- Home

- »

- Medical Devices

- »

-

Peripheral Vascular Devices Market, Industry Report, 2033GVR Report cover

![Peripheral Vascular Devices Market Size, Share & Trends Report]()

Peripheral Vascular Devices Market (2026 - 2033) Size, Share & Trends Analysis Report By Type, By Application (Peripheral Arterial Disease (PAD), Aneurysms, Venous Diseases), By End Use (Hospitals, Ambulatory Surgical Centers), By Region, And Segment Forecasts

Market Size, 2025

$9.5BMarket Estimate, 2026

$10.2BMarket Forecast, 2033

$16.1BCAGR, 2026–2033

6.6%Peripheral Vascular Devices Market Summary

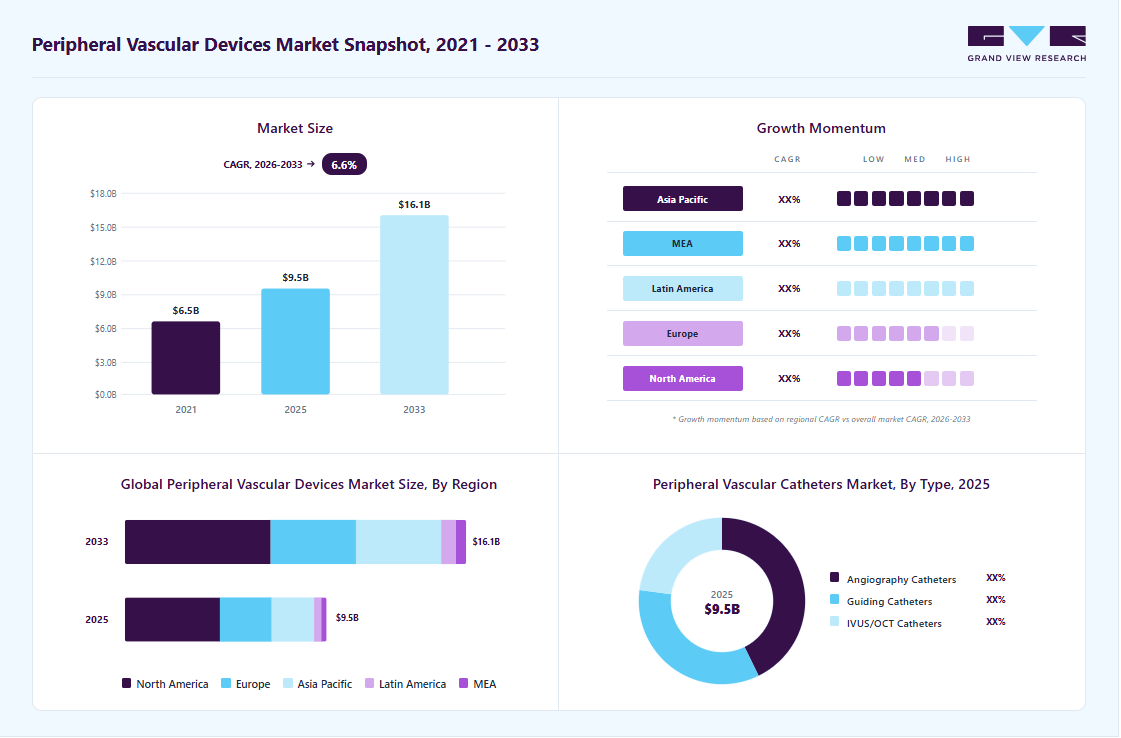

The global peripheral vascular devices market size was valued at USD 9.5 billion in 2025 and is projected to grow from USD 10.2 billion in 2026 to USD 16.1 billion by 2033, at a CAGR of 6.6% from 2026 to 2033. North America dominated the global peripheral vascular devices market with the largest revenue share of 47.1% in 2025. Growth in the market can be attributed to the increasing prevalence of peripheral vascular diseases, the rising geriatric population, and novel product launches.

