- Home

- »

- Automotive & Transportation

- »

-

Rolling Stock Market Size, Share, Industry Report, 2033GVR Report cover

![Rolling Stock Market Size, Share & Trends Report]()

Rolling Stock Market (2026 - 2033) Size, Share & Trends Analysis Report By Product (Locomotives, Rapid Transit Vehicle, Wagons), By Type (Diesel, Electric), By Train (Rail Freight, Passenger Rail), By Region (North America, Europe, APAC, MEA), And Segment Forecasts

Market Size, 2025

$70.6BMarket Estimate, 2026

$74.5BMarket Forecast, 2033

$123.0BCAGR, 2026–2033

7.4%Rolling Stock Market Summary

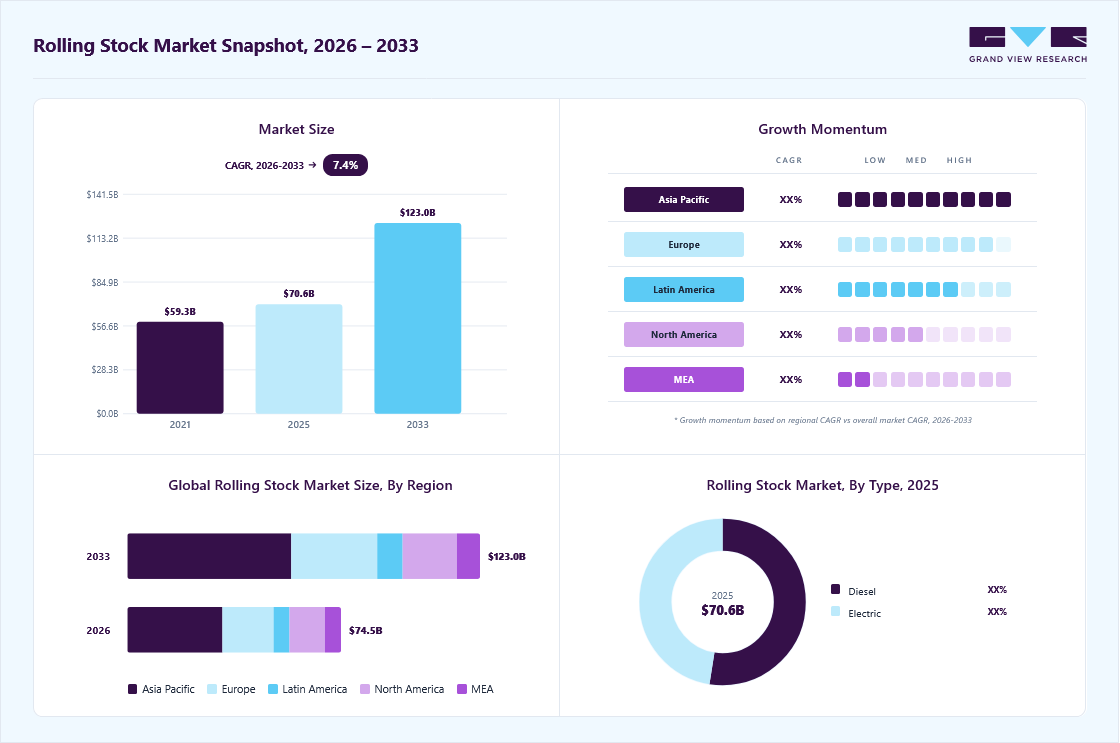

The global rolling stock market size was valued at USD 70.6 billion in 2025 and is projected to grow from USD 74.5 billion in 2026 to USD 123.0 billion by 2033, at a CAGR of 7.4% from 2026 to 2033. The market in Asia Pacific dominated with a revenue share of 44.3% in 2025. Increasing investment in rail infrastructure plays a significant role in driving the growth of the market.

Key Market Trends & Insights

- By product, the wagons segment accounted for the largest share of 40.5% in 2025.

- By type, the diesel segment held the largest market share in 2025.

