purchasing options among healthcare providers and patients. With the rise of e-commerce, hospitals and clinics are turning to online platforms to streamline their procurement processes, allowing them to quickly access a wide range of products without the need for extensive in-person negotiations or lengthy supply chain delays. For instance, companies such as Stryker and Zimmer Biomet have begun offering their products through online portals, enabling healthcare professionals to order implants directly from manufacturers with ease.

End Use Insights

By end use the hospitals segment held the largest market share of 63.73% in 2025 and is expected to witness the fastest growth during the forecast period from 2026 to 2033. The growth is attributed to the high preference for hospitals in case of any injury. This trend is especially observed in developing countries. Furthermore, the rising number of hospital admissions in case of bone fractures and injuries caused by road accidents is estimated to boost market growth. Favorable reimbursement policies for patients who visit hospitals as compared to those seeking treatment at outpatient facilities and presence of a large number of hospitals & primary care centers in developed & developing economies are key factors that are attributed to the high demand for hospitals. The segment is expected to witness the fastest growth during the forecast period from 2024 to 2030.

The orthopedic implants market is expected to experience significant growth in the outpatient facilities segment over the forecast period. This is due to the increasing preference for day care centers and ambulatory surgery centers in surgical procedures. Outpatient facilities offer advantages such as reduced waiting times, quick discharge, lower procedural costs, and improved efficiency. In addition, they provide patients with adequate postoperative pain control, rapid discharge, minimal side effects, and overall cost containment.

Regional Insights

North America dominated the orthopedic implants market with the largest revenue share of 45.1% in 2025. The growth is attributed to the growing need for advanced healthcare services, owing to the presence of major industry players, well-established healthcare infrastructure, and comprehensive reimbursement coverage. Moreover, the growing number of middle-aged & geriatric patients opting for orthopedic implants, increase in prevalence of low bone density, and introduction of biodegradable implants & internal fixation devices also drive the regional market.

U.S. Orthopedic Implants Market Trends

The orthopedic implants market in the U.S. held the largest share in the North America region in 2025. The U.S. market for orthopedic implants is driven by factors such as an increase in healthcare expenditure across the globe and rise in the applications of 3D printing in the healthcare sector. The need for regulatory compliance and the requirement of high capital investment restricts the entry of new players into the market. Companies offering various types of implants are increasingly adopting expansion strategies, such as product launches, mergers, acquisitions, partnerships, and collaborations. For instance, in March 2023, Bioretec Ltd received FDA approval for its bioresorbable metal product, RemeOs trauma screw, for the healing of bone fractures. This product is a combination of traditional surgical techniques with the latest bioresorbable polymer implants, which is patient-friendly and eliminates the need for implant removal operations.

Canada orthopedic implants market is anticipated to register the fastest growth rate during the forecast period. Market players are concentrating on boosting R&D efforts to introduce advanced products and maintain their market position through various strategies. In February 2024, Tyber Medical LLC, an orthopedic device manufacturer, received clearance from Health Canada for its anatomical plating system. The plating system includes a comprehensive range of titanium and stainless-steel plates.Previously, the portfolio had received clearance for FDA 510(k) in the U.S.

Europe Orthopedic Implants Market Trends

Europe orthopedic implants market is anticipated to register significant growth rate during the forecast period. This is attributed to several factors including increased healthcare spending as well as a rise in the number of elderly people suffering from osteoarthritis, osteoporosis, bone injuries, and obesity. According to Eurostat, as of January 2023, the EU population reached 448.8 million, with 21.3% of the population aged 65 or older.

Germany orthopedic implants market is anticipated to register a considerable growth rate during the forecast period. The high surgical volume reflects strong demand for orthopedic implants used in hip and knee replacements. According to the Organization for Economic Co-operation and Development (OECD) in April 2024, Germany has one of the highest rates of hip arthroplasty among member countries, with approximately 314.9 hip replacement procedures per 100,000 population in recent years, well above the OECD average.