Key Market Trends & Insights

- By type: the peripheral stents segment accounted for a significant share of 22.2% in 2025.

- By application: the peripheral arterial disease (PAD) segment held the largest share of 46.6% in 2025.

- By end use: the hospitals segment held the largest share of 40.5% in 2025.

Regional Highlights

- Largest regional market: North America (47.1% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 9.5 Billion

- Estimated market size in 2026: USD 10.2 Billion

- Projected market size by 2033: USD 16.1 Billion

- CAGR (2026-2033): 6.6%

The section below outlines key market drivers, including technological innovations and emerging trends shaping the market. It highlights advancements in technology, a shift toward minimally invasive catheter-based revascularization procedures, and the increasing prevalence of venous diseases and peripheral arterial diseases.

")

Market Drivers

Rapid Rise in Peripheral Arterial Disease (PAD) & Venous Disease

The rising prevalence of Peripheral Arterial Disease (PAD) is significantly driving the growth of the market. PAD has a significantly high prevalence in both developed and emerging economies globally. For instance, according to a study published in the National Library of Medicine in July 2025, compared with findings from the Global Burden of Disease Study 2021, the global prevalence of peripheral arterial disease (PAD) is projected to rise by approximately 220% by 2050, reaching around 360 million cases. More than half of these cases are expected to occur in low- and middle-income countries (LMICs). This surge is largely attributed to the increasing burden of metabolic disorders, particularly diabetes, which significantly contributes to both the prevalence and progression of PAD.

Shift Toward Minimally Invasive Catheter-Based Revascularization

The transition from open vascular surgery to minimally invasive endovascular procedures represents one of the most transformative shifts in this market. Clinicians increasingly prefer catheter-based interventions such as angioplasty, stenting, and atherectomy due to their lower procedural risk, reduced hospital stay, and faster patient recovery. For instance, according to data published by Yale Medicine in April 2025, approximately 900,000 percutaneous coronary intervention (PCI) procedures, including angioplasty and stenting, are performed annually in the U.S. These catheter-based interventions are widely used due to their minimally invasive nature, lower complication rates, and faster recovery compared to open surgical alternatives.

Increasing Clinical Trials & Studies

The growth of the market is significantly influenced by the increasing number of clinical trials and studies focusing on vascular health. Clinical trials allow researchers to evaluate the safety and efficacy of new devices and techniques in treating peripheral vascular diseases (PVD). For instance, in March 2024, BD initiated the AGILITY study, enrolling its first patient to evaluate the safety and effectiveness of the BD Vascular Covered Stent for the treatment of Peripheral Arterial Disease (PAD). This global, multi-center clinical trial will involve 315 patients across 40 U.S., European, Australian, and New Zealand sites. The study aims to address significant unmet needs in PAD treatment. It could provide interventionalists with a new solution to improve patient outcomes over the next three years of follow-up. While these trials expand, they validate existing technologies and pave the way for novel interventions that address unmet medical needs.

Technological Innovation

The introduction of novel products that address the evolving needs of patients and healthcare providers is significantly contributing to the market growth. These innovative devices include advanced stents, balloons, and grafts designed for treating peripheral artery disease (PAD) and other vascular conditions. These advancements include cutting-edge technologies such as drug-eluting capabilities, bioresorbable materials, and others. For instance, in September 2025, Johnson & Johnson launched the European Shockwave Javelin Peripheral IVL Catheter, an advanced intravascular lithotripsy (IVL) system designed to address calcification in severely narrowed vessels and expand treatment options for patients with Peripheral Artery Disease.

Funding and Strategic Investments in the Peripheral Vascular Devices Market

Date

Company

Description

In April 2025

Accor

Boston Scientific announced the U.S. launch of the Sterling SL balloon catheter, a low-profile peripheral PTA balloon designed to improve deliverability and dilatation outcomes in peripheral artery disease interventions.

