- Home

- »

- Network Security

- »

-

Security Information & Event Management Market Report, 2026-2033GVR Report cover

![Security Information And Event Management Market (2026 - 2033)Report]()

Security Information And Event Management Market (2026 - 2033)

Size, Share & Trends Analysis By Solution (Software, Service), Deployment (Cloud, On-premise), By Enterprise Size, By End-use (BFSI, IT & Telecom, Retail & E-commerce), By Region, And Segment Forecasts

Market Size, 2025

$5.8BMarket Estimate, 2026

$6.7BMarket Forecast, 2033

$18.2BCAGR, 2026–2033

15.5%Security Information And Event Management Market Summary

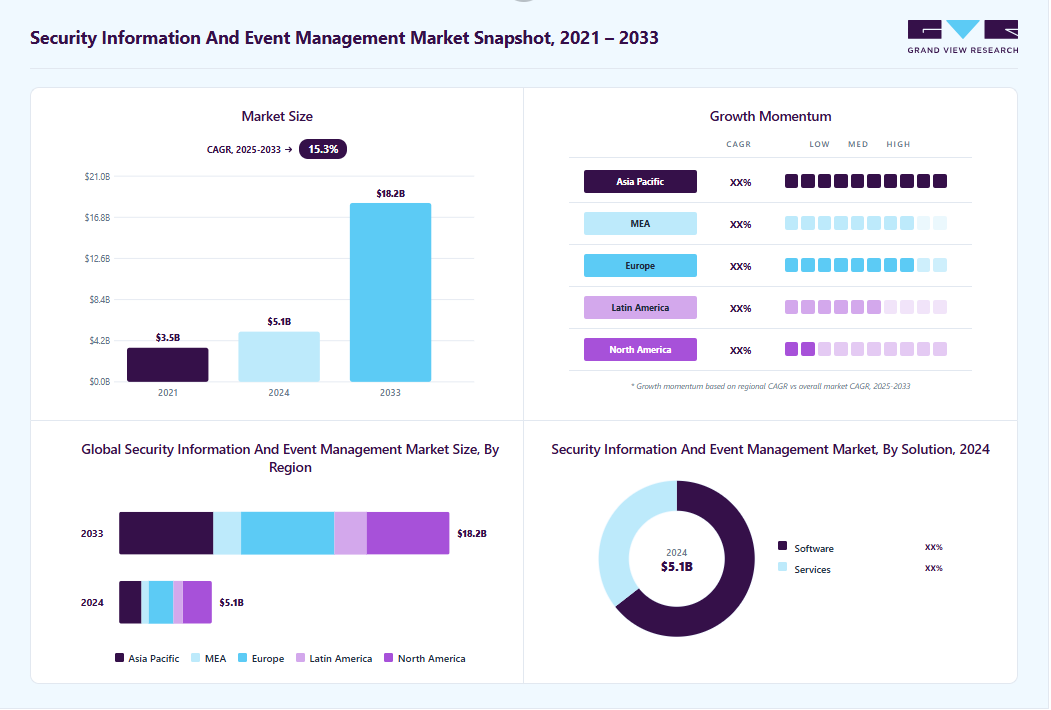

The global security information and event management market size was valued at USD 5.8 billion in 2025 and is projected to grow from USD 6.7 billion in 2026 to USD 18.2 billion in 2033, at a CAGR of 15.5% from 2026 to 2033. The market in North America dominated with a revenue share of 30.6% in 2025. The increasing frequency of ransomware, advanced persistent threats (APTs), phishing attacks, and insider threats is accelerating demand for SIEM platforms that provide real-time threat detection, security analytics, and rapid incident response across North America. As organizations face advanced threats such as ransomware, phishing, and insider attacks, the need for real-time monitoring, threat detection, and rapid incident response becomes critical.

Key Market Trends & Insights

- By solution: Software segment dominated the market, with a revenue share of 64.2% in 2025.

- By deployment: Cloud segment held the largest market share of 57.0% in 2025.

- By enterprise size: Large enterprises segment held the largest revenue share in 2025.