Asia Pacific Orthopedic Implants Market Trends

Asia Pacific is anticipated to be the fastest-growing region in the global orthopedic implants market. The rapidly developing healthcare infrastructure in major countries, such as India, China, & Japan, and the booming medical tourism industry are propelling demand for orthopedic implants in the region. The number of orthopedic implantations performed in the region is growing due to the rising incidence of chronic orthopedic ailments and improved diagnostic tools.

The orthopedic implants market in Japan is expected to grow over the forecast period. Japan has a highly developed medical device industry with advanced manufacturing facilities and technologies. Major locally present companies are adopting strategies such as mergers, collaborations, and product launches to maintain a competitive edge. For instance, in September 2022, Smith+Nephew announced the introduction of its OR3O Dual Mobility System in Japan; the system are used in both revision and primary hip arthroplasty procedures.

Latin America Orthopedic Implants Market Trends

Latin America orthopedic implants market is anticipated to register a considerable growth rate during the forecast period. Moreover, technological advancements in implant materials and surgical techniques are crucial in driving the adoption of orthopedic implants in this region. The growing number of sports-related injuries and road accidents that require orthopedic interventions further impels market growth. In addition, the availability of favorable reimbursement policies and government initiatives aimed at improving healthcare infrastructure & accessibility are essential drivers for the orthopedic implants market in Latin America.

The orthopedic implants market in Brazil is expected to grow over the forecast period. Medical tourism is growing in the country, the healthcare infrastructure is constantly improving, and patients are becoming more aware of the commercial availability of orthopedic implants. All these factors are contributing to market growth in the country. The rising geriatric population, with a higher susceptibility to musculoskeletal disorders, also contributes to market growth

Middle East & Africa Orthopedic Implants Market Trends

Middle East and Africa orthopedic implants market is anticipated to register a considerable growth rate during the forecast period. Technological advancements, government initiatives, and increase in awareness about bone-related treatments drive the market. In addition, the growing investment in R&D activities and the rising availability of smart orthopedic implants are expected to fuel the market growth further.

UAE orthopedic implants market is anticipated to register a considerable growth rate during the forecast period. The UAE orthopedic implants market is likely to be driven by the growing prevalence of osteoporosis & osteoarthritis and the rise in sports & road injuries. Furthermore, the market witnesses’ new growth prospects over the forecast period owing to an increase in the reconfiguration of supply chain models by medical device manufacturers and an increase in the demand for orthopedic implants.

Key Orthopedic Implants Company Insights

Key participants in the orthopedic implants market are focusing on devising innovative business growth strategies in the form of product portfolio expansions, partnerships & collaborations, mergers & acquisitions, and business footprint expansions.

Key Orthopedic Implants Companies:

The following key companies have been profiled for this study on the orthopedic implants market.

- DePuy Synthes

- Zimmer Biomet

- Stryker Corporation

- Smith+Nephew

- Medtronic

- NuVasive, Inc. (mergerd with Globus Medical)

- Arthrex, Inc.

- Acumed LLC

- Paragon Medical (AMETEK)

- Globus Medical

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (DePuy Synthes, Zimmer Biomet, Stryker Corporation, Smith+Nephew, Medtronic, Globus Medical (including NuVasive))

- Expand orthopedic implant portfolios through continuous product innovation, strategic acquisitions, surgeon education programs, and global distribution network expansion. Invest in advanced joint reconstruction systems, spinal implants, robotic-assisted surgery platforms, navigation technologies, biologics, and patient-specific implant solutions to strengthen market leadership. Focus on integrating digital surgery technologies, AI-enabled surgical planning, and value-based care solutions to improve clinical outcomes and procedural efficiency.

- Strong global brand recognition, extensive clinical evidence, broad orthopedic product portfolios, and well-established relationships with hospitals, ambulatory surgery centers, and orthopedic surgeons. Significant R&D capabilities, regulatory expertise, manufacturing scale, and comprehensive sales networks support widespread adoption across joint reconstruction, trauma, spine, and sports medicine applications.

