- Home

- »

- Plastics, Polymers & Resins

- »

-

Silica Market Size, Share, Growth Analysis Report 2026-2033GVR Report cover

![Silica Market (2026 - 2033)Report]()

Silica Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product (Amorphous, Crystalline), By End-use (Building & Construction, Glass Manufacturing, Oil & Gas, Water Treatment), By Region, And Segment Forecasts

Market Size, 2025

$42.9BMarket Estimate, 2026

$45.8BMarket Forecast, 2033

$85.9BCAGR, 2026–2033

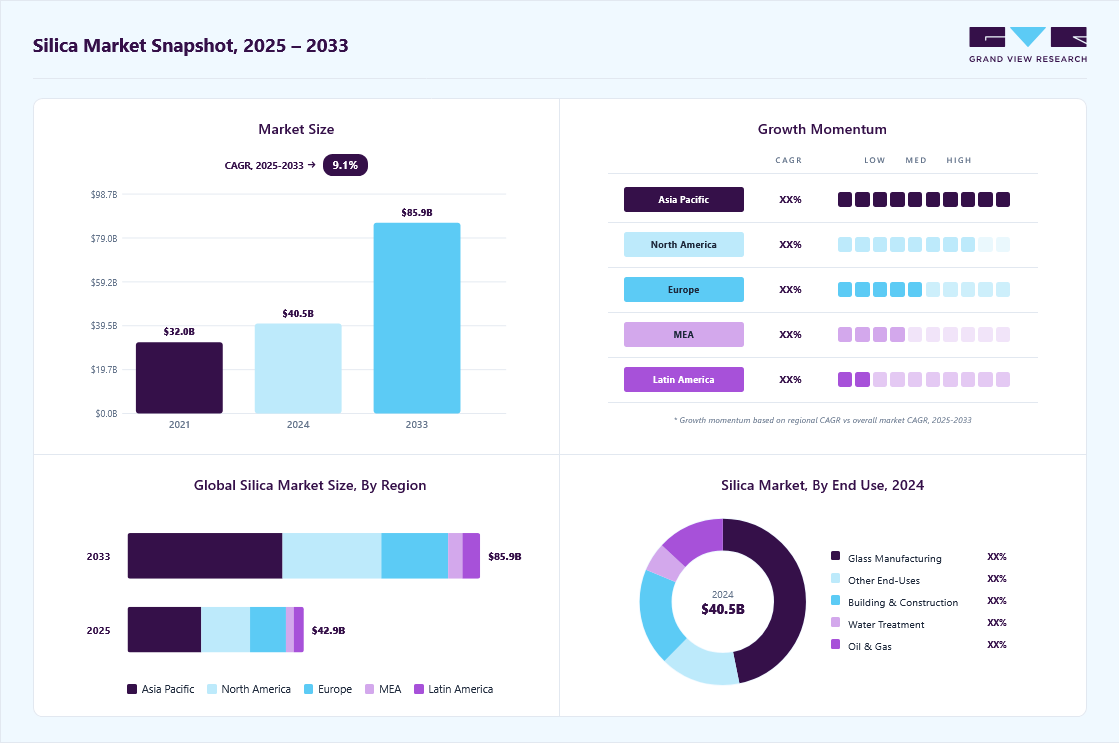

9.4%Silica Market Summary

The silica market size was valued at USD 42.9 billion in 2025 and is projected to grow from USD 45.8 billion in 2026 to USD 85.9 billion by 2033, at a CAGR of 9.4% from 2026 to 2033. The market in Asia Pacific dominated with a revenue share of 41.8% in 2025. Encompasses various forms of silica, including precipitated, fumed, gels, sols, and fumes.

Key Market Trends & Insights

- By Poduct: Crystalline segment dominated the market with a revenue share of 71.8% in 2025.

- By end use: Glass manufacturing led the market with the revenue share of 46.8% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (41.8% revenue share, 2025)

- By country: China held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 42.9 Billion

- Estimated market size in 2026: USD 45.8 Billion

- Projected market size by 2033: USD 85.9 Billion

- CAGR (2026-2033): 9.4%

The growing demand from the rubber industry serves as a key driver of market expansion. It plays a vital role in enhancing the performance of rubber products by providing superior abrasion resistance, tensile strength, and flex fatigue durability. Its extensive use in tire manufacturing is attributed to its ability to strengthen the bond between rubber and metallic reinforcements, thereby improving tear resistance. Rapid economic development, increased government infrastructure spending, and rising consumer preference for personal vehicles drive the automotive sector's growth and fuel its demand. For instance, Japan's preparations for Expo 2025 in Osaka have significantly accelerated construction activity, including large-scale projects such as the Yaesu redevelopment, which features a 390-meter, 61-story office tower slated for completion between 2023 and 2027.")