- By End-use: IT and Telecom segment held the largest revenue share in 2025.

Regional Highlights

- Largest regional market: North America (30.6% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 5.8 Billion

- Estimated market size in 2026: USD 6.7 Billion

- Projected market size by 2033: USD 18.2 Billion

- CAGR (2026-2033): 15.5%

SIEM solutions consolidate and analyze vast volumes of security data from networks, endpoints, and applications, enabling enterprises to identify vulnerabilities, detect anomalies, and comply with stringent regulatory requirements. The growing emphasis on cybersecurity resilience, especially with remote work and cloud adoption, has accelerated the adoption of SIEM platforms, making them an essential tool for protecting sensitive data and maintaining operational continuity.With the rise of stringent data protection and privacy regulations such as GDPR, HIPAA, and CCPA, organizations are under increasing pressure to monitor, log, and report security events. SIEM solutions help businesses maintain compliance by providing audit trails, automated reporting, and continuous monitoring capabilities. As regulatory frameworks become more complex and enforcement stricter, organizations are increasingly investing in SIEM tools to avoid penalties and safeguard their reputation.

")

In addition, trends like proactive threat hunting capabilities and low-code/no-code analytics empower security teams to analyze historical data, build custom alerts and dashboards, and anticipate threats without extensive technical expertise, ensuring that SIEM platforms remain agile and adaptive in dynamic cybersecurity landscapes. For instance, in May 2025, Exabeam partnered with Vectra AI to combine their strengths in security analytics and AI-driven threat detection. This collaboration enables faster identification of potential threats across networks and cloud environments. By automating routine security operations, it reduces manual workloads for analysts and strengthens overall cloud security posture.

Market Dynamics

Security Information and Event Management (SIEM) solutions are gaining significant traction as organizations face increasingly sophisticated cyber threats and growing complexity across hybrid IT environments. SIEM platforms provide advanced capabilities such as real-time threat detection, security event correlation, log management, compliance monitoring, incident investigation, user and entity behavior analytics (UEBA), threat intelligence integration, and automated response orchestration. These solutions enable security teams to improve visibility across networks, endpoints, cloud workloads, applications, and connected devices through centralized monitoring and actionable security insights. The growing need to strengthen cybersecurity posture, meet regulatory compliance requirements, reduce incident response times, and address the rising volume of cyberattacks, coupled with the increasing adoption of cloud computing, remote work environments, and AI-driven security operations, is expected to continue driving growth in the Security Information and Event Management (SIEM) market.

The increasing frequency and sophistication of cyberattacks are major drivers of the security information and event management (SIEM) market, as organizations seek advanced solutions to detect, investigate, and respond to evolving security threats. Modern cyberattacks, including ransomware, advanced persistent threats (APTs), phishing campaigns, insider threats, and supply chain attacks, often bypass traditional security controls and require continuous monitoring across diverse IT environments. SIEM platforms aggregate and correlate security data from multiple sources, enabling security teams to identify suspicious activities in real time and respond more effectively. As cyber risks continue to escalate across enterprises, governments, and critical infrastructure sectors, demand for SIEM solutions is increasing significantly.

The complexity of SIEM deployment and the shortage of skilled cybersecurity professionals represent significant restraints on the SIEM market. Effective SIEM implementation requires extensive integration with existing security tools, network infrastructure, cloud environments, and business applications. Organizations must also continuously fine-tune detection rules, manage large volumes of security events, and investigate alerts to maximize platform effectiveness. However, many enterprises face a shortage of qualified security analysts and SOC personnel capable of managing these sophisticated systems. The lack of in-house expertise can result in prolonged deployment timelines, increased operational costs, and suboptimal utilization of SIEM capabilities, limiting broader market adoption.

