- Home

- »

- Advanced Interior Materials

- »

-

Technical Ceramics Market Size & Share Report, 2026-2033GVR Report cover

![Technical Ceramics Market (2026 - 2033)Report]()

Technical Ceramics Market (2026 - 2033)

Size, Share & Trends Analysis Report By Material (Alumina, Titanate, Zirconate), By Product (Monolithic, Ceramic Coatings), By Application, By End Use, By Region, And Segment Forecasts

Market Size, 2025

$108.6BMarket Estimate, 2026

$113.8BMarket Forecast, 2033

$179.9BCAGR, 2026–2033

6.8%Technical Ceramics Market Summary

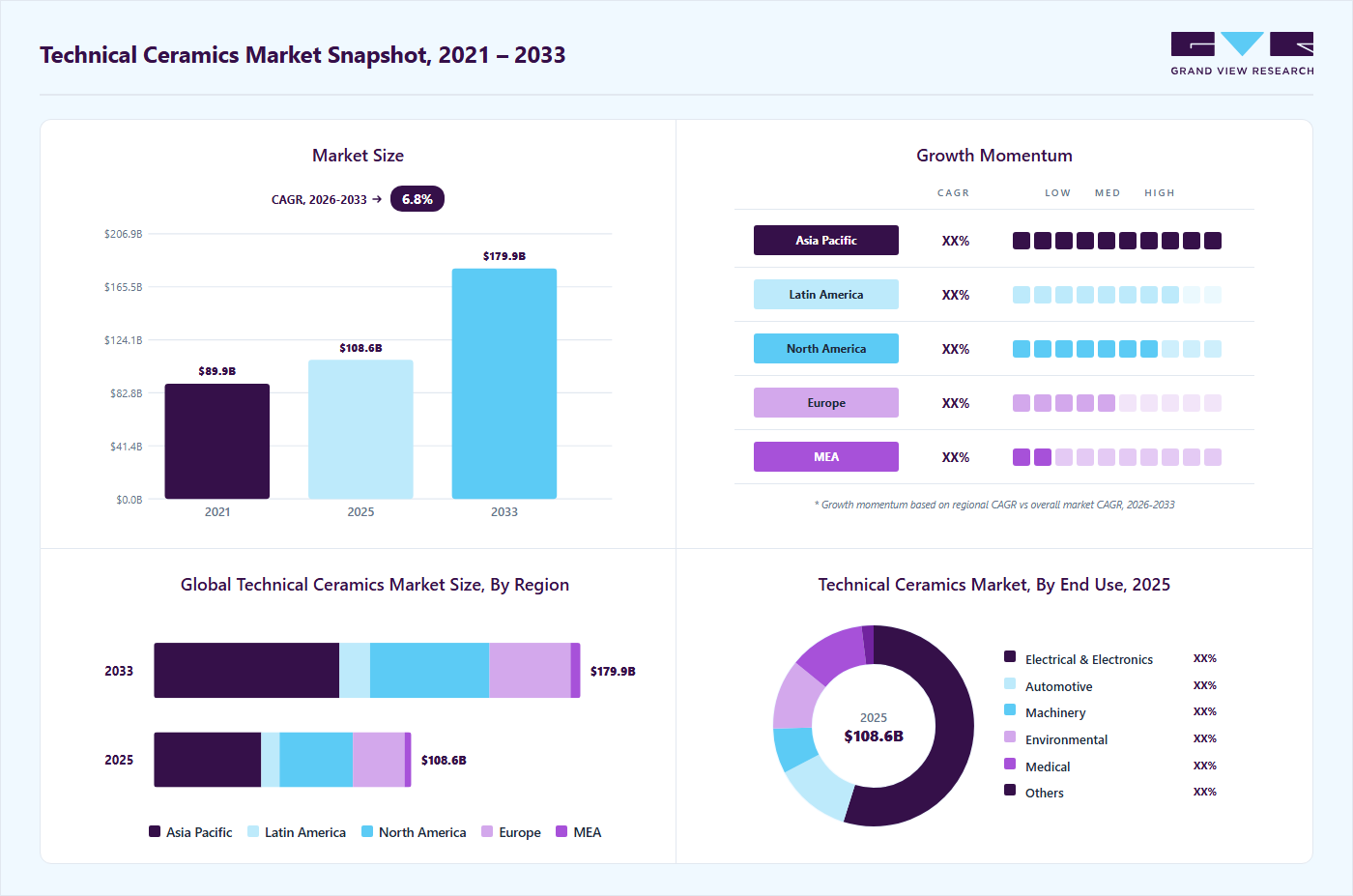

The global technical ceramics market size was valued at USD 108.6 billion in 2025 and is projected to grow from USD 113.8 billion in 2026 to USD 179.9 billion by 2033, at a CAGR of 6.8% from 2026 to 2033. The market in Asia Pacific dominated with a revenue share of 41.7% in 2025. Market growth is primarily driven by increasing demand from the electrical and electronics sector, where technical ceramics are extensively used in components such as substrates, capacitors, and insulators, along with the rapid expansion of the automotive industry, particularly electric vehicles (EVs), which require high-performance materials with superior thermal stability and wear resistance.

Key Market Trends & Insights

- By material: Titanate ceramics are projected to witness the highest growth, with an expected CAGR of 8.3% during 2026-2033.

- By product type: Monolithic ceramics held a dominant position in 2025, contributing around 83.6% of overall market revenue.

Regional Highlights

- Largest regional market: Asia Pacific (41.7% revenue share, 2025)

- Fastest-growing regional market: (highest CAGR, 2026-2033)

- By country: The China held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 108.6 Billion

- Estimated market size in 2026: USD 113.8 Billion

- Projected market size by 2033: USD 179.9 Billion

- CAGR (2026-2033): 6.8%

Sustainability considerations and shifting material preferences are increasingly influencing the technical ceramics market, as industries move toward more energy-efficient, durable, and environmentally resilient materials. Technical ceramics offer long service life, high corrosion resistance, and reduced maintenance requirements, contributing to lower lifecycle costs and less material waste than conventional metals and polymers. Additionally, their role in enabling