Simultaneously, the construction industry has emerged as a significant end-user, particularly in fumes that enhance concrete strength, durability, and longevity. The growing need for high-performance construction materials is a key factor propelling market demand. In Asia Pacific, infrastructure development continues to surge, driving the paints and coatings sector and increasing the use of silica-based products. For example, in 2025, India launched the "Urban Infrastructure Development Plan" with an investment of over USD 11 billion to modernize smart cities and develop affordable housing across major urban centers.

Moreover, Southeast Asian countries are making substantial investments in infrastructure that are expected to contribute significantly to their consumption. For instance, in 2025, Vietnam unveiled a USD 10 billion infrastructure investment strategy focusing on expressways, urban transport systems, and industrial zones. These developments will strengthen demand across construction and allied sectors during the forecast period.

Market Dynamics

The silica market is witnessing steady growth, driven by rising demand from the glass, construction, foundry, electronics, chemicals, automotive, and renewable energy sectors. Rapid urbanization, infrastructure development, increasing glass production, and expanding semiconductor manufacturing are significantly boosting silica consumption globally. Governments across North America, Europe, Asia Pacific, and the Middle East are investing heavily in transportation infrastructure, smart cities, renewable energy projects, and industrial development, creating sustained demand for silica-based products. Additionally, the growing use of specialty silica in tires, coatings, adhesives, personal care products, and advanced electronics is further supporting market expansion.

Increasing investments in infrastructure and construction projects worldwide are a major factor The increasing consumption of silica in glass manufacturing and construction applications is a major factor driving market growth. Silica sand serves as the primary raw material in the production of flat glass, container glass, fiberglass, and specialty glass used in buildings, automobiles, solar panels, and consumer electronics. Rising investments in residential, commercial, and infrastructure projects worldwide are fueling demand for glass products and construction materials, thereby increasing silica consumption.

Furthermore, rapid urbanization and industrialization in Asia Pacific, the Middle East, and Africa are generating significant demand for silica in cement, concrete, flooring, ceramics, and other building materials. The expansion of smart city projects, transportation networks, and industrial facilities continues to support long-term growth in silica demand across both developed and emerging economies.

Occupational health risks related to crystalline silica dust exposure remain a key challenge for the silica market. Prolonged inhalation of respirable crystalline silica can lead to serious health conditions, including silicosis, chronic obstructive pulmonary disease (COPD), and lung cancer. As a result, regulatory authorities across major economies have implemented stringent workplace safety standards governing silica handling, processing, and transportation. Compliance with these regulations often requires additional investments in dust control systems, worker protection measures, monitoring equipment, and environmental management practices, increasing operational costs for manufacturers and end users. These regulatory pressures may restrain market growth, particularly among small and medium-sized enterprises.

The increasing deployment of renewable energy projects and sustainable infrastructure, and the growing adoption of silica in high-tech industries, present significant growth opportunities for market participants. High-purity silica is an essential raw material in semiconductor fabrication, optical fibers, photovoltaic cells, and advanced electronic components. The rapid expansion of artificial intelligence infrastructure, data centers, 5G networks, and consumer electronics manufacturing is increasing demand for high-performance silica products globally. In addition, accelerating investments in solar energy installations are driving demand for silica used in photovoltaic glass and solar panel manufacturing. The increasing focus on clean energy transition, digitalization, and advanced manufacturing technologies is expected to create new revenue streams for silica producers.

Product Insights

The crystalline silica dominated the market with a revenue share of 71.8% in 2025. Crystalline silica, particularly in the form of quartz, holds the largest revenue market share due to its high hardness, thermal stability, and chemical inertness. It offers excellent mechanical strength and is ideal for construction materials like concrete, mortar, and tiles. Its high melting point and weather resistance make it suitable for foundry applications, glassmaking, and ceramics. Its crystalline form also exhibits abrasive properties, enabling its use in industrial abrasives and sandblasting. However, due to its delicate particulate nature, it requires careful handling to mitigate respiratory health risks.