The growing adoption of cloud-native and managed SIEM services presents a significant opportunity for the SIEM market, as organizations increasingly seek scalable, cost-effective, and easy-to-manage security monitoring solutions. Cloud-based SIEM platforms eliminate the need for substantial on-premises infrastructure investments while providing centralized visibility across hybrid and multi-cloud environments. Additionally, managed SIEM and SOC-as-a-Service offerings allow organizations to outsource threat monitoring, incident response, and compliance management to specialized security providers. These services are particularly attractive to small and medium-sized enterprises that lack dedicated cybersecurity resources. As cloud adoption accelerates and cybersecurity talent shortages persist, demand for cloud-native and managed SIEM solutions is expected to expand considerably.

Analyst Perspective

The security information and event management (SIEM) market sits at a compelling intersection of long-term cybersecurity and digital transformation trends that few security technology segments can match, including the rising frequency and sophistication of cyberattacks, expanding regulatory compliance requirements, accelerating cloud adoption, and growing demand for real-time security visibility across increasingly complex IT environments. Vendors that can leverage AI-driven analytics and automation to reduce alert fatigue, accelerate incident response, and improve security outcomes will be best positioned to deliver measurable reductions in cyber risk, operational costs, and compliance burdens across the enterprise security ecosystem.

Solution Insights

Based on solution, the software segment led the market with the largest revenue share of 64.2% in 2025 and is expected to grow at the significant CAGR over the forecast period. Stand-alone SIEM platforms are increasingly being integrated with or replaced by solutions that offer broader capabilities, most notably Security Orchestration, Automation, and Response (SOAR). The demand for SIEM software that natively includes or seamlessly integrates with SOAR modules is growing because it directly addresses the cybersecurity skills gap.

The services segment is anticipated to grow at the highest CAGR during the forecast period. The growing volume of alerts and the critical need for 24/7 monitoring are driving the expansion of Managed Security Services (MSS) and Managed Detection and Response (MDR) offerings that are built around SIEM technology. Many organizations, particularly mid-sized businesses, find it prohibitively expensive and challenging to recruit and retain a full team of skilled security analysts to operate their SIEM around the clock.

Deployment Insights

Based on deployment, the cloud segment led the market with the largest revenue share of 57.0% in 2025. As enterprises accelerate digital transformation, the adoption of cloud and hybrid infrastructures has become the norm, bringing with it complex, distributed environments that generate vast amounts of telemetry. Traditional on-premises SIEM solutions often lack the flexibility and scalability to process and analyze these dynamic data flows effectively, creating visibility gaps.

The on-premise segment is expected to grow at a significant CAGR during the forecast period. Stringent data sovereignty and regulatory compliance are significant drivers for on-premise SIEM solutions. Industries such as government, defense, finance, and healthcare operate under extreme regulatory pressures, often mandating that sensitive data never leaves the organization's physical control. Regulations may explicitly prohibit storing certain types of classified, personally identifiable information (PII), or financial data on third-party servers, especially those located in different countries.

Enterprise Size Insights

Based on enterprise size, the large enterprises segment led the market with the largest revenue share of 52.2% in 2025. Large enterprises operate extensive IT infrastructures, spanning multiple on-premises data centers, hybrid environments, and multi-cloud deployments. The complexity of these environments generates massive volumes of security data from servers, endpoints, applications, network devices, and cloud services. SIEM platforms help centralize and correlate this data, providing real-time visibility and advanced threat detection across the enterprise. The need to manage diverse, distributed systems efficiently drives large-scale SIEM adoption

The SMEs segment is expected to grow at a significant CAGR during the forecast period. Vendors are offering cloud-based and subscription-based SIEM solutions tailored for SMEs, which are cost-effective and easy to scale according to business needs. Unlike traditional enterprise SIEM deployments, these solutions reduce upfront investment and IT complexity, making advanced security accessible to smaller organizations.

End-use Insights

Based on end-use, the IT & Telecom segment led the market with the largest revenue share of 20.9% in 2025. The IT and telecom sector operates extensive networks, data centers, cloud services, and edge computing environments that generate enormous volumes of security-relevant data. The increasing complexity of these infrastructures, combined with high-speed data transmission and connectivity demands, necessitates advanced monitoring and threat detection. SIEM platforms help consolidate logs, monitor traffic anomalies, and correlate events in real time, enabling IT and telecom companies to maintain network reliability and service continuity.