- By train, the rail freight segment dominated the market in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (44.3% revenue share, 2025)

- By country: The China held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 70.6 Billion

- Estimated market size in 2026: USD 74.5 Billion

- Projected market size by 2033: USD 123.0 Billion

- CAGR (2026-2033): 7.4%

Governments and private-sector entities worldwide are allocating substantial funds to modernize and expand railway networks, thereby improving connectivity, efficiency, and safety. These investments include the construction of new railway lines, electrification of existing tracks, station upgrades, and the adoption of advanced signaling systems. As rail networks expand, the demand for rolling stock increases to support growing passenger and freight transportation needs.Electrification projects are particularly boosting the demand for electric rolling stock, as many countries aim to reduce carbon emissions and dependence on fossil fuels. Countries in Europe, the Asia Pacific, and North America are investing in sustainable rail transport. For instance, the Indian Railways invested over USD 22 billion in the fiscal year 2025 to modernize infrastructure and improve safety for passengers. These investments are part of a larger plan to introduce new train routes and expand electrification, aiming to achieve net-zero carbon emissions by the end of this decade. The investment includes USD 4.7 billion for new trains to ensure reliable operations, addressing passenger concerns about delays and overcrowding.

")

In addition, advancements in technology have significantly enhanced the design and production of energy-efficient rolling stock. Modern electric locomotives, for instance, incorporate regenerative braking systems that capture energy during braking and store it for later use, thereby reducing overall energy consumption and operating costs. Emerging technologies such as computer vision and artificial intelligence are also improving rail safety by enabling real-time obstacle detection, performance monitoring, and collision prevention. Systems like Positive Train Control (PTC), which integrate GPS, wireless communication, and onboard computing, can automatically regulate train speed and prevent accidents.

The high initial investment and maintenance costs associated with rolling stock restrain the growth of the market. Purchasing new trains, passenger coaches, freight wagons, or metro units requires substantial capital expenditure, which can be a major financial burden for railway operators, particularly in developing regions with limited funding. Advanced rolling stock equipped with modern technologies, such as energy-efficient propulsion systems, automation, real-time monitoring, and predictive maintenance features, comes at a high cost, making large-scale fleet modernization or expansion challenging. For instance, a diesel locomotive typically ranges in price from USD 500,000 to 2 million, whereas an electric locomotive can cost more than USD 6 million. The cost varies based on factors such as whether it uses AC or DC traction, its horsepower, and the type of electronics it includes.

Product Insights

The wagons segment accounted for the largest share of 40.5% in 2025. Car carrier wagons, flat wagons, hopper wagons, and tank wagons, among others are the most preferred wagon types for transporting goods. Companies such as CRRC Corporation Limited, Porterbrook, and GB Rail freight are investing considerable funds into making wagons. Modern wagons have a speed limit of up to 75 mph (121 km/h) in some countries and are equipped with GPS receivers and transponders, which help in monitoring location.

The rapid transit vehicle segment is expected to grow at the fastest CAGR during the forecast period. A rapid transit vehicle is a form of urban public transportation with a high capacity. The rapid transit vehicle segment is emerging significantly in the market as most passengers prefer rapid transit vehicles owing to their high-speed and enhanced comfortability features. These vehicles are competing with airlines, long-distance bus services, and other transportation services in terms of speed and improved infrastructure. In addition, the increasing demand for automated trains and magnetic levitation trains among end users for transportation is expected to drive the growth of the segment.

Type Insights

The diesel segment held the largest market share in 2025. Expansion of rail networks in non-electrified regions is driving the growth of the diesel segment in the market. Many countries, particularly in developing regions, continue to expand their rail infrastructure in areas where electrification remains limited due to high costs and long implementation timelines. Diesel locomotives provide a practical and flexible solution for these routes, enabling seamless operations without dependence on overhead power systems. Their ability to operate efficiently across remote and rural areas enhances connectivity and supports economic development, thereby sustaining strong demand for diesel rolling stock.

The electric segment is expected to grow at the fastest CAGR during the forecast period. Rising demand for energy-efficient, low-operating-cost transportation is driving the expansion of the electric segment. Electric rolling stock offers higher energy efficiency, lower fuel costs, and reduced maintenance requirements compared to diesel counterparts. Improved operational efficiency and long-term cost savings are encouraging rail operators to adopt electric trains, particularly for high-frequency passenger routes and urban transit systems. These economic advantages are strengthening the business case for electrification and boosting segment growth.

Train Insights

The rail freight segment dominated the market in 2025. The segment is witnessing steady growth as logistics and supply chain operators increasingly rely on rail transport for long-distance and bulk cargo movement. Investments in modern freight wagons, intermodal facilities, and high-capacity locomotives are driving efficiency and operational flexibility. The adoption of low-emission and fuel-efficient locomotives, including hybrid and electric models, is also supporting sustainability initiatives. Expanding cross-border rail corridors and intermodal hubs in Europe, Asia, and North America are further boosting demand.