clean energy technologies, such as components in renewable energy systems, electric vehicles, and energy-efficient electronics, is strengthening their adoption. Regulatory pressure and corporate sustainability goals are further accelerating the preference for technical ceramics in applications where performance and environmental impact are both critical.")

Technological advances are playing a pivotal role in expanding the application scope of technical ceramics, particularly through innovations in material engineering and manufacturing processes. Developments such as ceramic matrix composites (CMCs), additive manufacturing, and nano-ceramics are enhancing mechanical strength, thermal shock resistance, and design flexibility. These innovations are enabling the use of technical ceramics in high-performance applications across aerospace, defense, electronics, and healthcare sectors. Moreover, ongoing R&D efforts to improve cost efficiency and scalability are expected to further drive market penetration and unlock new growth opportunities.

Drivers, Opportunities & Restraints

The technical ceramics market is primarily driven by strong demand from the electronics, automotive, and healthcare sectors, supported by ongoing industrial expansions. For instance, in March 2025, TSMC announced continued capacity expansion for advanced semiconductor nodes, increasing the demand for high-purity ceramic components used in wafer processing and equipment. Additionally, in February 2025, Tesla, Inc. reported higher EV production targets for 2025, driving the need for technical ceramics in power electronics, sensors, and thermal management systems. These developments highlight the growing reliance on technical ceramics in high-performance applications.

Significant opportunities are emerging from advancements in aerospace materials and clean energy technologies. In April 2025, GE Aerospace expanded the use of ceramic matrix composites (CMCs) in jet engine components to enhance fuel efficiency and reduce emissions, reinforcing demand for high-performance ceramics. Furthermore, in January 2026, Bloom Energy announced progress in solid oxide fuel cell (SOFC) deployments, where ceramic materials play a critical role in energy conversion systems. These developments indicate strong future growth potential for technical ceramics in next-generation energy and aerospace applications.

