- Home

- »

- Plastics, Polymers & Resins

- »

-

Pharmaceutical Packaging Market Size & Share Report, 2033GVR Report cover

![Pharmaceutical Packaging Market (2026 - 2033)Report]()

Pharmaceutical Packaging Market (2026 - 2033)

Size, Share & Trends Analysis Report By Material (Plastics & Polymers, Glass, Aluminum Foil), By Product (Primary, Secondary, Tertiary), By End Use (Pharma Manufacturing, Contract Packaging), By Regions, And Segment Forecasts

Market Size, 2025

$166.4BMarket Estimate, 2026

$182.2BMarket Forecast, 2033

$353.1BCAGR, 2026–2033

9.9%Pharmaceutical Packaging Market Summary

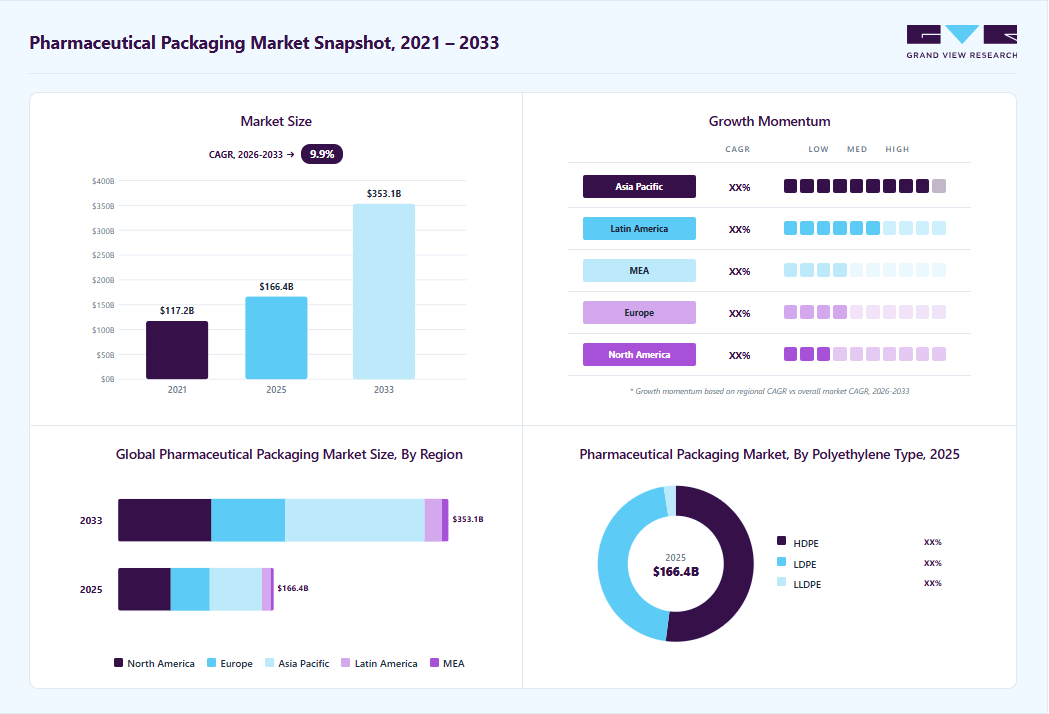

The global pharmaceutical packaging market size was valued at USD 166.4 billion in 2025 and is projected to grow from USD 182.2 billion in 2026 to USD 353.1 billion by 2033, at a CAGR of 9.9% from 2026 to 2033. The North America pharmaceutical packaging market held the largest share of 33.8% of the global market in 2025. The enormous growth of the pharmaceutical sector is one of the primary growth factors for the pharmaceutical packaging sector.

Key Market Trends & Insights

- By product: Primary segment dominated the market, with a revenue share of 76.4% in 2025.

- By material: Plastics & polymers segment held the largest market share of 36.6% in 2025.

- By end use: Pharma manufacturing segment held the largest revenue share of 49.4% in 2025.

