- Home

- »

- Next Generation Technologies

- »

-

Smart Manufacturing Market Size & Share Report 2026-2033GVR Report cover

![Smart Manufacturing Market (2026 - 2033)Report]()

Smart Manufacturing Market (2026 - 2033)

Size, Share & Trends Analysis Report By Component (Hardware, Software, Services) By Technology (Machine Execution Systems, Programmable Logic Controller, Enterprise Resource Planning), By End-use, By Region, And Segment Forecasts

Market Size, 2025

$410.7BMarket Estimate, 2026

$478.9BMarket Forecast, 2033

$1,063.2BCAGR, 2026–2033

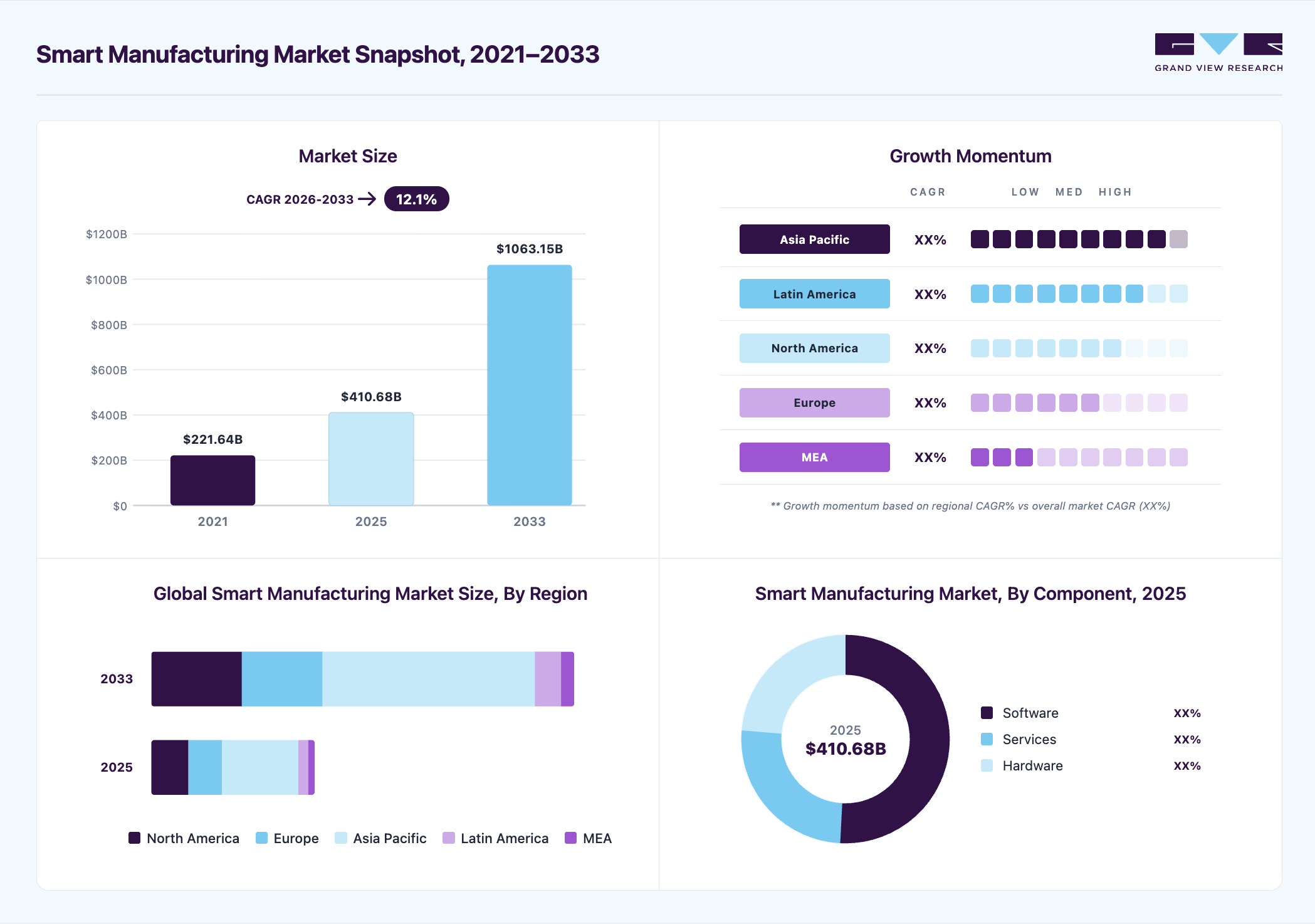

12.1%Smart Manufacturing Market Summary

The global smart manufacturing market size was valued at USD 410.7 billion in 2025 and is projected to grow from USD 478.9 billion in 2026 to USD 1,063.2 billion by 2033, at a CAGR of 12.1% from 2026 to 2033. Asia Pacific dominated the global market with the largest revenue share of 46.6% in 2025. This market expansion is driven by the widespread adoption of Industry 4.0 technologies, IoT, AI, machine learning, and cloud computing, and the growing demand for automation & cost efficiency.

Key Market Trends & Insights

- By component: Software segment dominated the market, with a revenue share of 50.8% in 2025.

- By technology: DCS segment held the largest market share of 16.1% in 2025.

- By end-use: Automotive segment hold the largest revenue share of 19.1% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (46.6% revenue share, 2025)

- By country: The smart manufacturing market in the China held the largest share in the Asia Pacific region in 2025.

Market Size & Forecast

- Market size in 2025: USD 410.7 Billion

- Estimated market size in 2026: USD 478.9 Billion

- Projected market size by 2033: USD 1,063.2 Billion

- CAGR (2026-2033): 12.1%

Governments worldwide are promoting smart manufacturing through initiatives focused on research into technologies such as digital twins and machine condition monitoring. Smart manufacturing industry growth is driven by the convergence of edge computing, low-power microelectronics, and AI-based analytics that enhance device intelligence beyond basic automation. The integration of generative AI technologies further accelerates this transformation, turning traditional manufacturing devices into interactive digital companions that understand and anticipate operational needs. These ecosystems are becoming increasingly context-aware, responsive, and embedded across production environments, facilitating enhanced productivity, cost efficiency, and quality control.The software segment dominates the smart manufacturing market due to the increasing adoption of advanced analytics, AI-driven platforms, and industrial