- High product development, regulatory compliance, and commercialization costs can impact profitability. Premium pricing of advanced implant systems and robotic-assisted surgical platforms may limit adoption in cost-sensitive healthcare markets. Product recalls, reimbursement pressures, and procurement-driven pricing competition may also affect market performance.

Emerging & Specialized Players (Arthrex, Inc., Acumed LLC, Paragon Medical (AMETEK))

- Focus on specialized orthopedic segments such as sports medicine, extremity reconstruction, trauma fixation, biologics, and customized implant solutions. Leverage niche expertise, surgeon-focused innovation, targeted product development, and specialized distribution strategies to address specific clinical needs and strengthen competitive positioning.

- Greater agility in responding to evolving surgical techniques and emerging orthopedic treatment trends. Ability to introduce specialized products rapidly, provide focused surgeon training, and deliver innovative solutions for niche orthopedic procedures, particularly in trauma, extremities, and sports medicine.

- Limited product breadth and lower global scale compared to multinational orthopedic leaders. Smaller distribution networks, lower financial resources, and reduced bargaining power may restrict penetration into large healthcare systems and global procurement contracts.

Recent Developments

-

In April 2025, MicroPort Orthopedics, announced the introduction of its flagship second-generation solution, the Evolution Medial-Pivot Knee, in India. The solution is designed to deliver superior flexion stability, anatomic motion, and a wear-limiting design, aiming to replicate the natural stability and motion of the knee to allow superior patient outcomes after total knee replacement surgery.

-

In March 2025, Johnson & Johnson MedTech showcased its latest digital orthopaedics advancements at the AAOS 2025 Annual Meeting in San Diego from March 10-14. Building on last year’s innovations, the company is introducing advanced implants, techniques, and data-driven technologies across various orthopaedic specialties, including joint reconstruction, trauma, extremities, and spine, all aimed at meeting the needs of surgeons and patients.

-

In February 2024, Zeda, Inc. acquired the Orthopaedic Implant Company (OIC), based in Nevada. The acquisition allows Zeda to produce OIC implants for its customers and strengthen its position in the orthopedic industry.

-

In January 2024, Pacific Research Laboratories, Inc. launched a web application, ENDPOINT, which allows orthopedic implant manufacturers to test devices using automated simulation applications.

-

In January 2024, Accelus launched Linesider, a spinal implant system with a modular-cortical design. The technology enables surgeons to insert screw shanks at the beginning of the procedure and customize the construct using modular rods & tulips.

-

In May 2023, Henry Schein signed an agreement to acquire S.I.N. Implant System, a Brazil-based manufacturer of dental implants. This strategy helped the company expand its dental specialty businesses.

-

In February 2023, Invibio opened a new orthopedic medical device product development and manufacturing center in Leeds, UK.

Orthopedic Implants Market Report Scope

Report Attribute

Details

Market size in 2025

USD 27.0 billion

Estimated Market size in 2026

USD 27.9 billion

Projected Market size by 2033

USD 36.6 billion

Growth rate

CAGR of 3.9% from 2026 to 2033

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product, Material, Distribution Channel, End Use, Region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; Norway; Denmark; Sweden; China; Japan; India; South Korea; Australia; Thailand; Brazil; Argentina; Saudi Arabia; South Africa; UAE; Kuwait

Key companies profiled

DePuy Synthes; Zimmer Biomet; Stryker Corporation; Smith+Nephew; Medtronic; NuVasive, Inc. (mergerd with Globus Medical); MArthrex, Inc.; Acumed LLC; Paragon Medical (AMETEK); Globus Medical

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Orthopedic Implants Market Report Segmentation

This report forecasts revenue and volume growth at global, regional, and country level and provides an analysis on industry trends in each of the sub segments from 2021 to 2033. For the purpose of this study, Grand View Research, Inc. has segmented the orthopedic implants market report on the basis of product, material, distribution channel, end use, and region.

