- Home

- »

- Plastics, Polymers & Resins

- »

-

Plastic Compounding Market Size, Share Report, 2026-2033GVR Report cover

![Plastic Compounding Market (2026 - 2033)Report]()

Plastic Compounding Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product (PE, PP, PVC, PS, PET, PBT, PA, PC, PU, PMMA, ABS), By Application (Automotive, Aerospace & defense, Electrical & electronics), By Region, And Segment Forecasts

Market Size, 2025

$76.6BMarket Estimate, 2026

$82.2BMarket Forecast, 2033

$133.7BCAGR, 2026–2033

7.2%Plastic Compounding Market Summary

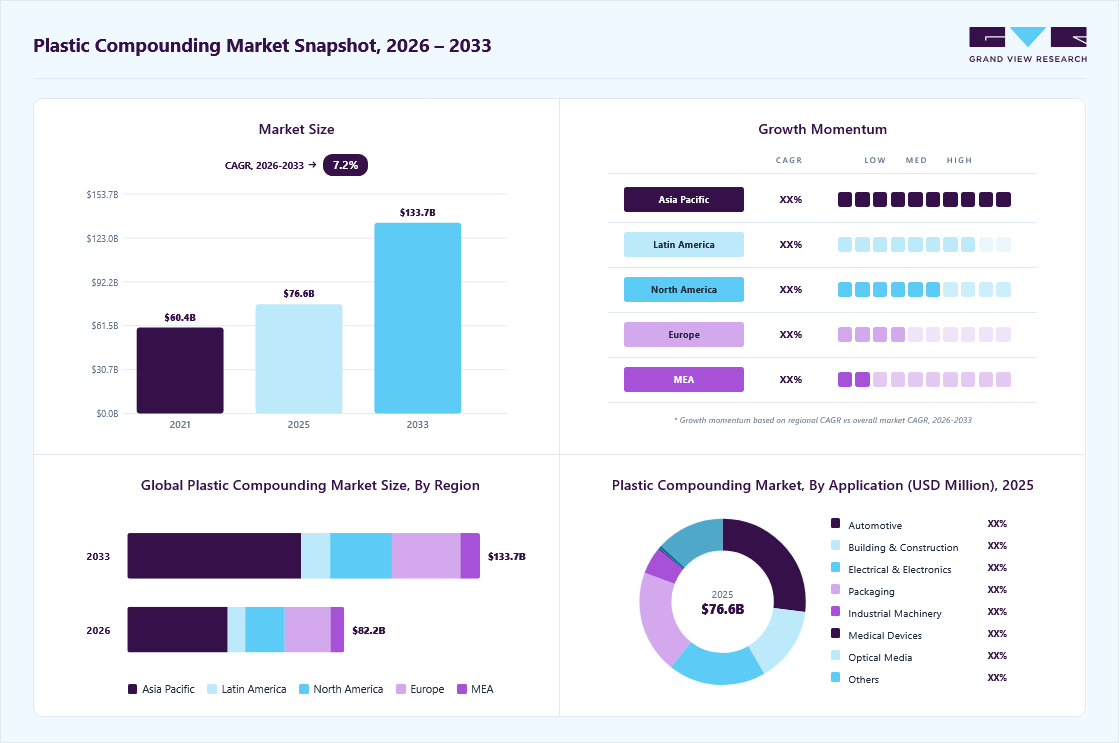

The global plastic compounding market size was valued at USD 76.6 billion in 2025 and is projected to grow from USD 82.2 billion in 2026 to USD 133.7 billion by 2033, at a CAGR of 7.2% from 2026 to 2033. The Asia Pacific market held the largest share of 45.8% of the global market in 2025. Increasing substitution of natural rubber, wood, metals, glass, and concrete with plastic is expected to drive the growth of the plastic compounding industry over the forecast period.

Key Market Trends & Insights

- By product: The polypropylene (PP) dominated the product segment in 2025, with a market share of 30.4%.

- By application: The automotive sub-segment dominated the application segment in 2025, with a market share of 25.4%.