Internet of Things (IIoT) solutions that enable real-time monitoring and predictive decision-making. Software solutions play a critical role in integrating data across production systems, improving operational efficiency, and reducing downtime through predictive maintenance. The rising demand for digital twins, manufacturing execution systems (MES), and cloud-based platforms further strengthens software adoption. Additionally, continuous advancements in automation, data visualization, and cybersecurity solutions are accelerating the reliance on software as the core enabler of smart factory ecosystems.

")

Additionally, rising enterprise expectations for operational efficiency, automation, and context-aware decision-making are key growth drivers. As industries demand systems that anticipate equipment needs, optimize workflows, and manage energy usage, manufacturers embed advanced sensors, AI, and connectivity into production lines. The need for smooth interoperability across equipment and software platforms pushes companies to invest in robust industrial connectivity infrastructure, edge computing capabilities, and collaborative ecosystem partnerships.

Evolving regulatory mandates and cybersecurity standards are pushing stronger adoption within the smart manufacturing industry. Government bodies require that manufacturing systems support data protection, secure firmware updates, and transparency in processing data. Platforms enabling automated alerts, anomaly detection, and secure provisioning help manufacturers comply with regulations, reducing operational risk and building trust in connected industrial ecosystems.

The proliferation of Industry 4.0 technologies, digital twins, and ambient intelligence is generating strong demand for integrated smart manufacturing solutions. Devices and systems become part of a unified digital ecosystem, allowing manufacturers to benefit from predictive analytics, cross-system control, and enhanced process optimization. These capabilities promote loyalty in the market, as integrated solutions deliver greater value than standalone technologies.

Market Dynamics

The smart manufacturing market is being driven by the convergence of edge computing, low-power microelectronics, and AI-based analytics that enhance device intelligence beyond basic automation. The integration of generative AI technologies further accelerates this transformation, turning traditional manufacturing devices into interactive digital companions that understand and anticipate operational needs. These ecosystems are becoming increasingly context-aware, responsive, and embedded across production environments, facilitating enhanced productivity, cost efficiency, and quality control.