-

Product Outlook (Revenue, USD Million; Unit Volume in ‘000 Units; 2021 - 2033)

-

Lower Extremity Implants

-

Knee Implants

-

Hip Implants

-

Foot & Ankle Implants

-

-

Spinal Implants

-

Dental

-

Dental Implants

-

Craniomaxillofacial Implants

-

-

Upper Extremity Implants

-

Elbow Implants

-

Hand & Wrist Implants

-

Shoulder Implants

-

-

-

Materials Outlook (Revenue, USD Million, 2021 - 2033)

-

Metallic Material

-

Stainless steel

-

Titanium

-

Titanium Alloy

-

Cobalt Alloy

-

Others

-

-

Ceramic Biomaterials

-

Polymeric Biomaterials

-

Others

-

-

Distribution Channel Outlook (Revenue, USD Million, 2021 - 2033)

-

Offline

-

Online

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Hospitals

-

Outpatient Facilities

-

-

Regional Outlook (Revenue, USD Million; Unit Volume in ‘000 Units; 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

U.K.

-

Spain

-

Italy

-

France

-

Denmark

-

Norway

-

Sweden

-

Rest of Europe

-

-

Asia Pacific

-

Japan

-

China

-

India

-

Australia

-

Thailand

-

South Korea

-

Rest of Asia Pacific

-

-

Latin America

-

Brazil

-

Argentina

-

-

Rest of Latin America

-

MEA

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

Rest of MEA

-

-

Research Methodology

The orthopedic implants market figures in this report are based on a proven research process that combines executive interviews with secondary research from proprietary databases, company filings, and recognized regulatory and institutional sources. Market size is built through value-chain sizing - reconciling supply-side and demand-side estimates - and triangulated with bottom-up and top-down approaches. Every estimate passes multiple levels of expert validation before publication, with each orthopedic implants segment quantified using the revenue-capture definitions in the table below.

Segment Definition

Segment - Product

Revenue capture definition

Lower Extremity Implants

Orthopedic implants designed to restore, stabilize, or replace damaged joints and bones in the lower limbs, including the hips, knees, feet, and ankles. These implants are commonly used to treat trauma, degenerative diseases, deformities, and sports injuries.

Knee Implants

Prosthetic devices used in partial or total knee replacement procedures to replace damaged knee joint surfaces caused by osteoarthritis, rheumatoid arthritis, trauma, or other degenerative conditions.

Hip Implants

Artificial components implanted during hip replacement surgeries to replace damaged hip joints and restore mobility, reduce pain, and improve joint function in patients with arthritis, fractures, or other hip disorders.

Foot & Ankle Implants

Implants used for reconstruction, fixation, fusion, and replacement procedures involving the foot and ankle. These devices help treat fractures, deformities, arthritis, and sports-related injuries.

Spinal Implants

Medical devices used to stabilize, align, and support the spinal column during procedures such as spinal fusion, deformity correction, trauma repair, and treatment of degenerative disc diseases. Examples include rods, screws, cages, plates, and artificial discs.

Dental

Orthopedic-related dental restoration devices used to replace missing teeth and support oral rehabilitation procedures. This category primarily includes dental implants and associated components.

Dental Implants

Biocompatible implant fixtures surgically inserted into the jawbone to replace missing tooth roots and provide a stable foundation for crowns, bridges, dentures, and other dental prostheses.

Craniomaxillofacial Implants

Specialized implants used in the reconstruction and fixation of cranial, facial, and jaw bones following trauma, congenital deformities, tumor resections, or reconstructive surgeries. These include plates, screws, meshes, and patient-specific implants.

Upper Extremity Implants

Orthopedic implants designed for the treatment and reconstruction of joints and bones in the upper limbs, including the shoulder, elbow, hand, and wrist.

Elbow Implants

Prosthetic devices used in total or partial elbow replacement procedures to restore joint function and reduce pain resulting from arthritis, fractures, or severe joint damage.

Hand & Wrist Implants

Implants used to repair, reconstruct, or replace damaged bones and joints in the hand and wrist. These devices are commonly utilized in trauma, arthritis, deformity correction, and reconstructive surgeries.

Shoulder Implants

Prosthetic components used in shoulder arthroplasty procedures to replace damaged shoulder joints and restore mobility in patients suffering from arthritis, rotator cuff arthropathy, fractures, or degenerative conditions.