Regional Highlights

- Largest regional market: North America (33.8% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 166.4 Billion

- Estimated market size in 2026: USD 182.2 Billion

- Projected market size by 2033: USD 353.1 Billion

- CAGR (2026-2033): 9.9%

The pharmaceutical business has been expanding quickly in recent years due to scientific and technological advancements, and this trend is predicted to continue over the projection period, particularly in developing nations like China, India, Saudi Arabia, and Brazil. Continuous advancements in medical science and bioscience fundamentally drive the pharmaceutical industry. In Europe, the sector represents a critical pillar of the regional economy, ranking among the continent’s top-performing high-technology industries. Over the past few years, the pharmaceutical landscape has undergone a significant transition, marked by a growing emphasis on biopharmaceutical and biotechnology-driven therapies. Many of these advanced drug formulations exhibit limited stability in liquid form and are therefore commercialized as lyophilized or dry-powder dosage forms. Such products require highly specialized packaging solutions to preserve efficacy, sterility, and shelf life, thereby creating substantial growth opportunities for pharmaceutical packaging manufacturers.

")

Pharmaceutical drugs are predominantly marketed in tablet, capsule, liquid, and powder formats, each requiring distinct packaging approaches. Common packaging types include rigid bottles, stand-up pouches, flat pouches, sachets, and blister packs. To meet evolving regulatory standards and patient expectations, packaging companies are increasingly incorporating advanced features such as dispensing mechanisms, administration aids, sustainable materials, tamper-evident designs, and anti-counterfeiting technologies. These functional enhancements not only improve patient safety and convenience but also support brand differentiation in a highly regulated market.

Sustainability has emerged as a key strategic focus within pharmaceutical packaging. Manufacturers are increasingly adopting post-consumer recycled (PCR) materials and developing packaging solutions using compostable and bio-based materials to reduce environmental impact. For instance, Gerresheimer AG, a leading pharmaceutical packaging provider, has been offering glass bottles made from PCR glass for several years and has expanded its portfolio to include bottles manufactured from recycled PET (R-PET) and bio-based PET (BIO-PET) derived from sugarcane. This shift toward sustainable packaging is expected to accelerate significantly in the coming years, driven by regulatory pressure and corporate sustainability commitments.

In addition, the development of intelligent and connected packaging represents a major opportunity for the pharmaceutical industry. Smart packaging solutions integrated with Internet of Things (IoT) technologies enable real-time monitoring of critical parameters such as temperature, humidity, and handling conditions, thereby ensuring product integrity throughout storage and transportation. Furthermore, the rising adoption of personalized medicine and specialty drugs is driving demand for customized packaging solutions tailored to specific dosages and administration requirements. Pharmaceutical packaging companies that successfully align with these technological, regulatory, and sustainability trends are likely to gain a competitive advantage and achieve sustained growth in an increasingly dynamic market.

Industry Characteristics

The pharmaceutical packaging industry is highly fragmented, with the presence of large and medium-sized international companies as well as small domestic players. Key players include Amcor plc, Becton, Dickinson and Company, AptarGroup, Inc., Drug Plastics Group, Gerresheimer AG, Schott AG, O-I GLASS, INC., SGD Pharma, West Pharmaceutical Services, Inc., Berry Global Group, Inc., WestRock Company, International Paper, Comar, LLC, CCL Industries, and Vetter Pharma International.

Most of the companies offer primary packaging products, including syringes, bottles, vials, closures, and cartridges, among others. A few players, such as International Paper, WestRock Company, and CCL Industries, offer secondary packaging products such as folding cartons. The packaging products are mainly utilized to pack injectable drugs, prescription drugs, and non-prescription drugs.

With growing demand patterns, companies such as Amcor Plc have started acquiring small-scale companies in the emerging market for a higher market share. For instance, in August 2023, Amcor Plc, a prominent player in the creation and manufacturing of sustainable packaging solutions on a global scale, revealed its decision to acquire Phoenix Flexibles Pvt Ltd. This strategic move aims to enhance Amcor's presence in the rapidly growing Indian market by increasing its capacity.

