- Home

- »

- Plastics, Polymers & Resins

- »

-

Polyolefin Market Size, Share And Growth Report, 2026-2033GVR Report cover

![Polyolefin Market (2026 - 2033)Report]()

Polyolefin Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product (PE, PP, EVA, TPO, POM, PC, PMMA), By Application (Film & Sheet, Injection Molding, Blow Molding), By Region (North America, Europe, APAC, Central & South America, MEA), And Segment Forecasts

Market Size, 2025

$274.4BMarket Estimate, 2026

$287.1BMarket Forecast, 2033

$432.4BCAGR, 2026–2033

6.0%Polyolefin Market Summary

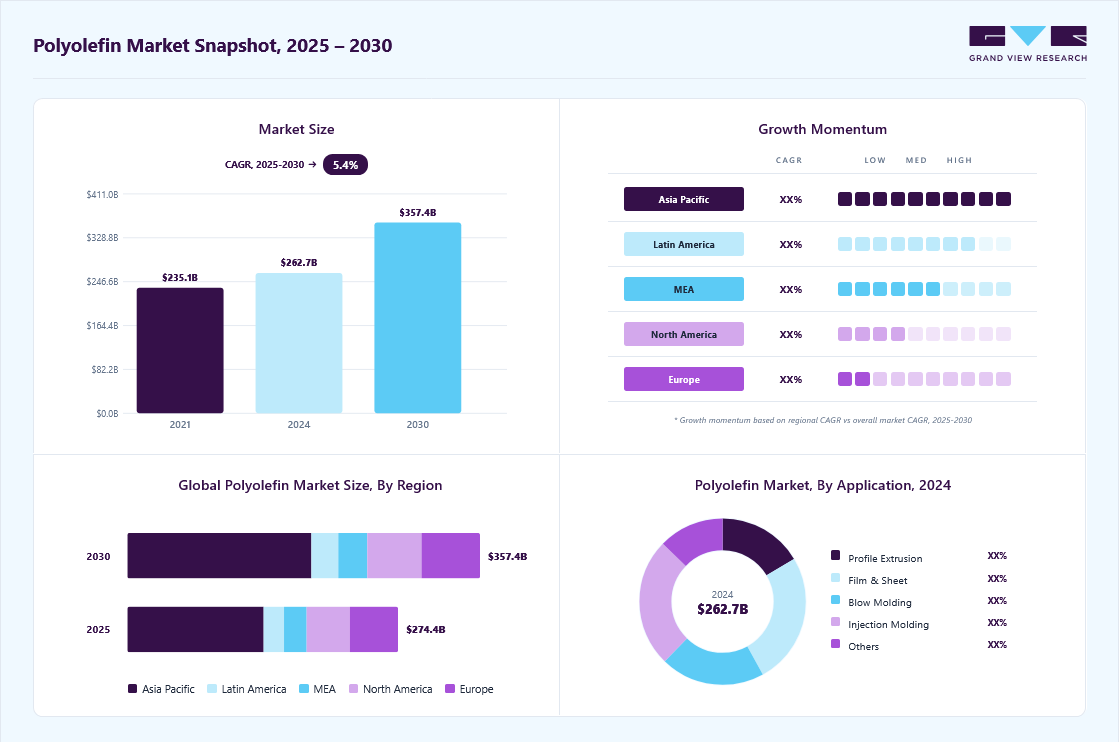

The global polyolefin market size was valued at USD 274.4 billion in 2025 and is projected to grow from USD 287.1 billion in 2026 to USD 432.4 billion by 2033, growing at a CAGR of 6.0% from 2026 to 2033. The market in Asia Pacific dominated with a revenue share of 50.3% in 2025. The market is poised for growth due to increasing adaptation across the end-use industries.

Key Market Trends & Insights

- By product: Polyethylene (PE) segment dominated the market, with a revenue share of 37.4% in 2025.

- By application: Film & sheet segment held the largest market share of 25.6% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (50.3% revenue share, 2025)

- By country: The China held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 274.4 Billion

- Estimated market size in 2026: USD 287.1 Billion

- Projected market size by 2033: USD 432.4 Billion

- CAGR (2026-2033): 6.0%

The use of polyolefins in automotive applications helps reduce fuel consumption on account of their ability to reduce the density and weight of vehicles compared to conventional materials such as rubber and metal. Increasing awareness regarding health hazards and consumer safety in various industries, such as electronics, healthcare, wire and cable, construction, and automotive, is expected to drive the global market over the forecast period. The rapidly developing automotive industry is expected to trigger the demand for plastics in under-the-hood components as well as exteriors and interiors of automobiles. Polyolefins are mainly used in under-the-hood components in the automotive industry.")