Segment - Material

Revenue capture definition

Metallic Material

Metallic biomaterials widely used in orthopedic implants due to their high strength, durability, corrosion resistance, and biocompatibility. These materials are commonly employed in load-bearing orthopedic applications.

Stainless Steel

A cost-effective metallic biomaterial used in orthopedic fixation devices such as plates, screws, wires, and pins. It offers good mechanical strength and corrosion resistance but is generally used less frequently in long-term implants than titanium-based materials.

Titanium

A highly biocompatible metal extensively used in orthopedic and dental implants due to its excellent corrosion resistance, low density, high strength-to-weight ratio, and ability to promote osseointegration with bone tissue.

Titanium Alloy

Advanced titanium-based alloys, such as Ti-6Al-4V, that provide enhanced mechanical strength, fatigue resistance, and biocompatibility for demanding orthopedic applications, including joint replacements and spinal implants.

Cobalt Alloy

High-strength metallic alloys, typically cobalt-chromium-based, used in orthopedic implants requiring exceptional wear resistance and durability, particularly in joint replacement procedures.

Others (Metallic Materials)

Includes additional metallic biomaterials such as tantalum, nitinol, magnesium alloys, and other specialized metals used in selected orthopedic and reconstructive applications.

Ceramic Biomaterials

Biocompatible ceramic materials used in orthopedic implants due to their excellent wear resistance, hardness, and biological compatibility. Common examples include alumina and zirconia used in joint replacement components.

Polymeric Biomaterials

Synthetic polymer materials utilized in orthopedic implants and implant components. Examples include ultra-high-molecular-weight polyethylene (UHMWPE), polyether ether ketone (PEEK), and biodegradable polymers used for cushioning, fixation, and spinal applications.

Others

Includes composite biomaterials, bioresorbable materials, carbon-fiber-reinforced materials, and emerging biomaterials developed to improve implant performance, longevity, and biological integration.

Segment - Distribution Channel

Revenue capture definition

Offline

Traditional sales channels involving direct procurement and distribution of orthopedic implants through hospitals, clinics, distributors, medical device representatives, and specialty healthcare facilities.

Online

Digital procurement channels that facilitate ordering, inventory management, and purchasing of orthopedic implants and related products through online platforms, manufacturer portals, and e-commerce systems used by healthcare providers.

Segment - End Use

Revenue capture definition

Hospitals

Healthcare institutions that perform orthopedic procedures such as joint replacements, trauma surgeries, spinal surgeries, dental implant procedures, and reconstructive surgeries. Hospitals represent the primary end users of orthopedic implants due to high surgical volumes and comprehensive care capabilities.

Outpatient Facilities

Ambulatory surgery centers (ASCs), specialty orthopedic clinics, dental surgery centers, and other outpatient healthcare facilities that perform orthopedic and implant-related procedures without requiring extended inpatient hospitalization.

Estimation Model

Market-specific Research Models

Consensus-Based Estimates & Forecasting

The orthopedic implants market presents emerging to dominant opportunities, featuring global key players such as DePuy Synthes; Zimmer Biomet; Stryker Corporation; Smith+Nephew; Medtronic; NuVasive, Inc. (mergerd with Globus Medical); MArthrex, Inc.; Acumed LLC; Paragon Medical (AMETEK); Globus Medical. To ensure a holistic approach, the GVR research team adopted a comprehensive methodology, considering multiple companies worldwide and utilizing various variables for data accuracy.

Our methodology included:

Model 1: Commodity Flow Analysis - For public players, annual reports were referenced. For private players, premium paid data sources such as S&P Global, Crunchbase, ZoomInfo, RocketReach, etc., were used for the latest revenue insights.

Model 2: Parent Market Analysis

Model 3: Country-level Multivariate Analysis Assumptions

Model 4: Segment-level Multivariate Analysis Assumptions

Model 5: Orthopedic Implants Market CAGR Calculations

Commodity flow analysis was employed to track the movement of orthopedic implants through the value chain, from technology providers to end users. This analysis provided insights into demand generation points, intermediary roles, and ultimate consumption patterns.