Manufacturers across industries are under increasing pressure to improve productivity while controlling operating expenses in highly competitive markets. Rising labor costs, fluctuating raw material prices, and growing customer expectations for faster delivery are driving companies to modernize production environments. Smart manufacturing technologies enable continuous monitoring of equipment, processes, and resource utilization, helping organizations identify inefficiencies and eliminate production bottlenecks. The integration of connected sensors, industrial IoT platforms, and advanced analytics provides greater visibility across manufacturing operations, supporting more informed decision-making.

Moreover, manufacturers are prioritizing solutions that reduce downtime, minimize waste, and improve product quality. Predictive maintenance and automated process control help prevent costly equipment failures while optimizing asset performance and production throughput. Real-time insights into factory operations allow businesses to adjust workflows quickly and improve inventory management. As organizations focus on maximizing output with existing resources and maintaining profitability, investments in smart manufacturing solutions continue to accelerate, making operational efficiency and production optimization a key market growth driver.

The adoption of smart manufacturing technologies requires substantial upfront investment in industrial automation systems, advanced sensors, robotics, industrial IoT platforms, cloud infrastructure, and AI-driven analytics solutions. Many manufacturers, particularly small and medium-sized enterprises, face financial constraints when upgrading legacy production facilities to support digitally connected operations. The cost of acquiring hardware, software licenses, network infrastructure, and cybersecurity solutions adds to the overall implementation burden.

In addition to capital expenditure, integrating new technologies with existing manufacturing equipment often involves complex customization, system redesign, and operational disruptions. Legacy systems may lack compatibility with modern digital platforms, increasing deployment timelines and project costs. Organizations also experience expenses related to employee training, maintenance, and ongoing system optimization, which can delay return on investment and limit the pace of smart manufacturing adoption across industries.

The increasing deployment of connected sensors, industrial IoT platforms, and advanced analytics is creating significant opportunities for AI-powered predictive maintenance across manufacturing facilities. Traditional maintenance approaches often result in unplanned equipment failures, production disruptions, and higher operational costs, prompting manufacturers to adopt data-driven maintenance strategies. AI algorithms can continuously analyze machine performance, vibration patterns, temperature fluctuations, and other operational parameters to identify potential faults before they lead to breakdowns.

As manufacturers pursue higher productivity and asset utilization, predictive maintenance solutions are becoming an integral part of smart factory initiatives. Technology helps reduce downtime, extend equipment lifespan, optimize maintenance schedules, and improve workforce efficiency. Growing investments in digital transformation, joined with the need to enhance operational resilience and reduce maintenance expenditures, are expected to accelerate the adoption of AI-powered predictive maintenance across industrial facilities.

Market Concentration & Characteristics

The smart manufacturing market driven by continuous advancements in AI, industrial IoT, digital twins, machine vision, robotics, and edge computing technologies. Manufacturers are increasingly investing in intelligent production systems that enable predictive maintenance, real-time process optimization, and autonomous decision-making. The merging of operational technology (OT) and information technology (IT) is accelerating the development of connected factories, while emerging technologies such as generative AI and digital simulation platforms are expanding the capabilities of smart manufacturing ecosystems.

End-user concentration in the market is moderate to high, with demand distributed across several major industrial sectors including automotive, electronics, aerospace, pharmaceuticals, food and beverage, and heavy machinery manufacturing. Large enterprises account for a significant share of investments due to their greater financial resources and extensive production networks, while small and medium-sized manufacturers are increasingly adopting scalable digital solutions. The broad applicability of smart manufacturing technologies across multiple industries prevents excessive dependence on a single end-user segment.

Analyst Perspective

The smart manufacturing market combines industrial automation, AI, industrial IoT, robotics, and advanced analytics to drive industrial digital transformation. Manufacturers are investing in connected production systems to improve efficiency, product quality, resource utilization, and supply chain resilience while addressing labor shortages and operational complexity. A key competitive advantage lies in integrating automation hardware, industrial software, data management, and analytics into a unified platform. Vendors with interoperable solutions and strong ecosystem capabilities are better positioned to secure long-term customer relationships. Market value is increasingly shifting from equipment sales toward software, analytics, and lifecycle services, supporting recurring revenue and data-driven manufacturing operations.