The government & defense segment is expected to grow at a significant CAGR over the forecast period.Cyber threats targeting government and defense sectors are becoming increasingly sophisticated, including Advanced Persistent Threats (APTs), insider attacks, and supply chain compromises. SIEM solutions integrated with AI/ML-based analytics, threat intelligence feeds, and UEBA (User and Entity Behavior Analytics) enable proactive threat detection and faster response, helping organizations mitigate risks before critical damage occurs.

Regional Insights

North America dominated the global security information and event management market with the largest revenue share of 30.6% in 2025, driven by the high adoption of advanced cybersecurity frameworks by enterprises. Organizations in the region are increasingly deploying AI-enabled and automated threat detection tools within SIEM platforms to protect critical infrastructure, financial systems, and sensitive data from sophisticated cyberattacks, fostering strong market growth.

U.S. Security Information and Event Management Market Trends

The security information and event management market in the U.S. held the largest share in the North America region in 2025. Stringent regulatory and compliance mandates such as HIPAA, GDPR for US-EU operations, and the CCPA are compelling organizations to adopt SIEM solutions for real-time monitoring, logging, and reporting of security incidents. The need to avoid regulatory penalties and safeguard customer trust fuels adoption among enterprises and SMEs alike.

Europe Security Information And Event Management Market Trends

The security information and event management (SIEM) market in Europe is anticipated to register considerable growth from 2025 to 2033, driven by rising government and enterprise investments in cybersecurity infrastructure. Countries across the EU are increasingly funding initiatives for digital resilience, critical infrastructure protection, and cross-border threat intelligence sharing, encouraging organizations to implement comprehensive SIEM platforms.

The UK security information and event management (SIEM) market is expected to grow rapidly in the coming years, owing to the increasing frequency of ransomware and phishing attacks targeting businesses of all sizes. The need for centralized threat monitoring, rapid incident response, and proactive vulnerability management pushes organizations to adopt SIEM solutions extensively

The Germany security information and event management (SIEM) market held a substantial market share in 2024 due tothe industry 4.0 adoption in manufacturing and critical infrastructure sectors, which requires robust security monitoring of OT (Operational Technology) and IT systems. SIEM solutions help organizations detect anomalies, prevent industrial cyberattacks, and ensure continuity of operations.

Asia Pacific Security Information And Event Management MarketTrends

Asia Pacific security information and event management (SIEM) held a significant share in the global market in 2024, due to rapid digital transformation and cloud adoption among enterprises. Organizations are increasingly moving operations to hybrid IT and cloud platforms, creating a demand for centralized security monitoring, threat detection, and compliance management provided by SIEM solutions.

The Japan security information and event management (SIEM) market is expected to grow rapidly in the coming years. Cybersecurity initiatives by the government and focus on protecting critical industries like automotive, electronics, and finance drive SIEM adoption. The emphasis on real-time threat intelligence and incident response to mitigate sophisticated attacks supports robust market growth.

The China security information and event management (SIEM) market held a substantial market share in 2024, due to the rise of large-scale digital ecosystems and smart city projects, which increase the number of connected devices and the potential attack surface. SIEM platforms are increasingly used to monitor networks, detect threats, and ensure regulatory compliance in this rapidly digitizing environment.

Key Security Information and Event Management Company Insights

Key players operating in the security information and event management (SIEM) industry are Splunk LLC, IBM Corporation, Exabeam, Securonix, and Sumo Logic. The companies are focusing on various strategic initiatives, including new product development, partnerships & collaborations, and agreements to gain a competitive advantage over their rivals. The following are some instances of such initiatives.

-

In August 2025, LevelBlue has finalized its acquisition of U.S.-based cybersecurity managed detection and response (MDR) provider Trustwave. The merger combines LevelBlue’s strengths in network security, strategic risk management, and threat intelligence with Trustwave’s MDR services, Fusion Security Operations Platform, offensive security offerings, and SpiderLabs threat intelligence team. The unified company aims to streamline operations, enhance response capabilities, optimize advanced cyber technologies, and provide integrated protection across cloud, on-premises, and hybrid environments.