Delivered Customizations

This report has been delivered with the following In-depth customizations

CLIENT REQUEST

CUSTOMIZATION DELIVERED

VALUE ADDS

Orthopedic Implant Adoption & Procedure Volume Analysis

Developed a tailored analysis of the global orthopedic implants market focused on joint reconstruction implants, spinal implants, trauma fixation devices, dental implants, sports medicine implants, and extremity implants. The study assessed adoption trends across hospitals, orthopedic specialty centers, ambulatory surgical centers (ASCs), and rehabilitation facilities while evaluating the impact of aging populations, musculoskeletal disorders, sports injuries, and increasing orthopedic surgical procedures on market growth.

Enables stakeholders to understand evolving orthopedic treatment trends, identify high-growth implant categories, assess procedure volume opportunities, and evaluate the impact of technological advancements and demographic shifts on long-term market expansion.

Implant Technologies, Clinical Outcomes & Surgical Innovation Assessment

Delivered a customized evaluation of orthopedic implant utilization across hip replacement, knee replacement, shoulder replacement, spinal fusion, fracture fixation, and sports injury repair procedures. The analysis assessed advancements in biomaterials, 3D-printed implants, robotic-assisted orthopedic surgery, patient-specific implants, minimally invasive surgical techniques, implant longevity, revision surgery trends, and demand for technologically advanced orthopedic solutions.

Provides actionable insights into commercially attractive implant segments, emerging surgical technologies, changing clinical requirements, and growth opportunities associated with personalized implants, improved patient outcomes, faster recovery times, and enhanced procedural efficiency.

Healthcare Infrastructure, Regulatory Environment & Competitive Landscape Assessment

Conducted a focused assessment of the orthopedic implants ecosystem, including implant manufacturing, supply chain dynamics, reimbursement frameworks, regulatory compliance requirements, hospital procurement practices, surgeon preferences, and competitive positioning. The analysis evaluated market access barriers, product approval pathways, pricing pressures, innovation strategies, technology adoption trends, and competitive differentiation initiatives among leading orthopedic implant manufacturers.

Supports strategic planning for product development, manufacturing investments, hospital partnerships, geographic expansion, regulatory compliance, and market entry initiatives by identifying demand drivers, operational challenges, revenue opportunities, reimbursement dynamics, and competitive advantages across the global orthopedic implants value chain.

Frequently Asked Questions About This Report

The global orthopedic implants market is expected to grow at a compound annual growth rate of 3.9% from 2026 to 2033 to reach USD 36.6 billion by 2033.

The market is driven by the growing prevalence of reduced bone density, weakened bones, and musculoskeletal disorders. The surging risk of degenerative bone disorders is another factor driving market growth over the forecast period. In addition, the availability of advanced orthopedic implants and rapid development in healthcare infrastructure globally are expected to impact market growth positively.

North America dominated with a 45.1% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

The metallic material segment led with a 46.4% revenue share in 2025, while polymeric biomaterials is the fastest-growing segment.

The hospitals segment led with a 63.7% revenue share in 2025 and is expected to grow at the fastest CAGR during the forecast period.

Some key players operating in the orthopedic implants market include DePuy Synthes, Zimmer Biomet, Stryker Corporation, Smith+Nephew, Medtronic, NuVasive, Inc. (mergerd with Globus Medical), Arthrex, Inc., Acumed LLC, Paragon Medical (AMETEK), Globus Medical.

The global orthopedic implants market size was estimated at USD 27.0 billion in 2025 and is expected to reach USD 28.0 billion in 2026.

By product, the lower extremity implants segment dominated the orthopedic implants market in 2025 and accounted for the largest revenue share of 52.09%. The growth is attributed to the aging population, increasing prevalence of orthopedic conditions, advancements in implant materials & designs, and the growing demand for improved quality of life through surgical interventions.

About the Author(s)

Medical Devices Research Team

Healthcare · Medical DevicesThis report was authored by the medical devices research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the medical devices segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.