Component Insights

Based on component, the software segment led the market with the largest revenue share of 50.8% in 2025 and is expected to grow at the fastest CAGR over the forecast period. Solutions such as ERP, MES, and advanced analytics support real-time monitoring, predictive maintenance, and overall operational efficiency. With the growing integration of IoT-enabled devices and blockchain-based data security frameworks, manufacturers are increasingly adopting more connected equipment and relying on consistent, secure data flows, making software the central layer that coordinates these activities. This continued shift toward digitally managed operations is the main factor behind the steady growth of the software segment.

The services segment is expected to witness a significant CAGR of over 12.0% from 2026 to 2033, driven by the need for ongoing system integration, maintenance, and operational support. As manufacturers adopt IoT, AI, and cloud-based systems, demand for consulting, implementation, and managed services continues to rise. The expansion of predictive maintenance, remote monitoring, and data-driven decision tools further increases reliance on external expertise. Companies require support to keep systems updated, interconnected, and functional, which contributes to the sustained growth of the services segment in smart manufacturing.

Technology Insights

DCS segment held the largest market share of 16.1% in 2025, driven by its extensive deployment across industries such as manufacturing, energy, and utilities. DCS platforms enable efficient management of complex processes while ensuring continuous and stable operations, making them ideal for automation environments that demand high precision and reliability. The integration of advanced analytics, IoT connectivity, edge computing, and AI-driven optimization enhances real-time monitoring, control, and decision-making capabilities. These advancements continue to reinforce the critical role of DCS in the evolution of smart and digitally connected manufacturing ecosystems.

The 3D printing segment is expected to witness the fastest CAGR from 2026 to 2033, driven by its adoption in aerospace, automotive, healthcare, and consumer goods. It allows manufacturers to produce complex, customized parts more quickly and at a lower cost. Advancements in materials and printing methods, along with the need for on-demand production and reduced inventory, support its growing use. Hence, these factors are likely to drive the rapid expansion of 3D printing in manufacturing operations.

End Use Insights

Based on end-use, the automotive segment led the market with the largest revenue share of 19.1% in 2025, owing to its extensive use of smart manufacturing technologies to improve production efficiency, reduce costs, and maintain product quality. Manufacturers use robotics, AI, IIoT, and automation to streamline assembly lines and support mass customization. The rising demand for electric vehicles and the focus on sustainable manufacturing practices have further increased adoption. Therefore, these factors have contributed to the significant role of the automotive sector in the market.

The renewable energy segment is expected to grow at the fastest CAGR from 2026 to 2033, driven by the use of advanced manufacturing technologies for precision and efficiency. Smart tools help meet the growing demand for sustainable energy solutions. Government support for renewable initiatives and the focus on reducing carbon emissions further encourage investment. These factors together increase the adoption of smart manufacturing in this sector. Hence, the renewable energy is likely to be the fastest-growing segment in the market.

Regional Insights

North America significantly dominated the smart manufacturing industry with a share exceeding 22.0% in 2025, driven by the region's early and rapid adoption of Industry 4.0 technologies. Key drivers include widespread integration of IoT devices, advanced AI analytics, and robotics that enhance automation and operational efficiency across manufacturing sectors. The increasing focus on sustainable and energy-efficient production methods further boosts market growth by reducing environmental impact and operational costs. These combined factors create a robust ecosystem that accelerates smart manufacturing deployment and innovation across North America.

U.S. Smart Manufacturing Market Trends

The U.S. smart manufacturing industry dominated in 2025, driven by rapid technological advancements in automation, robotics, AI, and IoT. The U.S. government’s support for advanced manufacturing through initiatives such as Manufacturing USA has accelerated the deployment of smart manufacturing solutions. Additionally, the growing focus on sustainability and energy efficiency, along with the rise of smart factories, is driving manufacturers to adopt innovative solutions for real-time monitoring, predictive maintenance, and improved supply chain management.

Europe Smart Manufacturing Market Trends

The Europe smart manufacturing industry is expected to grow at a CAGR of over 11.0% from 2026 to 2033. The European Union’s Industry 4.0 initiative encourages the adoption of smart manufacturing technologies, such as AI, IoT, and robotics, to enhance competitiveness. The region’s emphasis on environmental sustainability drives the demand for energy-efficient and low-emission manufacturing solutions, making smart manufacturing an attractive option in the Europe region.