The pharmaceutical industry is increasingly outsourcing packaging operations, driving steady growth in the pharmaceutical contract packaging market as drug manufacturers seek cost efficiency, regulatory compliance, and scalability. Contract packaging providers offer specialized capabilities such as serialization, labeling, blister packaging, and secondary packaging, enabling pharmaceutical companies to focus on core R&D and manufacturing activities.

Furthermore, rising regulatory pressure and corporate sustainability commitments are accelerating the transition toward environmentally responsible solutions, fueling the sustainable pharmaceutical packaging industry. Contract packagers are responding by adopting recyclable materials, reducing plastic usage, incorporating post-consumer recycled content, and optimizing packaging designs to lower environmental impact. The convergence of outsourcing trends and sustainability initiatives is creating new opportunities for innovation, positioning contract packaging providers that align with sustainable practices as key beneficiaries in the evolving pharmaceutical packaging landscape.

Material Insights

Based on material, the market is bifurcated into plastics & polymers, paper & paperboard, glass, aluminum foil, and others. Plastics & polymers held the highest revenue share of 36.62% in 2025. Various types of plastic resins, including PE, PET, PP, PVC, PS, and bioplastics, are widely used for manufacturing pharmaceutical vials, bottles, closures, syringes, pouches, sachets, cartridges, tubes, and blister packs. Polypropylene (PP) accounted for the largest revenue share in the plastic & polymer material segment in 2020 as it offers a combination of beneficial properties, such as mechanical, physical, electrical, and thermal characteristics.

Paper & paperboard are mainly used in secondary and tertiary packaging of pharmaceutical products. Excellent printability, low cost, wide availability, and sustainability of paper & paperboard make them lucrative secondary and tertiary packaging options. Paper-based materials are often used as lidding in blister packs on account of their low cost compared to aluminum lidding. International Paper and WestRock Company are some of the leading manufacturers of paper-based packaging.

Glass is one of the most critical materials used in pharmaceutical packaging due to its exceptional barrier properties. It is impervious to gases, moisture, odors, and microorganisms, making it highly suitable for preserving the stability, sterility, and efficacy of pharmaceutical products. As a result, glass is widely employed in the packaging of liquid and semisolid pharmaceutical formulations across the pharmaceutical glass packaging market. Common applications include injectable vials, ampoules, syrup bottles, cartridges, prefilled syringes, and other primary packaging components that require high chemical resistance and product integrity.

Aluminum is another commonly used material for pharmaceutical packaging. It is used as a lidding material in blister packs owing to its strong barrier and easy-to-tear properties. It is also used to make flexible strip packs used for packing tablets. In addition, most of the seals used in plastic or glass syrup bottles are made of aluminum on account of their strong barrier properties against oxygen and UV light.

The other material segment primarily includes rubber and cotton. Multiple types of rubber, including natural, neoprene, nitrile, butyl, chlorobutyl, bromobutyl, and silicone, are used in pharmaceutical packaging to make closures, cap liners, and bulbs for dropper assemblies. A rubber stopper is primarily used for multiple-dose vials and disposable syringes.

Product Insights

Pharmaceutical packaging is segmented into primary, secondary, and tertiary. The primary segment accounted for the major share of the market in 2026. Primary packaging, such as bottles, tubes, or blister packs, directly comes in contact with the drug and thereby envelopes the drug and protects it from contamination. In addition, it is often involved in dispensing and dosing drug contents. Packaging companies are focusing on easy-to-open closures and the incorporation of dispensing systems that deliver the right dose at the right time, which can aid the elderly population in drug dosage.