The demand for polyolefins such as polyethylene, polypropylene, ethylene-vinyl acetate, and thermoplastics is expected to grow over the forecast period. This is due to the surging usage of medical masks, gloves, shoe & head covers, and gowns owing to rising health awareness among the masses and their increasing focus on hygiene and infection prevention.

The proposed USD 2 trillion investment of the Federal Government of the U.S. in a 10-year infrastructure development plan is poised to capitalize on the low-risk environment, stable economy, and strong financial sector of the country. These favorable conditions have already attracted significant investor interest, fostering a conducive atmosphere for surged infrastructure expenditure and development in the U.S. This, in turn, is projected to positively impact the demand for polyolefins from the construction industry of the country.

Thermoplastic polyolefins segment of the market in the U.S. is projected to grow at a significant rate during the forecast period owing to an exceptional combination of durability, weather resistance, easy process ability, and versatility which refers to their ability to be molded and reshaped when heated, and solidify when cooled, without undergoing significant chemical change offered by them. This makes thermoplastic polyolefins highly sought-after materials in the U.S. for use in the automotive, construction, and consumer goods industries.

Market Dynamics

The polyolefin market is driven by broad, repeat consumption across packaging, automotive, construction, healthcare, and consumer goods, with film and sheet as the leading application and Asia Pacific as the dominant demand center. Demand is structurally concentrated in China, India, Japan, and other industrializing Asian markets, where capacity growth and end-use conversion are tightly linked. Commercially, the market remains price sensitive and moderately fragmented, with integrated producers competing through scale, process efficiency, and product qualification. Sustainability requirements are also reshaping commercial decisions, pushing suppliers toward recyclable grades, advanced catalysts, and lower-carbon production routes.

Polyolefin demand is being supported by its role as a low-cost, lightweight, and processable material across high-volume conversion industries. The report page highlights strong use in automotive, electronics, healthcare, wire and cable, construction, and packaging, while film and sheet remains the largest application segment. This reflects the commercial advantage of polyolefins in applications that require puncture resistance, clarity, durability, and efficient molding or extrusion performance. PE and PP remain core resins because they fit mass-market packaging, bottles, caps, containers, and molded parts with established processing economics.

A second layer of demand comes from regional industrial expansion, especially in Asia Pacific, where rising disposable incomes, infrastructure buildout, and manufacturing density sustain resin consumption across packaging and durable goods. At the same time, automotive lightweighting is keeping polyolefins relevant in under-the-hood, interior, and exterior applications where material substitution against metal and rubber improves cost and fuel efficiency. The market therefore benefits not only from unit volume growth, but also from continual replacement demand in established conversion chains.

The main restraint is persistent margin pressure in a commodity market that remains highly exposed to feedstock swings, pricing competition, and cyclical capacity additions. Because polyolefins are broadly available and technically mature, producers often compete on price and delivery reliability rather than on wide differentiation. The report also notes rising regulatory scrutiny around sustainability and circular economy requirements, which increases the burden of capital spending on recycling systems, advanced catalyst development, and lower-emission production. These factors can compress profitability, particularly for suppliers without upstream integration or specialty-grade differentiation.

The strongest opportunity lies in recyclable, bio-based, and performance-enhanced polyolefins. The market is already seeing R&D activity in advanced catalyst systems, metallocene-based grades, and bio-based alternatives, which broaden the commercial scope beyond standard commodity resin. Suppliers that can pair circularity claims with processing consistency, application qualification, and end-use performance will be better positioned to capture premium demand from packaging, automotive, and infrastructure converters.

Market Concentration & Characteristics

The market is moderately fragmented, with key participants involved in R&D and technological innovations. Notable companies include China Petrochemical Corporation, LyondellBasell Industries Holdings B.V., PetroChina Company Limited, TotalEnergies, Chevron Corporation, Repsol, Dow, Inc., among others. Several players are engaged in framework development to improve their market share.

The polyolefin market is anticipated to grow due to robust demand from end-users and significant innovations aimed at improving both material performance and sustainability. Ongoing research and development efforts are resulting in the creation of advanced catalyst systems, metallocene-based polyolefins, and bio-based alternatives, which broaden application possibilities and enhance recyclability.