The UK smart manufacturing market is expected to grow significantly in the coming years, driven by government-backed programs such as the Made Smarter initiative and the adoption of advanced manufacturing technologies, including IoT, AI, and robotics. Additionally, there is a growing emphasis on sustainable manufacturing practices as the UK works towards its net-zero goals, driving the need for more efficient, resource-conscious manufacturing systems.

The smart manufacturing market in Germany is characterized by its strong industrial base and commitment to Industry 4.0. German brands are increasingly using AR/VR to enhance product design and provide virtual product demonstrations. Moreover, Germany’s data protection laws and emphasis on user privacy shape how immersive technologies are deployed, creating a trend toward more secure and transparent customer experiences.

Asia Pacific Smart Manufacturing Market Trends

Asia Pacific dominated the smart manufacturing market with the largest revenue share of 46.6% in 2025 and is expected to grow at the fastest CAGR of over 13.0% from 2026 to 2033, driven by the increasing adoption of advanced technologies in countries. The region’s strong manufacturing base, particularly in electronics, automotive, and consumer goods, has led to the adoption of robotics and digitalization to streamline operations, enhance efficiency, and reduce costs.

The Japan smart manufacturing market is witnessing steady growth, supported by the country’s advanced industrial base, particularly in automotive, electronics, and robotics. Strong government initiatives promoting Industry 4.0 adoption, along with a focus on sustainability and energy efficiency, are accelerating the deployment of technologies such as IoT, AI-driven automation, digital twins, and advanced robotics, thereby strengthening innovation and operational excellence across manufacturing sectors.

The smart manufacturing market in the China held the largest share in the Asia Pacific region in 2025. The smart manufacturing market in China is experiencing rapid expansion, driven by substantial investments in automation, robotics, artificial intelligence, IoT, and 5G-enabled industrial networks to enhance production efficiency, product quality, and global competitiveness. With its vast manufacturing ecosystem spanning electronics, automotive, and consumer goods, China is increasingly integrating technologies such as cloud computing, big data analytics, and edge computing to optimize operations, reduce costs, and accelerate its transition toward high-tech, intelligent manufacturing.

Key Smart Manufacturing Company Insights

Some of the key players operating in the market are ABB Ltd. and Siemens AG.

-

ABB Ltd. provides innovative solutions that drive digital transformation in industries such as manufacturing, utilities, and transportation. ABB specializes in industrial robotics, AI-powered automation, and IoT systems that enhance operational efficiency, reduce costs, and improve sustainability. Its smart manufacturing solutions, including advanced automation and digital services, support manufacturers in optimizing production processes and achieving real-time operational insights, playing a key role in the smart manufacturing industry.

-

Siemens AG is a global technology conglomerate known for its cutting-edge innovations in automation, digitalization, and electrification. Siemens AG offers a comprehensive range of smart manufacturing solutions, including industrial automation, AI-driven analytics, digital twins, and IoT platforms. These solutions enable manufacturers to optimize production, improve asset management, and enhance operational efficiency.

FANUC Corporation and Mitsubishi Electric Corporation are some of the emerging participants in the smart manufacturing market.

-

FANUC Corporation specializes in manufacturing computer numerical control (CNC) systems, lasers, industrial robots, and robot machines such as electric injection molding machines and wire electrical discharge machines under brands such as ROBOSHOT and ROBOCUT. With operations spanning Asia, Europe, the Americas, and South Africa, the company is renowned for its innovative automation solutions and robust service support.

-

Mitsubishi Electric Corporation is a multinational company specializing in industrial automation and smart manufacturing technologies. The company offers advanced solutions, including programmable logic controllers (PLCs), industrial robots (MELFA series), and servo motors. The company is committed to Industry 4.0 innovations through strategic investments and partnerships.

Key Smart Manufacturing Companies

The following key companies have been profiled for this study on the smart manufacturing market.

-

ABB Ltd.

-

Cisco Systems, Inc.

-

Siemens AG

-

General Electric

-

Rockwell Automation Inc.

-

Schneider Electric

-

Honeywell International Inc.

-

Emerson Electric Co.

-

FANUC Corporation

-

Mitsubishi Electric Corporation

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (ABB Ltd.; Siemens AG; Schneider Electric; Honeywell International Inc.)

- Focus on integrated end-to-end smart factory ecosystems combining automation hardware, industrial software, cloud platforms, and services.