Amorphous silica, typically derived from diatomaceous earth, rice husk ash, and synthetic production, is known for its non-crystalline structure, high surface area, and chemical stability. It is widely used in rubber, paints and coatings, personal care, and food processing due to its reinforcing, thickening, and anti-caking properties. Its high porosity makes it effective in filtration and insulation applications, while its inert and non-toxic nature ensures safe use in pharmaceuticals and cosmetics. Its amorphous form is also critical in agriculture as a soil additive and pest control agent, promoting plant health without harmful residues.

End-use Insights

Based on end use, glass manufacturing led the market with the largest revenue share of 46.8% in 2025, making it the largest end-use sector. It is the primary raw material in glass production due to its high purity, chemical stability, and melting point. It is used extensively in the production of container glass (bottles and jars), flat glass (used in windows and mirrors), fiberglass (for insulation and reinforcement), and specialty glass for electronics, optics, and laboratory equipment. It ensures transparency, strength, and thermal resistance in glass products, making it indispensable to industrial and consumer applications. Growth in the construction, automotive, and packaging sectors continually fuels the demand for glass, thereby supporting the market.

The building & construction industry also holds a significant share in the market, driven by increasing infrastructure development and urbanization across regions. It is used as fumes and sand to enhance high-performance concrete and mortars' durability, strength, and chemical resistance. It is also a key component in ceramic tiles, adhesives, grouts, sealants, bricks, and fiber cement boards. Furthermore, its amorphous form is utilized in paints, coatings, and waterproofing agents to improve weather resistance and adhesion. The rise in sustainable and green construction practices has further driven the use of engineered materials, especially in energy-efficient buildings.

It plays a vital role in the oil and gas industry, particularly in drilling operations. It is primarily used as a proppant in hydraulic fracturing, where sand (also known as frac sand) is injected into rock formations to keep fractures open, allowing oil and gas to flow more freely. In addition, it is utilized in drilling muds to control pressure and stabilize boreholes. Its thermal stability and chemical inertness suit high-temperature and high-pressure environments encountered during exploration and production. Furthermore, silica-based materials are used in cementing operations to enhance wellbores' mechanical strength and durability.

Regional Insights

The silica market in North America accounted for a significant market revenue share in 2025. The region's growing construction sector continues to fuel demand for it across multiple applications, including concrete, paints and coatings, and adhesives and sealants. Furthermore, the surge in tire demand is significantly boosting usage in rubber applications within the U.S. According to a 2025 update from the U.S. Tire Manufacturers Association (USTMA), tire shipments for passenger vehicles and light trucks are projected to reach record levels, driven by increased vehicle usage and replacement demand. This upward trend will sustain the demand across the North American market in the coming years.

U.S. Silica Market Trends

U.S. dominated the revenue share of over 78.0% in 2025, the North America silica market. The silica market in the U.S. is experiencing steady growth, driven by strong demand from the construction, automotive, oil & gas, and glass manufacturing sectors. Industrial sand, particularly frac sand, continues to dominate due to its extensive use in hydraulic fracturing. Moreover, the growing adoption of green tires and electric vehicles has significantly boosted the demand for specialty in tire production, such as precipitated and fumed silica. Increased activity across major U.S. cities also contributes to increased consumption of high-performance concrete and eco-friendly coatings.

Asia Pacific Silica Market Trends

Asia Pacific dominated the silica market with the largest revenue share of 41.8% in 2025, driven by rapid industrialization, rising infrastructure investments, and growing automotive consumption. As of 2025, Asia Pacific remains dominant, supported by large-scale urban development projects and robust demand from end-use industries. According to the latest data from the International Organization of Motor Vehicle Manufacturers (OICA), Asia Pacific remains the world’s largest producer of motor vehicles, with countries such as China, India, Japan, and South Korea contributing significantly to global output.

China Silica Market Trends

China dominated the Asia Pacific market with a revenue share of 53.6% in 2025. China represents the largest share of the global silica market, driven by its strong manufacturing base and broad industrial demand. The country consumes significant volumes of silica across glass production, construction materials, foundry applications, chemicals, and electronics manufacturing. Growing investments in renewable energy, particularly solar photovoltaic manufacturing, are further increasing demand for high-purity silica used in photovoltaic glass and silicon processing. In addition, continued infrastructure development, expansion of advanced manufacturing industries, and increasing production of specialty glass and semiconductors are supporting market growth.