Regional Highlights

- Largest regional market: Asia Pacific (45.8% revenue share, 2025)

- By country: The China held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 76.6 Billion

- Estimated market size in 2026: USD 82.2 Billion

- Projected market size by 2033: USD 133.7 Billion

- CAGR (2026-2033): 7.2%

The demand for plastic is rising due to its use in various industrial applications, thanks to its ability to form desired shapes and its ease of molding. Plastic fittings are considered easier to install than metal or wood fittings. These fittings are available in a wide range of color combinations, which adds to their aesthetic appeal.

")

Rising demand for plastic compounded resins in comparison to the traditional plastic resins across various industries, including automotive and others, has provided an opportunity for the plastic compounding market to propel globally. Compared to traditional materials such as rubber or metals, the usage of plastic-compounded goods in automotive applications helps minimize fuel consumption by reducing the density and weight of cars. Over the projected period, rising consumer awareness of safety and health concerns across industries such as electronics, healthcare, wire & cable, construction, and automotive is expected to increase global demand for plastic compounding the manufacture compounded resins.

Drivers, Opportunities & Restraints

Demand is being supported by stricter hygiene expectations in food-contact and healthcare applications. FDA treats antimicrobials used in food packaging as food additives and requires a premarket safety review, thereby formalizing the approval pathway for compliant uses. At the same time, USDA research on antimicrobial food packaging focuses on delivering additives to food surfaces to reduce pathogens, extend shelf life, and improve food safety.

The strongest growth potential is in active packaging and biodegradable material platforms that combine shelf-life extension with antimicrobial functionality. USDA research projects on PLA-based active multilayer packaging and smart food packaging show room for fresh produce, ready-to-eat foods, and other high-spoilage categories. There is also room to expand into building products and technical plastics where antimicrobial control can support durability, odor resistance, and product differentiation.

Regulatory scrutiny remains a material barrier because antimicrobial additives are subject to detailed safety reviews, labeling requirements, and use-specific authorization. In the EU, treated articles and biocidal products fall under the Biocidal Products Regulation, which adds technical data and compliance requirements. In food-contact uses, the FDA requires rigorous scientific assessment before market entry. Broader antimicrobial resistance concerns also keep pressure high on product claims and active ingredient selection.

Market Concentration & Characteristics

The global plastic compounding industry is highly consolidated in nature, with the presence of various key players such as BASF SE, SABIC, Dow Inc., DuPont de Nemours, Inc., LyondellBasell Industries Holdings B.V., RTP Company, and Kingfa SCI. & TECH. CO., LTD., as well as a few medium and small regional players operating in different parts of the world. The global players face intense competition from each other as well as from the regional players who have strong distribution networks and good knowledge about suppliers & regulations.

The companies in the market compete on the basis of product quality offered and the technology used for the production of plastics. Major players, in particular, compete on the basis of their application development capabilities and the new technologies used in product formulation. Established players such as BASF SE are investing in research & development activities to formulate new and advanced plastics compounds, which gives them a competitive edge over the other players.

To maintain a strong and healthy competitive environment across the marketspace, the global plastic compounding companies manufacturing compounded plastics have implemented various strategic initiatives, such as acquisitions and mergers, new product launches, production expansions, and others. For instance, in October 2023, Covestro AG launched its new mechanical recycling polycarbonate compounding production unit in Shanghai, China, with a plastic compounding capacity of 25 kilotons per annum.

Product Insights

Polypropylene (PP) dominated the product segment in 2025, with a market share of 30.4%. Polypropylene can be processed using any of the thermoplastic processing methods, including injection molding, extrusion, blow molding, and general-purpose extrusion. It has good fatigue and chemical & temperature resistance. Although polypropylene is vulnerable to oxidative degradation in contact with copper and certain other materials. This has made it a popular material in developed and emerging economies for several application industries.

Automotive is the largest application segment for polypropylene (PP) compounds due to their high impact resistance and ease of maintenance. The rise of auto manufacturing in the Asian and Latin American markets has fueled the growth of the automotive sector, both in terms of vehicle sales and domestic production. Consumption of plastic compounds in automotive applications is expected to increase significantly over the forecast period due to continued growth in the automotive output market, as well as regulatory trends that are forcing manufacturers to reduce vehicle weight and improve energy efficiency.