In August 2025

Abbott

Abbott announced it has received CE Mark approval in Europe for the Esprit BTK Everolimus Eluting Resorbable Scaffold System, a first‑of‑its‑kind dissolvable stent for below‑the‑knee peripheral artery disease that supports vessel healing with drug delivery before gradually resorbing.

Market Concentration & Characteristics

The chart below illustrates the relationships among industry concentration, industry characteristics, and industry participants. There is a medium degree of innovation, a moderate level of merger & acquisition activities, a moderate impact of regulations, a low product substitute, and moderate expansion of the industry.

Market Dynamics

The market exhibits a medium degree of technological innovation, driven by continuous advancements and development in minimally invasive endovascular therapies and device engineering. Manufacturers are increasingly introducing next-generation solutions such as drug-coated balloons, drug-eluting stents, bioresorbable scaffolds, and intravascular lithotripsy systems to improve clinical outcomes and reduce restenosis rates. For instance, in May 2025, Medtronic received expanded CE Mark indications for the Prevail paclitaxel-coated PTCA balloon catheter, including complex bifurcation lesions. This highlights advancements in drug-coated balloon technology, aimed at improving deliverability and long-term clinical outcomes

Mergers and acquisitions activity is moderate, driven by leading medical device companies acquiring innovative firms to expand their endovascular portfolios and strengthen technological capabilities. In January 2026, Boston Scientific announced an agreement to acquire Penumbra, Inc., expanding its peripheral vascular and neurovascular portfolios, particularly in thrombectomy and clot-removal technologies relevant to acute and chronic peripheral occlusions.

The regulatory impact is medium. The peripheral vascular device market operates within an increasingly stringent and complex regulatory landscape across major markets such as the U.S., Europe, and emerging economies. Regulatory authorities such as the U.S. Food and Drug Administration and the European Medicines Agency have significantly tightened approval requirements, especially for high-risk devices such as drug-eluting stents. For instance, in May 2025, Cook Medical received U.S. FDA approval for an updated Zenith Iliac Branch device, supporting endovascular treatment of aortoiliac aneurysms while preserving internal iliac artery blood flow.

There are no direct substitutes for the product; the alternative treatment options, such as pharmacological therapy, lifestyle modification, and open surgical procedures (e.g., bypass surgery), are present along with minimally invasive endovascular interventions. According to the study by the American College of Cardiology in April 2025, exercise therapy is recommended as a first-line treatment for patients with peripheral artery disease, as it significantly improves walking performance and quality of life.

Regional expansion is significant, with companies actively targeting underserved markets across the Asia Pacific, the Middle East, and Latin America. In March 2026, Abbott introduced its most advanced drug-eluting stent, XIENCE Skypoint, in India.The stent is designed to be more flexible, easier to guide through the heart’s arteries, including large vessels, and better suited for treating complex heart blockages.

Type Insights

By type, the peripheral stents segment held the most significant share in 2025. The growth is driven by increasing demand for advanced treatment solutions for peripheral artery disease. Peripheral stents, which are small wire-mesh tubes used to reopen arteries narrowed or blocked by plaque, are witnessing continuous innovation supported by favorable regulatory approvals and funding initiatives. For instance, in August 2025, Abbott Laboratories announced it received CE Mark approval in Europe for its Esprit BTK resorbable scaffold system, designed to treat below-the-knee peripheral artery disease by keeping arteries open, delivering everolimus, and then dissolving over time.

The peripheral accessories segment is expected to grow at the fastest CAGR during the forecast period. The growing prevalence of peripheral artery disease (PAD), coupled with increasing adoption of minimally invasive procedures, is driving demand for these supportive devices. In addition, continuous regulatory approvals are accelerating innovation and adoption in this segment. For instance, in July 2024, the U.S. FDA approved the MYNX Control Venous Vascular Closure Device, demonstrating high procedural success, reduced time to hemostasis, and faster patient ambulation, highlighting the clinical benefits of advanced closure accessories in peripheral interventions.