- Emphasize strategic acquisitions, technology partnerships, and recurring revenue models through software subscriptions and lifecycle management services.

- Strong installed base across manufacturing industries enables cross-selling of advanced digital solutions and long-term customer retention.

- Extensive R&D capabilities, global service networks, and comprehensive product portfolios support large-scale industrial deployments.

- Large organizational structures can slow product development cycles and responsiveness to niche customer requirements.

- Dependence on legacy industrial systems may increase integration complexity and implementation costs for customers.

Emerging Players (Cisco Systems, Inc.; General Electric)

- Concentrate on specialized technologies such as AI analytics, industrial IoT, machine vision, digital twins, and predictive maintenance applications.

- Target specific manufacturing use cases with agile development models and cloud-native solution architectures.

- Faster innovation cycles enable rapid introduction of advanced features and industry-specific solutions.

- Flexible deployment models and focused offerings support quicker adoption among mid-sized manufacturers.

- Limited global presence and smaller customer bases can restrict market penetration and scalability.

- Lower financial resources compared with established automation vendors may constrain expansion and R&D investments.

Recent Developments

-

In March 2026, ABB Ltd. announced an investment of approximately USD 75 million to expand its manufacturing and R&D footprint in India, strengthening its position in the smart manufacturing and industrial automation sector. The investment focuses on enhancing production capacity, developing advanced electrification and automation technologies, and establishing new research facilities to support growing demand across sectors such as renewable energy, data centers, and transportation infrastructure

-

In February 2026, Schneider Electric unveiled EcoStruxure Foxboro Software Defined Automation (SDA), the industry’s first open, software-defined Distributed Control System (DCS), designed to enable flexible and future-ready industrial automation. The solution decouples software from hardware, allowing greater interoperability, rapid deployment, and scalable configurations while maintaining high system availability.

-

In March 2025, ABB Ltd. expanded its presence in the U.S. and China, strengthening its position in the smart manufacturing industry. The company’s investment in new facilities and technology aims to enhance its production capabilities and support the growing demand for automation and advanced manufacturing solutions.

-

In March 2025, Schneider Electric SE announced a 44 million euros investment in its Dunavecse facility in Hungary to enhance its smart manufacturing capabilities. This investment aims to support the company's commitment to increasing production capacity for energy management and automation solutions.

-

In January 2025, Siemens AG unveiled groundbreaking innovations in industrial AI and digital twin technology at CES. These advancements are designed to enhance manufacturing processes by integrating AI-driven analytics and virtual representations of physical assets, known as digital twins in the smart manufacturing industry.

Smart Manufacturing Market Report Scope

Report Attribute

Details

Market size in 2025

USD 410.7 billion

Estimated market size in 2026

USD 478.9 billion

Projected market size by 2033

USD 1,063.2 billion

Growth rate

CAGR of 12.1% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Component, technology, end-use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; Japan; India; South Korea; Australia; Brazil; Saudi Arabia; South Africa; UAE

Key companies profiled

ABB Ltd., Cisco Systems, Inc., Siemens AG, General Electric, Rockwell Automation Inc., Schneider Electric, Honeywell International Inc., Emerson Electric Co., FANUC Corporation, Mitsubishi Electric Corporation.

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Smart Manufacturing Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest technological trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global smart manufacturing market report based on components, technology, end use, and region:

-

Component Outlook (Revenue, USD Billion, 2021 - 2033)

-

Hardware

-

Software

-

Services

-

-

Technology Outlook (Revenue, USD Billion, 2021 - 2033)

-

Machine Execution Systems

-

Programmable Logic Controller

-

Enterprise Resource Planning

-

SCADA

-

Discrete Control Systems

-

Human Machine Interface

-

Machine Vision

-

3D Printing

-

Product Lifecycle Management

-

Plant Asset Management

-

-

End Use Outlook (Revenue, USD Billion, 2021 - 2033)

-

Oil & Gas

-

Energy & Power

-

Food & Beverages

-

Pharmaceuticals

-

Chemicals

-

Metals & Mining

-

Pulp & Paper

-

Automotive

-

Aerospace & Defense

-

Semiconductor & Electronics

-

Renewable Energy

-

Medical Devices

-

Heavy Machinery

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

South Africa

-

-

Research Methodology

Segment Definition

Segment - Component

Revenue capture definition

Hardware

Revenue is captured from industrial robots, sensors, controllers, machine vision systems, and connected manufacturing equipment deployed across production facilities. It also includes edge devices and automation infrastructure supporting real-time factory operations.