-

In July 2025, Rapid7 introduced Incident Command, a next-generation SIEM designed to extend the capabilities of its Command Platform. The new solution integrates attack surface management, threat detection, and response within a unified framework, powered by Agentic AI workflows built on SOC playbooks and continuously refined in real-world use. Using the platform’s data mesh, Incident Command combines Surface Command for attack surface context with Intelligence Hub for curated threat insights, enabling analysts to investigate and respond with greater speed, precision, and efficiency.

-

In May 2025, Exabeam expanded its global partnership with Inspira Enterprise, an India-based cybersecurity, data analytics, and AI services company operating across North America, ASEAN, the Middle East, India, and Africa. Under the renewed collaboration, Inspira will provide the full range of Exabeam solutions both as a managed security services provider (MSSP) and an authorized reseller, strengthening its ability to deliver advanced security offerings to organizations worldwide.

Key Security Information And Event Management Companies:

The following key companies have been profiled for this study on the security information and event management market.

-

Exabeam

-

Fortinet, Inc.

-

Fortra, LLC.

-

IBM Corporation

-

LevelBlue

-

Logpoint

-

ManageEngine

-

Trellix

-

NetWitness LLC.

-

Open Text Corporation

-

Rapid7

-

Securonix

-

SolarWinds Worldwide, LLC Splunk LLC

-

Splunk LLC

-

Sumo Logic

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (Microsoft; IBM; Splunk; Fortinet; LogRhythm)

Mature players focus on comprehensive security operations platforms that combine log management, threat detection, security analytics, compliance monitoring, SOAR, and threat intelligence. They emphasize cloud-native deployments, AI-driven threat detection, and deep integration with broader cybersecurity portfolios. These vendors also leverage extensive partner ecosystems and managed security service provider (MSSP) networks to expand market reach.

Established players benefit from strong brand recognition, large customer bases, and extensive cybersecurity ecosystems. Their platforms offer advanced analytics, scalability, broad third-party integrations, and global support capabilities. Significant R&D investments enable continuous innovation in AI, automation, and security operations. Their ability to support complex enterprise environments strengthens their competitive position.

These companies often face lengthy deployment cycles and high implementation costs. Their platforms can be complex to configure and manage, requiring skilled cybersecurity personnel. Licensing and data-ingestion costs may be challenging for SMEs. Large organizations can also experience vendor lock-in due to extensive integrations across security infrastructure.

Emerging Players (Securonix; Exabeam; Sumo Logic; Devo; Hunters)

Emerging players focus on cloud-native SIEM architectures, AI-powered analytics, behavioral monitoring, and automated threat investigation. Many offer SaaS-based platforms with flexible subscription pricing and rapid deployment models. Their strategies emphasize reducing alert fatigue, improving SOC efficiency, and simplifying security operations through automation and machine learning.

Emerging players provide agile, scalable, and easier-to-deploy solutions compared to traditional SIEM platforms. Their strong focus on cloud environments, AI-driven analytics, and user experience enables faster time-to-value. Flexible pricing models and lower infrastructure requirements make them attractive to mid-sized enterprises and organizations undergoing digital transformation.

Emerging players often have smaller customer bases and lower global market penetration. Limited channel networks and brand recognition can slow enterprise adoption. Their platforms may lack some of the extensive integrations and compliance certifications offered by established vendors. Resource constraints and competitive pressure from larger cybersecurity vendors can also limit expansion opportunities.