Application Insights

On the basis of application, the peripheral arterial disease (PAD) segment held the largest share of 46.6% in 2025. The rising prevalence of peripheral artery disease and government initiatives drive segment growth. In recent years, research on peripheral arterial disease (PAD) has increased significantly, driven by the growing prevalence of cardiovascular disease and advancements in diagnostic technologies. For instance, in March 2024, BD, a medical technology firm, initiated the "AGILITY" study by enrolling its first participant. This study is part of an investigational device exemption (IDE) trial designed to evaluate the BD Vascular Covered Stent's safety and efficacy in treating PAD.

The aneurysms segment is expected to grow at the fastest CAGR during the forecast period. The increasing prevalence of aneurysms across high-risk demographic groups is influenced by the incidence rising with age and lifestyle factors such as smoking, expanding the at-risk patient population and demand for screening and intervention. Unruptured brain aneurysms affect 2-5% of the population, with nearly 25% of patients having multiple aneurysms, while abdominal aortic aneurysms increase with age and are 4-6 times more common in males, particularly those over 60 and smokers, highlighting a large and growing high-risk population.

End Use Insights

The hospitals segment held the largest share in 2025. Hospitals are crucial in administering advanced medical procedures, including percutaneous transmural arterial bypass (PTAB). These facilities have specialized surgical units, advanced imaging technologies, and highly trained medical personnel for minimally invasive surgeries. Such factors contribute to the large share of the segment.In February 2025, the University Hospitals Harrington Heart & Vascular Institute announced the establishment of a dedicated Limb Preservation Center to advance multidisciplinary care for patients with peripheral artery disease and prevent amputations through advanced interventional procedures.

The ambulatory surgical centers segment is expected to grow at the fastest CAGR during the forecast period. The growth of ambulatory surgery centers (ASCs) is driven by the shift toward minimally invasive therapies, cost containment, and patient preference for shorter hospital stays. ASCs facilitate efficient patient flow while maintaining high standards of procedural safety and recovery. In February 2026, an article published in Ambulatory Surgery Center News highlighted that select ambulatory surgery centers (ASCs) performing percutaneous coronary interventions reported complication rates comparable to hospitals at about 1%, while achieving cost savings of roughly USD 4,000 per procedure, emphasizing the potential for safe and more efficient cardiac care in the ASC setting.

Regional Insights

The peripheral vascular devices industry in North America dominated the global market in 2025 with a share of 47.1%. The market is experiencing consistent growth driven by factors such as the growing incidence of PAD, the aging population, and rapid advances in medical technology. According to a CDC article published in May 2024, in the U.S., around 6.5 million individuals aged 40 and older are affected by peripheral artery disease (PAD). The substantial number of PAD cases highlights the increasing demand for advanced stenting solutions to address the challenges associated with this condition, driving growth.

U.S. Peripheral Vascular Devices Market Trends

The U.S. peripheral vascular devices industry is expected to grow significantly as the market is characterized by a dynamic regional landscape featuring substantial growth and notable technological progress. The demand for peripheral vascular devices is growing due to several factors, such as the rising incidence of cardiovascular diseases and an increasing number of clinical trials exploring stent applications in PAD. Moreover, advanced healthcare facilities, rising healthcare expenditures, and product launches boost market growth. For instance, in June 2024, MicroVention, a division of Terumo, officially launched its LVIS EVO intraluminal support device in the U.S. This new stent is designed to provide advanced intraluminal support, marking a significant addition to the company’s product lineup.

Europe Peripheral Vascular Devices Market Trends

The peripheral vascular devices industry in Europeis expected to grow significantly during the forecast period, driven by an increasing prevalence of vascular diseases. This rise in vascular conditions is primarily linked to demographic changes and lifestyle factors, particularly among the aging population. As the geriatric demographic expands, so does the demand for peripheral vascular devices used in diagnosis and treatment. In addition, ongoing advancements in medical technology are leading to the development of innovative, minimally invasive devices for vascular interventions, which often contribute to better patient outcomes and reduced recovery times.