Europe Silica Market Trends

The silica market in Europe is expected to grow significantly from 2026 to 2033 due to environmental regulations such as the Paints Directive 2004/42/EC, implemented by the European Commission to limit volatile organic compound (VOC) emissions. The shift toward low-VOC and sustainable paint formulations encourages the adoption of eco-friendly additives, including silica. In 2025, several European coatings manufacturers announced new product lines featuring low-VOC and silica-enhanced formulations in response to tightening environmental regulations. In addition, Europe's position as a leading consumer and exporter of agrochemicals, particularly in countries like France, Germany, and the Netherlands, continues to drive its demand in agricultural formulations. The region's emphasis on sustainable agriculture and crop protection will further support market growth during the forecast period.

Key Silica Company Insights

Some of the key players operating in the market include Cabot Corporation, Evonik Industries AG, Wacker Chemie AG, and Solvay SA.

-

Evonik is one of the world’s largest silica producers, offering a comprehensive range of precipitated and fumed forms under the ULTRASIL, SIPERNAT, and AEROSIL brands. Its products are widely used in automotive tires, pharmaceutical formulations, food processing, and cosmetics. With strong R&D capabilities and a global production network, Evonik continues to lead innovation in high-performance materials.

-

Cabot is a U.S.-based multinational known for its fumed silica and specialty materials. It is extensively used in rubber reinforcement, industrial sealants, coatings, and insulation technologies. Cabot focuses on sustainability and circular material practices, making it a preferred choice in eco-conscious industries.

-

Wacker produces fumed silica under the HDK brand, targeting sectors such as construction chemicals, personal care, silicone rubber, and battery systems. The company is highly invested in developing EV and energy storage applications, aligning with global clean energy trends.

-

Solvay is a major player in precipitated silica, producing energy-efficient tire-grade materials under its ZEOSIL brand. It caters to the automotive, oral care, and food industries. Solvay emphasizes reducing CO₂ emissions in its manufacturing processes and expanding its presence in Asia and North America.

Key Silica Companies:

The following key companies have been profiled for this study on the silica market.

-

Cabot Corporation

-

Evonik Industries AG

-

Imerys S.A.

-

Nissan Chemical Corp.

-

Oriental Silicas Corp.

-

PPG Industries Inc.

-

Solvay SA

-

Tosoh Corporation

-

W.R. Grace & Co.

-

Wacker Chemie AG

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (e.g., Evonik Industries AG, Cabot Corporation, Solvay SA, Wacker Chemie AG, PPG Industries Inc.)

- Focus on large-scale production of precipitated silica, fumed silica, colloidal silica, silica gel, and other specialty silica products.

- Emphasize technology-driven manufacturing, product innovation, and development of high-performance silica grades for tires, coatings, electronics, personal care, and industrial applications.

- Invest heavily in R&D, capacity expansions, sustainability initiatives, and strategic collaborations with end-use industries.

- Possess advanced production technologies, extensive intellectual property portfolios, strong R&D capabilities, and global distribution networks.

- Benefit from diversified product portfolios, long-standing customer relationships, and strong positions in high-value specialty silica segments.

- Well-positioned to serve multinational customers across automotive, electronics, chemicals, and consumer goods industries.

- Face high capital and operating costs associated with specialty silica production and environmental compliance.

- Vulnerable to fluctuations in energy, raw material, and transportation costs.

- Increasing regulatory requirements related to emissions, sustainability, and workplace safety may impact profitability.

Emerging & Regional Players (e.g., Oriental Silicas Corporation, Imerys S.A., Nissan Chemical Corp., Tosoh Corporation, W.R. Grace & Co.)

- Focus on regional silica production and supply, specialty product development, and strengthening domestic distribution networks.

- Pursue operational efficiency, selective capacity expansion, and strategic partnerships with local end users.

- Target growing demand from tires, construction materials, water treatment, food processing, and industrial manufacturing sectors.

- Greater flexibility in addressing regional customer requirements and niche application needs.

- Strong domestic market presence and established relationships with local manufacturers and distributors.

- Ability to capitalize on regional industrialization, infrastructure development, and rising specialty silica demand.

- Limited global reach and lower production scale compared to multinational silica producers.

- Higher dependence on regional economic conditions and industry demand cycles.

- May face challenges in competing with larger players on technology, product breadth, R&D investment, and global supply capabilities.

Recent Developments

-

In 2025, Evonik announced the expansion of its silica plant in Thailand to meet rising demand for green tire materials in Southeast Asia. The company also introduced a next-generation AEROSIL product optimized for lithium-ion battery separators and cosmetic formulations, enhancing thermal stability and performance.

-

Cabot inaugurated a new fumed silica production unit in Texas, USA, to enhance its domestic supply capabilities. It also partnered strategically with an EV battery manufacturer to supply fumed silica for advanced gel electrolytes, further expanding into the energy storage space.