Software

This segments revenue is captured from manufacturing execution systems, industrial IoT platforms, digital twins, AI analytics software, and automation applications. It includes licensing, subscriptions, and support fees associated with digital manufacturing solutions.

Services

Revenue from consulting, system integration, deployment, training, and technical support services for smart manufacturing projects. It also includes managed services, maintenance, and optimization engagements for connected factory environments.

Segment - Technology

Revenue capture definition

MES

Revenue is captured from software licenses, cloud subscriptions, implementation services, and maintenance contracts that enable production monitoring, scheduling, quality management, and shop-floor execution. The segment includes expenditures on MES platforms integrated with factory automation and enterprise systems.

PLC

Revenue comprises sales of PLC hardware, controllers, programming software, communication modules, and associated engineering services used for industrial automation and machine control. It covers both new installations and upgrade projects across manufacturing facilities.

ERP

Revenue is generated from ERP software licenses, SaaS subscriptions, deployment services, and support solutions that manage manufacturing operations, procurement, inventory, finance, and supply chain functions. The segment includes manufacturing-focused ERP platforms and related integrations.

SCADA

Revenue includes software platforms, visualization tools, communication infrastructure, and implementation services used for real-time monitoring and control of industrial processes. It also covers system upgrades, maintenance, and remote operational management solutions.

DCS

Revenue is derived from controllers, operator stations, engineering software, networking components, and lifecycle services deployed for continuous and complex industrial process control. The segment encompasses both greenfield installations and modernization projects.

HMI

Revenue captures sales of industrial display panels, touchscreen devices, visualization software, and configuration tools that facilitate operator interaction with manufacturing equipment. It also includes integration, maintenance, and replacement demand.

Machine Vision

Revenue consists of cameras, sensors, vision software, image processing systems, and integration services used for inspection, quality assurance, measurement, and automation applications. The segment includes both hardware and analytics-based vision solutions.

3D printing

Revenue is generated from industrial additive manufacturing equipment, printing materials, software platforms, and related support services used in prototyping, tooling, and production applications. It also includes aftermarket revenue from consumables and system maintenance.

PLM

Revenue includes software licenses, cloud subscriptions, consulting, and support services that manage product design, engineering data, collaboration, and lifecycle processes. The segment covers platforms connecting product development with manufacturing operations.

Plant Asset Management

Revenue is captured from software solutions, analytics platforms, monitoring systems, and professional services used to optimize equipment performance, maintenance planning, and asset utilization. The segment includes predictive maintenance and reliability management applications.

Segment - End Use

Revenue capture definition

Oil & Gas and Energy & Power

Revenue includes spending on automation systems, predictive maintenance platforms, industrial control solutions, and digital monitoring technologies deployed across upstream, midstream, downstream, power generation, and transmission facilities.

Food & Beverages

Revenue is generated from investments in smart production lines, quality inspection systems, packaging automation, and manufacturing execution solutions used to improve productivity, traceability, and compliance.

Pharmaceuticals

Revenue captures expenditures on connected manufacturing equipment, process automation platforms, digital quality management systems, and data-driven production technologies utilized in pharmaceutical manufacturing facilities.

Chemicals

Revenue comprises sales of process control systems, plant optimization software, industrial analytics platforms, and asset management solutions implemented across chemical production operations.

Metals & Mining

Revenue includes investments in autonomous equipment, remote monitoring systems, predictive maintenance technologies, and industrial automation solutions used in extraction, processing, and refining activities.

Pulp & Paper

Revenue is derived from smart process control, machine condition monitoring, production optimization software, and automation technologies deployed across paper mills and pulp manufacturing plants.

Automotive

Revenue encompasses spending on industrial robotics, machine vision systems, digital twin platforms, manufacturing software, and connected production technologies used in vehicle and component manufacturing.

Aerospace & Defense

Revenue captures expenditures on advanced manufacturing systems, precision automation equipment, quality inspection technologies, and digital production management platforms supporting aerospace and defense production.