The UK peripheral vascular devices industry is expected to grow significantly due to the increasing cases of PAD in this region. According to the British Heart Foundation article published in August 2024, about one in five individuals over the age of 60 in the UK experience some form of peripheral artery disease (PAD). The key risk factors contributing to PAD, such as smoking, diabetes, obesity, and high blood pressure, mirror those associated with heart disease and stroke. The rising prevalence of diabetes is driving an increase in PAD cases.

The peripheral vascular devices industry in Germany is expected to grow over the forecast period. Germany’s advanced healthcare infrastructure and well-established hospital networks are fueling the adoption of minimally invasive vascular procedures. Moreover, increasing awareness among patients and clinicians about early diagnosis and effective treatment of vascular disorders is fueling the demand for innovative peripheral vascular devices. The German market is highly competitive, with major global players and local companies vying for market share. Leading companies focus on expanding product portfolios, enhancing distribution networks, and launching technologically advanced devices tailored to complex vascular anatomies. For instance, in January 2026, in Germany, Zylox-Tonbridge agreed to acquire Optimed, strengthening its presence in the industry by expanding product portfolios, manufacturing capabilities, and global commercialization and distribution networks.

Asia Pacific Peripheral Vascular Devices Market Trends

The peripheral vascular devices industryin the Asia Pacificis expected to witness the fastest growth over the forecast period, driven by the rising burden of vascular diseases, expanding healthcare infrastructure, and increasing focus on advanced treatment solutions. The companies in this region are focusing on product innovation and strengthening their manufacturing and research capabilities to support long-term growth and regional expansion.

The China peripheral vascular devices industry isexpected to grow over the forecast period. The growing prevalence of peripheral artery disease in China fuels the demand for covered stent solutions. According to the NCBI article published in August 2023, over the past three decades, China has made significant strides in improving the accessibility and quality of medical care, now leading among middle-income countries. The nation's cardiovascular technologies are among the most advanced globally, and substantial progress has been made in addressing the "treatment difficulty" associated with cardiovascular diseases (CVD.

The peripheral vascular devices industry in Japan is expected to witness growth during the forecast period. Due to the rising disease burden, strategic initiatives by domestic players are playing a crucial role in shaping the Japan’s market. Companies are increasingly focusing on strengthening their technological capabilities and expanding their presence in high-growth segments such as endovascular therapies. For instance, on November 30, 2023, Kaneka Corporation acquired Japan Medical Device Technology Co., Ltd., making it a wholly owned subsidiary to enhance its expertise in vascular intervention and stent technologies. This development reflects a growing emphasis on innovation in bioresorbable and advanced stent platforms, which is expected to support long-term market expansion in Japan.

Latin American Peripheral Vascular Devices Market Trends

The peripheral vascular devices industry in Latin Americais expected to undergo substantial expansion during the forecast period. PAD emerges as a prominent healthcare challenge within the region, owing to the growing geriatric population and rising risk factors such as diabetes and obesity. The growing prevalence of PAD is boosting the demand for minimally invasive interventions that involve the use of advanced peripheral vascular devices.

The Brazil peripheral vascular devices industry is expected to grow during the forecast period due to growing awareness about peripheral vascular diseases and advanced treatment options among both healthcare professionals and the public, which is expected to fuel market expansion. Moreover, government efforts and policies to enhance healthcare infrastructure and facilitate access to medical devices may boost the market.The increasing volume of vascular interventions in Brazil highlights the growing reliance on both surgical and minimally invasive treatment approaches.