-

In early 2025, Wacker began commercial production at its new HDK fumed silica facility in South Korea, strategically located to serve Asia's growing electronics and coatings markets. The plant focuses on producing high-purity grades suitable for semiconductors and specialty adhesives.

-

Solvay launched a new low-carbon precipitated silica line in its plant in France as part of its “Green Materials 2030” initiative. The 2025 development includes integrating biomass-based energy into silica production, aimed at reducing emissions by 30% over the next five years.

Silica Market Report Scope

Report Attribute

Details

Market definition

The apparent consumption of amorphous and crystalline silica across end-use industries, including construction, glass, oil & gas, and others, is considered in the scope.

Market size in 2025

USD 42.9 billion

Estimated market size in 2026

USD 45.8 billion

Projected market size by 2033

USD 85.9 billion

Growth rate

CAGR of 9.4% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million, volume in kilotons, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, volume forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; UK; Russia; Turkey; China; India; Japan; South Korea; Brazil

Key companies profiled

Cabot Corporation; Evonik Industries AG; Imerys S.A.; Nissan Chemical Corp.; Oriental Silicas Corp.; PPG Industries Inc.; Solvay SA; Tosoh Corporation; W.R. Grace & Co.; Wacker Chemie AG

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase—addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Silica Market Report Segmentation

This report forecasts revenue growth globally, nationally, and regionally from 2021 to 2033 and analyzes the latest trends in each sub-segment. For this study, Grand View Research has segmented the global silica market report by product, end-use, and region:

-

Product Outlook (Volume, Kilotons; Revenue, USD Billion, 2021 - 2033)

-

Amorphous

-

Crystalline

-

-

End-use Outlook (Volume, Kilotons; Revenue, USD Billion, 2021 - 2033)

-

Building & Construction

-

Oil & Gas

-

Glass Manufacturing

-

Water Treatment

-

Others

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

Russia

-

Turkey

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

Research Methodology

The silica market figures in this report are based on a proven research process that combines executive interviews with secondary research from proprietary databases, company filings, and recognized regulatory and institutional sources. Market size is built through value-chain sizing - reconciling supply-side and demand-side estimates - and triangulated with bottom-up and top-down approaches. Every estimate passes multiple levels of expert validation before publication, with each silica segment quantified using the revenue-capture definitions in the table below.

Segment Definition

Product

Revenue Capture Definition

Amorphous

This segment includes synthetic and non-crystalline silica products such as precipitated silica, fumed silica, silica gel, colloidal silica, and fused silica. Revenue is generated from the sale of amorphous silica used in rubber and tire manufacturing, paints & coatings, adhesives & sealants, personal care products, electronics, catalysts, food additives, and specialty industrial applications requiring high purity, reinforcement, adsorption, or rheology control properties.

Crystalline

This segment comprises naturally occurring silica, including quartz, silica sand, and sandstone. Revenue is derived from the sale of crystalline silica used in glass manufacturing, foundry casting, construction materials, ceramics, hydraulic fracturing, water filtration, and other industrial applications requiring high silica content, hardness, and thermal stability.

End Use

Revenue Capture Definition

Building & Construction

This segment includes silica used in cement, concrete, mortars, flooring, ceramics, roofing materials, insulation products, and specialty construction chemicals. Revenue is generated from the sale of silica products that enhance strength, durability, workability, and long-term performance in residential, commercial, and infrastructure projects.

Oil & Gas

This segment covers silica used primarily as frac sand in hydraulic fracturing operations and in drilling, cementing, and well-completion activities. Revenue is generated from the sale of silica products that improve hydrocarbon extraction efficiency and well productivity in upstream oil and gas operations.

Glass Manufacturing

This segment includes silica consumed in the production of flat glass, container glass, fiberglass, specialty glass, solar glass, and optical glass. Revenue is derived from the sale of silica as the primary raw material for glass production, providing transparency, chemical resistance, durability, and thermal stability.

Water Treatment

This segment comprises silica used in filtration media for municipal, industrial, and wastewater treatment systems. Revenue is generated from the sale of silica sand and related filtration products used to remove suspended solids, impurities, and contaminants from water streams.

Others

This segment includes silica utilized in foundry, rubber & tires, chemicals, paint & coatings, electronics & semiconductors, agriculture, personal care, and other industrial applications. Revenue is generated from the sale of silica products that provide reinforcement, abrasion resistance, thermal stability, adsorption capacity, and performance enhancement across various end-use industries.