Despite strong demand, the market faces constraints due to high production costs and volatile raw material prices. In June 2025, several global alumina producers reported price increases due to rising energy costs and supply chain disruptions, directly impacting ceramic manufacturing costs. Additionally, in September 2025, CoorsTek, Inc. highlighted ongoing challenges related to precision machining and the processing complexity of technical ceramics, which increase production lead times and limit scalability. These factors continue to restrain adoption, particularly in cost-sensitive industries.

Material Insights

Alumina ceramics accounted for the largest market share in 2025, primarily due to their cost-effectiveness, high mechanical strength, and broad applicability across electrical, electronic, and industrial applications. These ceramics are extensively used in substrates, insulators, wear-resistant parts, and cutting tools, making them a preferred material across multiple industries. Their availability, proven performance, and relatively lower cost compared to other advanced ceramics continue to support their dominant position in the market.

Titanate ceramics are anticipated to register the highest CAGR during the forecast period, driven by their superior dielectric properties and increasing usage in electronic components such as capacitors, sensors, and actuators. The rapid expansion of the electronics and telecommunications industries, along with the growing demand for miniaturized and high-performance devices, is significantly boosting the adoption of titanate-based ceramics. Additionally, advancements in material engineering are further enhancing their functionality, supporting faster growth.

Product Insights

Monolithic ceramics held the largest market share in 2025, owing to their extensive use across a wide range of applications, including industrial machinery, electrical components, and structural parts. These ceramics are valued for their high strength, thermal stability, and resistance to wear and corrosion, making them suitable for demanding environments. Their simpler manufacturing process compared to that of composite ceramics also contributes to their widespread adoption.

Ceramic matrix composites are expected to witness the highest growth rate over the forecast period, driven by their superior performance characteristics, including enhanced fracture toughness, lightweight properties, and high-temperature resistance. These materials are increasingly adopted in aerospace, defense, and energy applications, particularly in turbine engines and thermal protection systems. Continuous advancements in manufacturing technologies and increasing demand for fuel-efficient systems are further accelerating their growth.

Application Insights

Electronic devices dominated the application segment in 2025, supported by the extensive use of technical ceramics in components such as substrates, capacitors, insulators, and semiconductor parts. The rapid growth of the global electronics industry, coupled with increasing demand for consumer electronics, data centers, and semiconductor devices, has significantly contributed to this dominance. Technical ceramics play a critical role in ensuring reliability and performance in high-temperature and high-frequency environments.

Bioceramics are projected to grow at the highest CAGR during the forecast period, driven by increasing demand in the healthcare sector for applications such as dental implants, bone grafts, and orthopedic devices. The aging global population, rising healthcare expenditure, and growing preference for advanced medical treatments are key factors supporting this growth. Additionally, continuous innovations in bio-compatible ceramic materials are expanding their application scope in regenerative medicine and implant technologies.

End Use Insights

The electrical & electronics segment accounted for the largest market share in 2025, driven by the widespread use of technical ceramics in electronic components, circuit boards, and insulation systems. The ongoing expansion of semiconductor manufacturing, the increasing adoption of smart devices, and the growth of communication technologies are key factors driving this segment’s dominance. Technical ceramics are essential in maintaining performance, durability, and efficiency in modern electronic systems.

The environmental segment is expected to register the highest CAGR during the forecast period, supported by increasing focus on sustainability and pollution control. Technical ceramics are widely used in applications such as filtration systems, catalyst supports, and emission control technologies across industries such as automotive and energy. Growing environmental regulations and rising investments in clean energy and waste management solutions are further driving the adoption of technical ceramics in this segment.

Regional Insights

The North American market is driven by strong demand from the aerospace, defense, electronics, and healthcare industries, supported by advanced manufacturing capabilities and high R&D investments. The region benefits from the presence of key players such as CoorsTek, Inc., and 3M, as well as the increasing adoption of ceramic matrix composites in aircraft engines and defense systems. Additionally, the expansion of semiconductor manufacturing and medical device production is further supporting market growth, particularly in high-performance and precision applications.

U.S. Technical Ceramics Market Trends

The U.S. represents the largest market within North America, driven by technological innovation and strong end-use industries such as aerospace, automotive, and electronics. Increasing investments in semiconductor manufacturing, supported by government initiatives like the CHIPS Act, are boosting demand for technical ceramics used in fabrication equipment and electronic components. Companies such as CeramTec GmbH and Morgan Advanced Materials play a significant role in supplying technical ceramics solutions across industries, while the growing EV market is further accelerating demand.