Additionally, the market is seeing a rise in merger and acquisition activities, as leading companies aim to broaden their product offerings, integrate operations, and extend their geographic presence—especially in rapidly growing regions like Asia-Pacific and the Middle East. This trend of consolidation, along with advancements in technology, is likely to boost economies of scale and speed up the adoption of specialty and high-performance polyolefins in packaging, automotive, and infrastructure industries.

The polyolefin market is anticipated to be influenced by changing regulatory frameworks, a low risk from alternative products, and concentrated demand from end-users. Increasing regulatory demands that focus on sustainability and circular economy initiatives are fostering innovation in recyclable and bio-based polyolefins, prompting manufacturers to invest in more sustainable production methods and advanced recycling technologies. Although environmental concerns are rising, the threat posed by alternatives like bioplastics or engineered resins remains moderate, thanks to the cost-effectiveness, versatility, and well-established processing systems of polyolefins.

Analyst Perspective

The polyolefin market is moving from volume-led growth toward a more performance- and sustainability-led phase, where demand will continue to be anchored by packaging, automotive, consumer goods, infrastructure, and industrial applications. While commodity PE and PP grades will remain the backbone of consumption, stronger value creation is expected in differentiated grades that offer lightweighting, durability, processability, recyclability, and compatibility with circular economy requirements. Companies with feedstock integration, regional production strength, recycling partnerships, and the ability to develop application-specific grades are likely to be better positioned, while margin pressure may persist for players exposed to feedstock volatility, oversupply cycles, and tightening plastic waste regulations.

Product Insights

Based on product, the polyethylene (PE) segment led the market with the largest revenue share of 37.4% in 2025. Polyethylene has witnessed significant growth in recent years, with an increase in utilization across prototype development on 3D printers and CNC machines.

Furthermore, driven by the upsurge in industrialization, China, India, and Japan have emerged as prominent countries in the polyethylene market across the Asia Pacific (APAC) region. The expansion of the construction and furniture sectors, along with the presence of major automotive industries and increasing demand for sophisticated infrastructure, has emerged as a pivotal catalyst propelling the polyethylene industry in the Asia Pacific.

For instance, in April 2025, STEER World, a company specializing in materials transformation technology, introduced an innovative method to recycle crosslinked polyethylene (XLPE), which has been regarded as non-recyclable for a long time, by employing its unique Omega Twin-Screw Extrusion Technology. Frequently utilized in cable insulation, piping systems, and various high-performance applications, XLPE is known for its remarkable durability, which is attributed to its three-dimensional network of covalent bonds. While this structure provides exceptional thermal and mechanical resilience, it also renders the material challenging to recycle through traditional methods. As a result, most XLPE waste is disposed of in landfills, raising ongoing environmental issues.

Following polyethylene, polypropylene witnessed a market revenue share above 27.0% in 2024. Polypropylene can be easily manufactured into living hinges, extremely thin plastics that can be bent without breaking. Although polypropylene is not particularly used in structural applications, it finds its major usage in applications such as bottling certain edible products or even liquid soaps, shampoos, and more.

Ethylene vinyl acetate (EVA) is a redispersible polymer that is available in the form of a free-flowing powder. It shares resemblances with low-density polyethylene, showcasing heightened gloss, softness, and flexibility. These polyolefins exhibit excellent performance under low temperatures and are commonly employed as hot-melt adhesives, finding widespread application in products like soccer cleats and plastic wraps. Furthermore, EVA extends its utility to biomedical engineering, serving as a part and component of a drug delivery device in various healthcare applications.

Application Insights

Based on application, the film & sheet segment led the market with the largest revenue share of 25.6% in 2025. Polyolefins provide high-quality shrink films with improved clarity and appearance for the consumer goods industry. Polyolefins have stronger puncture resistance, are FDA approved, have no chlorine content, and are more durable; however, they are relatively more expensive.

Due to increased use in the packaging business, Asia Pacific (APAC) is one of the significant markets for polyolefin, which includes both edible and non-edible goods. Rising disposable income and living standards in China, India, Japan, Malaysia, Indonesia, and Thailand will support industry expansion throughout the forecast period. However, the European market has significant potential due to high demand for polyolefins in the furniture and interior industries.

Growing emphasis on sustainability and progressive efforts to reduce carbon footprint by various consumer electronics manufacturers have augmented the demand for post-consumer recycled plastic resins in recent years. Laptop manufacturers such as Lenovo manufactures notebooks, desktops, workstation, monitors, and other accessories using post-consumer recycled plastic resins. This increasing adoption of post-consumer recycled plastic resins is expected to continue over the forecast period.