Estimation Model

Layer Name

Key Question

Description

End-Use Industry Demand Base Layer

What forms the demand base?

Identify silica demand generated across key end-use industries, including glass manufacturing, building & construction, foundry, oil & gas, rubber & tires, electronics & semiconductors, chemicals, water treatment, paints & coatings, and renewable energy. Assess silica consumption associated with glass production, construction materials, metal casting, hydraulic fracturing, tire manufacturing, semiconductor fabrication, and industrial processing applications. This layer establishes the total addressable demand for silica globally.

Silica Production & Supply Layer

Where is silica produced and supplied?

Estimate silica availability from major silica sand mines, quartz producers, and specialty silica manufacturers across key regions. Analyze production capacities, reserve availability, processing infrastructure, purity grades, trade flows, import-export dynamics, and regional supply-demand balances. Evaluate the role of mining companies, silica processors, distributors, and specialty silica manufacturers in ensuring supply across end-use industries.

Application Consumption Intensity Layer

How much silica is consumed?

Analyze silica consumption intensity across glass manufacturing, concrete and cement production, foundry casting, hydraulic fracturing, rubber reinforcement, semiconductor manufacturing, filtration systems, and specialty chemical applications. Evaluate silica usage per unit of glass produced, construction activity, metal casting output, oil & gas well completion, tire production, and electronic component manufacturing. Consumption intensity varies by application, purity requirements, performance specifications, processing technologies, and regional industrial practices.

Revenue Layer

How is market revenue generated?

Market revenue is quantified through the production and sale of silica products, including silica sand, quartz, fused silica, precipitated silica, fumed silica, colloidal silica, silica gel, and other specialty silica materials across multiple end-use industries. Revenue generation is influenced by silica grade, purity levels, processing costs, mining activities, transportation expenses, trade dynamics, and end-user demand. Growth in glass production, infrastructure development, semiconductor manufacturing, renewable energy deployment, oil & gas activities, and industrialization drives overall market value.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Cross-Segmentation Analysis

Detailed analysis of silica demand across key intersections such as region × end use, product type × application, and purity grade × industry. Identified consumption patterns, growth rates, and market attractiveness across individual sub-segments.

Enabled identification of the most lucrative market pockets, niche growth opportunities, and priority investment areas. Supported targeted marketing and resource allocation strategies.

Trade Assessment

Detailed evaluation of global silica trade flows, including key exporting and importing countries, trade volumes, trade balances, logistics routes, and supply chain dependencies. Assessed the impact of trade regulations, tariffs, and regional supply-demand gaps on market dynamics.

Enabled identification of sourcing opportunities, export potential, trade risks, and supply chain vulnerabilities. Supported procurement optimization and international market expansion strategies.

Opportunity Assessment by High-Growth Applications

In-depth evaluation of emerging opportunities across semiconductors, solar photovoltaics, specialty chemicals, lithium-ion batteries, advanced glass, and electronics applications. Assessed demand outlook, adoption trends, investment activity, and revenue potential for each application segment.

Enabled identification of high-margin growth areas, diversification opportunities, and future demand centers. Supported strategic investment decisions and long-term business planning.

Frequently Asked Questions About This Report

The global silica market was valued at USD 42.9 billion in 2025 and is projected to reach USD 45.8 billion in 2026.

The silica market is projected to grow at a CAGR of 9.4% from 2026 to 2033, reaching USD 85.9 billion by 2033.

Some of the key players operating in the silica market are Cabot Corporation, Evonik Industries AG, Imerys S.A., Nissan Chemical Corp., Oriental Silicas Corp., PPG Industries Inc., Solvay SA, Tosoh Corporation, W.R. Grace & Co., and Wacker Chemie AG, among others.

The silica market is witnessing strong growth driven by rising demand across various end-use industries, particularly automotive, construction, electronics, and personal care. In the automotive sector, silica is increasingly used in producing high-performance tires due to its ability to enhance fuel efficiency, grip, and overall tire durability.

Asia Pacific dominated the silica market, accounting for a 44.2% revenue share of the global silica market in 2025.

Crystalline silica led the market with the largest revenue share of 71.8% in 2025.

Glass manufacturing led the market with the revenue share of 46.8% in 2025.

About the Author(s)

Plastics, Polymers & Resins Research Team

Bulk Chemicals · Plastics, Polymers & ResinsThis report was authored by the plastics, polymers & resins research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the plastics, polymers & resins segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.