Europe Technical Ceramics Market Trends

Europe’s market is characterized by strong demand from automotive, industrial, and renewable energy sectors, supported by stringent environmental regulations and a focus on sustainable materials. The region is home to leading manufacturers such as CeramTec GmbH and Morgan Advanced Materials, which are actively involved in developing high-performance ceramic components for medical, automotive, and energy applications. Additionally, increasing adoption of ceramics in hydrogen energy systems and electric mobility is contributing to steady market growth.

Asia Pacific Technical Ceramics Market Trends

Asia Pacific dominates the market due to its strong manufacturing base, particularly in electronics, automotive, and industrial sectors. Countries such as China, Japan, South Korea, and India are key contributors, with major players like KYOCERA Corporation and Murata Manufacturing Co., Ltd. leading in electronic ceramics production. Rapid industrialization, expanding semiconductor manufacturing, and increasing EV production are key factors driving regional growth, making the Asia Pacific the largest and fastest-growing market.

The China technical ceramics market is expanding rapidly, driven by strong demand from electronics, automotive, energy, and industrial manufacturing sectors. Growth is supported by increasing adoption of advanced materials in applications such as semiconductors, electric vehicles, and high-temperature industrial processes. The market benefits from China’s well-established manufacturing base and ongoing investments in high-performance materials and precision engineering. Domestic players dominate volume production, while continuous advancements in material science are improving product performance and enabling higher-value applications.

Latin America Technical Ceramics Market Trends

The market in Latin America is gradually expanding, driven by growth in industrial manufacturing, mining, and energy sectors. Countries such as Brazil and Mexico are witnessing increasing adoption of technical ceramics in wear-resistant components and industrial applications. While the market remains relatively smaller compared to other regions, rising investments in infrastructure and automotive production are expected to create moderate growth opportunities over the forecast period.

Middle East & Africa Technical Ceramics Market Trends

The Middle East & Africa market is primarily driven by demand from oil & gas, energy, and industrial sectors, where high-performance materials are required to withstand extreme operating conditions. The region is seeing increased adoption of technical ceramics in applications such as catalyst supports, filtration systems, and thermal insulation. Growing investments in industrial diversification and renewable energy projects, particularly in the Middle East, are expected to support gradual market growth.

Key Technical Ceramics Company Insights

Some of the key players operating in the market include 3M, Saint-Gobain, and others.

-

3M, founded in 1902, is a diversified global technology company with a strong presence across North America, Europe, and Asia, offering a wide range of advanced material solutions, including technical ceramics. The company operates through multiple business segments, supplying ceramic-based products for applications in electronics, automotive, aerospace, and industrial sectors. Its portfolio includes ceramic abrasives, fibers, and engineered ceramic components designed for high-performance environments. 3M is recognized for its strong innovation capabilities, extensive R&D infrastructure, and focus on developing advanced materials that enhance durability, efficiency, and performance.

-

Saint-Gobain, established in 1665, is a France-based multinational corporation with a significant presence in advanced materials, including technical ceramics, across Europe, North America, and Asia. The company provides engineered ceramic solutions for applications in industrial processing, mobility, electronics, and energy sectors. Its product portfolio includes ceramic components, refractories, abrasives, and high-performance materials designed for extreme operating conditions. Saint-Gobain is known for its strong global footprint, sustainability-driven innovations, and continuous investment in material science to support high-performance industrial applications.

-

Morgan Advanced Materials, established in 1856, is a UK-based global manufacturer specializing in advanced materials, including technical ceramics, with a strong footprint in Europe, North America, and Asia. The company delivers engineered ceramic solutions for applications in energy, healthcare, electronics, transportation, and industrial sectors. Its product portfolio includes thermal ceramics, carbon electrical products, and high-performance ceramic components. Morgan Advanced Materials is known for its expertise in material science, innovation-driven approach, and ability to deliver customized solutions for high-temperature and electrically demanding applications.