Injection molding is used for producing custom polyolefin materials. As polyolefin parts are made in molds and must be cooled before removal, the process is discontinuous. Injection molding necessitates the use of a machine, plastic materials, and molds. To make the final product, molten plastic is pumped into the mold cavity and cooled. It is commonly used in the production of automobile parts, medical devices, containers, and others.

Growing demand for polyolefin injection molding from a variety of end-use sectors, combined with increased manufacturer awareness about the benefits of polyolefin injection molding, is expected to fuel the demand for polyolefin injection molding. Heat and pressure-resistant materials are becoming increasingly popular as infrastructure development accelerates in countries such as Brazil and India. This is likely to increase the use of polyolefin injection molding by manufacturers of building products.

Regional Insights

Asia Pacific dominated the polyolefin market with the largest revenue share of 50.3% in 2025. The region stands out for its abundance of skilled labor available at a low cost and easily accessible land. This shift in production focus toward emerging economies, particularly China and India, is poised to have a positive impact on market growth throughout the forecast period. The region is a major hub for rapidly expanding industries like construction, automotive, and electronics, offering significant potential for polyolefin manufacturers.

Continuing infrastructural investments are expected to sustain economic growth in China, and the automotive, aerospace, and construction sectors are expected to benefit from reforms, including regulatory changes, policy adjustments, or structural enhancements. However, these prospects are not long-term, and growth is likely to remain sluggish in the industrial sector, which is likely to impact the consumption of polyolefin over the forecast period.

The polyolefin market in China held the largest share in the Asia Pacific region in 2025. China's Polyolefin market growth is expected to be driven by increasing domestic demand, expansion of production capacity, and the material's diverse applications. China's robust industrial foundation, along with innovation and sustainability initiatives supported by policy, is anticipated to contribute to the polyolefin market's long-term development.

North America Polyolefin Market Trends

The polyolefin industry in North America is poised for significant growth, fueled by readily available feedstock, expanding end-use industries, and a rising emphasis on sustainable materials.

The U.S. Polyolefin market is projected to experience considerable growth in the next few years, fueled by an uptick in demand from critical sectors like packaging, automotive, and construction. The flexible packaging sector remains on the rise, bolstered by a growing consumer inclination towards lightweight, durable, and recyclable materials, which makes polyethylene (PE) and polypropylene (PP) the ideal material.

Europe Polyolefin Market Trends

The polyolefin market in Europe is likely to witness sluggish growth owing to various factors, such as stalled industrial output caused by economic uncertainties, supply chain disruptions, and regulatory changes, which have collectively impacted market dynamics and expansion. Nevertheless, a promising outlook in Eastern Europe, driven by robust consumerism and manufacturing, is poised to stimulate the growth of the polyolefin market.

The growing industrial advancements, regulatory changes, and increased demand from end-users fuel the Polyolefin market in Germany. A significant emphasis on sustainability and circular economy principles is promoting the usage of recyclable and mechanically recycled polyolefins, especially in the packaging and consumer goods sectors.

Key Polyolefin Company Insights

In the Polyolefin Market, major players have adopted various strategic initiatives, such as new product launches, production expansion, mergers and acquisitions, and others. These initiatives enable the market players to maintain the competitive environment and meet global demand.

-

For instance, in February 2025, CCL Label announced the introduction of a new generation of shrink sleeves crafted from recycling-friendly polyolefin (PO) material in Southeast Asia. The low-density PO material is appropriate for flotation separation during the sink/float process at PET recycling facilities. The advancement of this high-shrink variant of EcoFloat shrink sleeve allows brand customers to transition from PVC or PET-G shrink sleeves, which hinder recycling, to an eco-friendlier alternative made from polyolefin. This material has received approval from recyclers and has been recognized by RecyClass in Europe and APR in the United States.

-

For instance, in October 2024, ExxonMobil unveiled Signature Polymers, a fresh strategy for engaging with customers and the wider value chain. The primary goal of Signature Polymers is to establish itself as the most valued global partner in the industry by enhancing service and collaboration. ExxonMobil will roll out new initiatives designed to inspire and inform how it markets its products and offers support, aiding customers in their innovation, strategy, and growth efforts. This new approach will help customers feel more assured in addressing the intricate challenges of the value chain by simplifying processes and promoting greater collaboration.