Followed by polyethylene (PE) with a market revenue share of 20.4% in 2025. Polyethylene compounds are widely used in various industries such as automotive, construction, electrical & electronics, and packaging. PE is an integral material for the packaging industry. Construction is the leading application market for polyethylene compounds, with a significant market share in the global market.

Application Insights

The automotive sub-segment dominated the application segment in 2025, with a market share of 25.4%. Exterior body parts, wiper arm casings and housings, bumpers, moldings, ignition, front grilles, cladding, roof trim, and other automobile applications all use PP and PET compounds. Low thermal expansion, high stiffness, lightweight, dimensional stability, moisture resistance, exceptional scratch resistance, and impact resistance in low temperatures are just a few of the properties that these materials possess.

Several grades of PP and PET compounds have been developed over the past years to meet diverse performance requirements. The growing demand for sustainable materials in this segment has been a major driver for lightweight plastic. In addition, the implementation of emission norms and vehicular weight regulations in the automotive industry, owing to rising greenhouse gas emissions, is anticipated to propel the demand for global automotive plastic compounding over the forecast period.

Followed by packaging with a market revenue share above 18.0% in 2023. Demand for compounded plastics in the packaging industry is driven by mass consumption in major economies such as China, India, Germany, the United States, and Brazil. Various regulatory agencies have established guidelines for packaging materials for food contact applications. The polypropylene formulation provides a cost-effective packaging solution that helps improve impact strength, flexibility, transparency, and process efficiency. The high demand for polyethylene in the packaging industry has contributed significantly to the growth of the plastic compounding market.

Regional Insights

Asia Pacific dominated the market and held a revenue share of 45.8% in 2025, owing to the favorable conditions in Asia Pacific, such as increasing manufacturing output, a booming e-commerce market, and favorable demographics, which are promising. Investments in six Asian economies (China, Thailand, Indonesia, India, Vietnam, and Malaysia) for developing talent, improving infrastructure, and supply chain facilities are expected to drive the market growth.

Increasing demand for consumer goods such as refrigerators and washing machines in countries such as India, Vietnam, the Philippines, China, and Thailand is expected to fuel the demand for plastic compounding in these applications. Growing demand for automotive in the region, coupled with favorable FDI norms by governments, is further projected to facilitate investment in the Asia Pacific. In addition, low manufacturing costs in China and India, as compared to Europe is expected to propel the use of plastic compounding in automobiles.

Followed by Europe, with a market revenue share of above 21.0% in 2023. Growth in automotive production, a high standard of living, and a growing aging population are significantly contributing towards growth for plastic compounding in Europe. Well-developed infrastructure, along with the presence of renowned automakers including Fiat, BMW, and Volkswagen, among others are propelling the development of the automotive market in this region, which in turn is creating an application scope of plastic compounding in this region.

Key Plastic Compounding Company Insights

Key companies are adopting several organic and inorganic growth strategies, such as capacity expansion, mergers & acquisitions, and joint ventures, to maintain and expand their market share.

-

In October 2025, Mitsui Chemicals, Inc. revealed that the companies had finalized a contract concerning the marketing operations for engineering plastics products, particularly the ARLEN and AURUM brands developed and offered by Mitsui Chemicals. Under this agreement, beginning January 1, 2026, Mitsui Chemicals will delegate certain marketing functions to Polyplastics. Polyplastics will exclusively manage marketing tasks such as customer engagement, the development of new clients, and the provision of technical assistance.

-

In May 2025, DOMO Chemicals, a prominent global provider of high-performance solutions under the TECHNYL brand, officially enhanced its compounding operations in Mumbai, India. This strategic growth reinforces DOMO’s role as a solutions provider in the area and broadens its range of engineered materials derived from polyamides and various resins.

Key Plastic Compounding Companies:

The following key companies have been profiled for this study on the plastic compounding market.

- SABIC

- Dow, Inc.

- KRATON CORPORATION

- LyondellBasell Industries Holdings B.V.

- DuPont de Nemours, Inc.

- RTP Company

- S&E Specialty Polymers, LLC (Aurora Plastics)

- Asahi Kasei Corporation

- Covestro AG

- Washington Penn

- Eurostar Engineering Plastics

- KURARAY CO., LTD.