Security Information And Event Management Market Report Scope

Report Attribute

Details

Market size in 2025

USD 5.8 billion

Estimated market size in 2026

USD 6.7 billion

Projected market size by 2033

USD 18.2 billion

Growth rate

CAGR of 15.5% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Solution, deployment, enterprise size, end-use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; Japan; India; South Korea; Australia; Brazil; Saudi Arabia; South Africa; UAE

Key companies profiled

Exabeam; Fortinet, Inc.; Fortra, LLC.; IBM Corporation; LevelBlue; Logpoint; ManageEngine; NetWitness LLC.; Open Text Corporation; Rapid7; Securonix; SolarWinds Worldwide, LLC; Splunk LLC; Sumo Logic; Trellix

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Security Information And Event Management Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global security information and event management market report based on solution, deployment, enterprise size, end-use, and region:

-

Solution Outlook (Revenue, USD Billion, 2021 - 2033)

-

Software

-

Services

-

-

Deployment Outlook (Revenue, USD Billion, 2021 - 2033)

-

Cloud

-

On-premise

-

-

Enterprise Size Outlook (Revenue, USD Billion, 2021 - 2033)

-

Small and Medium-Sized Enterprises (SMEs)

-

Large enterprises

-

-

End-use Outlook (Revenue, USD Billion, 2021 - 2033)

-

BFSI

-

IT and Telecom

-

Retail & E-commerce

-

Healthcare and Life Sciences

-

Manufacturing

-

Government & Defense

-

Energy & Utilities

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Research Methodology

Segment Definition

Segment - Solution

Revenue capture definition

Software

SIEM software refers to platforms that collect, aggregate, correlate, analyze, and store security event and log data generated from networks, endpoints, servers, applications, cloud environments, and security tools. These solutions provide capabilities such as threat detection, incident investigation, security monitoring, compliance reporting, user behavior analytics, and security orchestration.

Services

SIEM services include professional and managed services that support the deployment, integration, customization, monitoring, optimization, and maintenance of SIEM platforms.

Segment - Deployment

Revenue capture definition

Cloud

Cloud-based SIEM solutions are delivered through public, private, or hybrid cloud environments and provide scalable security monitoring without requiring extensive on-premises infrastructure. These solutions enable centralized visibility, faster deployment, remote accessibility, and simplified management across distributed and multi-cloud environments.

On-Premise

On-premise SIEM solutions are deployed within an organization's own data center or IT infrastructure. They offer greater control over security data, configurations, and compliance requirements, making them suitable for organizations with strict regulatory, privacy, or data sovereignty obligations.

Segment - Enterprise Size

Revenue capture definition

Small and Medium-Sized Enterprises (SMEs)

The SMEs segment, with respect to the number of employees, generally includes organizations employing between 10 and 999 employees.

Large Enterprises

The Large enterprises segment, with respect to the number of employees, typically comprises organizations employing more than 1,000 employees for multinational corporations.

Segment - End-use

Revenue capture definition

BFSI

Includes banks, financial institutions, insurance companies, investment firms, payment processors, and fintech organizations that use SIEM solutions to detect fraud, protect sensitive financial data, and comply with industry regulations.

IT and Telecom

Comprises IT service providers, cloud service providers, software companies, internet firms, data center operators, and telecommunications companies that utilize SIEM platforms to monitor large-scale digital infrastructure and protect customer and operational data.

Retail & E-commerce

Includes brick-and-mortar retailers, online marketplaces, e-commerce platforms, and payment service providers that deploy SIEM solutions to safeguard customer information, secure payment transactions, and monitor cybersecurity threats.

Healthcare and Life Sciences

Encompasses hospitals, clinics, healthcare networks, pharmaceutical companies, biotechnology firms, medical device manufacturers, and research organizations that use SIEM solutions to protect patient records, intellectual property, and critical healthcare systems.

Manufacturing

Includes discrete and process manufacturers across sectors such as automotive, electronics, chemicals, aerospace, industrial equipment, and consumer goods. SIEM solutions help secure operational technology (OT), industrial control systems (ICS), and connected manufacturing environments.

Government & Defense

Comprises federal, state, and local government agencies, military organizations, intelligence agencies, law enforcement departments, and public sector institutions that deploy SIEM platforms to protect national security assets, critical infrastructure, and sensitive government information.