The passenger rail segment is projected to grow at the fastest CAGR of 9.2% over the forecast period. The passenger rail segment is experiencing robust expansion driven by urbanization, rising commuter demand, and government initiatives to reduce road congestion. High-speed rail networks, regional trains, and suburban transit systems are being modernized to improve capacity, speed, and passenger comfort. Electrification of lines and the introduction of battery-electric or dual-mode trains are reducing carbon footprints and operational costs. Investments in smart ticketing, real-time passenger information systems, and advanced onboard amenities are enhancing the travel experience.

Regional Insights

The North America rolling stock industry held a significant share in 2025. The market in the region is expected to witness significant growth over the forecast period, supported by increasing investments in high-speed rail, fleet modernization, and energy-efficient train technologies. The region hosts several established players actively advancing the development and deployment of trams and high-speed trains. For instance, in August 2025, Alstom launched Amtrak’s NextGen Acela trains on the U.S. Northeast Corridor, capable of 160 mph.

U.S. Rolling Stock Market Trends

The U.S. rolling stock industry held a dominant position in 2025. The increasing focus on decarbonization and adoption of alternative, low-emission propulsion technologies is driving demand for modern rolling stock in the U.S. Rail operators are actively investing in cleaner fuel solutions and energy-efficient technologies to reduce carbon emissions and meet environmental targets, thereby accelerating the modernization and expansion of rolling stock fleets.

Europe Rolling Stock Market Trends

The Europe rolling stock industry was identified as a lucrative region in 2025. Cities and national operators in the region are increasingly investing in higher-capacity, energy-efficient, and technologically advanced trains to meet growing transportation demands while reducing environmental impact.

The UK rolling stock industry is expected to grow rapidly in the coming years. Operators in the country are increasingly adopting advanced technologies to improve operational efficiency, enhance passenger experience, and support sustainable transport. Innovation in rolling stock design and testing is a major growth driver. In April 2023, Hitachi Rail partnered with the Global Centre of Rail Excellence (GCRE) in Wales to test British-built trains, battery technology, and digital rail solutions. This collaboration supports energy-efficient operations, predictive maintenance, and advanced signaling.

The Germany rolling stock industry held a substantial market share in 2025. The market in the country is advancing steadily, driven by fleet modernization, sustainable transport initiatives, and high-speed rail expansion. Investments are increasingly focused on energy-efficient rolling stock, improved passenger capacity, and infrastructure that supports faster, more reliable rail connections.

Asia Pacific Rolling Stock Market Trends

Asia Pacific rolling stock industry accounted for a 44.3% share of the overall market in 2025. The Asia Pacific rolling stock industry is anticipated to grow at a CAGR of 8.1% during the forecast period. The Asia Pacific rolling stock industry is poised for strong growth, driven by investments from emerging economies such as China, India, and Japan to modernize transportation services. Governments are increasingly adopting trams, electric locomotives, and large-scale infrastructure upgrades to meet rising demand and optimize existing railway networks.

The India rolling stock industry is expected to grow rapidly in the coming years, fueled by rising urbanization, increasing government initiatives including “Make in India,” and the demand for electrified, high-speed, and energy-efficient trains. Expanding production capacity and modern manufacturing facilities are supporting the country’s growing need for high-performance rolling stock. For instance, in July 2025, Titagarh Rail Systems Ltd signed a 99-year lease for a 40-acre land parcel in West Bengal, valued at ~USD 15.35 million (INR 126.63 crore), to accelerate production of rolling stock, including Vande Bharat sleeper trains, ensuring operators can meet rising rail transport demand efficiently.

The China rolling stock industry held a substantial market share in 2025. Rising industrial output, growing freight volumes, and the push for energy-efficient, high-capacity rail transport are driving the China market. Investments in technologically advanced locomotives are enabling operators to meet increasing cargo demand while improving operational reliability and sustainability.

Key Rolling Stock Company Insights

Some of the key companies in the rolling stock industry include Alstom SA, CRRC Corporation Limited, Hitachi, Ltd., Hyundai Rotem, and others. Organizations are focusing on increasing their customer base to gain a competitive edge in the industry. Therefore, key players are taking several strategic initiatives, such as mergers and acquisitions, and partnerships with other major companies.

-

Alstom SA operates across multiple transport sectors, offering integrated rail mobility systems. In the rolling stock domain, it designs and manufactures passenger trains including high-speed, regional, metro, and tram systems. The company develops complete train solutions under product lines such as Coradia and Avelia, integrating traction, control systems, and digital signaling into its rolling stock portfolio. Alstom SA also undertakes train refurbishment, maintenance, and energy-efficient technology projects across various rail networks.