Secondary pharmaceutical packaging is a consecutive covering or package that stores several groups of pharmaceutical packages together and protects the packages from external impacts. Secondary packaging is primarily used for branding & display, which play a vital role in the marketing strategy for the product, and logistics, wherein grouping several products together offers ease of handling. Tertiary packaging is used for wrapping or packaging a set of products. The packaging is used for safe handling and smooth transportation of goods. Some of the examples of tertiary packaging include brown cardboard boxes, shrink-wraps, and plastic bags. The increasing trend of e-pharmacy is expected to further increase the adoption of tertiary packaging in the market over the forecast period.

End Use Insights

Pharma manufacturing is the key end use segment that accounted for the highest share of 49.46% in 2025 and is expected to witness strong growth from 2026 to 2033. This is owing to the increasing demand for medicines. As per the World Health Organization (WHO), between 2015 and 2050, the proportion of the world’s population aged over 60 years will nearly double from 12% to 22%. The geriatric population requires additional medical assistance, thereby fueling pharmaceutical manufacturing activities. This, in turn, is likely to boost the demand for pharmaceutical packaging.

Market players in the pharmaceutical industry have increased the outsourcing of packaging activities to save on expenses and time. Instead of investing in packaging products, manufacturers are outsourcing packaging operations to specialized and highly capable contractors to ensure efficient packaging. This is expected to push the demand for contract manufacturing and pharmaceutical packaging equipment. Retail pharmacies are increasingly incorporating branding activities on their packaging to differentiate themselves from others. Polybags and paper pouches are the commonly used packaging products by such retail pharmacies. The increasing penetration of retail, especially in developing countries like India, China, and Brazil, is expected to boost the retail pharmacy end-use segment. Institutional pharmacies are the pharmaceutical outlets operating within the institutions, such as medical hospitals, nursing care facilities, and assisted living communities. An increasing number of hospitals and nursing homes and rising healthcare spending are likely to have a positive impact on the institutional pharmacy end-use segment.

Region Insights

North America dominated the market with a revenue share of 33.80% in 2025, wherein pharma manufacturing, which includes in-house production, was the largest end-use segment in the region. The presence of a large number of manufacturers of pharmaceutical plastic bottles in the country, such as AptarGroup Inc., Gerresheimer AG, Amcor Ltd., and Berry Plastics Group, Inc., is likely to have a positive impact on the demand for pharmaceutical plastic bottles over the forecast period.

U.S. Pharmaceutical Packaging Market Trends

The pharmaceutical packaging market in the U.S. represents the largest and most technologically advanced country in the world. Demand is driven by a sophisticated healthcare infrastructure, stringent regulatory requirements, and high levels of innovation in drug development, particularly in biologics and specialty medications that require complex packaging solutions. Packaging companies in the U.S. prioritize patient safety features such as serialization, tamper-evident designs, and smart tracking systems to meet FDA regulations and ensure supply chain integrity. With continued growth in specialty therapeutics and emphasis on patient-centric packaging, the U.S. market is expected to maintain steady expansion in both traditional and advanced packaging segments.

Europe Pharmaceutical Packaging Market Trends

The pharmaceutical packaging market in Europe is well-established, underpinned by a large pharmaceutical manufacturing base and harmonized regulatory frameworks across the EU. The industry places strong emphasis on compliance, quality assurance, and sustainability, leading to widespread adoption of recyclable materials and environmentally friendly packaging formats. European regulatory mandates, including stringent serialization and anti-counterfeiting requirements, further elevate demand for sophisticated packaging technologies. Countries such as France, Italy, and the UK contribute to a diversified regional market where sustainability and regulatory compliance remain central drivers of growth.

Germany pharmaceutical packaging market holds a leading position within the continent’s pharmaceutical packaging landscape. A robust domestic pharmaceutical production sector, covering both small-molecule drugs and biologics, supports high packaging demand across multiple formats. Germany’s regulatory environment strongly emphasizes product safety, quality assurance, and environmental responsibility, encouraging innovation in areas such as recyclable materials and tamper-resistant solutions. The country’s strong industrial base and focus on advanced manufacturing technologies position it as a key regional hub for both conventional and next-generation pharmaceutical packaging solutions.