- Arkema

- TEIJIN LIMITED

- LANXESS

- Solvay

- SO.F.TER

- Polyvisions, Inc.

- Ravago

Plastic Compounding Market Report Scope

Report Attribute

Details

Market size in 2025

USD 76.6 billion

Market size value in 2026

USD 82.2 billion

Revenue forecast in 2033

USD 133.7 billion

Growth rate

CAGR of 7.2% from 2026 to 2033

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Volume in kilotons, revenue in USD million, and CAGR from 2026 to 2033

Report coverage

Volume forecast, revenue forecast, competitive landscape, growth factors, and trends

Segments covered

Product, application, region

Regional scope

North America; Europe; Asia Pacific; Central & South America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; Netherlands; China; India; Japan; South Korea; Singapore; Malaysia; Indonesia; Thailand; Vietnam; Australia; Brazil; Argentina; Saudi Arabia; United Arab Emirates (UAE); South Africa

Key companies profiled

SABIC; Dow, Inc.; KRATON CORPORATION; LyondellBasell Industries Holdings B.V.; DuPont de Nemours, Inc.; RTP Company; S&E Specialty Polymers, LLC (Aurora Plastics); Asahi Kasei Corporation; Covestro AG; Washington Penn; Eurostar Engineering Plastics; KURARAY CO., LTD.; Arkema; TEIJIN LIMITED; LANXESS; Solvay; SO.F.TER; Polyvisions, Inc.; Ravago

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Plastic Compounding Market Report Segmentation

This report forecasts revenue and volume growth at the global, regional, and country levels and provides an analysis of the latest industry trends and opportunities in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global plastic compounding market report based on product, application, and region:

-

Product Outlook (Volume, Kilotons; Revenue, USD Million; 2021 - 2033)

-

Polyethylene (PE)

-

Polypropylene (PP)

-

Thermoplastic Vulcanizates (TPV)

-

Thermoplastic Polyolefins (TPO)

-

Polyvinyl Chloride (PVC)

-

Polystyrene (PS)

-

Polyethylene Terephthalate (PET)

-

Polybutylene Terephthalate (PBT)

-

Polyamide (PA)

-

Polycarbonate (PC)

-

Polyurethane (PU)

-

Polymethyl Methacrylate (PMMA)

-

Acrylonitrile Butadiene Styrene (ABS)

-

Others

-

-

Application Outlook (Volume, Kilotons; Revenue, USD Million; 2021 - 2033)

-

Automotive

-

Building & construction

-

Electrical & electronics

-

Packaging

-

Consumer goods

-

Industrial machinery

-

Medical devices

-

Optical media

-

Aerospace & defense

-

Others

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Million 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

Netherlands

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Singapore

-

Malaysia

-

Indonesia

-

Thailand

-

Vietnam

-

Australia

-

-

Central & South America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

United Arab Emirates (UAE)

-

South Africa

-

-

Frequently Asked Questions About This Report

The global plastic compounding market size was estimated at USD 76.6 billion in 2025 and is expected to reach USD 82.2 billion in 2026.

The global plastic compounding market is expected to grow at a compound annual growth rate of 7.2% from 2026 to 2033 to reach USD 133.7 billion by 2033.

Some key players operating in the plastic compounding market include BASF SE, LyondellBasell Industries, N.V., and The Dow Chemical Company, SABIC, Asahi Kasei Plastics, Covestro (Bayer Material Science), and others.

Key factors that are driving the plastic compounding market growth include increasing incorporation of plastics as opposed to metals and alloys in automotive components and rising demand from the packaging, building & construction sectors.

The polypropylene segment dominated the plastic compounding market with a share of 30.4% in 2025. This is attributable to the rising demand from the automotive industry owing to the high impact resistance and serviceability.

Asia Pacific dominated with a 45.8% revenue share in 2025.

The automotive segment led with a 25.4% revenue share in 2025.

About the Author(s)

Plastics, Polymers & Resins Research Team

Bulk Chemicals · Plastics, Polymers & ResinsThis report was authored by the plastics, polymers & resins research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the plastics, polymers & resins segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.