-

CRRC Corporation Limited manufactures a full range of railway vehicles for passenger and freight transport. Its rolling stock production covers high-speed EMUs, locomotives, metro cars, trams, and freight wagons. The company operates large-scale production bases and research centers that support advancements in lightweight materials, high-efficiency traction, and intelligent rail systems. CRRC supplies rolling stock for both domestic and international markets, contributing to high-speed and urban rail infrastructure development in multiple regions.

Key Rolling Stock Companies:

The following key companies have been profiled for this study on the rolling stock market.

- Alstom SA

- CRRC Corporation Limited

- Hitachi, Ltd.

- Hyundai Rotem

- Kawasaki Heavy Industries, Ltd.

- Siemens AG

- Stadler, Inc.

- The Greenbrier Co.

- Trinity Industries, Inc.

- CAF (Construcciones y Auxiliar de Ferrocarriles) S.A.

Recent Developments

-

In December 2025, VinSpeed High-Speed Railway Investment and Development JSC (part of Vingroup) and Siemens Mobility GmbH (a subsidiary of Siemens AG, Germany) signed a comprehensive strategic cooperation and technology transfer agreement. The partnership focused on high-speed rail development in Vietnam, enabling technology transfer, localization, and the creation of a modern, international-standard rail infrastructure.

-

In December 2024, CRRC unveiled the CR450 high-speed electric multiple unit (EMU) prototype, designed to operate at speeds exceeding 400 km/h. The train integrates advanced aerodynamic design, lightweight materials, and energy-efficient traction systems, marking a significant leap in China’s high-speed rail technology.

Rolling Stock Market Report Scope

Report Attribute

Details

Market size in 2025

USD 70.6 billion

Estimated market size in 2026

USD 74.5 billion

Projected market size by 2033

USD 123.0 billion

Growth rate

CAGR of 7.4% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product, type, train, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; Japan; India; South Korea; Australia; Brazil; KSA; UAE; South Africa

Key companies profiled

Alstom SA; CRRC Corporation Limited; Hitachi, Ltd.; Hyundai Rotem; Kawasaki Heavy Industries, Ltd.; Siemens AG; Stadler, Inc.; The Greenbrier Co.; Trinity Industries, Inc.; CAF (Construcciones y Auxiliar de Ferrocarriles) S.A.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Rolling Stock Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global rolling stock market report based on product, type, train, and region:

-

Product Outlook (Revenue, USD Million, 2021 - 2033)

-

Locomotive

-

Rapid Transit Vehicle

-

Wagon

-

-

Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Diesel

-

Electric

-

-

Train Outlook (Revenue, USD Million, 2021 - 2033)

-

Rail Freight

-

Passenger Rail

-

-

Regional Outlook (Revenue, USD Million, 2021- 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

Australia

-

South Korea

-

-

Latin America

-

Brazil

-

-

Middle East & Africa (MEA)

-

UAE

-

KSA

-

South Africa

-

-

Frequently Asked Questions About This Report

The global rolling stock market size was estimated at USD 70.6 billion in 2025 and is expected to reach USD 74.5 billion in 2026.

The global rolling stock market is expected to witness a compound annual growth rate of 7.4% from 2026 to 2033 to reach USD 123.0 billion by 2033.

The key factors driving the growth of the rolling stock market include the growing concertation of the population in urban areas and the increasing demand for rail vehicles such as trams, local trains, passenger rails, and so on. Moreover, the rising preference for high-speed trains over conventional trains owing to faster transportation and comfortability is likely to further boost the market growth over the forecast period.

Asia Pacific region held the largest share of 44.3% in 2025.

Key players include Alstom SA; CRRC Corporation Limited; Hitachi, Ltd.; Hyundai Rotem; Kawasaki Heavy Industries, Ltd.; Siemens AG; Stadler, Inc.; The Greenbrier Co.; Trinity Industries, Inc.; CAF (Construcciones y Auxiliar de Ferrocarriles) S.A.

The wagons segment led with a 40.5% revenue share in 2025, while rapid transit vehicle is the fastest-growing segment.

The diesel held the largest revenue share in 2025, while electric segment is the fastest-growing market.

The rail freight held the largest share in 2025 and passenger rail is the fastest-growing market.

About the Author(s)

Automotive & Transportation Research Team

Technology · Automotive & TransportationThis report was authored by the automotive & transportation research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the automotive & transportation segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.