Key Polyolefin Companies:

The following are the leading companies in the polyolefin market.

-

China Petrochemical Corporation

-

LyondellBasell Industries Holdings B.V.

-

PetroChina Company Limited

-

TotalEnergies

-

Chevron Corporation

-

Repsol

-

Dow, Inc.

-

Exxon Mobil Corporation

-

Braskem

-

Borealis AG

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weakness

Established Players (China Petrochemical Corporation, LyondellBasell Industries Holdings B.V., PetroChina Company Limited)

- Maintain integrated feedstock-to-polymer production models.

- Expand specialty resin portfolios and sustainable product offerings.

- Optimize global manufacturing footprints and regional supply networks.

- Strong feedstock integration and scale advantages.

- Extensive global distribution and customer relationships.

- Significant R&D investments and technology ownership.

- Exposure to commodity resin pricing cycles.

- Large asset bases can limit operational flexibility.

- Higher regulatory and sustainability compliance obligations.

Emerging Players (Repsol, Braskem)

- Focus on specialty polyolefin grades and application-specific solutions.

- Expand circular polymer and recycled-content portfolios.

- Strengthen partnerships across packaging and automotive value chains.t

- Greater flexibility in specialty product development.

- Strong positioning in sustainability-focused initiatives.

- Ability to target higher-value application segments.

- Smaller global production footprint relative to market leaders.

- Lower bargaining power in some regional markets.

- Greater exposure to competitive pressure from integrated producers.

Polyolefin Market Report Scope

Report Attribute

Details

Market size in 2025

USD 274.4 billion

Estimated market size in 2026

USD 287.1 billion

Projected market size by 2033

USD 432.4 billion

Growth rate

CAGR of 6.0% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, volume in kilotons, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product, application, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; UK; Italy; France; Spain; China; India; Japan; South Korea; Australia; Brazil; Argentina; South Africa; Saudi Arabia

Key companies profiled

China Petrochemical Corporation; LyondellBasell Industries Holdings B.V.; PetroChina Company Limited; TotalEnergies; Chevron Corporation; Repsol; Dow, Inc.; Exxon Mobil Corporation; Braskem; and Borealis AG

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Polyolefin Market Report Segmentation

This report forecasts revenue and volume growth at global, regional & country levels and provides an analysis of the industry trends in each of the sub-segments from 2023 to 2033. For this study, Grand View Research has segmented the global polyolefin market report on the basis of product, application, and region:

-

Product Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Polyethylene (PE)

-

Polypropylene (PP)

-

Ethylene-Vinyl Acetate (EVA)

-

Thermoplastic Polyolefins (TPO)

-

Polyoxymethylene (POM)

-

Polycarbonate (PC)

-

Polymethyl Methacrylate (PMMA)

-

Others

-

-

Application Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Film & Sheet

-

Injection Molding

-

Blow Molding

-

Profile Extrusion

-

Others

-

-

Regional Outlook (Volume, Tons; Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

Italy

-

France

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Central & South America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

South Africa

-

Saudi Arabia

-

-

Research Methodology

Segment Definition

Segment - Product

Revenue capture definition

Polyethylene (PE)

Revenue generated from the sale of high-density, low-density, linear low-density, and specialty polyethylene resins supplied for packaging, construction, consumer goods, wire and cable, and industrial applications.

Polypropylene (PP)

Revenue captured from homopolymer, copolymer, impact-modified, and specialty polypropylene grades utilized in automotive components, rigid packaging, appliances, fibers, and molded products.

Ethylene-Vinyl Acetate (EVA)

Revenue derived from EVA resin sales used in footwear, photovoltaic encapsulation, packaging films, adhesives, foam products, and specialty industrial applications.

Thermoplastic Polyolefins (TPOs)

Revenue generated through compounded and engineered TPO materials supplied for automotive exterior parts, roofing membranes, construction products, and industrial applications.

Polyoxymethylene (POM)

Revenue captured from engineering-grade POM resins utilized in precision components, automotive systems, electrical devices, industrial machinery, and consumer products.

Polycarbonate (PC)

Revenue generated from polycarbonate resin sales serving automotive glazing, electronics, optical media, industrial equipment, medical devices, and construction applications.

Polymethyl Methacrylate (PMMA)

Revenue derived from PMMA materials used in transparent panels, lighting systems, automotive components, signage, displays, and architectural applications.