Semiconductor & Electronics

Revenue includes sales of high-precision automation solutions, smart factory software, AI-enabled inspection systems, and process monitoring technologies used in semiconductor fabrication and electronics assembly.

Renewable Energy

Revenue is generated from smart manufacturing technologies supporting the production of solar panels, wind turbine components, battery systems, and other renewable energy equipment.

Medical Devices

Revenue comprises investments in automated assembly systems, quality control platforms, traceability solutions, and connected manufacturing technologies used in medical device production.

Heavy Machinery

Revenue includes spending on industrial automation, equipment monitoring systems, robotics, and digital manufacturing solutions applied in the production of construction, agricultural, and industrial machinery.

Others

Revenue captures demand from additional manufacturing sectors such as textiles, plastics, consumer goods, marine, and building materials that utilize smart manufacturing technologies to improve operational efficiency and production performance.

Estimation Model

Layer Name

Key Questions

Description

Industrial Base Layer

Which manufacturing facilities are addressable?

Identify the total installed base of manufacturing plants across industries such as automotive, electronics, pharmaceuticals, food & beverage, chemicals, metals, aerospace, and machinery. This establishes the addressable universe of facilities capable of adopting smart manufacturing technologies.

Digitalization Layer

How many facilities adopt smart manufacturing solutions?

Apply digital transformation and automation penetration rates to estimate the number of factories implementing technologies such as industrial IoT, robotics, MES, SCADA, AI analytics, and advanced process control systems. This converts the industrial base into active smart manufacturing users.

Technology Deployment Layer

Which smart manufacturing technologies are implemented?

Measure the distribution of spending across hardware, software, and services, including industrial automation, machine vision, digital twins, predictive maintenance, additive manufacturing, and industrial cybersecurity. This reflects technology adoption intensity across manufacturing operations.

Monetization Layer

How much revenue is generated?

Apply average spending per facility based on technology deployment scale, software subscriptions, automation equipment investments, integration services, maintenance contracts, and lifecycle support. Aggregating these expenditures across adopting facilities produces total smart manufacturing market revenue.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Market Entry & Expansion Assessment

Regional demand sizing and forecasting

Customer segmentation and buying behavior analysis

Competitive landscape benchmarking

Regulatory and distribution channel assessment

Identified high-growth market opportunities

Supported go-to-market strategy development

Highlighted investment priorities and risks

Enabled data-driven expansion planning

Technology & Innovation Assessment

Emerging technology trend analysis

Innovation pipeline

Technology adoption readiness assessment

Ecosystem and partnership mapping

Identified future growth areas

Supported innovation roadmap planning

Evaluated commercialization potential

Strengthened strategic partnership decisions

Product Positioning & Competitive Intelligence

Product benchmarking and feature comparison

Pricing and value proposition analysis

Brand perception and customer preference study

Competitor strategy evaluation

Improved product differentiation strategy

Supported pricing optimization

Identified unmet customer needs

Enhanced competitive positioning

Frequently Asked Questions About This Report

The key players in the smart manufacturing market are ABB Ltd., Cisco Systems, Inc., Siemens AG, General Electric, Rockwell Automation Inc., Schneider Electric, Honeywell International Inc., Emerson Electric Co., FANUC Corporation, Mitsubishi Electric Corporation.

Key drivers of the smart manufacturing market include the widespread adoption of Industry 4.0 technologies, IoT, AI, machine learning, and cloud computing, and the growing demand for automation & cost efficiency.

The global smart manufacturing market was estimated at USD 410.7 billion in 2025 and is expected to reach USD 478.9 billion in 2026.

The global smart manufacturing market is expected to grow at a compound annual growth rate of 12.1% from 2026 to 2033 and to reach USD 1,063.2 billion by 2033.

Asia Pacific dominated with 46.6% revenue share in 2025. The region’s strong manufacturing base, particularly in electronics, automotive, and consumer goods, has led to the adoption of robotics and digitalization to streamline operations, enhance efficiency, and reduce costs.

The software segment accounted for the largest share of 50.8% in 2025 and is expected to continue its dominance over the forecast period.

Latin America is the fastest-growing region over the forecast period.

The DCS segment led with a 16.1% revenue share in 2025, while 3D printing is the fastest growing segment.

Automotive held the largest revenue share in 2025, while Renewable Energy is the fastest growing segment.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.