Asia Pacific Pharmaceutical Packaging Market Trends

The pharmaceutical packaging market in the Asia Pacific region is the fastest-growing globally, driven by rapid industrialization, expanding healthcare access, and rising pharmaceutical production across major economies such as India, China, Japan, and South Korea. Growth is supported by increasing domestic demand for medicines, rising exports of generic drugs, and growing investments in manufacturing infrastructure. Packaging companies in the region are scaling up capacity and integrating automation to meet demand for high-barrier materials, child-resistant features, and unit-dose formats. The combination of cost-competitive manufacturing and rising adoption of modern packaging technologies makes the Asia Pacific a critical growth engine for the global pharma packaging industry.

China pharmaceutical packaging market stands out as one of the most dynamic segments within the Asia Pacific region. Fueled by rapid expansion in both domestic drug consumption and pharmaceutical exports, the country is accelerating production of advanced therapies, including biologics and high-value specialty drugs. Strengthened regulatory oversight and national initiatives to improve quality standards have heightened the adoption of modern packaging solutions that enhance traceability and safety. In addition, sustainability goals and industry partnerships are expanding the use of recyclable and eco-friendly materials. Together, these factors position China as a major driver of growth and innovation in the global pharmaceutical packaging landscape.

Key Pharmaceutical Packaging Company Insights

The global market is highly competitive owing to the presence of numerous players across the globe. Moreover, key players are consolidating their market positions mainly by acquisitions, which is further intensifying the competition. Key players directly compete with each other in securing agreements from large pharmaceutical manufacturers. Thus, the competitive rivalry in the global market is observed to be high.

Players are focusing on offering value-added services to attract a greater number of clients. Spray painting, ultraviolet coating, and metallization are the commonly employed processes for coloring packaging containers that are used by packaging manufacturers. In addition, labeling and the incorporation of various anti-counterfeit packaging measures, including overt and covert technologies, such as barcodes, holograms, sealing tapes, and radio frequency identification devices, are often undertaken by the packaging manufacturers.

-

In November 2023, Amcor Plc, a renowned global company known for its development and production of environmentally conscious packaging solutions, revealed a Memorandum of Understanding (MOU) with NOVA Chemicals Corporation, a leading producer of sustainable polyethylene. The agreement includes the procurement of mechanically recycled polyethylene resin (rPE) from NOVA Chemicals Corporate, which will be utilized in the production of flexible packaging films. This initiative aligns with Amcor's dedication to promoting packaging circularity by increasing the utilization of rPE in flexible packaging applications.

-

In July 2023, Constantia Flexibles introduced a new pharmaceutical packaging solution called REGULA CIRC, which utilizes coldform foil. The packaging replaces conventional PVC with a PE sealing layer, resulting in a reduction in plastic content while increasing the proportion of aluminum. This optimization not only enhances the sustainability of the packaging but also improves material recovery during recycling processes.

-

In April 2023, Südpack introduced its PharmaGuard blister, a polypropylene-based blister packaging. This new product offers an outstanding water vapor barrier along with effective barrier resistance against UV and oxygen.

Key Pharmaceutical Packaging Companies:

The following are the leading companies in the pharmaceutical packaging market. These companies collectively hold the largest market share and dictate industry trends.

- Amcor plc

- Becton, Dickinson, and Company

- AptarGroup, Inc.

- Drug Plastics Group

- Gerresheimer AG

- Schott AG

- Owens Illinois, Inc.

- West Pharmaceutical Services, Inc.

- Berry Global, Inc.

- WestRock Company

- SGD Pharma

- International Paper

- Comar, LLC

- CCL Industries, Inc.