Middle East and Africa Peripheral Vascular Devices Market Trends

The peripheral vascular devices industry in the Middle East and Africais witnessing steady growth, driven by the rising prevalence of cardiovascular and peripheral artery diseases, increasing diabetes rates, and expanding healthcare infrastructure. As per the data published by the World Heart Federation 2026, Cardiovascular disease is the number one cause of death in the Middle East and North Africa region, responsible for more than one-third of all deaths, or 1.4 million people every year. In addition to growing investments in healthcare infrastructure, marked by the establishment of new hospitals and clinics, are anticipated to fuel the demand for peripheral vascular devices. As more patients seek treatment for cardiovascular diseases, the market is expected to grow.

The Saudi Arabia peripheral vascular devices industry is expanding significantly over the forecast period, supported by increasing investment in modern healthcare infrastructure and rising awareness of cardiovascular diseases. The prevalence of peripheral artery disease (PAD), diabetes, and hypertension has created a growing demand for minimally invasive vascular interventions. According to a BioMed Central Ltd article published in March 2024, a recent study conducted in Saudi Arabia reported a prevalence of peripheral artery disease (PAD) at 11.7% among a cohort of 471 patients aged 45 years and older.

The peripheral vascular devices industry in Kuwait isgrowing due to the increase in the use of peripheral vascular devices in Kuwait, which is due to the high rate of cardiovascular disease mortality. According to an NCBI article published in October 2023, in Kuwait, cardiovascular diseases (CVDs) account for 46% of mortality rates, highlighting a significant public health concern. This high mortality rate highlights the urgent need for effective management and treatment options for CVD, including peripheral artery disease (PAD).

Key Peripheral Vascular Devices Company Insights

Companies are focusing on strategic initiatives, such as introducing novel products through customization according to consumers’ needs, partnerships, collaborations, and mergers & acquisitions, to expand their product portfolio and extend leadership positions in the field of cardiology.

Key Peripheral Vascular Devices Companies:

The following key companies have been profiled for this study on the peripheral vascular devices market.

- Abbott

- Koninklijke Philips N.V.

- Edward Lifesciences Corporation

- Medtronic

- Teleflex Incorporated

- Boston Scientific Corporation

- BD

- Terumo Corporation

- W. L. Gore & Associates, Inc.

- Cordis

- Cook Group

- B. Braun SE

Recent Developments

-

In January 2025, Gore announced that the GORE VIABAHN FORTEGRA Venous Stent, the first stent specifically indicated for treating deep venous disease in the inferior vena cava (IVC) and iliofemoral veins, received FDA approval after clinical data showed strong patency and safety outcomes in complex deep venous obstructions.

-

In November 2025, BD achieved a milestone in the AGILITY study for its Revello vascular-covered stent, designed for PAD treatment in occluded or narrowed peripheral arteries. The study confirmed the stent’s safety, deliverability, and potential to reduce restenosis, providing real-world clinical evidence for broader adoption.

-

In September 2024, Boston Scientific completed the acquisition of Silk Road Medical, Inc., strengthening access to peripheral intervention devices and supporting growth in peripheral angioplasty and embolic protection solutions.

-

In January 2024, W.L. Gore & Associates, Inc. received FDA approval for its own profile GORE VIABAHN VBX Balloon Expandable Endoprosthesis.

Peripheral Vascular Devices Market Report Scope

Report Attribute

Details

Market size in 2025

USD 9.5 billion

Estimated market size in 2026

USD 10.2 billion

Projected market size by 2033

USD 16.1 billion

Growth rate

CAGR of 6.6% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, Unit Volume in Thousand Units, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Type, application, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East and Africa

Country scope

U.S.; Mexico; Canada; U.K.; Germany; France; Italy; Spain; Denmark; Sweden; Norway; Japan; China; India; Australia; Thailand; South Korea; Brazil; Argentina; South Africa; Saudi Arabia; UAE; Kuwait.