Others

Revenue generated from specialty polyolefin and related polymer grades serving niche industrial, packaging, infrastructure, electronics, and consumer applications.

Segment - Application

Revenue capture definition

Film & Sheet

Revenue captured from polyolefin consumption in blown films, cast films, shrink films, agricultural films, industrial sheets, and flexible packaging structures.

Injection Molding

Revenue is generated through resin volumes processed into automotive parts, consumer products, industrial components, closures, containers, and household goods using injection molding technologies.

Blow Molding

Revenue derived from polyolefin materials consumed in bottles, drums, fuel tanks, industrial containers, and hollow plastic products manufactured through blow molding processes.

Profile Extrusion

Revenue captured from polyolefin usage in pipes, tubes, construction profiles, cable conduits, window systems, and infrastructure-related extrusion products.

Others

Revenue generated from fibers, rotational molding, thermoforming, compounding, coatings, and specialized conversion processes utilizing polyolefin materials.

Estimation Model

End-Use Demand Screen

Regional Weighting Filter

Product and Application Split

Price and Competitive Validation

Which sectors drive consumption?

Where is demand concentrated?

How does revenue flow?

How is value validated?

This layer anchors the model on consumption from packaging, automotive, construction, and healthcare, establishing the primary volume base.

This layer captures demand concentration in Asia Pacific, North America, Europe, and the rest of the world through region-specific consumption intensity.

This layer allocates revenue across PE, PP, EVA, and the remaining grades, then maps consumption into film, molding, and extrusion channels.

This layer reconciles volume with resin pricing, producer positioning, and commercialization structure to avoid overstating value in commodity-heavy segments.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Country-Level Demand Assessment for Asia Pacific

Detailed evaluation of polyolefin consumption, import dependence, production capacity, pricing trends, and demand outlook across China, India, Japan, South Korea, and Southeast Asian markets.

Supports regional investment prioritization, capacity planning, and market entry decisions through country-specific demand visibility.

Polyolefin Recycling and Circular Economy Analysis

Comprehensive assessment of recycled resin supply, advanced recycling developments, regulatory impacts, sustainability initiatives, and adoption trends across major end-use industries.

Provides visibility into emerging revenue opportunities and long-term sustainability-driven growth areas.

Competitive Benchmarking and Capacity Mapping

Comparative analysis of production capacities, integration levels, product portfolios, geographic footprints, and strategic initiatives of major market participants.

Enables evaluation of competitive intensity, market positioning, and potential partnership or acquisition opportunities.

Frequently Asked Questions About This Report

The global polyolefin market size was valued at USD 274.4 billion in 2025 and is estimated at USD 287.1 billion for 2026.

Key players include China Petrochemical Corporation; LyondellBasell Industries Holdings B.V.; PetroChina Company Limited; TotalEnergies; Chevron Corporation; Repsol; Dow, Inc.; Exxon Mobil Corporation; Braskem; and Borealis AG.

Key factors that are driving the polyolefin market growth include rising innovation in plastic technologies, the advent of cheap interior furnishings in automobiles, and strict industrial standards concerning carbon emissions.

The Asia Pacific polyolefin market is expected to grow at the fastest CAGR of 6.8% over the forecast period.

The use of polyolefins in automotive applications helps reduce fuel consumption on account of their ability to reduce the density and weight of vehicles compared to conventional materials such as rubber and metal. Increasing awareness regarding health hazards and consumer safety in various industries, such as electronics, healthcare, wire and cable, construction, and automotive, is expected to drive the global market over the forecast period. The rapidly developing automotive industry is expected to trigger the demand for plastics in under-the-hood components as well as exteriors and interiors of automobiles. Polyolefins are mainly used in under-the-hood components in the automotive industry.

Asia Pacific dominated the polyolefin market with the largest revenue share of 50.3% in 2025.

The polyethylene (PE) segment led the market with the largest revenue share of 37.4% in 2025 and is expected to grow at the fastest CAGR over the forecast period.

The global polyolefin market is expected to grow at a CAGR of 6.0% from 2026 to 2033, reaching USD 432.4 billion by 2033.

Film & sheet segment dominated the polyolefin market with a share of 25.6% in 2025. Polyolefin is diversely applied in food packaging, blown film bags, industrial thermoforming, and more.

About the Author(s)

Plastics, Polymers & Resins Research Team

Bulk Chemicals · Plastics, Polymers & ResinsThis report was authored by the plastics, polymers & resins research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the plastics, polymers & resins segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.