- Vetter Pharma International

Pharmaceutical Packaging Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 166.4 billion

Estimated Market size in 2026

USD 182.2 billion

Projected Market size by 2033

USD 353.1 billion

Growth rate

CAGR of 9.9% from 2026 to 2033

Historical data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, competitive landscape, growth factors, and trends

Segments covered

Product, material, end use, region

States scope

North America; Europe; Asia Pacific; Latin America; MEA

Country Scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; Russia; Turkey; China; India; Japan; South Korea; Southeast Asia; Brazil; Argentina; GCC; Egypt

Key companies profiled

Amcor plc; Becton, Dickinson, and Company; AptarGroup, Inc.; Drug Plastics Group; Gerresheimer AG; Schott AG; Owens Illinois, Inc.; West Pharmaceutical Services, Inc.; Berry Global, Inc.; WestRock Company; SGD Pharma; International Paper; Comar, LLC; CCL Industries, Inc.; Vetter Pharma International

Customization scope

Free report customization (equivalent up to 8 analyst’s working days) with purchase. Addition or alteration to country, regional, and segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Pharmaceutical Packaging Market Report Segmentation

This report forecasts revenue growth at a global level and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global pharmaceutical packaging market report based on product, material, end use, and region:

-

Material Outlook (Revenue, USD Million, 2021 - 2033)

-

Plastics & Polymers

-

Polyvinyl Chloride (PVC)

-

Polypropylene (PP)

-

Homo

-

Random

-

-

Polyethylene Terephthalate (PET)

-

Polyethylene (PE)

-

HDPE

-

LDPE

-

LLDPE

-

-

Polystyrene (PS)

-

Others

-

-

Paper & Paperboard

-

Glass

-

Aluminium Foil

-

Others

-

-

Product Outlook (Revenue, USD Million, 2021 - 2033)

-

Primary

-

Plastic Bottles

-

Caps & Closures

-

Parenteral Containers

-

Syringes

-

Vials & Ampoules

-

Others

-

-

Blister Packs

-

Prefillable Inhalers

-

Pouches

-

Medication Tubes

-

Others

-

-

Secondary

-

Prescription Containers

-

Pharmaceutical Packaging Accessories

-

-

Tertiary

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Pharma Manufacturing

-

Contract Packaging

-

Retail Pharmacy

-

Institutional Pharmacy

-

-

Region Outlook (Revenue, USD Million 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

France

-

UK

-

Italy

-

Spain

-

Russia

-

Turkey

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South East Asia

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Egypt

-

GCC

-

-

Frequently Asked Questions About This Report

Asia Pacific is the fastest-growing region over the forecast period.

The primary segment led with a 76.4% revenue share in 2025, driven by the critical role of bottles, tubes, or blister packs that directly come into contact with drugs.

Plastics & polymers held the largest revenue share of 36.6% in 2025, owing to their versatility, durability, and cost efficiency.

The global pharmaceutical packaging market size was valued at USD 166.4 billion in 2025 and is estimated at USD 182.2 billion for 2026.

The global pharmaceutical packaging market is expected to grow at a CAGR of 9.9% from 2026 to 2033, reaching USD 353.1 billion.

The key market player in the global pharmaceutical packaging market includes Amcor plc, Becton, Dickinson and Company, AptarGroup, Inc., Drug Plastics Group, Gerresheimer AG, Schott AG, Owens Illinois Inc., West Pharmaceutical Services, Inc., Berry Global Inc., WestRock Company, SGD Pharma, International Paper, Comar, LLC, CCL Industries, Inc, Vetter Pharma International.

Key factors that are driving the pharmaceutical packaging market growth include the growing pharmaceutical industry most notably in several emerging economies including China, India, and Brazil on account of increasing population, rising disposable income, and growing focus on increasing life expectancy.

Pharma manufacturing segment held the largest share with 49.5% in 2025, owing to increasing demand for medicines worldwide.

North America emerged as a dominating region with a value share of 33.8% in the year 2025 owing to the increased production of branded drugs, strong healthcare system, high per capita income, and large investments in drug development in countries such as the U.S.

About the Author(s)

Plastics, Polymers & Resins Research Team

Bulk Chemicals · Plastics, Polymers & ResinsThis report was authored by the plastics, polymers & resins research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the plastics, polymers & resins segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.