Energy & Utilities

Includes electricity providers, oil and gas companies, renewable energy operators, water utilities, nuclear facilities, and power grid operators that utilize SIEM solutions to monitor and secure critical infrastructure and industrial control environments

Others

This category includes education institutions, transportation and logistics companies, media and entertainment organizations, hospitality providers, real estate firms, professional services organizations.

Estimation Model

Layer

Question

Analysis

Security Operations Addressable Layer

Who can benefit from SIEM solutions?

Identify organizations with significant digital assets, regulated data, and cybersecurity exposure across industries such as BFSI, healthcare, government, telecom, retail, manufacturing, and energy. This layer estimates the total potential user base by assessing enterprises requiring continuous security monitoring, threat detection, compliance management, and incident response capabilities.

Security Infrastructure Readiness Layer

Who can deploy SIEM solutions effectively?

Evaluate organizations based on cybersecurity maturity, IT infrastructure complexity, cloud adoption, security tool integration requirements, SOC readiness, and availability of cybersecurity personnel. This layer determines the operationally and technically reachable market capable of implementing and managing SIEM platforms.

Adoption & Utilization Layer

Who actively uses SIEM platforms?

Analyze SIEM deployment rates, SOC maturity levels, managed security service adoption, compliance-driven security investments, and cybersecurity spending patterns. This layer converts the reachable market into active SIEM users by measuring actual implementation and utilization of security monitoring and analytics capabilities.

Monetization Layer

How much revenue is generated?

Assess revenue potential by analyzing spending on SIEM software licenses, cloud-based SIEM subscriptions, managed SIEM services, threat intelligence integrations, security analytics modules, compliance management tools, and ongoing support services across the active customer base. This layer quantifies the total addressable revenue opportunity within the SIEM ecosystem.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Managed SIEM & SOC-as-a-Service Adoption Assessment

Evaluated enterprise adoption of managed SIEM, MDR, and SOC-as-a-Service offerings, including deployment preferences, outsourcing trends, and service provider ecosystems.

Helps organizations understand outsourcing opportunities, reduce operational complexity, and optimize cybersecurity spending.

Regulatory Compliance & Risk Management Assessment

Evaluated the impact of regulations such as GDPR, HIPAA, PCI-DSS, NIS2, SOX, and regional cybersecurity frameworks on SIEM deployment and security monitoring requirements.

Helps organizations align cybersecurity investments with compliance mandates, reduce audit risks, and strengthen governance frameworks.

Industry-Specific SIEM Adoption Benchmarking

Analyzed SIEM adoption patterns across BFSI and critical infrastructure sectors, focusing on threat landscapes, compliance requirements, and cybersecurity investment priorities

Provides actionable insights into sector-specific growth opportunities, budget allocation trends, and vertical-focused go-to-market strategies.

Frequently Asked Questions About This Report

The global security information and event management market size was estimated at USD 5.8 billion in 2025 and is expected to reach USD 6.7 billion in 2026.

Key factors driving the security information and event management market growth include the increasing sophistication and frequency of cyberattacks across industries. As organizations face advanced threats such as ransomware, phishing, and insider attacks, the need for real-time monitoring, threat detection, and rapid incident response becomes critical.

The software segment led with a 64.2% revenue share in 2025, while services segment is the fastest-growing segment.

The cloud segment led with a 57.0% revenue share in 2025, and is the fastest-growing segment during the forecast period.

The large enterprises segment led with a 52.2% revenue share in 2025, while small & medium enterprises (SMEs) segment is the fastest-growing segment.

Some key players operating in the security information and event management (SIEM) market include Exabeam, Fortinet, Inc., Fortra, LLC., IBM Corporation, LevelBlue, Logpoint, ManageEngine, Trellix, NetWitness LLC., Open Text Corporation, Rapid7, Securonix, SolarWinds Worldwide, LLC, Splunk LLC, Sumo Logic

The global security information and event management market is expected to grow at a compound annual growth rate of 15.5% from 2026 to 2033 to reach USD 18.2 billion by 2033.

North America dominated with 30.6% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

About the Author(s)

Network Security Research Team

Technology · Network SecurityThis report was authored by the network security research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the network security segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.