Key companies profiled

Abbott; Koninklijke Philips N.V.; Edward Lifesciences Corporation; Medtronic; Teleflex Incorporated; Boston Scientific Corporation; BD; Terumo Corporation; W. L. Gore & Associates, Inc.; Cordis; Cook Group; B. Braun SE

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Peripheral Vascular Devices Market Report Segmentation

This report forecasts global, regional, and country revenue growth. It provides an analysis of the latest industry trends and opportunities in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global peripheral vascular devices market report based on type, application, end use, and region:

-

Type Outlook (Volume, Thousand Units; Revenue, USD Million, 2021 - 2033)

-

Peripheral Stents

-

Iliac Artery Stents

-

Femoral Artery Stents

-

Carotid Artery Stents

-

Renal Artery Stents

-

Other

-

-

PTA Balloons

-

Catheters

-

Angiography Catheters

-

Guiding Catheters

-

IVUS/OCT Catheters

-

-

Endovascular Aneurysm Repair Stent Grafts

-

Thoracic Endovascular Aneurysm Stent Grafts

-

Abdominal Endovascular Aneurysm Stent Grafts

-

-

Plaque Modification Devices

-

Atherectomy Devices

-

Thrombectomy Devices

-

-

Peripheral Accessories

-

Guidewires

-

Workhorse Guidewires

-

Specialty Guidewires

-

Extra Support Guidewires

-

Frontline Finesse Guidewires

-

-

Peripheral Vascular Closure Devices

-

Balloon Inflation Devices

-

Introducer Sheaths

-

-

Inferior Vena Cava Filters

-

Permanent Filters

-

Retrievable Filters

-

-

Hemodynamic Flow Alteration Devices

-

Chronic Total Occlusion Devices

-

Embolic Protection Devices

-

-

-

Application Outlook (Volume, Thousand Units; Revenue, USD Million, 2021 - 2033)

-

Peripheral Arterial Disease (PAD)

-

Aneurysms

-

Venous Diseases

-

Others

-

-

End use Outlook (Volume, Thousand Units; Revenue, USD Million, 2021 - 2033)

-

Hospitals

-

Ambulatory Surgical Centers

-

Others

-

-

Regional Outlook (Volume, Thousand Units; Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

Sweden

-

Norway

-

Denmark

-

-

Asia Pacific

-

Japan

-

China

-

India

-

South Korea

-

Australia

-

Thailand

-

-

Latin America

-

Brazil

-

Argentina

-

-

MEA

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Frequently Asked Questions About This Report

The global peripheral vascular devices market is expected to grow at a compound annual growth rate of 6.6% from 2026 to 2033 to reach USD 16.1 billion by 2033.

Peripheral stents dominated the type segment held the largest share of 22.2% in 2025. This dominance can be attributed to the increasing use of stents owing to the high efficacy, safety, and tolerability associated with it.

Key factors that are driving the market growth include rising prevalence & increasing diagnosis of peripheral artery disease (PAD) ,growing burden of diabetes and diabetes related PAD, increasing adoption of minimally invasive endovascular procedures and technologically advanced product launches in peripheral vascular devices.

North America dominated with a 47.1% revenue share in 2025.

The global peripheral vascular devices market size was estimated at USD 9.5 billion in 2025 and is expected to reach USD 10.2 billion in 2026.

Some key players operating in the peripheral vascular devices market include Abbott, Terumo Corporation, Nipro, Medtronic, Boston Scientific Corporation, Cordis, Koninklijke Philips N.V., AngioDynamics., ASAHI INTECC CO., LTD., BD, Teleflex Incorporated. (Biotronik), Edward Lifesciences Corporation, B. Braun SE, W. L. Gore & Associates, Inc., Merit Medical Systems, Inc., Cook.

The peripheral arterial disease (PAD) segment led with a 46.6% revenue share in 2025, while aneurysms is the fastest-growing segment.

Hospitals held the largest revenue share in 2025, while ambulatory surgical centers is the fastest-growing area.

Asia Pacific is the fastest-growing region over the forecast period.

About the Author(s)

Medical Devices Research Team

Healthcare · Medical DevicesThis report was authored by the medical devices research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the medical devices segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.