Key Technical Ceramics Companies:

The following key companies have been profiled for this study on the technical ceramics market.

- 3M

- CeramTec GmbH

- CoorsTek Inc.

- Elan Technology

- KYOCERA Corporation

- Morgan Advanced Materials

- Murata Manufacturing Co., Ltd.

- Nishimura Technical Ceramics Co., Ltd.

- Ortech Technical Ceramics

- Saint-Gobain

Recent Development

-

In January 2025, Murata Manufacturing Co., Ltd. announced increased capital expenditure for expanding production of multilayer ceramic capacitors (MLCCs), as outlined in its financial guidance. The investment is aimed at strengthening the supply of automotive electronics and communication infrastructure, which rely heavily on advanced ceramic materials.

-

In April 2025, 3M highlighted continued innovation in advanced materials, including ceramic-based solutions, in its quarterly investor update. The company emphasized growing demand from electronics, aerospace, and industrial sectors, where high-performance ceramic materials are critical for durability and thermal management.

-

In June 2025, Saint-Gobain reported progress in its High-Performance Solutions segment through its official half-year communication, with advanced ceramics contributing to growth in mobility, electronics, and energy applications. The update reflects increasing adoption of engineered ceramic components in high-temperature and precision-driven environments.

Technical Ceramics Market Report Scope

Report Attribute

Details

Market definition

The market size represents the revenue generated from the sale of technical ceramics material across various regions.

Market size in 2025

USD 108.6 billion

Estimated market size in 2026

USD 113.8 billion

Projected market size by 2033

USD 179.9 billion

Growth rate

CAGR of 6.8% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, competitive landscape, growth factors, and trends

Segments covered

Material, Product, Application, End Use, and Region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; China; India; Japan; Brazil; Argentina; Saudi Arabia; UAE; Egypt

Key companies profiled

3M; CeramTec GmbH; CoorsTek Inc.; Elan Technology; KYOCERA Corporation; Morgan Advanced Materials; Murata Manufacturing Co., Ltd.; Nishimura Technical Ceramics Co., Ltd.; Ortech Technical Ceramics; Saint-Gobain

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Technical Ceramics Market Report Segmentation

This report forecasts revenue growth at the country & regional levels and provides an analysis of the industry trends in each of the sub-segments from 2021 to 2033. For the purpose of this study, Grand View Research has segmented the global technical ceramics market report on the basis of material, product, application, end use, and region.

-

Material Outlook (Revenue, USD Million, 2021 - 2033)

-

Alumina

-

Titanate

-

Zirconate

-

Ferrite

-

Aluminum Nitride

-

Silicon Carbide

-

Silicon Nitride

-

-

Product Outlook (Revenue, USD Million, 2021 - 2033)

-

Monolithic

-

Ceramic Coatings

-

Ceramic Matrix Composites (CMCs)

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Electrical Equipment

-

Catalyst Supports

-

Electronic Devices

-

Wear Parts

-

Engine Parts

-

Filters

-

Bioceramics

-

Others

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Electric & Electronics

-

Automotive

-

Machinery

-

Environmental

-

Medical

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

-

Asia Pacific

-

China

-

India

-

Japan

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

Egypt

-

-

Frequently Asked Questions About This Report

The eSourcing held the largest revenue share in 2025.

The cloud held the largest share in 2025.

North America dominated with a 36.9% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

The global technical ceramics market size was valued at USD 108.6 billion in 2025 and is expected to reach USD 113.8 billion in 2026.

The global technical ceramics market is expected to grow at a compound annual growth rate of 6.8% from 2026 to 2033 to reach USD 179.9 billion by 2033.

The monolithic ceramics accounted for the revenue share of 83.6% in 2025.

Key players include 3M, CeramTec GmbH, CoorsTek Inc., Elan Technology, KYOCERA Corporation, Morgan Advanced Materials, Murata Manufacturing Co., Ltd., Nishimura Technical Ceramics Co., Ltd., Ortech Technical Ceramics, among others.

The global technical ceramics market is driven by growing demand from the electronics, automotive, and healthcare sectors, where high-performance materials are essential for durability and efficiency.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.